The Asia Pacific Region - Continental Profile - Western Cape Government

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Continental Profile The Asia Pacific Region

Table of

CONTENTS

ASIA PACIFIC OUTBOUND TOURISM

Unprecedented Growth in the Asia Pacific Region

Asia Pacific’s Interregional Outbound Travel

Tourism Expenditure

Asia Pacific countries leads as Origin Markets

Growth in Asia Pacific’s Socio-economic environment

Tourism Forecast

KEY TOURISM TRENDS IN ASIA PACIFIC

Four Key Trends

Key Growth Markets

China Outbound Market

Halal Tourism Market

1

ASIA PACIFIC OUTBOUND TOURISM TO SOUTH AFRICA

Tourists Arrivals

Purpose of Travel

Asia Pacific Total Foreign Spending

Asia Pacific Travellers Length of Stay

Accommodation Type

Seasonality

Preferred Activities

SOUTH AFRICA TOURISM COMPETITIVENESS INDEX

Competitiveness Index

Tourism Performance Overview

ACTIVATING ASIA PACIFIC TOURISM 2020

Geographic Focus

Target Market Definition

Key Tourism Potentials and Opportunities for Development

Perceived Constraints and Barriers

2

STRATEGIC FOCUS AREAS

Expand Western Cape Experiences

Marketing and Communicating: Reaching the target markets

Quality Service: Human Capacity Building

3

INTRODUCTION

Travel and tourism impacts the global economy significantly and is becoming

one of the largest and fastest growing economic sectors. In 2018, international

tourist arrivals increased by a remarkable 6 percent, recording a total of 1.4

billion. 2018 witnessed the second strongest growth year in international tourism

since 2010 and reached the 1.4. billion mark two years ahead of UNWTO’s long

term projection issued in 2010. This strong momentum can be attributed to a

favourable global economic environment and robust outbound tourism from

major source markets.

Home to over half the world’s population, the Asia Pacific region has undergone

dramatic changes over the past decade, with economic, infrastructure and

technological development fuelling rapid travel market growth. An expanding

middle class and rising disposable income in Asia Pacific markets including

China, India, Indonesia and Malaysia are driving increased travel demand. In

addition to rising domestic travel, a growing share of travellers is venturing

abroad, many for the first time, with China’s large and growing outbound travel

population.

Asia Pacific households now account for one in three global traveling

households, up from one out of four in 2006 (Visa Inc, 2018). Growth could

accelerate even faster as more Asia Pacific households in more cities cross the

4

tipping point into the ranks of the global traveling class, adding an estimated

nearly 90 mil. households by 2025. Accounting for 37% of the world’s

international tourism expenditure, the contribution of Asia and the Pacific to

global tourism warrants attention (UNWTO/GTERC, 2018).

UNPRECEDENTED GROWTH IN THE ASIA PACIFIC REGION

Asia Pacific region can be separated into 4 areas which are North-East Asia,

South Asia, Oceania, and Southeast Asia. The region has played a vital role in

global tourism as an outbound tourism market and demonstrated eight

consecutive years of strong growth in outbound travel since 2009. Visitation out

of Asia and the Pacific comprised 25% of global outbound tourism in 2017,

totalled 335 million tourists and increased 7% from 2016-2017 (almost 60% on

aggregate). This average growth has been maintained between 2010 and 2017,

resulting in an aggregate increase of 63% during this period. Interregional travel

(to other regions) witnessed a strong 10% growth from 2017-2018 indicating a

positive demand for long haul travel.

5

Outbound Tourism by Region of Origin (%)

Source: UNWTO (2018)

Outbound tourism from the region is strongly led by the North-East Asia, primarily

due to the growth of Mainland China. China’s demand for international travel

can be seen in its volume of outbound trips comprising130 million trips abroad in

2017 (total departures including same-day trips, as reported by China), the

majority of which to North-East Asian and South-East Asian destinations.

6

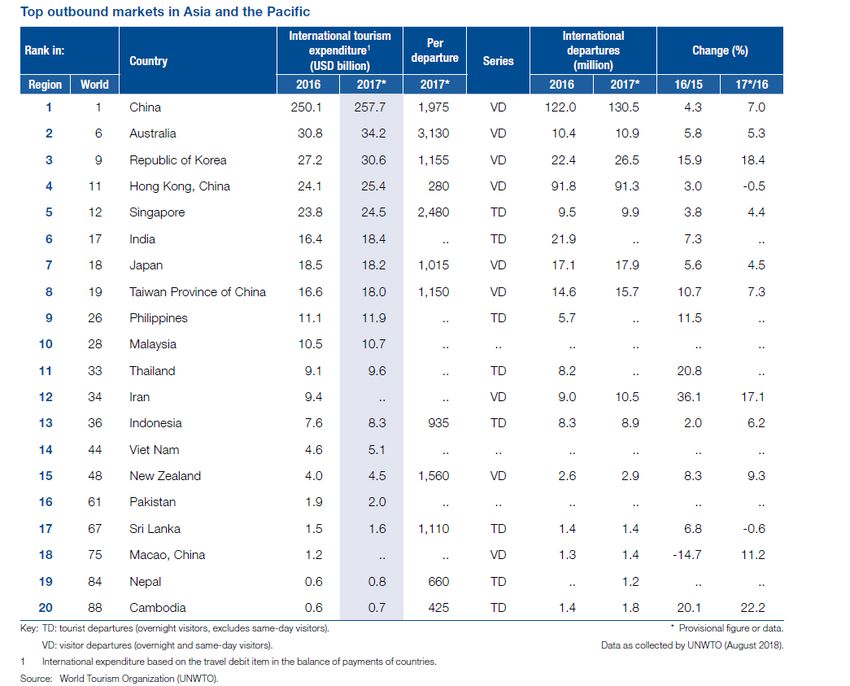

Top Outbound Markets in Asia and the Pacific

Source: UNWTO (2018)

7

Air traffic Demand

IATA reported that Asia Pacific will be the biggest driver of air traffic demand

during the period of 2015-2035, and account for more than 42% of air traffic with

more than half of the new passenger traffic coming from the region (IATA, 2019).

Of the five fastest-growing markets globally in terms of additional passengers per

year over the forecast period, four will be from Asia.

1. China (817 million new passengers for a total of 1.3 billion)

2. US (484 million new passengers for a total of 1.1 billion)

3. India (322 million new passengers for a total of 442 million)

4. Indonesia (135 million new passengers for a total of 242 million)

5. Vietnam (112 million new passengers for a total of 150 million).

ASIA PACIFIC’S INTERREGIONAL OUTBOUND TRAVEL

Europe is the top long-haul destination for travellers from Asia and the Pacific,

accounting for 56% of Asia Pacific’s interregional travel (outside the region) and

13% of Asia Pacific travel overall (measured in arrivals in destinations). The

Americas account for 22% of interregional travel from Asia and the Pacific and

5% of outbound travel overall. The Middle East represents 19% of Asia Pacific’s

interregional tourism and 4% of the region’s total outbound flows. Travel to Africa

is still rather low, accounting for 4% of interregional trips and 1% of Asia Pacific’s

outbound travel (UNWTO/GTERC, 2018).

8

The Europe region is the fastest-growing interregional destination for Asians in the

period 2010-2018 (+9% per year), followed by the Middle East (+8% per year), the

Americas (+7%) and Africa (+6%). The development of economic links between

Asia and the Middle East and with Africa will stimulate both business and leisure

travel beyond Asia and the Pacific (UNWTO/GTERC, 2018).

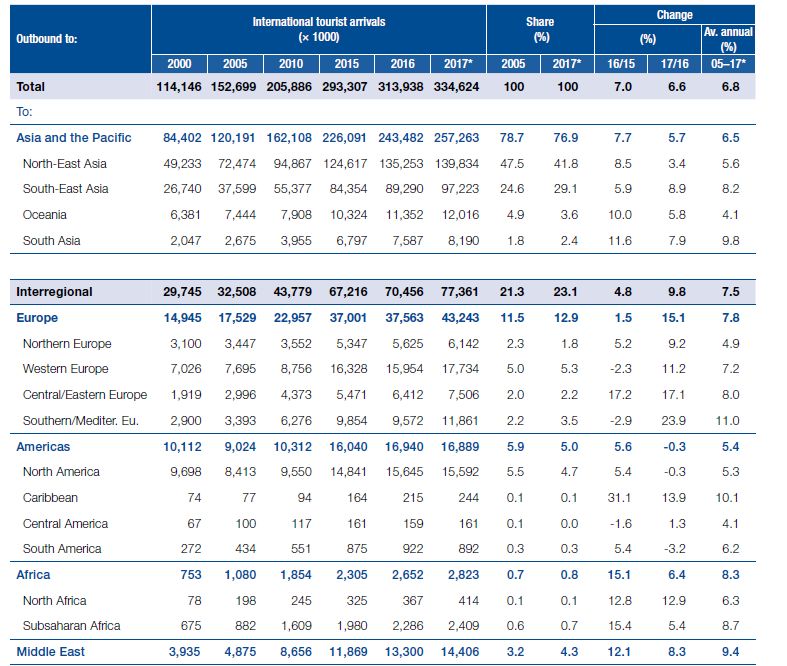

Asia Pacific Outbound Travel to All Regions

Source: UNWTO (2018)

9Growth (% change) in Asia Pacific outbound travel to all regions in the year 2017

and 2018.

Source: UNWTO (2018)

TOURISM EXPENDITURE

Tourism expenditure from the region has also increased substantially,

experiencing double digit growth. Asia Pacific travellers spent USD 502 billion on

international tourism in 2017, some 37% of the world total, up from 24% in 2010

(UNWTO/GTERC, 2018). North-East Asia accounts for 70% of Asia Pacific’s

spending, amounting to USD 352 billion. South- East Asia accounts for 14% of the

10region’s tourism spending, while Oceania and South Asia account for 8% and 7%

respectively.

World’s Top 10 Spenders

Source: UNWTO (2018)

Mainland China represents over half (51%) of the total spending of North-East

Asia, amounting to USD 258 billion. Australia is the 2nd largest tourism spender in

the region, with USD 34 billion recorded in 2017. The Republic of Korea is the 3rd

largest with USD 31 billion spent last year, Hong Kong (China) is 4th with USD 25

billion and Singapore is 5th with USD 24 billion. Combined, these four markets

11represent 23% of international tourism spending in Asia and the Pacific. India,

Japan and Taiwan Province of China are increasingly noted as growing source

markets, totalling about USD 18 billion on international tourism in 2017.

Australia and Singapore recorded a relatively low number of outbound trips, but

spend the most per trip. China is the third biggest spender per trip with an

average of USD 1,975, followed by New Zealand (USD 1,560) and the Republic of

Korea (USD 1,150). These sources markets (with the exception of China) are high-

income economies with relatively small populations, which results in high

spending per trip, and also per capita.

ASIA PACIFIC COUNTRIES LEADS AS ORIGIN MARKETS

Mastercard’s Global Destination Cities Index (2019) which ranks the world’s top

200 cities reported the significance of the Asia Pacific region as a noteworthy

origin market that deserves the attention of both the public and private sectors

at global destinations. It is critical to better understand commerce patterns and

deliver attractive experiences for these eager and affluent travellers from across

the region.

An important finding is that since 2009, mainland China has jumped six places to

be the No. 2 origin country for travellers to the 200 included destinations—

behind only the U.S. In addition, South Korea and Japan are promising origin

12markets fuelling rising travel expenditure and overnight arrivals across the top

200 destinations globally.

Ranking of the Asia Pacific destinations among the top 200 international origin

markets.

Rank Origin Market % Share Contribution To Top 3 global cities of origin

200 Global Destinations in 2018 markets

By

Ovn International Expenditure

Arrivals

2 Mainland China 8.90% 9.40% Bangkok

Seoul

Tokyo

6 South Korea 3.50% 3.30% Osaka

Hokkaido

Tokyo

7 Japan 3.10% 3.40% Taipei

Seoul

Bangkok

10 Australia 2.30% 2.60% Bali

Singapore

New York

11 India 2.00% 2.80% Dubai

Singapore

Makkah

14 Taiwan 1.50% 1.50% Tokyo

Hokkaido

Okinawa

10 Indonesia 1.20% 1.60% Singapore

Kuala Lumpur

Makkah

11 Malaysia 1.10% 1.30% Singapore

Bangkok

13Chennai

Source: Mastercard’s Global Destination Cities Index (2019)

GROWTH IN ASIA PACIFIC’S SOCIO-ECONOMIC ENVIRONMENT

The strong tourism growth in the region can be attributed to several favourable

factors. Rapid economic growth in a region with increasing population, coupled

with rising air connectivity, market openness and travel facilitation have largely

boosted international travel in Asia and the Pacific, both within the region

(intraregional) and to/from other regions (interregional).

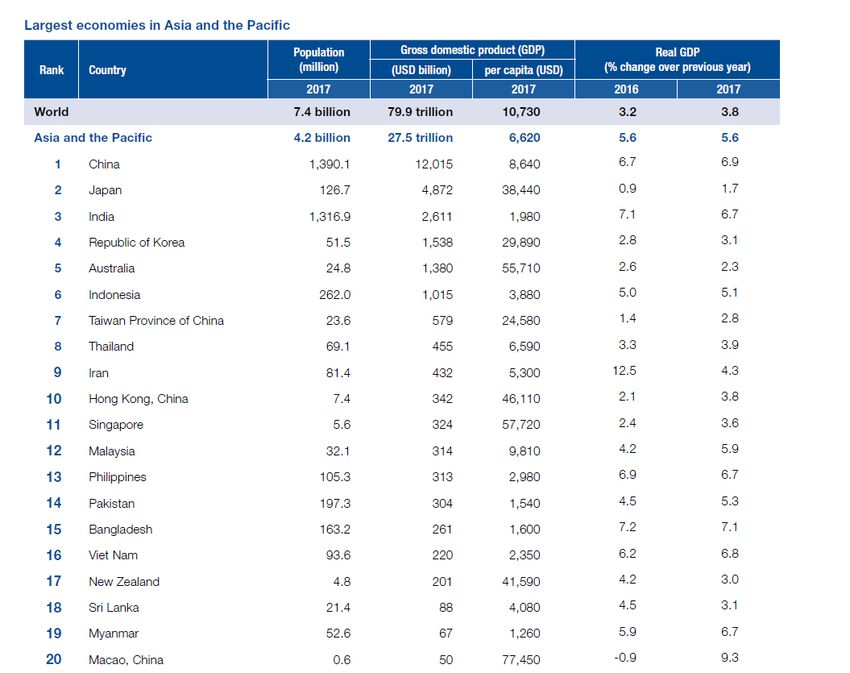

With a population of 4.2 billion inhabitants, Asia Pacific is the world’s largest

region demographically, accounting for more than half of the population on

the planet (56%). In 2017 the GDP of Asia and the Pacific reached USD 27.5

trillion, the highest of all world regions, measured in US dollars. Between 2000 and

2017, Asia experienced the fastest economic growth across world regions,

largely driven by China and India.

Most of Asia and the Pacific’s GDP is generated in North- East Asia (70%),

particularly by China (44%) and Japan (18%), which are Asia’s leading

economies. India (South Asia) contributes 9% to regional GDP, while the

Republic of Korea and Australia (Oceania) account for about 6% and 5%,

respectively.

14Asia Pacific Population and GDP

Source: UNWTO/GTERC (2018)

IMF (2018) Regional Economic Outlook: Asia and Pacific report highlighted Asia

as the world’s most dynamic economic region which will continue to be the

main growth engine of the world. Overall per capita income in Asia still

substantially lags that in the United States and Europe, but in growth terms, the

region is very much at the forefront of the global economy, accounting for more

15than 60 percent of world growth and projected to grow at 5.6 percent in 2018

and 5.4 percent in 2019.

Income levels have surged in Asia and the Pacific since the past decade, with

the region’s per capita GDP more than doubling from USD 3,170 in 2005 to USD

6,620 in 2017 an increase of 109%. By subregion, South Asia (+145%) and South-

East Asia (+144%) recorded the highest growth. North-East Asia (+115%) also saw

its per capita GDP more than double. By subregion, South Asia (+145%) and

South-East Asia (+144%) recorded the highest growth. North-East Asia (+115%)

also saw its per capita GDP more than double. Macao (China) has the highest

GDP per capita in Asia and the Pacific, at USD 77,450, followed by Singapore

(USD 57,700) and Australia (USD 55,700).

16Source: Statista (2019)

In Asia Pacific, as in many travel markets worldwide, total travel market growth is

outpacing overall economic gains. With the exception of South Korea and Hong

Kong, Asia Pacific travel markets are expanding faster than GDP on a local

currency basis. In Malaysia, for example, travel gross bookings rose a projected

9.7% in 2018, compared to GDP growth of 4.7%. In China, the region’s largest

individual travel market by a wide margin, travel gross bookings jumped 9.7%,

versus GDP gains of 6.6% (PhocusWright, 2019).

17APAC Gross Domestic Product and Total Travel Market, Annual Change (%,

Local Currencies) by Market, 2018

Source: Phocuswright Inc (2019)

Visa Inc (2018) reported a similar finding that outbound travel demand is

outpacing income growth throughout much of the Asia Pacific. Measured by

travellers’ spending abroad, demand in 12 of the major Asia Pacific economies

has grown on average twice as fast in constant dollars and prices over the last

decade as real economic growth, which is often viewed as a proxy for income

growth. For instance, outbound travel demand in China, the regional leader,

rose 22 percent per year from 2006 to 2016, compared with only 9 percent per

year growth in real GDP. Trends in outbound travel from Southeast Asia are also

18encouraging, with growth in outbound travel significantly exceeding real

economic growth in the Philippines, Malaysia and Thailand.

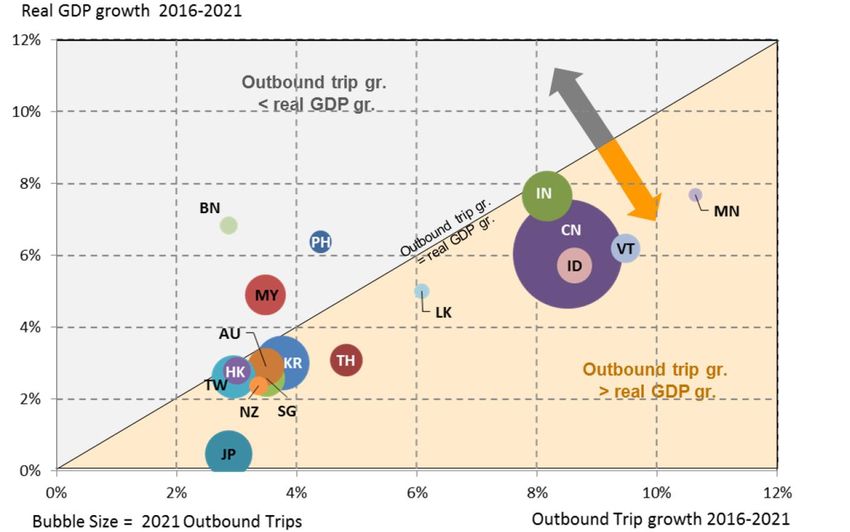

Mastercard Insights (2016) studied the regional outlook of outbound travel from

2016-2021 of 17 tourism markets in Asia Pacific and reported that outbound

travel is generally growing faster than real GDP in most of these destinations

except in the case of Bangladesh, Philippines and Malaysia. Myanmar is the

fastest growing outbound market at 10.6 percent over the forecast period,

followed by Vietnam (9.5 percent) Indonesia (8.6 percent), China (8.5 percent)

and India (8.2 percent). The fastest growing developed markets are South Korea

at 3.8 percent, followed closely by Singapore, Australia, and New Zealand, all of

which are projected to grow by about 3.5 percent over the forecast period.

Interestingly, the three growth markets Singapore, Taiwan and Hong Kong, are

also the smallest in geographic size among the 14 markets covered, but the

limited competition from domestic tourism destinations adds to the overall size of

international tourism.

The chart below locates the positions of each of the 17 Asia Pacific markets in

the two-dimensional space combining real GDP growth rates vertical axis) and

the growth rates of outbound travel (horizontal axis). The chart also suggests that

the outbound travel growth tends to be higher than real GDP growth (as

indicated by points further below the diagonal line) for the developing markets

of Myanmar, Vietnam, Indonesia, Thailand, and China compared to the

19developed markets (excluding Japan) which tend to have outbound growth

much closer to the forecasted real GDP growth (as indicated by points hugging

or close to the diagonal line).

Outbound travel growth versus Real GDP growth

Source: Mastercard Insights (2016)

20TOURISM FORECAST

According to the forecast report Tourism Towards 2030 (UNWTO, 2018), the

number of international tourist arrivals worldwide will increase by an average of

3.3% a year over the period 2010 to 2030. At the projected rate of growth,

international tourist arrivals worldwide are forecast to reach 1.4 billion by 2020

and 1.8 billion by 2030.

Collectively, outbound travel from Asia Pacific is expected to grow by an

annual rate of 6 percent over the forecast period of 2016-2021 (Mastercard,

2017). China is projected to be the largest outbound travel market by 2021,

(excluding trips to Hong Kong and Macau), followed by South Korea and India.

At a projected 103.4 million trips in 2021, outbound China travel will be four to

five times that of South Korea and India, and will constitute almost 40 percent of

all Asia Pacific outbound travel by 2021.

Emerging Asia Pacific destinations currently records about 1.5 times more

outbound trips than Developed Asia Pacific destinations and will grow more

than twice as fast as Developed Asia Pacific (7.6 percent versus 3.3 percent)

over the forecast period of 2016-2021.

Given the dynamics around international travel, Asia Pacific travel could

accelerate even faster than its current pace as more cities reach the necessary

size to support mass tourism. Although, currently, travellers within Asia Pacific

residents skew more heavily to short-haul and regional cross-border travel. as the

21level of income and affluence rises in the rapidly developing Asia, more and

more of its cities will likely grow in importance for outbound cross border tourism.

In China alone, the number of cities reaching the tipping point in cross-border

tourism is likely to double by 2025—adding around 80 million more households to

the global traveling class (Visa Inc. 2018).

Asia Pacific Outbound Trips Forecast: 2016-2021

Source: Mastercard (2016)

22KEY TOURISM TRENDS IN ASIA PACIFIC

The potential for outbound tourism growth from the Asia Pacific region is

tremendous. The continued rise of the middle class, increased market openness,

air connectivity, and travel facilitation are expected to fuel growth. Thus, it is

important for the industry stakeholders to keep up-to-date with the key drivers

impacting tourism growth, with the following being of particular influence and

impact.

The dominance of China:

Chinese tourists are already the world’s most powerful single source of demand,

yet its potential is far greater, as only an estimated 9 percent of the Chinese

population have currently been issued passports. China’s National Immigration

Administration revealed that for the first half of 2018, a total of 164.16 million

Chinese residents applied for their passports for private purposes, a 21% increase

from the previous year. 160 million, that’s half the size of America’s population

and 3 times the size of UK’s population according to the World Bank. The industry

expects 200 million Chinese to travel abroad in a few years’ time. The growth of

this market and its development potential will continue generating tremendous

business opportunities for tourism destinations, local tourism suppliers and service

providers.

Emerging India. The planet’s second-fastest-growing outbound market is steered

by similar socio-economic drivers as China, but garners less global face-time.

23Around 22 million Indians travelled overseas in 2017 spending approximately

USD19 billion, and the UNWTO has predicted Indian outbound travellers will total

50 million in 2020, contributing USD28 billion in expenditure. The average

propensity to spend of Indian holidaymakers is impressive, the LCC sector is

expanding and thriving outbound niches range from destination weddings to

extended family travel and MICE.

Asian Millennial Travellers

Millennials represent more than 45 percent of Asia Pacific’s population and 60

percent of the world’s millennials expected to live in Asia by 2020 and more

than one-third of the Asian millennial travellers will originate China or India

(Amaedus, 2017). With these millennials entering their peak earning and

spending years, with an estimated spending of $340 billion on international

travel by 2020, it’s not a market segment that destinations can afford to ignore.

Within our key source markets in the Asia Pacific, markets with high proportions

of millennials amongst its total leisure outbound travellers include the Philippines,

China, India, Indonesia and South Korea (Euromonitor International, 2014).

More so than the generations that have come before them, millennials are

embracing new technology, experiences, and ways of traveling. Millennial

travellers travel to take a break from their daily life while broadening their

horizons. They seek authentic experiences that allow them to get a taste of the

local culture and are more open to novel experiences compared to other

24segments. These travellers value autonomy over travel experience and being

extremely savvy with technology, they thrive on being connected and having

information at their fingertips.

Technological (R)Evolution

The rapid development of technology is one of the key factors that drive the

development of tourism industry. Worldwide, rapid adoption of mobile devices

has changed the way travellers’ research, shop and book travel and profoundly

altered how travellers’ access information while in destination. Nowhere is this

shift more evident than in Asia Pacific.

In 2019, Phocuswright projected that 55% of online travel bookings in the APAC

region will be made via a mobile device. By comparison, mobile share of the

online market will be just 25% in the U.S. and 30% in Europe. In a smartphone

saturated Asia pacific region, technology is largely shaping the travel

experiences of the outbound travellers from this region. China is the key driver of

APAC’s mobile dominance, with mobile in 2019 to account for nearly 80% of

China’s online travel gross bookings. Asia Pacific boasts three of the top five

mobile travel markets worldwide: India and Japan will each have projected

mobile travel penetration of 37% in 2019.

To stay competitive, product and service providers must adapt to and

implement new technologies to ensure traveller satisfaction. The influence of

25technology can be analysed under 3 components which are payment

methods, messaging systems, and digital advertisements.

Payment method

As mentioned, Chinese travellers’ have become the primary source for global

tourism industry. Nielson (2017) reported that although Chinese travellers’ will still

heavily rely on cash payment and cashless payment (bank cards), mobile

payment can help to increase their satisfaction during overseas travel.

Messaging system with extended functionality

The messaging system has become more critical as a tool to connect people

and for customer service, content-sharing, and information (Ho, 2018). The most

significant example is WeChat. Service and product providers are required to

integrate these new systems and their functionalities in their operation to stay

competitive. While traveller preferences vary by market, global social networks,

including Facebook, Twitter and Instagram, are popular in Asia Pacific, as well

as Asia Pacific -grown players like Weibo (China) and Line (Japan). Top

messaging platforms include Facebook Messenger, WhatsApp and China’s

super app WeChat.

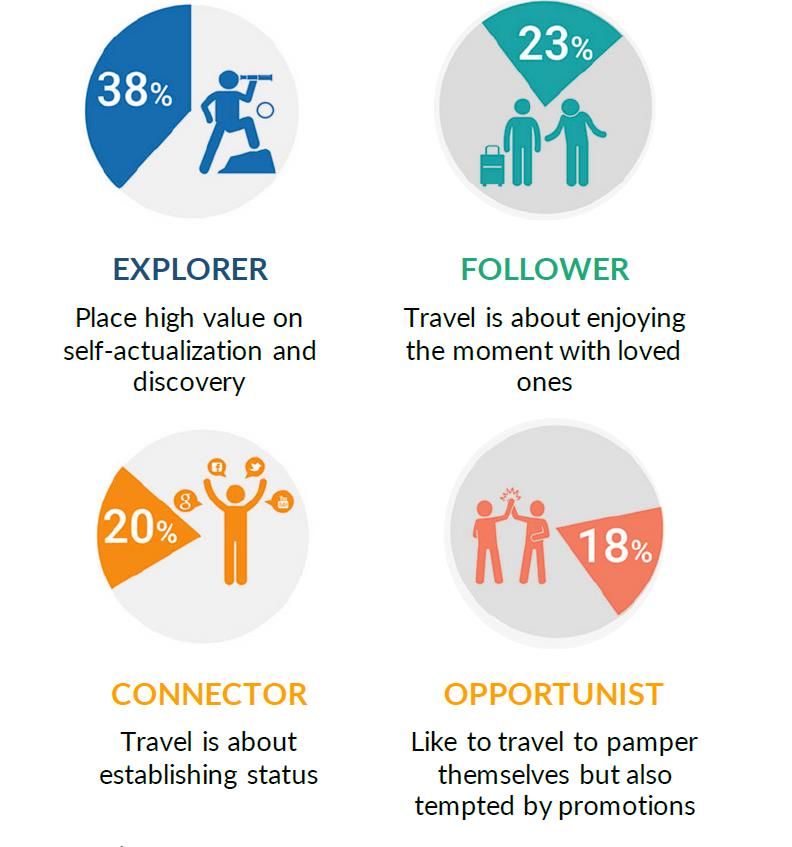

Travel as a form of self-expression and self-actualization

Sabre (2017) published a study detailing four new types of travellers emerging in

Asia Pacific. The largest share of travellers falls into the category of ‘Explorers’,

26who place high value on discovery and self-actualisation. Travel is about

helping them grow as individuals. A one-stop approach is no longer valid in the

travel market. With travel becoming an important means of self-expression,

travel products and services need to be more personalized. Furthermore, as

travellers crave new and novel experiences - something that is ‘share-worthy’ -

hotels need to rise to the challenge and go beyond cookie-cutter rooms and

services to surprise and delight guests. Meanwhile, 20 percent of travellers are

‘Connectors’ and 18 percent are ‘Opportunists’, whose travel motivations are

mainly self-expression, self-indulgence, establishing status, and sharing

experiences.

Types of Emerging Travellers in Asia Pacific

Source: Sabre (2017)

27KEY GROWTH MARKETS

1) Chinese Outbound Market

The Chinese tourists have already become the most powerful market segment.

International outbound travel by China’s residents was around 68.7 million in

2016, and is forecasted to grow by an average of 8.5 percent per year to reach

103.4 million trips by 2021. Total outbound trips will grow much faster than total

household growth (8.5 percent versus 0.4 percent) over the forecast period

resulting in a ratio of outbound trips to households that is projected to reach 23.0

percent in 2021 from 15.6 percent in 2016. The disposable income per capita has

increased (Ho, 2018) and outbound travel will be dominated by the fast-growing

middle and higher-income households which together make up 35.7 percent of

all households (Mastercard, 2016). The role of Chinese travellers will continue to

be crucial in generating tremendous business opportunities and considerable

income in the future to tourism service providers.

28(excludes trips to HK and Macau) 2013 2014 2015 2016 2021 2016-2021

CAGR

Outbound trips (mn) 38.8 48.1 61.6 68.7 103.4 8.5%

Households (mn) 435.2 437.5 439.6 441.7 449.7 0.4%

Total outbound trips as % of total 8.9% 11.0% 14.0% 15.6% 23.0%

households

Source: Mastercard (2016)

Chinese travellers’ profile

Nielson (2017) conducted an in-depth study and analysis of current

consumption and payment behaviours of outbound Chinese tourists travelling

overseas. The top three categories of expenses by outbound Chinese tourists are

shopping, hotel accommodations, and dining. Regardless of destination country

or region, Chinese tourists tend to always spend the largest portion of total travel

expenses on shopping. Chinese tourists spent an average of USD 762 per person

towards shopping on their most recent overseas trip, while non-Chinese tourists

averaged USD 486.

The survey showed that to the Chinese travellers, tourist attractions and the

travel experience are more important factors than the costs that might be

incurred. The beauty and uniqueness of the destinations were an important

consideration in addition to the safety of the destination, ease of visa

29procedures and the friendliness of the local communities. Expedia Media

Solution (2017) indicated that the top 3 considerations that influence Chinese

travellers’ decision making before the trip include activities, food experience

and accommodations.

Factors that influence Chinese travellers when traveling overseas

Source: Nielson (2017)

Chinese tourists expressed that they desired to have unique experiences during

their travels, such as visiting historical sites, trying local cuisine, shopping for local

products, and various other unique options. Chinese travellers prefer natural

scenery and theme parks compared to cultural and historical attractions. In

Nielson (2017) study, the Chinese travellers reflect a preference for independent

or semi-independent travel followed by package travel.

TrekkSoft (2019) reported that the modern Chinese traveller wants an

experience of a lifetime. Chinese travellers are searching for experiences that

allow them to “travel like a local”. This shift in travel behaviour shows no signs of

slowing down. Chinese travellers are taking even more “independent” trips

(40%), while others are taking “modular” trips (40%) and only 20% still book

themselves on traditional packaged tours.

30Chinese tourists travel overseas mainly for leisure, such as dining and shopping.

However, there are minor differences in the travel objectives of Chinese

travellers among the various age groups. The millennials tend to be more

adventurous, the post-80s generation is more focused on shopping and

romantic getaways while the post-70s prefer a relaxing travel experience.

According to Travel China Guide, an average trip to countries nearby like

Japan or Thailand averages 6 to 9 days. For trips further from home, to

destinations like Australia, Europe and the United States, an average trip would

be 12.6 days. When it comes to visiting Europe, people tend to visit an average

of two countries per trip (TrekkSoft, 2019).

Globally, Travel China Guide (2018) reports the following to be the top

destinations for Chinese travellers:

1. Thailand

2. Japan

3. Singapore

4. Vietnam

5. Indonesia

6. Malaysia

7. Philippines

8. America

9. South Korea

10. Maldives

31Influence of technology

When it comes to mobile payments, China is leading the way. China is living in

3019 compared to the rest of the world. According to TrekkSoft (2019), by

October 2017, mobile payments grew by 37.8% compared to 2016, totalling USD

12 trillion, 50 times larger than America’s. Chinese travellers favour mobile

payments as it eliminates the risk of carrying cash and of exchange fluctuations.

As of 2018, eMarketer reports that adults in China will spend more time on their

mobile devices (2 hours 39 minutes) than they will watching TV (2 hours and 32

minutes). This is an 11.1% increase compared to 2017, taking up 41.6% of their

daily media time. Consumption of short videos is said to be the key driver of

increased mobile time.

The two dominant service providers for mobile payments are Alipay (54%) and

WeChat Pay (40%). Chinese consumers use their smartphones to scan a simple

QR Code and enter their password to easily make a payment. When travelling,

this habit spills across international borders with 65% of Chinese travellers making

a payment via mobile, compared to just 11% of non-Chinese travellers

(TrekkSoft, 2019). Companies interested in driving more Chinese travel spend are

going along with the trend. Chinese tech leaders are partnering with hotel

brands, retailers, and banks to create data-driven services and changing travel

booking trends and methods. A few examples include:

32• Travel agencies, hotels, and airlines are finding new ways to provide full brand

experience to their customers via WeChat. i.e.: control of hotel room (Caesar

Entertainment), check-in services (China Southern Airline), customer services (Air

France), Loyalty Program (IHG), etc.

• Alipay and WeChat are spreading rapidly throughout the world. The number

of foreign airports, retail stores, hotels, and other service providers accepting

Alipay and WeChat Pay has increased substantially.

Destinations and hotels need to adopt diverse marketing strategies, as well as

using popular Chinese technologies and media channels, to target Chinese

consumers. In addition, it must closely cooperate with Chinese tour operators,

leveraging on their understanding of, and influence in, the local market.

332) HALAL TOURISM

The burgeoning growth of the global Muslim travel population signals an

immense potential for Muslim travel related products and services. According to

the Mastercard-CrescentRating Global Muslim Travel Index 2017 (GMTI 2017),

there were an estimated 121 million Muslim international travellers in 2016, and

this is projected to grow to 156 million by 2020. This market segment has been

acknowledged as the ‘third one billion’ opportunity following the interest in

Indian and Chinese billions (Janmohamed, 2016) and predicted to reach 30% of

the world’s travel population by 2050 (Pew Research Centre, 2017).

Asia and the Pacific is the home to the largest population of Muslims. Of the

world’s 1.6 billion Muslims, an estimated 62% are in Asia, specifically in Indonesia,

(which has the largest number of Islamic adherents in the world with an

approximate 203 million), India, Pakistan, Bangladesh, Iran, China, Malaysia,

Brunei Darussalam, Afghanistan and the Maldives (Pew Research, 2017 ). In

addition, smaller minorities are present in Thailand, Sri Lanka, Philippines,

Cambodia, Singapore and Viet Nam. The growing middle-class of Islamic

countries in Asia and the Pacific with disposable income to travel has led to a

lucrative outbound market of Muslim travellers that has been targeted by many

“non-Muslim” countries in the region.

34FAITH BASED NEEDS OF MUSLIM TRAVELLERS

A total of 9 key faith-based needs that would influence the consumption

behaviour of Muslim travellers which includes (1) Halal Food, (2) Prayer Facilities,

(3) Water-friendly Washrooms, (4) No Islamophobia, (5) Social Causes, (6)

Ramadhan Services, (7) Local Muslim Experiences, (8) Recreational Spaces with

Privacy and (9) No Non-Halal Activities (Mastercard-CrescentRating, 2019).

These factors are grouped under 3 different sections (1) need to have, (2) good

to have and (3) nice to have.

• Need to have

Halal food is the most important factor that a Muslim traveller needs when

travelling. Restaurants that can be easily identified as Halal is the mostly wanted

by Muslims. Next, the availability of prayer facilities with prayer rooms, qibla

directions and ablution friendly washrooms are needed by Muslim travellers.

Thirdly, water-friendly washrooms as water plays an important role in purity and

cleanliness for Muslims. These facilities have become easier now that there is a

widespread availability of hand showers, bidets and Japanese-style toilets.

With increasing hate crimes seen around the world, safety has become a

primary concern for Muslims travellers. In addition, Islamophobic sentiments has

been lingering in some regions and Muslim travellers are not encouraged to

travel to destinations that are perceived to be unwelcoming. Also, with

35increasing hate crimes around the world, safety and security has become a

primary concern for Muslim travellers (Mastercard-CrescentRating, 2019).

• Good to have

Good to have services includes Social Causes, Ramadhan Services and local

Muslim Experience. Driven by faith and global trend towards sustainability,

Muslims are becoming more conscious of being socially responsible during their

travels. Social causes include the ability to improve local living conditions,

various green initiatives to perfect the environment and eco-friendly tourism

practices.

Ramadhan services include the provision of Suhour and Iftaar meals, prayer

facilities, services during the Eid among others, Even though Muslims are most

unlikely to be traveling, there are a few Muslims that wishes to be away from

home during the period. Destinations that wishes to attract Muslim travellers

during this period need to be able to accommodate their special needs during

this month.

Local Muslim experiences which refers to experiences unique to the destination

that allows Muslim travellers to connect with their Muslim identity and heritage.

This could include visiting Islamic heritage sites, interacting with local Muslim

communities at a local mosque or experiencing the country with a Muslim tour

guide (Mastercard-CrescentRating, 2019).

36• Nice to have

The nice to have services include: Recreational Spaces with Privacy and no

Non-Halal Activities. Recreational Spaces with Privacy refers to facilities such as

swimming pools and gyms, beaches, spas and beauty salons that provides

privacy for males and females. This is especially important for females as they

need to have appropriate modesty. No Non-Halal Activities are regarded as

nice to have as some Muslims would prefer to avoid facilities and activities that

serve alcohol or staying in gambling resort.

KEY MARKET SEGMENTS

Within the broader Muslim travel market in the region, two key markets have

been given prominence due to their growth potential, namely the Muslim

women travellers and the Muslim millennial travellers (MMT).

Muslim female travellers usually travel with their friends and family to seek for

new and authentic experiences. The Muslim identity and religious beliefs largely

influence the Muslim women′s tourism experiences, lifestyles and travel patterns

and/or behaviors. With sharing their experiences, they hope that it would be an

inspiration to others. They have a stronger influence in planning their trips

whether they are travelling alone, with their family or friends (Mastercard-

CrescentRating, 2018). Muslim female travellers find it important to have gender-

segregated facilities such as swimming pools, gyms, spas or saunas for privacy

37as it would affect them since they are required to have appropriate modesty

(Razzaq, Hall & Prayag, 2016). They would usually travel for leisure or to distress.

The Muslim millennials The Muslim millennials are tech-savvy, self-empowered

and enthusiastic consumers whose identities proudly encompass both faith and

modernity. Muslim millennial travelers are distinct from their previous generations

and other millennial travelers, with a unique set of values, needs and

expectations in their travel consumption and expenditure patterns. They often

spend more time and effort to conduct comprehensive research before making

travel arrangements.

The Muslim millennial travellers mostly travel for leisure and holidays,

experiencing local culture and heritage, and visiting friends and relatives

(Mastercard-CrescentRating, 2017). On average, they travel 2 to 5 times a year,

and are generally cost conscious. When planning for trips, the top 3 factors that

would influence them were cost of flights and accommodation, safety and

tourism concerns and availability of Halal food (Mastercard-CrescentRating,

2017).

For Muslim millennial travellers, they prioritise affordability, location and free Wi-Fi

when selecting an accommodation. Specifically, for Muslim-friendly services

and facilities, they value availability and proximity of Halal food options,

mosques and prayer facilities and water-friendly facilities. When booking for

flights, ticket pricing, safety records, baggage allowances and Halal meal

38choices were important considerations. They also preferred Halal assured and

certified places but would not mind dining in a seafood-only or vegetarian-only

restaurant. Finally, they love to share their photos during their travels on social

media pages such as Instagram, Facebook and Snapchat (Mastercard-

CrescentRating, 2017).

RANKING OF SOUTH AFRICA AS A MUSLIM FRIENDLY DESTINATION

The global Muslim population is diverse and geographically distributed into

segments in Muslim majority destinations as sizeable minorities in other

destinations. According to the Regional Analysis of GMTI 2017 Scores, Africa is

the third best region that is friendly for Muslim travellers (Mastercard-

CrescentRating, 2017) reflecting the regions concerted efforts in adapting and

improving their services to attract the Muslim travel market.

South Africa is one of the destinations that is ranked well in the Global Muslim

Tourism Index 2019. South Africa is ranked 29 under the GMTI global ranking and

6 under the top 10 Non-OIC destinations. It is evident that South Africa is

becoming more friendly for Muslim tourists. South Africa is also ranked under the

top 10 destinations in terms of ease of communications where there are

outreach initiatives that includes public education, media outreach and Muslim

visitor guidebooks.

Cape Town has a rich Muslim history and heritage, with the Cape Malay

Muslim’s making up around a quarter of the city’s population. It was ranked as

39the 4th best travel destination for Muslim travellers in the 2017 Global Muslim

Travel Index.

Key Drivers in the Muslim Travel Market in South Africa

• Mosques, kramats, and prayer rooms

The Cape Town city offers prayer rooms in major centres and a large number of

mosques found across the province. It is also the home to the oldest mosque in

South Africa, dating back an impressive 200 years. There are also a number of

Kramats, known collectively as the Circle of Saints or the Ring of Kramats.

• Muslim Community

Cape Town is the place for South Africa’s first Muslim settlers and the Cape

Malay Muslim’s make up around a quarter of the city’s population.

• Culture and Heritage

The Bo-Kaap area in Cape Town, which was formally known as the Malay

quarter, is still home for many Muslims. In the area that is popular for its rainbow-

like houses, there are more than seven mosques. The Bo-Kaap museum

highlights the early contribution of Muslim settlers to Cape Town and a major

attraction to Muslim travellers.

Halal food options

Cape Town, renowned for its’ gastronomy, is the food capital of the Western

Cape. Recently, halal restaurants serving these traditional dishes have been

40increasing, making it possible for Muslim travellers to enjoy local food and

observe their faith-based needs.

Muslim friendly hotels

Major chains, such as Hilton, One and Only, have introduced Muslim-friendly rooms.

These rooms include a prayer mat and the Qur’an. The rooms are also free of alcoholic

drinks. All the food that is prepared in the kitchen is made without alcohol and pork. The

Hilton Cape Town City Centre kitchen is completely ‘halal’.

KEY DRIVERS IN THE MUSLIM TRAVEL MARKET IN SOUTH AFRICA

With the increasing growth in the Muslim Travel Market, more businesses and

destinations are now entering the industry to better cater to the needs of the

Muslim travellers by adapting their products and services. The increase in Muslim-

friendly destinations creates a virtuous cycle, creating more opportunities for

Muslim to travel.

IMPLICATIONS FOR SOUTH AFRICA

• Market Outreach

As South Africa is ranked under the top 10 destinations in terms of

communication, South Africa has outreach initiatives which includes public

education, media outreach and Muslim visitor guidebooks. However, to attract

more international clientele, Western Cape could leverage on these initiatives

41as well as use the right channels and the right language medium (e.g. English,

Arabic and Malay) to reach the target market in the Asia Pacific region. A

concerted effort needs to be made to build online content to attract and

improve its overall global Halal destination branding (Mastercard-

CrescentRating, 2018)

• Muslim Visitors Guides (MVG)

More travel information, recommendations and tips for Muslim visitors should be

curated and organised into province-specific Muslim Visitors Guides (MVG).

Besides publishing it in English, the MVG should also be made available in Malay

and Arabic, as these are among the common languages spoken among the

Muslim population (Mastercard-CrescentRating, 2018)

• Halal Tourism Stakeholder Workshops

Western Cape could organise more Halal Tourism workshops to educate tourism

stakeholders with varying degrees. Workshops and discussions should be carried

out for better improvement of the Western Cape’s halal positioning

(Mastercard-CrescentRating, 2018)

• Language courses for tour guides and hospitality workers

English, Malay and Arabic are some of the most widely spoken languages

among the Muslim population in the region. English, Malay and Arabic

language courses and training should be conducted for tour guides and

42employees in the hospitality and tourism sector to better serve the Muslim

travellers

• Improve Wi-Fi Network Coverage

Travellers perceive staying connected as being of high importance when

travelling as it allows them to navigate their travels, search for information and

book tourist services such as lodging, transportation and activities and even

sharing of their travel experiences on their social media platforms to their

personal network. Therefore, improving Wi-Fi network coverage and introducing

Wi-Fi hotspot is important and this is not just limited to airports but other public

areas such as convenient stores, restaurants, hotels and malls (Mastercard-

CrescentRating, 2018)

• Enabling Climate

With the huge potential of Halal Tourism, the Western Cape province should

develop an enabling climate for start-ups and innovation for Halal-related

services to flourish. Many services in the hospitality sector today have been

disrupted by the proliferation of digital technologies. By enabling a vibrant

environment for start-ups, Halal Tourism services and products will be able to

integrate latest technologies and business models (Mastercard-CrescentRating,

2018.

• Championing Sustainability and Community Initiatives

43With its ready beautiful locations that highlight the wonders of nature, Western

Cape could package services around travel themes that promote sustainability

and the care of the environment. This can further attract the Muslim millennials

who are attracted to serving Islam’s message of preserving the environment

while enjoying their travel experiences and travellers in general who value

sustainable tourism.

• Position Halal Benefits for All Guests

Although Halal Tourism mainly target Muslim travellers, the concept can also

have a universal appeal for non-Muslims due to numerous benefits such as

peace and security, family-friendly environments and water-friendly services.

The non-alcoholic nature of some Halal hotels and restaurants can also attract

families who are looking for an overall environment which they perceive to be

family-friendly (Mastercard-CrescentRating, 2018)

• Halal Certification and Rating

Halal certification and rating is necessary as it provides assurance, diminishes

possible scepticism and instils trust and confidence in Muslim consumers

(Mastercard-CrescentRating, 2018). As such, such Halal assurance will also be

valued by Muslim travellers as they look for their idea hotels and restaurants.

44Following this trend for standardisation, global Halal assurance and rating

schemes such as Crescentrating will also assist the country in obtaining better

acceptance from guests around the world.

• Increase in Global Service and Governance Standard

The drive to develop the tourism space represents an opportunity for South

Africa to further strengthen its level of hospitality services and governance

standards (Mastercard-CrescentRating, 2018). Beyond infrastructure and skills

development, adequate and integrated Halal assurance across its service value

chains which communicate both permissibility and high quality is key to

attracting both Muslim and non-Muslim travellers to its destinations. Hotel staff

should be trained and educated about Muslim travellers’ values and teachings

to be able to cater to halal conscious tourists in accordance to Islamic principles

(Mastercard-CrescentRating, 2018). Gender-separated facilities such as

gymnasiums, spas and family entertainment will further enhance its offering for

this market segment.

• Differentiated Destination Strategies

Western Cape can capitalise on its diverse regions to cater to a variety of

Muslim travellers who may have different travelling profiles (Mastercard-

CrescentRating, 2018). Muslim millennials who may be looking for more

authentic experiences can savour its many off beaten tracks while still

connected via WIFI to share their experiences, whereas family travellers may be

45greeted with more warmth and developed service-oriented facilities at resorts.

These differentiated activations of destination-spaces can attract a wider

variety of Muslim travellers from around the world and further improve the

country-branding of Western Cape as a safe and vibrant destination for all

(Mastercard-CrescentRating, 2018).

• Innovative Tourism Products and Experiences

Western Cape con converge with other Islamic economy sectors and bundle

them into innovative tourism products (Mastercard-CrescentRating, 2018). For

example, the province can include Islamic heritage sites and religious travel

experiences with activities pertaining to culture and heritage in a unique and

innovative travel package (Mastercard-CrescentRating, 2018).

• Enhanced Prayer Spaces and Facilities

For Muslim women, the need for proper ablution facilities is high (Mastercard-

CrescentRating, 2018). Most of the ablution areas at mosques or prayer spaces

are in a public area and there is little privacy for Muslim women who are

covered. By providing proper ablution areas and water-friendly facilities and

thus making it convenient for Muslim travellers, it can add value to their travel

experience.

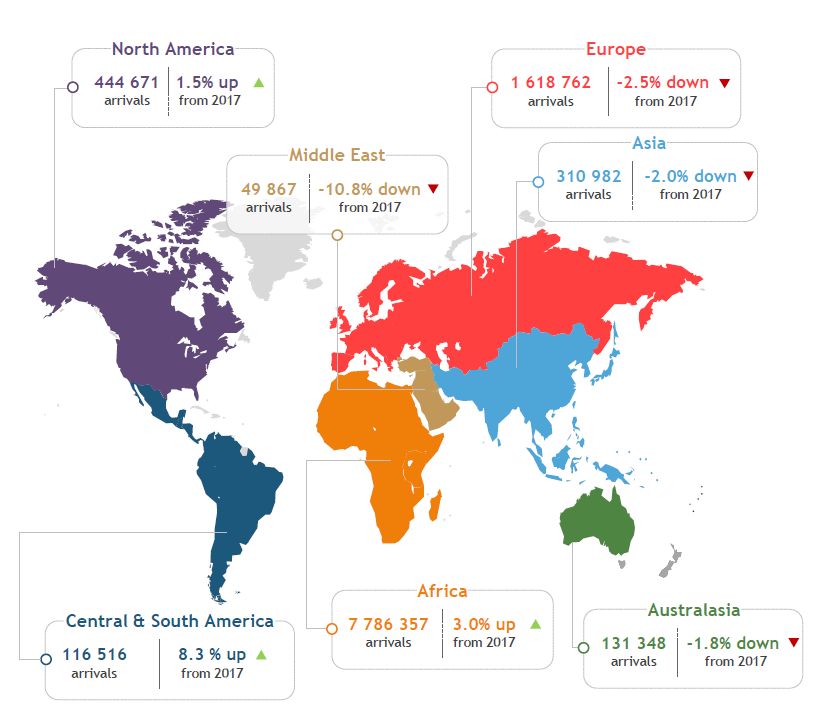

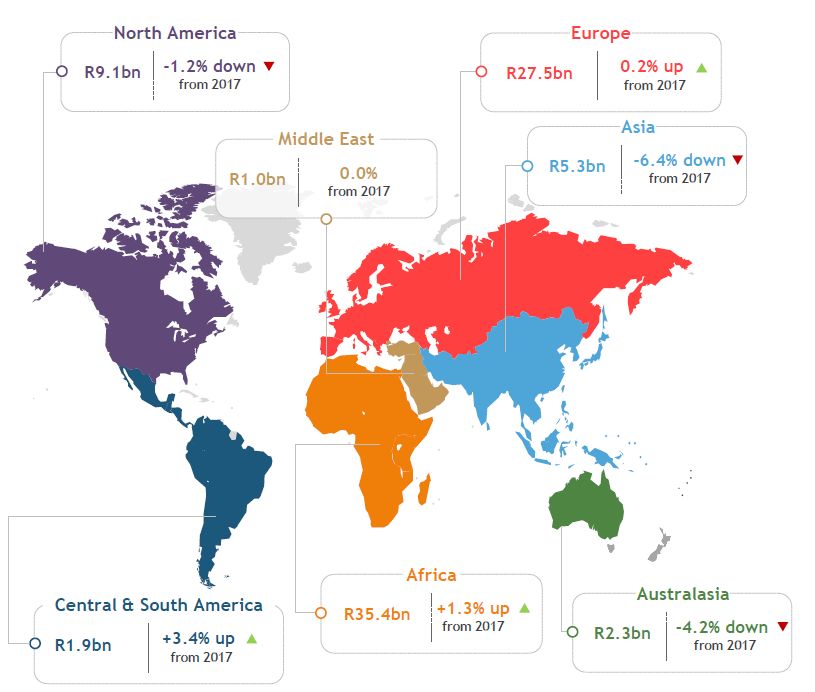

46ASIA PACIFIC OUTBOUND TOURISM TO SOUTH AFRICA Tourists Arrivals South Africa recorded 10.5 million international tourist arrivals in 2018, a +1.8% increase compared to 2017. The Asia Pacific region contributed 442, 330 arrivals in 2018. The top outbound markets were Australia, China, India, Japan and South Korea. International tourism arrivals from this region declined by -2.0% in 2018 to reach a total of 310 982. All major markets except for Japan (+0.5%) declined in 2018. China (-0.2%), India (-4.6%), Malaysia (-19.6%), Singapore (-7.1%) and South Korea (-1.4%). The tourism revenue generated from this region decreased further by -6.4% to a total of R5.3 billion. Tourist arrivals from China decreased by 0.2% in 2018 compared to 2017. For Chinese tourists, South Africa has become more of a VFR (31.1%) and business events (20.0%) destination in 2018. The share of VFR tourists increased from 25.5% in 2017 to 31.1% in 2018 MICE tourists increased from 19.4% in 2017 to 20% in 2018. The holiday travel to South Africa from this market dropped to 29.8% in 2018 from 36.3% in 2017. South Africa experienced a decline in holiday arrivals from China since 2016. However, arrivals have started to improve since April 2018 with the Western Cape recording a positive growth out of this market.

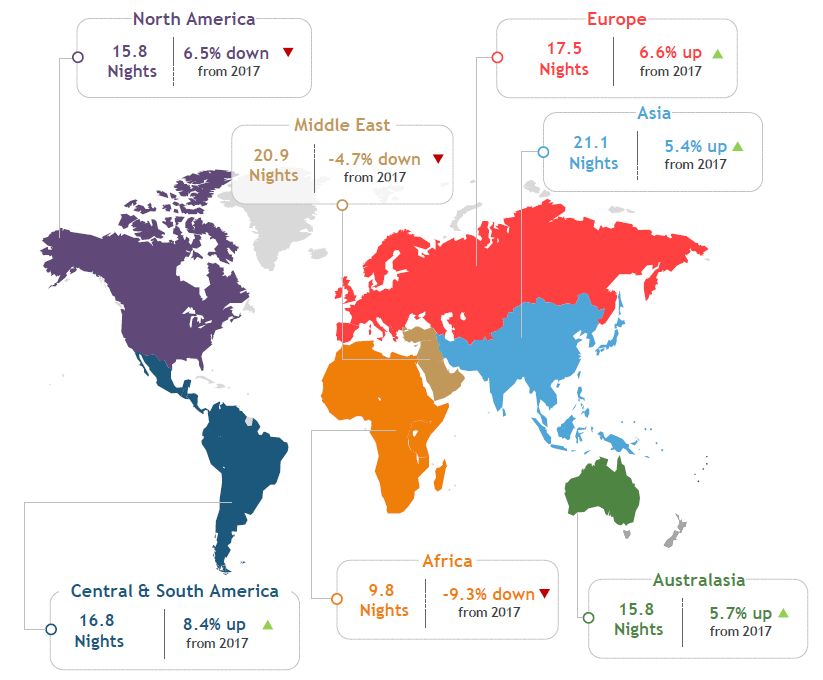

South Africa experienced stiff competition from destinations in the Europe in luring the Chinese outbound travellers. Improved air connectivity in addition to the EU-China Tourism year initiative by EU Commission President Jean- Claude Juncker and the Chinese Premier Li Keqiang in 2018 encouraged travel and investment between EU countries and China. Tourist arrivals from India declined by 4.6% in 2018 compared to 2017. The declines in volume are driven by declines in MICE, holiday and VFR tourists. Majority of the Indian travellers (1 out of every 2 tourists from India) visit South Africa as either a business traveller (corporate travel) or a MICE tourist. The share of business travellers travel increased to 25.4% in 2018 from 18.9%. The share of first-time travellers to SA increased to 54.5% whereas the repeat travellers declined. International tourist arrivals from Australia (a key source market), New Zealand and the Pacific declined by -1.8% in 2018 to a total of 131 348. Tourism receipts declined by -4.2% to R2.3 billion. The average nights increased to 15.8 nights to a total of 1.9 million bed nights. Australian arrivals declined by -0.4% to 115 846. The share of holiday arrivals dropped from 62.5% to 53.2% while VFR has increased from 24.3% to 27.4%. New Zealand declined by -11.0% and has been declining for the past 2 years since the reciprocal introduction of visas in 2017.

International arrivals from Asia Pacific

INTERNATIONAL ARRIVALS

2016 2017 2018 % Growth

Asia 327 890 317 181 310 982 -2%

China (incl. Hong Kong) 116 946 97 069 96 915 -0.20%

India 95 377 97 921 93 428 -4.60%

Japan 25 802 27 410 27 541 0.50%

Malaysia 8 713 9 282 7 460 -19.60%

Singapore 8 367 10 964 9 093 -17.10%

South Korea 18 840 22 173 21 868 -1.40%

Other Asia 327 890 317 181 310 982 -2.00%

Australasia 131 856 133 713 131 348 -1.80%

Australia 109 146 116 257 115 846 -0.40%

New Zealand 22 443 17 094 15 213 -11.00%

Other Australasia 131 856 133 713 131 348 -1.80%

Source: South Africa Tourism (2019)Source: South African Tourism (2019) Provincial Distribution: Western Cape Total number of international tourists that visited Western Cape increased by 0.2% to a total of 1.7 million. Arrivals decreased from the following key source markets: UK, Namibia, Netherlands and Australia. All other source markets recorded increases in arrivals to the province. The city of Cape Town received 2.6 million international visitors in 2018 with a growth of 11.5% in international arrivals at Cape Town International Airport. Outbound travel from Asia Pacific to Western Cape recorded 191919 arrivals and the major source markets being China (57868), Australia (53843), India (31,402), Japan (11665), South Korea (7684) and New Zealand (7252).

INTERNATIONAL TOURIST ARRIVALS- PROVINCAL DISTRIBUTION

2018

Nor

th

Western Eastern Kwazulu Mpuma Limpop We Norther Free

Gauteng Cape Cape Natal langa o st n Cape State

Asia 45 196 31 1447 5 442 10 220 5 762 2 250 826 5 439 1 968

China (incl.

Hong Kong) 16 688 12 265 2 707 3 080 2 143 1 140 324 2 134 827

India 13 388 6 321 859 2 479 1 297 255 273 1 798 439

Japan 3 912 3 237 388 1 165 778 198 44 287 223

Malaysia 1 149 931 149 149 188 89 15 99 60

Singapore 1 976 1 777 100 100 361 0 36 236 100

South Korea 3 037 1 956 396 770 550 439 48 319 242

Other Asia 5 045 4 659 843 2 477 445 129 86 566 77

Australasia 17 358 18 257 4 693 4 928 8 793 3 131 456 3 003 690

Australia 15 515 16 172 4 407 4 427 7 857 2 681 385 2 534 647

New Zealand 1 823 2 086 286 500 936 449 71 468 43

Other

Australasia 20 0 0 0 0 1 0 0 0

Source: South African Tourism (2019)

Source: South African Tourism (2019)Purpose of Travel

Travellers from Asia Pacific visited South Africa mostly for holiday and for

visiting friends and relatives (VFR). A substantial share of Asian travellers also

visited South Africa for MICE (21%) and Business travel (15%). Medical tourism

and shopping tourism (personal and business) were not popular among the

Asia Pacific travellers.

Purpose of Travel

2018

Shopping Shopping Business Religio

Holiday (personal) (business) traveller MICE Medical VFR n Other

27.7 21.1 0.10 27.7 0.3 7.90

Asia 0% 0.00% 0.20% 15% 0% % 0% 0% %

China (incl. 29.8 12.80 0.00 31.1 0.0 5.70

Hong Kong) 0% 0.00% 0.60% % 20% % 0% 0% %

22.9 25.40 26.4 0.00 11.4 0.6 13.3

India 0% 0.00% 0.00% % 0% % 0% 0% 0%

13.40 21.1 0.00 23.4 0.0 8.10

Japan 34% 0.00% 0.00% % 0% % 0% 0% %

35.4 0.00 15.5 0.0 7.50

Malaysia 34% 0.00% 0.00% 7.50% 0% % 0% 0% %

42.6 23.6 0.00 16.7 0.0 8.30

Singapore 0% 0.00% 0.00% 8.80% 0% % 0% 0% %

27.5 13.0 1.7% 46.2 0.0 5.20

South Korea 0% 0.00% 0.00% 6.40% 0% % %% 0% %

21.0 10.60 15.3 0.00 47.0 1.1 5.10

Other Asia 0% 0.00% 0.00% % 0% % 0% 0% %

52.7 4.10 20.0 28.3 1.0 6.80

Australasia 0% 0.00% 0.00% 6.90% % 0% 0% 0% %

53.2 3.60 20.0 27.4 1.2 7.10

Australia 0% 0.00% 0.00% 7.30% % 0% 0% 0% %

48.6 7.40 0.00 36.0 0.0 4.70

New Zealand 0% 0.00% 0.00% 3.30% % % 0% 0% %

Other 50.0 45.0 0.00 0.00 5.0 0.00

Australasia 0% 0.00% 0.00% 0.00% 0% % % 0% %

Source: South African Tourism (2019)Majority of the Asia Pacific travellers were first time visitors to South Africa, and

a quarter of the visitors have revisited South Africa 2-3 times.

First time and Repeat visitors

2018

First 2-3 4-5 6-9 10 times or

timers times times times more

Asia 48.30% 22.60% 10.70% 9.30% 9.10%

China (incl. Hong

Kong) 45.10% 25.30% 9.40% 10% 10.30%

India 54.50% 19.30% 11.50% 8.50% 6.20%

Japan 47.80% 19.80% 13.20% 10.60% 8.70%

Malaysia 56.20% 7.80% 17.70% 6.90% 11.40%

Singapore 45.10% 21.20% 11.30% 7.20% 15.20%

South Korea 41.50% 27.30% 13.70% 6.20% 11.20%

Other Asia 49.70% 22.30% 9.00% 10.00% 9.00%

Australasia 44.40% 23.40% 12.60% 10.10% 9.50%

Australia 44.80% 22.70% 12.30% 10.60% 9.60%

New Zealand 41.70% 29.10% 14.70% 6.30% 8.20%

Other Australasia 50.00% 0.00% 37.50% 0.00% 12.50%

Asia Pacific Total Foreign Spending

International tourists spent R82.5-billion in 2019 and the average amount

spent by tourists directly in South Africa was R8 200. This declined by - 2.4%

(R100) compared to 2017. Visitor spending in Western Cape amounted to

R16.3 Bn. Cape Town (R1 147.31) and the Western Cape (R1 029.19) as a

whole achieved the highest revenue among all provinces and top cities in

2018.Total foreign direct spending by travellers from Asia and the Pacific totalled R5,338726481 and R2,307 862 394 respectively. The biggest spenders were from China, Australia, India, Japan, New Zealand and South Korea. The New Zealanders spent the highest average amount per traveller (R 21 808), followed by Australians (18 965), Chinese (18 858), Malaysians (17 480) and Singaporeans (16 389). Total Foreign Direct Spending by Travellers Source: South African Tourism (2019)

TOTAL FOREIGN DIRECT SPEND BY COUNTRY

2016 2017 2018 % Growth

Asia R 3 522 281 763 R 4 204 171 081 R 5 338 726 481 27.00%

China (incl. Hong Kong) R 1 075 909 313 R 1 401 438 043 R 2 371 666 767 69.20%

India R 1 201 670 653 R 1 367 320 414 R 1 299 727 386 -4.90%

Japan R 275 610 924 R 332 493 791 R 390 087 262 17.30%

Malaysia R 145 732 789 R 146 505 728 R 120 927 328 -17.50%

Singapore R 133 478 141 R 152 626 907 R 144 615 552 -5.20%

South Korea R 184 941 375 R 253 039 050 R 291 084 240 15.00%

Other Asia R 504 938 559 R 550 495 372 R 720 478 269 30.90%

Australasia R 2 319 996 930 R 2 408 704 391 R 2 307 862 394 -4.20%

Australia R 1 904 760 939 R 2 408 704 391 R 307 862 394 -4.80%

New Zealand R 414 499 389 R 299 299 134 R 301 117 518 0.60%

Other Australasia R 736 601 R 823 389 R 376 550 -54.30%

Source: South African Tourism (2019)

Average amount spent per traveller

Source: South African Tourism (2019)You can also read