3Q-2021 Market Intelligence Reports Release Presentation - Better Lodging Analytics For Better Business Decisions

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

3Q-2021 Market Intelligence

Reports Release

Presentation

Better Lodging Analytics For Better Business Decisions

1. Our Approach to Market Intelligence 2. U.S. Market Review 3. This Recovery Will Be Different 4. U.S. Outlook 5. Market Highlights 6. Q&A

Our Approach

The LARC Approach

Everything To Analyze a Market in One Place

• Historical Operating Results Forecasts for the following key industry metrics:

On a Quarterly Basis

• Detailed Economic Summary • Supply

• Citywide Pacing Data • Demand

• Occupancy

• Air Traffic Data • Average Daily Rate

• Office Market • RevPAR

• Wages

• Supply Pipeline • Hotel EBITDA and Margins

• Home Sharing On an Annual Basis

• Property Taxes

• Recent Transactions • Cap Rates

• Key Capital Projects (Public and Private) • Hotel Values

LARC’s Core Values

Transparency Market-Based Realism

LARC believes its forecast LARC recognizes that each LARC’s baseline forecasts

accuracy should be forecast/ project completed represent the most likely

transparent and offer a should be constructed with outcomes, grounded in the

means for clients to alter the specific factors that drive current market environment

inputs to key drivers, should that individual market in and realistic outlooks for key

they have differing mind, yielding a unique macro drivers.

assumptions. analytical model that results

in highly accurate findings

and conclusions.

Forecast Methodology

Multi-Variable Linear Regression No Subjective Adjustments

• We find the industry and macro-economic • We incorporate special events like the Super

factors that drive lodging fundamentals in Bowl into our models

each market we analyze • Taking the time to build market specific models

o While there is overlap among the markets, no creates heightened forecasting accuracy

two markets have the same forecast model

o We include leading indicators as well as • We don’t allow the psychology of the moment to

concurrent indicators alter our forecasts by applying subjective

adjustments.

• We build as many factors as necessary into

our models (usually between 3 and 7) to • Subjectively adjusting the results eliminates the

build a model that has impeccable back advantage of using data analytics

testing strength going back to 2000

o Our models account for past downturns

Only the Best Data Sources

Better Data In = Better Data Out

• We know that regression forecasting is based Key Data Providers

on data and specifically forecasts for key • Historical Operating Results- STR

industry drivers that come from platforms other

than us. • Detailed Economic Summary- Moody’s Analytics

• We use the best data providers we can find to • Citywide Pacing Data- Local CVBs

make sure that our outputs are the best • Office Market- Moody’s Analytics

possible. • Supply Pipeline- BuildCentral

• Home Sharing- AirDNA

• Historical Cap Rates and Transactions – Real

Capital Analytics, LW Hospitality Advisors

U.S. Market Review

Monthly 2021 RevPAR Growth From 2019

Recovery Progressing Monthly RevPAR Change vs. 2019

• U.S RevPAR has been on a steady 20%

recovery since the start of the year

0%

• January: -48%

-20%

• April: -29%

• July: +0.2% -40%

U.S.

• STR’s Top-25 markets are down -60% Top 25

more, but recovering at a similar pace All Other

-80%

• Smaller markets turned positive vs.

June

January

May

July

March

February

April

2019 in June

Source: Lodging Analytics Research & Consulting, STR4%

• Market

from 2019

through July

down 25.2%

Extreme YTD

Divergence is

is down 71%

• Norfolk is up

• San Francisco

U.S. Headlines

• 2021 U.S. RevPAR

10%

0%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

Norfolk/Virginia Beach, VA

Miami, FL

Tampa, FL

Charleston, SC

Memphis, TN

Omaha, NE

San Antonio, TX

Dayton, OH

Source: Lodging Analytics Research & Consulting, STR, LVCVA

Salt Lake City, UT

Phoenix, AZ

Des Moines, IA

Saint Louis, MO

Cleveland, OH

Kansas City, MO

Houston, TX

Indianapolis, IN

Detroit, MI

San Diego, CA

Atlanta, GA

Dallas, TX

Pittsburgh, PA

Ann Arbor, MI

Orlando, FL

An Inconsistent Start to the Recovery

Los Angeles, CA

Austin, TX

Orange County, CA

Columbus, OH

YTD-July RevPAR vs. YTD 2019

Nashville, TN

Raleigh, NC

Las Vegas

Louisville, KY

Philadelphia, PA

Denver, CO

YTD-July 2021 RevPAR vs. 2019

Portland, OR

Oahu Island, HI

Chicago, IL

Minneapolis, MN

New Orleans, LA

Seattle, WA

New York, NY

Washington, DC

Boston, MA

San Jose, CA

San Francisco/San Mateo, CAJuly

36%

vs. 2019 in July

• U.S. RevPAR up

• 11 of LARC’s 44

0.2% vs. 2019 in

markets positive

Remains Extreme

• San Francisco

U.S. Headlines

• Miami was up

• Market Divergence

was down 50%

10%

20%

30%

40%

0%

-60%

-50%

-40%

-30%

-20%

-10%

Miami, FL

Tampa, FL

Norfolk/Virginia Beach, VA

Charleston, SC

Phoenix, AZ

Orlando, FL

San Antonio, TX

Omaha, NE

Source: Lodging Analytics Research & Consulting, STR, LVCVA

Las Vegas

Nashville, TN

Memphis, TN

Atlanta, GA

San Diego, CA

Kansas City, MO

Orange County, CA

Austin, TX

Salt Lake City, UT

Oahu Island, HI

Des Moines, IA

Houston, TX

Detroit, MI

Saint Louis, MO

Indianapolis, IN

An Inconsistent Start to the Recovery

Los Angeles, CA

Dayton, OH

Louisville, KY

New Orleans, LA

July 2021 RevPAR vs. July 2019

Dallas, TX

Pittsburgh, PA

Cleveland, OH

Ann Arbor, MI

July 2021 RevPAR vs. 2019

Denver, CO

Philadelphia, PA

Raleigh, NC

Columbus, OH

Chicago, IL

Portland, OR

New York, NY

Seattle, WA

Minneapolis, MN

Washington, DC

Boston, MA

San Jose, CA

San Francisco/San Mateo, CATSA Throughput

Air Traffic Recovery Stalled

TSA Throughput Growth vs. 2019

On 14-Day Moving Average

• Air traffic volumes troughed at year- 0%

over-year declines of 96% in mid-April -20%

2020

-40%

• From September 2020 through June -60%

2021 there was steady improvement

-80%

• However, since the start of July

-100%

throughput has stabilized at levels

about 20% below 2019 -120%

10/14/2020

11/14/2020

12/14/2020

3/14/2020

4/14/2020

5/14/2020

6/14/2020

7/14/2020

8/14/2020

9/14/2020

1/14/2021

2/14/2021

3/14/2021

4/14/2021

5/14/2021

6/14/2021

7/14/2021

8/14/2021

Source: Lodging Analytics Research & Consulting, TSAVaccinations Driving Increased Travel

Vaccinations Driving Air Traffic

TSA Throughput Relative to 2019 vs. U.S.

Vaccination Totals

• As of September 4, approximately 176 0% 200

million U.S. citizens had been fully

Millions

180

vaccinated -10%

160

• Data From January 19 to September 4 -20% 140

shows that vaccinations are driving an -30% 120

increase in air traffic 100

• 97.1% correlation -40% 80

• 94.4% R-squared -50% 60

Air Traffic vs. 2019 40

• However, moving forward vaccinations -60%

20

will slow and the recovery will be reliant U.S. Vaccination Total

on the return of corporate and group -70% 0

2/2/2021

3/2/2021

6/8/2021

7/6/2021

8/3/2021

demand

1/19/2021

2/16/2021

3/16/2021

3/30/2021

4/13/2021

4/27/2021

5/11/2021

5/25/2021

6/22/2021

7/20/2021

8/17/2021

8/31/2021

• Less than 30% of the global population

is fully vaccinated

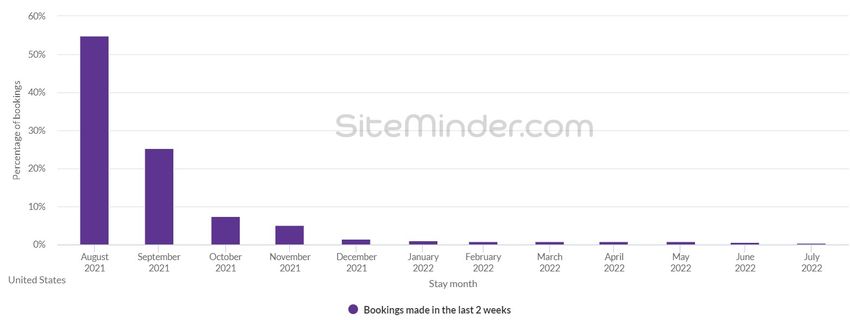

Source: Lodging Analytics Research & Consulting, TSA, CDCHotel Booking Volumes

Volumes Beginning to Hotel Booking Volumes as % of 2019

Accelerate Levels

• U.S. hotel booking volumes have started to

improve

• As of 2/1, 54.6% of 2019 booking volumes

were completed

• As of 3/1, 62.8%

• As of 5/27, 88.4%

• As of 7/1, 82.0%

• As of 8/13, 74.2%

• As of 9/5, 82.4%

• The Delta Variant clearly caused a

deceleration in the bookings recovery from Booking Window is Very Short

late July through Mid-August, but booking

volumes have recovered that lost ground

• Booking windows remain extremely short

Source: Siteminder.comSupply- Hotel Closures

Peak Rooms Closures

Peak Room Closure Highlights

as a % of Existing Market Inventory

• The U.S. closure peak occurred in April 60%

2020 at almost 800,000 rooms,

50%

equating to 14.3% of the rooms

inventory 40%

• Markets with the highest level of peak 30%

closures have the following attributes:

20%

• Heavy concentration of union labor

10%

• Large resorts

• International destination 0%

Anaheim

San Francisco

Orlando

San Diego

Nashville

New York

Norfolk

St. Louis

Philadelphia

Denver

Boston

Washington D.C.

Honolulu

Chicago

Seattle

Houston

Phoenix

Minneapolis

Miami

Tampa

Atlanta

Detroit

Los Angeles

Dallas

New Orleans

• Theme parks as a large demand

driver

Source: Lodging Analytics Research & Consulting, BuildCentral and STRSupply- Closures As of July 2021

July Room Closure Highlights July Room Closures

as a % of Existing Inventory

• As of July 2021, only about 20,000 10%

rooms remained closed across the 7.8%

U.S., equating to 0.4% of the rooms

inventory

• New York now accounts for about half 3.7%

of all closures, though we estimate 2.3%

that only about 5,500 rooms across 1.6% 1.3%

0.9%

the New York market will be 0.4% 0.3% 0.3% 0.2%

0%

permanently closed

Source: Lodging Analytics Research & Consulting, BuildCentral and STRHome Sharing- Leisure Focused and Supply Driven

Hotel-Comparable Home Sharing Revenue and YoY Hotel-Comparable Home Sharing Available Room Hotel-Comparable Home Sharing ADR and YoY

Growth on a Rolling 4-Quarter Basis Nights and YoY Growth on a Rolling 4-Quarter Basis Growth on a Rolling 4-Quarter Basis

$2,500 120% 20 120% $180 8%

Millions

Millions

100% 18 100% $170 7%

$2,000 16 $160 6%

80% 80% 5%

14 $150

$1,500 60% 12 60% $140 4%

40% 10 40% 3%

$130

2%

$1,000 20% 8 20% $120 1%

6 $110 0%

0% 0%

$500 4 $100 -1%

-20% 2 -20% $90 -2%

$0 -40% 0 -40% $80 -3%

2016-3Q

2016-4Q

2017-1Q

2017-2Q

2017-3Q

2017-4Q

2018-1Q

2018-2Q

2018-3Q

2018-4Q

2019-1Q

2019-2Q

2019-3Q

2019-4Q

2020-1Q

2020-2Q

2020-3Q

2020-4Q

2021-1Q

2021-2Q

2016-3Q

2016-4Q

2017-1Q

2017-2Q

2017-3Q

2017-4Q

2018-1Q

2018-2Q

2018-3Q

2018-4Q

2019-1Q

2019-2Q

2019-3Q

2019-4Q

2020-1Q

2020-2Q

2020-3Q

2020-4Q

2021-1Q

2021-2Q

2016-3Q

2017-1Q

2017-3Q

2018-1Q

2018-3Q

2019-1Q

2019-3Q

2020-1Q

2020-3Q

2021-1Q

Source: AirDNA and Lodging Analytics Research & Consulting Source: AirDNA and Lodging Analytics Research & Consulting Source: AirDNA and Lodging Analytics Research & Consulting

Hotel-Comparable Home Sharing Segment Share of

Accommodations Revenue

8%

7%

6%

5%

4%

3%

2%

1%

0%

2014-4Q

2015-2Q

2015-4Q

2016-2Q

2016-4Q

2017-2Q

2017-4Q

2018-2Q

2018-4Q

2019-2Q

2019-4Q

2020-2Q

2020-4Q

2021-2Q

Source: AirDNA and Lodging Analytics Research & ConsultingThis Recovery Will be Different

This Cycle is Unlike Any Other- RevPAR

RevPAR Recovery Timeline RevPAR Recovery in Past Cycles (TTM)

110

• This cycle’s RevPAR decline is

deeper and steeper than any 100

experienced prior 90

• Following the Great Financial Crisis, it 80

took 59 months for trailing-12-month

70

RevPAR to recover to the prior peak

Current Downturn

level 60

Great Financial Crisis

50

• Following 9/11, it took 52 months 9/11

40

Month 0

Month 3

Month 6

Month 9

Month 12

Month 15

Month 18

Month 21

Month 24

Month 27

Month 30

Month 33

Month 36

Month 39

Month 42

Month 45

Month 48

Month 51

Month 54

Month 57

Source: Lodging Analytics Research & Consulting, STRThis Cycle is Unlike Any Other- Occupancy

Occupancy Recovery in Past Cycles

Occupancy Recovery Timeline

(TTM)

110

• This cycle’s Occupancy decline is

deeper and steeper than any 100

experienced prior

90

• Following the Great Financial Crisis, it

took 81 months for trailing-12-month 80

Occupancy to recover to the prior 70 Current Downturn

peak level Great Financial Crisis

60

• Following 9/11, it took 65 months 9/11

50

Month 0

Month 12

Month 24

Month 36

Month 48

Month 60

Month 72

Source: Lodging Analytics Research & Consulting, STRThis Cycle is Unlike Any Other- ADR

ADR Recovery Timeline ADR Recovery in Past Cycles (TTM)

110

• This cycle’s ADR decline is deeper

and steeper than any experienced 100

prior

90

• Following the Great Financial Crisis, it

took 52 months for trailing-12-month 80

ADR to recover to the prior peak level 70 Current Downturn

• Following 9/11, it took 45 months 60

Great Financial Crisis

9/11

50

Month 0

Month 2

Month 4

Month 6

Month 8

Month 10

Month 12

Month 14

Month 16

Month 18

Month 20

Month 22

Month 24

Month 26

Month 28

Month 30

Month 32

Month 34

Month 36

Month 38

Month 40

Month 42

Month 44

Month 46

Month 48

Month 50

Month 52

Source: Lodging Analytics Research & Consulting, STRThis Cycle is Unlike Any Other- Hotel Values

Hotel Value Recovery in Past Cycles

Hotel Value Recovery Timeline

(Values Indexed to 2019)

• Following the Great Financial Crisis, 110

Hotel Values dropped 27% from the

2007 peak to the 2009 trough 100

• Following the Great Financial Crisis,

Hotel Values did not recover to the 2007 90

peak until 2015

80

• By 2018, values were 18% above the

prior 2007 peak 70

• Values began declining in 2019, in

advance of the pandemic 60

2020 E

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

• We estimate that in a fully transparent

environment, 2020 values would have

fallen another 24% Source: Lodging Analytics Research & Consulting, Real Capital AnalyticsConvention Demand Could Recover Quickly

Recovery Will Be Faster Than U.S. Convention Center Bookings as of

Past Cycles June 2021

• We have aggregated definite room nights for over 30 120 Index 10%

of the largest convention centers across the United

% Chg vs. 2019 0%

States 100

-10%

• 2021 is pacing up 21% from 2020 but still 58% below 80

that of 2019 as cancellations have continued to -20%

materialize. Regardless, the majority of 2021 softness 60 -30%

was in the front half of the year, so if cancellations

-40%

don’t accelerate (something we believe is unlikely) the 40

recovery will begin in 4Q-2021. -50%

20

• 2022 is pacing just 11% below 2019 levels -60%

• While group is normally the slowest segment to 0 -70%

2019 2020 2021 2022 2023 2024

recover, with so many definite room nights already on

Source: Lodging Analytics Research & Consulting

the books, we believe convention group will snap back

faster than in past recoveriesGross Savings Rate

Unprecedented Savings Rate NIPA U.S. Gross Savings Rate

Coming Out of Downturn (Billions, SAAR)

• The U.S. Gross Savings Rate ended 2020 at

$4.2 trillion $4,500

• Not only is this the highest level on record, $4,000

but it is a 3% increase from pre-pandemic $3,500

levels $3,000

• The increase is primarily fueled by stock

$2,500

market gains and low spending during the $2,000

pandemic $1,500

$1,000

• During the GFC the gross savings rate

declined 11% and during the 9/11 downturn

$500

the gross savings rate declined 5% $0

1990Q1

1992Q1

1994Q1

1996Q1

1998Q1

2000Q1

2002Q1

2004Q1

2006Q1

2008Q1

2010Q1

2012Q1

2014Q1

2016Q1

2018Q1

2020Q1

• The current U.S. gross savings rate is

approximately double what it was after the

GFC Source: Moody’s Analytics, Lodging Analytics Research & Consulting2020 Economic Activity Better than Headlines for Lodging

Sector Performance, Stock Market

Support Corporate Transient 2020 Sector GDP Growth

Recovery

• Combined- the sectors that drive the most 10%

5% 3.6%

corporate transient demand across the 0.3%

lodging sector experienced no decline in 0%

2020; information Technology was up 3.6%, -5% -3.2% -2.2% -2.2% -2.1%

Financial Activities were up 0.3% and -10% -5.8% -5.6% -4.5%

Professional Services were down 2.2% -15% -12.3%

• In 2020, the S&P 500 set an all-time high -20%

and closed 15.2% above year-end 2019. It -25%

is up another 22% year-to-date (9/7/2021). -30% -27.2%

Education and Health

Leisure and Hospitality

Professional and Business

Information Technology

Other Services

Financial Activities

Natural Resources and

Trade, Transportation and

Manufacturing

Government

Construction

• During the GFC, the S&P 500 dropped

27%

Services

Mining

Services

• During the 9/11 Downturn, the S&P 500

Utilities

dropped 40%

Source: Lodging Analytics Research & ConsultingFiscal Stimulus- Covid-19 is 5x As Large as the GFC

Fiscal Stimulus Packages Fiscal Stimulus Totals (Billions)

Stimulus Package Value (Billions)

$9,000 $8,320

Great Financial Crisis

2008 Economic Stimulus Act $152 $8,000

American Recovery Act $840

$7,000

Total $992

as % of 2007 GDP 6.3% $6,000

$4,820

$5,000

Covid-19 Pandemic

CARES Act $2,000 $4,000

December Emergency Coronavius Relief $920

American Rescue Plan $1,900

$3,000

Total Covid-19 Stimulus To Date $4,820 $2,000

as % of 2019 GDP 25.2% $992

$1,000

Infrastucture Plan + Budget Reconcilation "Build Back Better" Agenda $3,500 $0

Total Assumed Covid-19 Stimulus $8,320 Great Financial Crisis Total Covid-19 Stimulus To Total Assumed Covid-19

as % of 2019 GDP 43.6% Date Stimulus

Source: Lodging Analytics Research & ConsultingU.S. Outlook

Covid-19 and Fiscal Policy Assumptions

• The Delta Variant slows the corporate/ group travel recovery by a couple months

• No new variants impact children or the vaccinated in any meaningful way

• $550 billion infrastructure bill gets signed in the Fall

• President Biden’s $3 trillion “Build Back Better” fiscal package will pass in late 2021 via

budget reconciliation and be implemented beginning in 2022

• Elevated inflation is transitory and labor supply constraints will ease in SeptemberDelta Impact – Return to Office Delays

Sampling of Delta-Induced Reopening Delays

Company Scheduled Date Comments

Goldman Sachs June-21 Vaccinated only

• Many companies have pushed JP Morgan Chase July-21 Encouraging vaccines

back their return to the office as a Eli Lilly

Bank of America

July-21

September-21

Vaccine Mandate by 11/15

Vaccinated only

little as one month, to all the way CVS September-21

to early 2022 Pfizer September-21 Vaccine/ Testing mandate

UPS September-21 Vaccine Mandate by 10/1/2021

• Financial services are generally Washington Post September-21 Vaccination Mandate

the more aggressive companies Wells Fargo

Blackrock

October-21

October-21

Pushed back from 10/4 to 10/18

Vaccinated only

in the timing of a return to the Microsoft October-21 Vaccinated only

office Comcast October-21 Pushed back from September

Viacom CBS October-21 Delayed from September

• Tech companies are less Travelers Cos. October-21 Delayed "at least a month" from September

aggressive TJ Maxx

PwC

November-21

November-21

Vaccine Mandate

Delayed from September

• Some companies have Apple

Amazon

January-22

January-22

Pushed back from October

Pushed back from September

postponed their returns Starbucks January-22 Pushed back from October

indefinitely Ford Motor Company January-22

Google January-22 Pushed back from mid-October to January

Uber January-22 Pushed back from late September

Lyft February-22

Airbnb September-22 No change due to Delta variant

Twitter TBD Closed offices in New York and San Francisco in July

New York Times TBD Cancelled September return

Source: Lodging Analytics Research & ConsultingSupply

Key Supply Assumptions U.S. Lodging Supply Growth

(forecasts begin 3Q-2021)

• Almost all current hotel closures are 2019

1Q

2.0%

2Q

2.0%

3Q

2.0%

4Q

2.1%

Year

2.0%

temporary and virtually all temporarily 2020 2.0% -10.2% -3.4% -3.4% -3.6%

closed hotels will be open by the end 2021 F -1.9% 13.4% 7.9% 5.6% 6.3%

2022 F 5.7% 4.1% 1.9% 1.8% 3.4%

of 3Q-2021. 2023 F 1.5% 1.1% 1.1% 1.5% 1.3%

• Construction/ opening delays have '20 - '23F CAGR 3.6%

been rolling off throughout 2021, '20 - '25F CAGR 2.9%

which will cause more hotels to open

in late 2021 driving an acceleration in U.S. Economic Supply Growth

economic supply growth into late 2021 (forecasts begin 3Q-2021)

and early 2022, before supply growth 1Q 2Q 3Q 4Q Year

begins to moderate again. 2019 2.0% 2.0% 2.0% 2.1% 2.0%

2020 2.0% 2.7% 1.3% 1.2% 1.4%

2021 F 1.0% 1.6% 1.4% 2.3% 1.6%

2022 F 2.7% 2.0% 1.9% 1.8% 2.1%

2023 F 1.5% 1.1% 1.1% 1.5% 1.3%

'20 - '23F CAGR 1.7%

'20 - '25F CAGR 1.8%

Source: Lodging Analytics Research & Consulting, BuildCentral and STRRevPAR Model

Key Model Drivers RevPAR, Seasonally Adjusted

$120

Actual RevPAR, SA

• Unemployment Rate Modeled RevPAR, SA

• Real GDP $100 R-Squared = 99.7%

Standard Error = 4.3%

• Business Investment $80

• S&P 500 Index

• Real Foreign Exchange Rate $60

• Supply $40

$20

$0

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

1Q16

1Q17

1Q18

1Q19

1Q20

1Q21

1Q22

1Q23

1Q24

1Q25

Source: STR and Lodging Analytics Research & ConsultingADR Model

Key Model Drivers ADR, Seasonally Adjusted

$160

Actual ADR, SA

• Business Investment Modeled ADR, SA

$140

• Inflation R-Squared = 98.6%

Standard Error = 3.0%

$120

• Consumer Confidence

$100

• Unemployment Rate

$80

$60

$40

$20

$0

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

1Q16

1Q17

1Q18

1Q19

1Q20

1Q21

1Q22

1Q23

1Q24

1Q25

Source: STR and Lodging Analytics Research & ConsultingExpenses and EBITDA

U.S. Lodging Wage Growth

Key Expense Assumptions (forecasts begin 2Q-2021)

1Q 2Q 3Q 4Q Annual

• Property Taxes will grow at a 4.5% 2019 3.8% 3.8% 3.9% 2.4% 3.5%

CAGR through 2025 2020 2.3% -2.9% 0.0% 4.8% 1.1%

2021 F 8.0% 7.9% 2.3% -3.1% 3.7%

• Wages will increase at a 3.4% CAGR

through 2025 2022 F -5.9% -0.7% 2.3% 3.9% -0.2%

2023 F 4.4% 4.5% 4.4% 5.1% 4.6%

• Other Expenses will grow at inflation 2024 F 5.0% 4.8% 4.8% 4.5% 4.8%

• We assume historical levels of cost 2025 F 4.3% 4.3% 4.3% 4.3% 4.3%

Source: Lodging Analytics Research & Consulting, Moody’s Analytics

flexing related to occupancy and for

negative environments U.S. Hotel EBITDA Growth

1Q 2Q 3Q 4Q Annual Vs. 2019

2021 F -84.0% -330.1% -28995% 863.7% 403.1% -51.0%

2022 F 601% 71% 5.0% 78.6% 65.2% -19.1%

2023 F 50.0% 26.7% 15.0% 7.8% 23.1% -0.4%

2024 F 10.5% 10.3% 8.2% 7.0% 9.1% 8.6%

2025 F -0.2% -2.1% -1.6% -1.1% -1.3% 7.2%

Source: Lodging Analytics Research & ConsultingCap Rate Model

Key Model Drivers Hotel Cap Rates

10.0%

Macro-economic Factors 9.0%

• Baa Bond Yields 8.0%

• High Yield Bond Spreads 7.0%

• Real Foreign Exchange Rate 6.0%

• Real GDP 5.0%

4.0%

• Unemployment Rate Actual Cap Rate

3.0% Modeled Cap Rate

Lodging Industry Factors: R-Squared= 98.3%

2.0% Standard Error= 22 bps

• Lodging Supply

1.0%

0.0%

2005-2Q

2006-2Q

2007-2Q

2008-2Q

2009-2Q

2010-2Q

2011-2Q

2012-2Q

2013-2Q

2014-2Q

2015-2Q

2016-2Q

2017-2Q

2018-2Q

2019-2Q

2020-2Q

2021-2Q

2022-2Q

2023-2Q

2024-2Q

2025-2Q

Source: Real Capital Analytics and Lodging Analytics Research & ConsultingU.S. Forecast Summary

U.S. Hotel Industry Forecast Summary

Key Takeaways 3-Year 5-Year

We forecast ADR to recover to 2019 levels in 2022, while RevPAR,

2021 Forward Forward

Hotel EBITDA and asset values will reach 2019 levels in 2023. Growth CAGR CAGR

Occupancy won’t reach 2019 levels until 2024. Economic Supply 1.6% 1.7% 1.8%

Key changes from June Outlook: Demand 29.6% 15.9% 10.4%

• The summer leisure season proved stronger than expected as ADR Occupancy 28.0% 14.2% 8.6%

proved much more resilient despite low absolute occupancy levels ADR 17.1% 10.7% 7.5%

• The Delta Variant has delayed the acceleration of corporate and RevPAR 49.9% 26.4% 16.8%

group travel by at least a couple months. In June, we had expected it

to occur after Labor Day, now we are looking at November and Hotel EBITDA 403.1% 117.1% 61.6%

possibly after the new year. Hotel Values 19.5% 11.8% 7.0%

• Despite the stronger summer leisure season, our longer-term outlook

for demand and occupancy is essentially unchanged 2021 U.S. Hotel Industry Outlook

9/2021 Update 6/2021 Update Outlook

• Our long-term outlook on ADR has improved by about 3% as the

improved 2021 ADR recovery will give the industry a stronger base to YoY Growth YoY Growth Change

build from going forward, slightly enhancing pricing power over the Growth vs. 2019 Growth vs. 2019 vs. 2019

course of the next few years. Economic Supply 1.6% 2.9% 1.4% 2.9% 0.0%

• 2021 values improve tied to lower base rates and better cash flows, Demand 29.6% -13.7% 28.4% -17.4% 3.8%

but longer–term values are only slightly higher. Occupancy 28.0% -14.7% 21.8% -18.8% 4.1%

ADR 17.1% -7.9% 7.2% -15.7% 7.8%

RevPAR 49.9% -21.4% 30.6% -31.5% 10.1%

Hotel EBITDA 403.1% -51.0% 167.7% -73.8% 22.8%

Hotel Values 19.5% -8.9% 1.2% -22.9% 14.1%

Source: Lodging Analytics Research & ConsultingHotel Values- This Cycle

Hotel Value Recovery in GFC vs.

Hotel Value Recovery Timeline

Forecast for Current Cycle

• Following the Great Financial Crisis, Hotel Values dropped

27% from the 2007 peak to the 2009 trough 110 GFC Downturn Current Cycle

• Following the Great Financial Crisis, Hotel Values did not

recover to the 2007 peak until 2015

100

• Roughly $1 trillion in fiscal stimulus passed

• By 2018, values were 18% above the prior 2007 peak 90

• Values began declining in 2019, in advance of the

pandemic

80

• We assume $8 trillion in fiscal stimulus- $4.8 trillion

already passed and another $3.5 trillion passed in late

2021, but rolled out over several years for Biden’s “Build 70

Back Better” agenda

• We estimate values would have declined 23.8% in 2020, in

a fully transparent environment, which will bring the total 60

decline from the 2018 peak to 29%, comparable to the

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

decline experienced in the GFC

• We forecast values to recover to 2019 levels by 2023, and

to the 2018 prior peak by 2024. However, we forecast a

decline in values in 2025, that will bring 2025 values on par Source: Lodging Analytics Research & Consulting, Real Capital Analytics

with the 2018 peak.Outlook vs. Past Cycles

Months of Recovery to Prior Peak

Recovery Timeline

By Cycle

• In general, we expect the recovery 120 9/11 GFC Covid

from this cycle to be meaningfully 100 vs. 9/11 vs. GFC 96

swifter than past cycles, despite the 81

80 72

deeper decline 65 63 59

60 45

52 52

• Relative to the Great Financial Crisis, 36

42

our outlook is anywhere from a year 40

and a half to two years faster, 20

depending on the metric 0

-2

• Relative to 9/11, our outlook is -20 -18

-9

-16

-10

-17

anywhere from 2 to 10 months faster, -40

-24

depending on the metric Occupancy ADR RevPAR Values

Source: Lodging Analytics Research & Consulting, Real Capital AnalyticsLARC vs. Other Forecasts

Highlights Current Forecasts

2021 2022 2023 2024 2025

STR/ Tourism Economics - August 12

• Most recent forecasts are most

Occupancy 57.9% 65.5%

positive for 2021 (LARC and STR) as ADR $115.64 $122.58

the summer season exceed all RevPAR $66.99 $80.19 $84.99 $90.10

expectations

PwC - May 28

• LARC remains much more positive for Occupancy 57.2% 61.8%

ADR recovery than others ADR $111.20 $118.49

RevPAR $63.57 $73.25

CBRE - March 30

Occupancy 49.1% 61.7% 65.1% 65.5% 65.2%

ADR $99.46 $113.21 $127.02 $136.63 $143.07

RevPAR $48.81 $69.85 $82.65 $89.51 $93.27

July 20 Update

ADR $107.69 $119.97

LARC - September 1

Occupancy 56.4% 61.1% 65.6% 66.5% 66.6%

ADR $120.86 $133.42 $140.06 $145.31 $148.16

RevPAR $68.15 $81.47 $91.88 $96.66 $98.71

Source: Lodging Analytics Research & Consulting, STR, PwC, CBREMarket Highlights

LARC’s Top-26 Market Coverage Universe

26 Hotel Markets: STR’s Top 25, Las VegasModel Statistics

Model Accuracy Based on R-squareds and

Back-Testing to 2000 (2005 for cap rates)

R-Squareds for our Mult-Variable Regression Forecasting Models

RevPAR Forecast ADR Forecast Cap Rate Forecast

Anaheim, CA 99.2% 99.8% 99.6%

Atlanta, GA 99.2% 99.8% 98.2%

Boston, MA 99.4% 91.1% 99.5%

Chicago, IL 99.2% 99.7% 98.3%

Dallas, TX 99.5% 89.2% 99.8%

Denver, CO 92.3% 99.7% 99.8%

Detroit, MI 99.4% 89.9% 99.6%

Houston, TX 91.7% 92.1% 98.2%

Las Vegas, NV 99.5% 99.7% 99.5%

Los Angeles, CA 94.0% 93.8% 98.3%

Miami, FL 99.5% 99.6% 99.7%

Minneapolis, MN 99.4% 99.8% 99.7%

Nashville, TN 99.3% 99.6% 99.6%

New Orleans, LA 99.2% 99.6% 98.4%

New York, NY 99.6% 99.7% 94.8%

Norfolk, VA 98.9% 99.7% 98.4%

Honolulu, HI 95.5% 97.6% 98.3%

Orlando, FL 99.5% 98.7% 98.3%

Philadelphia, PA 99.6% 99.8% 99.7%

Phoenix, AZ 99.5% 99.8% 99.2%

San Diego, CA 99.6% 99.8% 98.3%

San Francisco, CA 94.7% 92.3% 98.3%

Seattle, WA 93.6% 92.9% 99.7%

St Louis, MO 89.8% 93.1% 99.6%

Tampa, FL 99.2% 91.2% 99.8%

Washington, DC 89.7% 99.8% 99.5%

United States Total 99.7% 98.6% 98.3%

Source: Lodging Analytics Research & Consulting2021 Outlook

2021 Top Performers (vs. 2019) 2020 Market

2021 Performance

Bottom Performers (vs. 2019)

Norfolk, Miami and Tampa: The only markets San Francisco, Boston, New York, Washington,

among the top-26 with RevPAR projected to D.C., and Seattle: Fly-to, High-Density,

exceed 2019 levels this year. They all have International-Focus

strong leisure activity and two of the three are

almost exclusively domestic markets.

RevPAR Growth Rates for the Top 26 Markets - 2021 vs. 2019

20%

10%

0%

-10%

-20%

-30%

-40%

-50%

-60%

-70%

Dallas, TX

New York, NY

Denver, CO

Miami, FL

Atlanta, GA

Orlando, FL

Los Angeles, CA

San Diego, CA

St Louis, MO

Las Vegas, NV

Phoenix, AZ

Seattle, WA

Boston, MA

Tampa, FL

Minneapolis, MN

San Francisco, CA

Honolulu, HI

New Orleans, LA

Anaheim, CA

Philadelphia, PA

Houston, TX

Nashville, TN

Chicago, IL

Norfolk, VA

Detroit, MI

Washington, DC

Source: Lodging Analytics Research & ConsultingRevPAR Recovery Back to 2019 Levels- Markets Diverge

% of Markets Reaching 2019 RevPAR by Year

Key Takeaways 70%

60%

• The majority of the 44 markets in our standard

coverage universe will recover to 2019 in 2023 or 50%

2024. However, some will diverge 40%

30%

• 3 will recover in 2021

20%

• 2 in 2022

10%

• 2 in 2025

0%

2021 2022 2023 2024 2025

• A faster recovery largely coincides with a higher Comparison of RevPAR recovery Year to

RevPAR looking out to 2025, but not always.

2025 RevPAR Premium to 2019 Levels

30%

There are several markets that won’t reach 2019

levels until 2023 or 2024 but will have higher 25%

2025 RevPAR vs. 2019

relative RevPAR by 2025 than markets that reach 20%

2019 levels in 2021 or 2022. 15%

10%

5%

0%

2020 2021 2022 2023 2024 2025 2026

Year Back to 2019 RevPAR

Source: Lodging Analytics Research & Consulting2025 Outlook Relative to 2019

Top Performers

Tampa: Strong economic growth, moderate supply growth and outsized exposure to domestic RevPAR Growth Rates for the Top 26 Markets – 2025 Outlook vs. 2019

leisure demand will make Tampa an outperformer. Additionally, with cap rates stabilizing only 30%

slightly above 2019 levels, 2025 asset values will be 18% above 2019 levels. 25%

20%

Phoenix: Strong economic growth will offset elevated supply growth, driving Phoenix operating

fundamentals to recover to 2019 levels at a swifter pace than most other major markets. We 15%

expect RevPAR to reach 2019 levels by 2022 and Hotel EBITDA by 2023. EBITDA growth, 10%

coupled with modest cap rate compression, will result in 2025 asset values that are 15% above 5%

2019 levels.

0%

Denver, CO

Dallas, TX

Orlando, FL

New York, NY

Las Vegas, NV

Los Angeles, CA

Atlanta, GA

St Louis, MO

Boston, MA

Miami, FL

San Diego, CA

Seattle, WA

San Francisco, CA

Anaheim, CA

Philadelphia, PA

Tampa, FL

Phoenix, AZ

New Orleans, LA

Houston, TX

Nashville, TN

Minneapolis, MN

Honolulu, HI

Norfolk, VA

Detroit, MI

Washington, DC

Chicago, IL

Denver: Fueled by above average economic growth and moderating economic supply growth,

Denver’s recovery is off to a strong start and is expected to accelerate into 2022. Outsized

economic growth will generate outsized ADR and RevPAR growth, while limited expense

growth will help drive outsized EBITDA growth. While cap rates will stabilize slightly below 2019

levels, EBITDA growth will be the primary driver of value appreciation as we expect 2025 asset

values to be 12% above 2019 levels. Source: Lodging Analytics Research & Consulting

Los Angeles: Once occupancy begins to recover, the market will have robust pricing power, Hotel Value Change for the Top 26 Markets – 2025 Outlook vs. 2019

driving outsized RevPAR and ADR growth. Elevated expense growth will mitigate some of the

20%

benefits of strong ADR growth, limiting EBITDA growth. However, EBITDA growth coupled with 15%

cap rate compression will result in 2025 asset values which are 10% above 2019 levels. 10%

5%

Nashville: Elevated supply growth will weigh on the market, preventing occupancy from fully 0%

recovering to 2019 levels by 2025. However, the market’s emergence as a three-demand- -5%

-10%

segment (corporate, group and leisure) locale will drive ADR and RevPAR to 2019 levels by -15%

2023. By 2025, Hotel EBITDA will be just 1% below 2019 levels, while cap rate compression -20%

drives 2025 asset values to be 7% above 2019 levels. -25%

Dallas, TX

New York, NY

Denver, CO

Los Angeles, CA

San Diego, CA

Miami, FL

Orlando, FL

Atlanta, GA

Seattle, WA

Las Vegas, NV

Boston, MA

St Louis, MO

Tampa, FL

Phoenix, AZ

Minneapolis, MN

Anaheim, CA

Philadelphia, PA

San Francisco, CA

New Orleans, LA

Honolulu, HI

Nashville, TN

Houston, TX

Detroit, MI

Chicago, IL

Washington, DC

Norfolk, VA

Source: Lodging Analytics Research & ConsultingThird Quarter Sentiment Shifts

Improving Outlook 2020Markets

Marketswith Greatestwith

Changes inlargest

Long-Term Value Change (vs. 2019)

Norfolk: Much stronger ADR growth through the summer leisure season indicates the market has

much more pricing power than previously expected. That will support stronger ADR growth, change Outlook vs. Last Quarter

Current Quarter Value Change

which will drive EBITDA and values higher. Last Quarter Value Change

13.6%

Anaheim & Orlando: The recovery of the theme park demand happened much more quickly than 15% Difference

anticipated. We now forecast these leisure heavy markets to recover more quickly than last 10% 6.9% 8.3%

quarter, particularly pertaining to ADR growth which fuel an increase in our EBITDA outlook, 3.9% 5.5% 4.2% 5.4% 4.2%

2.6% 3.6%

driving values higher.

5% 2.3%

Seattle: An improving economic outlook, across the market support an improvement to our long- 0%

term views on Seattle, making us less cautious on the market long-term. -5% -1.6% -1.2% -1.2%

-3.3%

-10% -6.0% -5.4%

Deteriorating Outlook -15% -11.1%

Atlanta

Orlando

Anaheim

Seattle

Boston

Norfolk

Boston: Our cap rate outlook, while still very positive is not as positive as a quarter ago, as rising

base rates, coupled with slowing fundamentals in the later years of our forecast weigh on Boston

values. We remain positive on Boston, but our outlook is moderating

Atlanta: Our models now forecast lower ADR growth over the long-term based on the components

Source: Lodging Analytics Research & Consulting

of economic growth across the market. That lower ADR growth will limit revenues and EBITDA

over the longer-term. That will weigh on cap rates and drive modest value erosion vs. our prior

forecast.Standard Pricing Product Standard Pricing December Promotion Single Report $2,000 - Single-Market Annual Contract $3,000 - (4 Quarterly Reports) Annual Contract - Full Research Platform $29,500 $19,500 • 4 Quarters of Reports • 26 Markets • U.S. Market Intelligence Report • Market Comparison Report • Excel Forecast Files • Access to LARC Team for assistance related to market analysis/understanding

Questions? If you are interested in access to LARC’s industry-leading Market Intelligence Reports, please contact us. information@larcanalytics.com

Better Lodging

Analytics For Better

Business Decisions

Ryan Meliker

President

200 West 41st Street, Suite 602

New York, NY 10036

929.416.4783

information@larcanalytics.comYou can also read