DAIRY INDUSTRY RESTRUCTURING ACT REVIEW - Initial Submission from Westland Milk Products - Te Uru Rākau

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DAIRY INDUSTRY RESTRUCTURING ACT

REVIEW

Initial Submission from Westland Milk Products

June 2018

Disclaimer

The economic modelling and expert comments in this report have been prepared by TDB Advisory Ltd

(TDB) for Westland Milk Products with care and diligence. The statements and opinions in this report

are given in good faith and in the belief on reasonable grounds that such statements and opinions are

correct and not misleading. However, no responsibility is accepted by Westland Milk Products, TDB or

any of its officers, employees, subcontractors or agents for errors or omissions arising out of the

preparation of this report, or for any consequences of reliance on its content or for discussions arising

out of or associated with its preparation.

2

Table of contents

1. Introduction and summary ............................................................................................................................................ 4

2. Background .......................................................................................................................................................................... 9

3. Is DIRA achieving its objectives .................................................................................................................................14

4. Regional development ..................................................................................................................................................38

5. Environmental considerations ....................................................................................................................................39

6. Fonterra Co-operative Group Limited.....................................................................................................................40

7. Conclusions ........................................................................................................................................................................41

Appendix 1: Calculation of Fonterra’s capital value including assumed merger benefits.............................43

List of tables

Table 1: Summary responses to MPI’s questions ............................................................................................................ 6

Table 2: Major farm gate competitors ...............................................................................................................................17

Table 3: Attributes of milk production changes since 2001 ......................................................................................19

Table 4: Farm gate competition............................................................................................................................................24

List of figures

Figure 1: Milk curves – international comparison..........................................................................................................10

Figure 2: Timeline of FGMP and commodity prices ......................................................................................................15

Figure 3: Dairy processing volume in NZ ..........................................................................................................................16

Figure 4: Farm gate competition in 2001 and 2017 .....................................................................................................16

Figure 5: Revenue per kgMS per processing company ...............................................................................................18

Figure 6: 7-year average adjusted ROA-WACC 2011-2017 .......................................................................................19

Figure 7: Farm gate competition ..........................................................................................................................................24

Figure 8: Milk production by region ...................................................................................................................................25

Figure 9: Three channels to market in domestically-focused dairy sector ..........................................................32

3

1. Introduction and summary

1.1 Introduction

Westland Milk Products (Westland) is a key economic driver of the West Coast economy and New

Zealand’s second biggest dairy cooperative. Dairy is also the biggest single contributor to GDP on the

West Coast and consistently contributes almost a quarter of a billion dollars annually ($234.4 million in

2016 alone.)

Westland has 342 shareholding farmers and over 420 supplying farms. It employs 555 staff in total as

well as indirect supplier jobs and contributes to considerable economic ‘spill overs’ to the region. During

the deliberations which became the Dairy Industry Restructuring Act 2001 (DIRA), Westland chose to

remain an independent processor in order to maintain processing on the West Coast. The company

believes that New Zealand needs strong independent processors that work as part of NZInc and that it

is very important to counter against any global perception of New Zealand having a state-supported

monopoly.

Westland agrees with our economic experts, TDB, in that the DIRA enabled Fonterra to be set up as a

near monopoly / monopsony in New Zealand’s dairy markets. DIRA was designed to be the counter-

balance. It included a number of provisions designed to foster competition at the farm gate and to

protect New Zealand dairy product consumers. The key “contestability” provisions that apply to

Fonterra are:

• open entry;

• open exit;

• no discrimination between suppliers;

• the right for Fonterra suppliers to supply up to 20 percent of their weekly production to an

independent processor; and

• the setting of the base milk price.

In addition, the Dairy Industry Restructuring (Raw Milk) Regulations 2012 (DIRA regulations) require

Fonterra to supply raw milk to Goodman Fielder and independent processors (IPs) subject to certain

conditions.

DIRA was originally envisaged as temporary legislation with automatic expiry provisions once certain

milk-supply thresholds were met. Those automatic expiry provisions have now been removed.

The objectives of the current review by the Government are to ask:

• is the DIRA regulatory regime operating in a way that protects the long-term interests of New

Zealand dairy farmers, consumers and the nation’s overall economic, environmental and social

wellbeing?

• does the DIRA regulatory regime give rise to any unintended consequences manifesting

themselves in other parts of the wider regulatory system and, if so, to what extent? and

4

• does the purpose and form of the DIRA regulatory regime remain fit-for-purpose, given the

dairy industry’s current structure, conduct and performance, as well as the global and domestic

challenges and opportunities facing the industry, the wider regulatory system within which it

operates, and the Government’s broader policy objectives?

1.2 Executive summary

The DIRA contestability provisions have helped protect the long-term interests of New Zealand dairy

farmers, consumers and the nation’s overall economic wellbeing. This is demonstrated by:

• farmers have an increasing level of farm gate competition;

• New Zealand consumers have been at least partially protected from the adverse impact of the

formation of Fonterra to the extent that there is more competition in the domestic market now

than there was, although in our opinion, regulatory changes are required to remove the

competitive limits unintentionally imposed; and

• the dairy industry continues to be an important contributor to New Zealand’s economic health.

It is recognised that the dairy industry’s environmental impact has worsened as intensification has

increased and as land has been converted to dairy. We consider that, at the margin, DIRA’s open-entry

provisions have contributed to this outcome and could be phased out without imposing significant

costs.

The poor environmental situation (and, probably more importantly, the industry’s slow and hesitant

response to it) means that there is a lot of discussion now about dairy farmers having lost their social

license to operate. From that perspective, we would argue that DIRA has not protected the nation’s

wellbeing. However, we would argue that any environmental protections required should be imposed

by generic environmental legislation rather than through DIRA.

The purpose of the DIRA regulatory regime remains fit-for-purpose, although we would recommend

the following changes:

• we contend that open-entry (and open re-entry) could be phased out. To be clear, by open

entry and open re-entry we mean milk from new dairy conversions. We do not mean that

Fonterra could not choose to collect milk from an existing dairy farm. Open entry has

contributed to the development of marginal farming land so we would be happy to have that

area closed to entry. We do not want to see a situation whereby any farmer would not have

their milk collected;

• the base milk price provisions remain crucial, but we would recommend a number of changes

to the milk price methodology as follows:

− Fonterra’s average currency conversion rate should be excluded from the calculation,

− non-Global Dairy Trade sales should be excluded from the calculation, and

− the asset beta used should not be that of the hypothetical efficient processor, but that

of the industry. (Note – this is a different discussion to the one that the Commerce

Commission is currently consulting on.);

5

• the special provisions relating to Goodman Fielder should be removed and Fonterra should be

required to supply 100 percent of the raw milk required by any domestic dairy products market

competitor; and

• full accounting separation and reporting of Fonterra and FBNZ should be required.

The recommended changes to the milk price methodology are intended to increase the transparency

of the calculation. Currently, Westland believes Fonterra’s prices appear to be unacceptably

manipulated.

With regard to the domestic market, the highly seasonal nature of the milk production in New Zealand,

relative to the pattern of domestic demand, and the absence of a factory gate market mean that

domestic competitors are largely reliant on Fonterra for their milk supply. The raw-milk supply

provisions, therefore, essentially limit the size of domestic competitors by limiting their access to 50M

litres of milk (or 250M litres in the case of Goodman Fielder (GF)). We consider that the individual

company limits should be removed and all potential suppliers to the domestic market be treated equally

in terms of their access to Fonterra milk. Full accounting separation and reporting of Fonterra and FBNZ

is required to ensure that FBNZ’s ability to compete in the domestic market is not being subsidised by

another part of the business.

Westland believes that there are some unintended outcomes from the DIRA such as the dominant player

mentality displayed by Fonterra. We want measures in place that prevent discriminatory behaviour. For

this we see a need for the legislation to potentially be strengthened in a way that prevents abuse of

market power and the maintenance and encouragement of true contestability.

Table 1: Summary responses to MPI’s questions

Question Summary response

1. Benefits of 2001 industry • There is little evidence that Fonterra has delivered the

restructure realised? anticipated benefits to farmer/shareholders

• The anticipated benefits for farmer/shareholders were $310

million per annum

• We estimate that those benefits should translate into a

theoretical share price now of $8.43 versus the current actual

price of $5.15

• We estimate that, in the absence of those benefits, the

theoretical share price now should be $6.07

2. Is the DIRA contestability • Leaving aside the original mega-merger, performance and

regime contributing to competition within the dairy sector has not been impeded by

and/or impeding the DIRA

sector’s performance? • Fonterra’s farm gate market share has decreased by 14

percent in 16 years – from 96 percent to 82 percent

• Five new IPs have started up since Fonterra was established,

with one of those failing. An additional two new IPs have

announced their intention to build new processing plants.

Along with Westland and Tatua, the addition of the two new

companies would bring the total number of IPs competing

with Fonterra at the farm gate to eight

• The organisational structures of IPs range from co-operative

companies to private companies to publicly listed companies

6• The strategies employed by the IPs range from commodity to

business-to-business to consumer products

• We estimate that capital of approximately $19 billion has

been invested by the processors since 2001

3. Who is benefiting? • Farmers – the amount of on-farm investment since 2001

indicates that farmers have been earning an adequate return

on their investment

• Processing company shareholders – the return on asset

performance of the IPs vis-à-vis their capital cost is variable

• NZ Inc – the contribution of the sector to the NZ economy

continues to be significant

• However, it is generally accepted that the environment has

suffered as a consequence of dairying. It could be argued that

DIRA has contributed to that outcome

4. What incentives exist for • There isn’t any incentive but neither is there any disincentive

the dairy industry to • Moving up the value chain brings potential for higher

transition to higher value investment returns

products? • Moving up the value chain also increases risk

• The challenge for companies is to create value rather than to

necessarily move up the value chain

• The Government’s role is to create an environment that allows

the processors and their shareholders to make their own

decisions about their business strategy and how much risk

they want to take

5. Are the current • The incentives and ability for Fonterra to operate to the

contestability provisions detriment of the long-term dynamic efficiency of the broader

still fit-for-purpose? dairy industry remain and, with stalled milk growth, might be

stronger now than they were in 2001

• There is more competition at the farm gate now than there

was in 2001 and there have been a number of

announcements since the last Commerce Commission review

regarding increasing competition at the farm gate

• There is more domestic consumer market competition now

than there was in 2001, although there are a number of

unintended consequences with respect to the raw-milk

supply provisions

• No factory gate market has developed

6. What changes are • The open-entry provision is no longer required

required? • The base milk price provision is still required but changes are

7. Are changes to the industry needed to make the calculation of the FGMP more

and/or the DIRA regulatory transparent

regime required? • Fonterra’s obligation to supply raw milk destined for the

domestic market to competitors should not be capped

8. Is the domestically-focused • The domestic market is still dominated by the same two

dairy sector operating in companies (although one has a different owner – GF)

the long-term interests of • In the grocery channel, we estimate that Fonterra and GF’s

New Zealand consumers? combined market share has decreased by 8 percent (from

approximately 95 percent to 87 percent) since 2001

7• The milk-supply volume limits do not restrict the number of

domestic competitors that could emerge but do

unnecessarily limit the absolute and relative size of any of

those competitors in an environment of domestic market

growth

9. Are there significant • Yes – in two areas – collection costs and capacity costs

economies of scale in the • The domestic market requires a flat milk curve supplying

collection, processing, and constant monthly milk volumes

wholesale distribution of • The NZ milk-production curve is not flat. There is twenty times

into domestic consumer more milk produced in the peak month than there is in the

markets? low month

• We estimate that 10 to 15 percent of Fonterra suppliers

supply winter milk

• A larger proportion would require the processor to either pay

higher winter-milk premiums than Fonterra or to travel

further to collect milk

• A larger proportion would require the processor to hold more

capacity in reserve to manage daily demand fluctuations

10. What would the • The absence of DIRA regulations would lead to fewer

domestically-focused dairy competitors and higher prices for domestic consumers as per

sector look like in the the Commerce Commission’s 2016 report

absence of the DIRA

regulations?

11. Does the DIRA regulatory • Yes – the regulatory objective remains fit-for-purpose,

objective of ensuring although changes to the regulations are required to remove

“competition in the the disincentive that potential domestic competitors have to

wholesale supply of invest, and to remove the regulatory limits on the size of

domestic consumer dairy individual competitors

products” remain fit-for-

purpose?

12. What changes would be • Fonterra’s obligation to supply raw milk destined for the

required to ensure that the domestic market to competitors should be unlimited

DIRA regulatory regime • That obligation needs to be on-going and needs to survive

supports a well-functioning any future phasing out of the other contestability provisions

domestically-focused dairy • Fonterra should be obliged to separately account for and

sector that operates in the report on its domestic consumer brands business ‘Fonterra

long-term interests of New Brands New Zealand’, to demonstrate that its financial

Zealand consumers? performance is not being subsidised by some other part of

the business

82. Background

2.1 Context

Total global annual milk production is estimated to be around 500 billion (B) litres of milk 1. The size of

the internationally traded dairy-products market is estimated to be the equivalent of around 65B litres,

or around 15 percent of total production.

New Zealand’s annual milk production is estimated to be approximately 21B litres (or less than 5 percent

of global production), of which, approximately 5 percent is consumed domestically and 95 percent is

exported. New Zealand’s share of the internationally traded dairy-products market is approximately 30

percent, or 20B litres p.a.

While being able to produce huge volumes at internationally competitive prices is positive, there are

aspects of the New Zealand industry that are very challenging, including the proportion of production

that needs to be exported, the consequent exposure to international prices, the distance from export

markets and the shape of the seasonal milk curve.

The New Zealand dairy industry is internationally cost-competitive, in part because New Zealand’s

temperate climate and abundant water allows the farming system to be a pasture-based system where

milk production matches grass growth. The pasture-based system, however, means milk production is

highly seasonal, with milk production in the peak month (October each year) being typically 20 times

as large as milk production in the slowest month (June each year).

Given the seasonal milk curve and the non-seasonal nature of domestic demand, it is no surprise that

the original two large pre-Fonterra domestic businesses were subsidiaries of very large export

businesses (NZ Co-operative Dairy Group Ltd (NZDG) and Kiwi Co-operative Dairies Ltd (Kiwi)). Both

NZDG and Kiwi had large ingredient businesses to funnel their excess milk through to manufacture and

export as long-life products (through the New Zealand Dairy Board at the time).

As Figure 1, below, illustrates, the shape of the seasonal milk curve in New Zealand is much more

extreme than in the US or EU.

1

USDA, Dairy: World Markets and Trade, December 2016.

9Figure 1: Milk curves – international comparison

These peak to trough variations graphically illustrate the difficulty the New Zealand milk curve causes

New Zealand processors, especially those who are focused on the domestic market.

2.2 Historical development of DIRA

New Zealand’s largest dairy processor, the co-operative company Fonterra, was established in 2001

from an amalgamation of the then two largest dairy co-operatives: NZDG and the New Zealand Dairy

Board. In forming Fonterra, participants sought to realise efficiencies of scale and scope in the collection

and processing of farmers’ milk, so as to better compete in international dairy markets, for the overall

benefit of New Zealand.

At the time, the value of the benefits of the mega-merger (ie, Fonterra) to New Zealand farmers was

estimated to be $310M 2 p.a., or almost $2.5 billion (B) on a capitalised present value basis 3.

On creation, Fonterra collected approximately 96 percent of New Zealand’s raw-milk production.

Allowing the creation of such a dominant firm had competition policy implications. In particular, a

dominant firm could have:

• the incentives and ability to create barriers to farmers switching to potential competitors;

• the incentives and ability to impede entry into the farm gate market by new dairy processors;

2

“The Quigley report on dairy megamerger”, 24 January 2001. Section 4.1 of the Quigley report refers to the“Business Case for

Global Dairy Co Ltd: Executive Summary”that outlines the sources of the $310M in benefits that were claimed to be associated

with the merger.

3

Using Fonterra’s FY16 pre-tax WACC of 7.9% to capitalise a benefit expressed in 2001 dollar values.

10• the incentives and ability to set wholesale prices in downstream domestic dairy markets; and

• fewer incentives to drive cost efficiencies and invest in innovation, as it could use its market

position to retain farmer suppliers even if they were dissatisfied with the company’s

performance.

The Dairy Industry Restructuring Act, 2001 (DIRA) authorised the amalgamation and allowed it to bypass

the Commerce Commission. The Commerce Commission’s earlier draft determination found that the

merger would result in a strengthening of a dominant position in each of the relevant markets 4.

As the amalgamation resulted in an entity with a substantial degree of market power in several New

Zealand dairy markets, DIRA was designed and implemented to mitigate the risks of Fonterra's market

power. In particular, DIRA seeks to promote contestability in the New Zealand raw-milk market and

provides for access for other dairy goods or services supplied by Fonterra to be regulated, if necessary.

Regulations made under the Dairy Industry Restructuring (Raw Milk) Regulations, 2001 (and as amended

and re-enacted in 2012) contain further provisions to facilitate the entrance of independent processors

(IPs) to New Zealand dairy markets and enable them to obtain the raw milk necessary to compete in

dairy markets.

The original regulations required Fonterra to supply, at a DIRA price, up to 50M litres of raw milk p.a. to

any IP and up to 250M litres p.a. to Goodman Fielder (GF). The price of this regulated raw milk was the

farm-gate base milk price (FGMP) 5 for that season, plus reasonable transport costs.

An IP, in DIRA:

• is defined as a processor of milk, milk solids or dairy products that is not associated with

Fonterra; and

• includes GF and any associated person of that company, other than Fonterra.

IPs, therefore, include the obvious companies such as Tatua and Westland, but also the less obvious

companies like GF and Cadbury 6. The latter IPs outsource their raw-milk supply to vertically integrated

dairy processors, rather than sourcing it directly from farmers.

The default price specified in the regulations is a calculated price that is meant to ensure the following

outcomes:

• Fonterra is constrained from offering farmers a higher price for their milk. This reduces the risk

of Fonterra being able to offer a higher FGMP to limit the ability of competing processors to

persuade farmers to switch to supplying them; and

4

The Commerce Commission had reached the preliminary conclusion, in 1999, that the merger that formed Fonterra could not

be authorised under the Commerce Act. The Commission’s preliminary estimate was that the merger would result in a price rise

in domestic dairy-products markets (other than spreads) of between 10% and 20%. This translates to a wealth transfer from

domestic consumers to the merged entity (Fonterra) of between $75M and $146M p.a., and a net deadweight welfare loss in the

domestic dairy production and supply markets of up to $4M p.a. This deadweight loss included both allocative losses in the

domestic dairy products-market and dynamic efficiency concerns.

5

The FGMP is a notional calculation of the cost of milk supplied to Fonterra on the basis that Fonterra is an efficient processor.

6

Supermarkets do not meet the definition of an IP under DIRA and do not have any direct access to DIRA milk.

11• from a domestic consumer perspective, competition in the domestic market between wholesale

companies is sufficient to ensure that Fonterra does not have the power to charge prices in

excess of what is required to generate an adequate return on capital employed.

Thus, the DIRA contestability provisions were designed to ensure that milk flows to the highest-value

user (whether the user is a producer of dairy commodities, ingredients or fresh consumer products) and

to avoid wealth transfers from domestic consumers to Fonterra. The provisions work in parallel with,

and are supplementary to, the general competition provisions of the Commerce Act, 1986.

2.3 Changes to DIRA Regulations in 2012

The 2001 Regulations were revoked on 1 June 2013 and replaced by the Dairy Industry Restructuring

(Raw Milk) Regulations, 2012 (“the 2012 Regulations”).

Under subpart 1 of the 2012 Regulations:

• the total amount of raw milk to be supplied by Fonterra to IPs increased from 600M litres per

season to 795M litres per season;

• the total amount of raw milk to be supplied by Fonterra to GF was unchanged, at 250M litres

per season, but supply in the non-winter months was limited to 110 percent of the amount of

raw milk supplied in the preceding October;

• the total amount of raw milk to be supplied by Fonterra to any one individual IP was unchanged,

at 50M litres per season, but maximum monthly limits for non-winter milk were put in place;

and

• the obligation on Fonterra to supply raw milk to an IP in a season beginning on or after 1 June

2016 was extinguished if that IP’s own supply of raw milk in the three previous seasons was

30M litres or more.

Subpart 3 of the 2012 Regulations divided IPs into two categories:

• those with no, or less than 30M litres of own-supply raw milk; and

• those with more than 30M litres of own-supply raw milk and those that do not require a fixed

quarterly raw-milk price from Fonterra and GF.

For the first group, the new regulations changed the price of raw milk supplied by Fonterra from the

FGMP plus $0.10 per kilogram of milk solids (plus transport costs and winter-milk premiums) to a fixed

quarterly price being Fonterra’s most recent forecast FGMP (plus transport costs and winter-milk

premiums).

For the second group, the new regulations changed the price of raw milk supplied by Fonterra from the

FGMP plus $0.10 per kilogram of milk solids (plus transport costs and winter-milk premiums) to the

FGMP (plus transport costs and winter-milk premiums).

122.4 The Dairy Industry Restructuring Amendment Bill, 2017

In March 2017, as a consequence of the recommendations made by the Commerce Commission and a

subsequent MPI-led review, the then-Minister introduced into the House the Dairy Industry

Restructuring Amendment Bill. That Bill was subsequently substantially altered by the new Government

before being passed into law on February 15, 2018.

The changes made to the DIRA by the amendment prevent the relevant DIRA provisions from expiring

in the South Island and remove the market share thresholds that would trigger the Act’s expiration in

the future. The other provisions that were set out by the original Bill (under the previous Government)

were removed 7.

In removing the previous provisions which timetabled a further review for 2020/21, the new Government

announced its intention to “undertake a comprehensive review of the DIRA and consult fully with the

dairy sector” 8, commencing in 2018.

7

The original Bill (among other things):

− removed the default expiry provisions and the market share thresholds in the North and South Islands that trigger a

review of the state of competition;

− required a review of the state of competition to commence during the 2020/21 dairy season;

− required a review at five-year intervals thereafter if competition has not yet been considered sufficient;

− allowed Fonterra the discretion to refuse supply from new dairy conversions;

− reduced the total volume of raw milk that Fonterra must supply to IPs from 795M litres to 600M litres per season; and

− removed the requirement for Fonterra to supply DIRA milk to large export-focused processors from the beginning of

the 2019/20 season. The definition of a large export-focused processor was one that has the capacity to process more

than 100M litres of milk per season and exports more than 50% of its production by volume.

8

https://www.beehive.govt.nz/release/dairy-industry-restructuring-amendment-bill-passed

133. Is DIRA achieving its objectives

3.1 Introduction

There are two components to the question ‘is DIRA achieving its objectives?’:

• have the originally anticipated benefits been realised?; and

• has DIRA enabled competition to emerge?

These two questions are answered in turn below.

3.2 To what extent have the anticipated benefits of the 2001 industry

restructure been realised?

As noted in section 2.2, above, the anticipated benefits of the establishment of Fonterra were $310

million per annum 9. The sources of the benefits were anticipated to be as follows:

• annual cost savings in the order of $120 million as a consequence of the elimination of

duplicated facilities and activities;

• annual revenue enhancements and productivity improvements in the order of $70 million as a

consequence of enhanced economies of scale and scope if manufacturing activities are

integrated with marketing and distribution functions; and

• additional increased earnings of $120 million per year as a consequence of being able to

harness the synergies between different parts of the industry, provide fresh strategic impetus

and broaden options to exploit new market, technology and biotech opportunities.

We would expect to be able to measure the realisation of the benefits with reference to Fonterra’s share

price as follows (details of the calculations are provided in Appendix 1):

• the expected benefit in 2001 was $310m per year to farmer-shareholders. If we assume that the

expected benefit was expressed in pre-tax terms, it would equate to $223m after tax;

• if we assume an average cost of equity for Fonterra of 9 percent, an average dividend ratio of

70 percent, and add all the new equity associated with increased production, we estimate that

the current share price should be $8.43;

• Fonterra’s current share price is $5.15;

• if we exclude the anticipated benefit from the theoretical share price calculation, the current

share price should be $6.07; and

• we note that since Fonterra’s change in capital structure in 2012, its share price has averaged

$6.10 with a range of $4.60 to $8.08. We also note that over the same period of time, Fonterra’s

normalised EBITDA has increased by 0.6 percent, year-on-year 10.

9

Refer to footnote 2 above.

10

ANZ Research, Agri Focus – we have lift off, June 2018, p.24.

14The logic employed above would lead us to conclude that there is little evidence that Fonterra has

delivered the anticipated benefits to farmer / shareholders.

However, it should be noted that Fonterra, like most companies, has been subject to some adverse

shocks over the period (like the GFC and WPC80 crisis) that will have affected its financial performance.

We do not think that it could be argued that the benefit has been passed through to shareholders via

the FGMP. In the first instance, the anticipated benefits can only be achievable as a consequence of the

merger and not otherwise. We can observe that most of the IPs are paying slightly more than the FGMP

to their suppliers for their milk on average and are earning more than their required rate of return, which

implies that the merger was not required for any benefits to be received via the FGMP. In addition,

Figure 2, below, indicates that the FGMP has generally been consistent with international commodity

prices.

Figure 2: Timeline of FGMP and commodity prices

Similarly Westland does not think it can be argued that the costs imposed on Fonterra by DIRA have

therefore been excessive. The contestability provision that has received the most attention by Fonterra

(and has subsequently been changed most significantly as a consequence) is the raw-milk supply

provision. We estimate that the opportunity cost to Fonterra of having to sell raw milk to IPs at the

FGMP has been approximately $25-$30 million per annum.

DIRA, by allowing the mega-merger to be formed without going through the normal Commerce

Commission process, was a major step. DIRA itself was an attempt to offset the adverse competition

effects of the merger. DIRA has been reasonably successful in this regard. Figure 3, below, presents a

time series of dairy processing volumes in New Zealand since 1983.

15Figure 3: Dairy processing volume in NZ

3.3 To what extent and in what way is the DIRA contestability regime

contributing to or impeding the sector's performance?

Figure 3 shows no notable change in the trend in New Zealand’s milk production following Fonterra’s

creation (although New Zealand has likely now reached (or passed) peak cow numbers, which will see

continuing growth in milk production stall or at least slow considerably from now on). In our opinion,

this overall trend indicates that DIRA has not impeded industry growth.

3.3.1 Farm gate competition

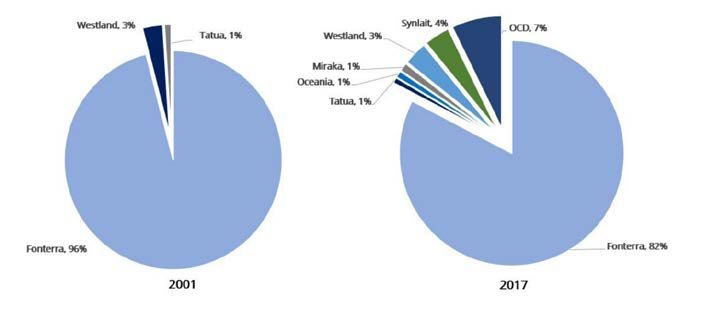

As presented in Figure 4, in addition to volume growth in the industry, the market share of competition

at the farm gate has increased from 4 percent to 18 percent over the last 16 years.

Figure 4: Farm gate competition in 2001 and 2017

In 2001, directly following the formation of Fonterra, there were three processors competing at the farm

gate in the New Zealand dairy industry with Fonterra being almost completely dominant, processing 96

16percent of all volume collected. Since then, although Fonterra’s collection volumes have continued to

grow, its market share (in terms of New Zealand milk collected) has fallen to 82 percent.

The market share that has been captured from Fonterra has been distributed across multiple

competitors in the farm gate market that have varying corporate structures and strategic objectives.

Apart from Fonterra there are now six IPs competing at the farm gate and collecting 18 percent of New

Zealand’s raw milk. An additional two IPs have announced their intentions to build new processing

plants in the near future (subject to milk supply).

3.3.2 Industry composition

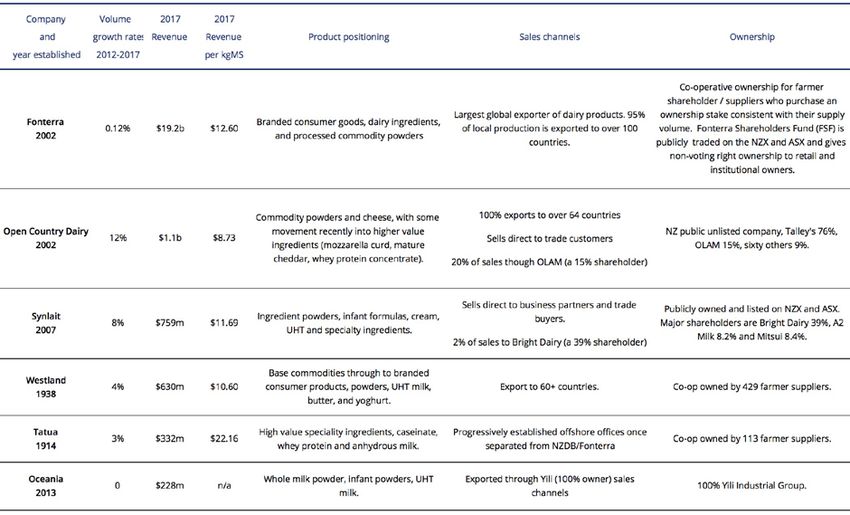

Table 2 presents an overview of the major competitors at the farm gate (based on publicly available

information). The table notes when each company was established, their total revenues in the 2017

financial year, their revenues per kgMS (which indicates where in the value chain they compete), their

product positioning and their ownership structure.

Table 2: Major farm gate competitors

In 2001, the three competitors in the processing sector (Fonterra, Westland and Tatua), were all co-

operative companies. Since 2001, new processing firms have emerged with differing corporate

structures. OCD is a public unlisted company. Synlait is publicly listed on the NZX and the ASX. Oceania

is a wholly owned subsidiary of a major foreign company.

The nature of each processing business has also varied, with some processors like OCD continuing to

be focused on commodity processing for the export market, other new entrants focusing on the

ingredients and consumer business segments and incumbent competitors diversifying away from

commodity processing into ingredients and consumer segments.

17Our conclusion is that DIRA has contributed to increasing competition at the farm gate without placing

significant structural constraints around the way in which that competition has emerged.

Figure 5 presents the 2017 firm revenue per kgMS.

Figure 5: Revenue per kgMS per processing company

Figure 5 highlights the variation in strategy and market positioning in the industry. Revenue per kgMS

gives insight into the product mix, as it gives both an indication of sale price of products per unit of

milk processed and the cost of production. The pure commodity value calculated for the hypothetical

efficient processor (HEP) used for the calculation of the FGMP was $8.13 for the 2017 season. OCD (as

noted above) is close to a commodity processor and only competes in the export market. Its revenue

per kgMS of $8.73 is close to that of the notional processor. Revenue per kgMS increases with Fonterra,

Synlait and Westland as, in addition to commodity products, they also compete in the ingredients and

the consumer markets, both domestically and internationally. A2 Milk is a consumer company and

outsources its processing. Tatua is a processor of speciality ingredients and has the highest level of

revenue per kgMS processed (and the highest cost of production).

Figure 5 shows that the sector in general is now made up of a diverse array of corporate strategies and

that DIRA has contributed to increasing competition at the farm gate, without placing structural

constraints around the way in which that competition has emerged.

3.4 Where and by whom are the benefits of the sector’s performance being

captured and the costs / risks incurred?

We would expect to see the benefits and the costs of the sector’s performance being captured by

farmers, by the processing companies’ shareholders and the broader economy generally. We think that

leaving aside how the market may have evolved in the absence of DIRA, the cost to the broader

economy has been largely environmental.

183.4.1 Farmers

Total milk production in New Zealand has increased by 60 percent since Fonterra was established in

2001. Part of that increase in production has been the result of improving genetics (animals and pasture)

and farmers investing in more intensive, higher cost farming systems leading to higher production per

hectare. The other part of the increase has been the result of farmers converting more land to dairy.

Table 3: Attributes of milk production changes since 2001

Source: New Zealand Dairy Statistics 2016-17, LIC - DairyNZ

Table 3, above, records the breakdown of the changes in milk production on-farm since 2001. We

conclude that the continuing investment by farmers in both productivity improvements and land

suggests that farmers have been earning an adequate return on their capital for the risks being taken.

3.4.2 Processing company shareholders

While on-farm investment by farmers seems to indicate that farmers believe that they are being

adequately rewarded for the risks they are facing, it is not at all clear that the same can be said for the

milk-processing companies’ shareholders. We have measured the investment performance of Westland,

Fonterra, Synlait, OCD and Tatua by subtracting their weighted average cost of capital from their return

on assets to see which companies have generated an adequate return and which haven’t. We have used

the FGMP to adjust each company’s reported earnings to make their relative performances comparable.

Figure 6: 7-year average adjusted ROA-WACC 2011-2017

19Figure 6 indicates that both Westland’s and Fonterra’s capital providers (and therefore shareholders)

have not received an adequate return on capital employed, while Synlait’s, OCD’s, and Tatua’s have 11.

We have not analysed the causes of any under or over-performance, although it is unlikely that DIRA

was a major factor in the differing returns.

3.4.3 Macro economy

According to the New Zealand Institute of Economic Research, from a macro-economic perspective, it

is estimated that the dairy sector 12:

• contributes $7.8 billion (3.5 percent) to New Zealand’s total GDP, comprising dairy farming

($5.96 billion) and dairy processing ($1.88 billion);

• supports rural New Zealand, with the sector accounting for 14.8 percent of Southland’s

economy, 11.5 percent of the West Coast, 10.9 percent of the Waikato, 8.0 percent of Taranaki

and 6.0 percent of Northland;

• remains New Zealand's largest goods export sector, at $13.6 billion in the year to March 2016.

Export growth has averaged 7.2 percent per year, over the past 26 years, faster than any primary

industry apart from the wine and ‘wood and wood products’ industries;

• exports twice as much as the meat sector, almost four times as much as the ‘wood and wood

products’ sector and nine times as much as the wine sector;

• accounts for more than one in four goods export dollars coming into New Zealand;

• employs over 40,000 workers, with dairy employment growing more than twice as fast as total

jobs, at an average of 3.7 percent per year since 2000;

• creates jobs at a faster rate than the rest of the economy in all but 5 territorial authorities across

New Zealand;

• provides over 1 in 5 jobs in three territorial authority economies (Waimate, Otorohanga,

Southland); and over 1 in 10 in a further eight (Matamata-Piako, South Taranaki, Hauraki, Waipa,

South Waikato, Clutha and Kaipara);

• delivered $2.4 billion in wages to farmers and processing workers in 2016;

• supports a range of supplying industries; in 2016, farmers spent $711 million on fertilisers and

agro chemicals, $393 million on forage crops and bought over $190 million of agricultural

equipment. Farmers also spent $914 million on agricultural services, $432 million on financial

services and $197 million on accounting and tax services; and

• as well as taking farmers’ raw milk, the dairy processing sector also spends significant amounts

on packaging ($288 million in 2016), hired equipment ($199 million) and plastics ($174 million).

11

This measure is a proxy shareholder measure because the companies’ assets are funded via both debt and equity but it is a

reasonable measure.

12

“Dairy trade’s economic contribution to New Zealand”, NZIER report to DCANZ, February 2017.

203.4.4 Environment

It is generally accepted that the environment has suffered as a consequence of the performance of the

dairy industry. From the dairy industry’s perspective, and leaving aside the behaviour of individual

participants, it has been operating to applicable laws and regulations and they have been tightened as

their inadequacies have been revealed.

It might be reasonably argued that DIRA has contributed to poor environmental outcomes by

incentivising the conversion of land to dairy that probably should not have been and otherwise probably

would not have been converted. An obvious example would be the Mackenzie Country land. The open-

entry provisions require Fonterra to accept all the milk that farmers want to supply. This means that

farmers could have converted cheap (and therefore, by definition, marginal) land into dairy if it was

economical to do so, knowing that Fonterra would have to collect the milk. This point is expanded upon

in section 5.

3.5 What and how strong are the existing incentives and disincentives for the

dairy industry to transition to a higher-value based dairy production and

processing industry, that global consumers seek out, for a premium?

In our opinion, the challenge for dairy companies (like other companies in the economy) is not

necessarily to move up the value chain, but to create value. Creating value is not necessarily the same

as moving up the value chain. Economic value is created if the return earned on the capital employed

is greater than the cost of the capital employed. From that perspective, if we refer back to Figure 6,

above, we can observe that Synlait, OCD, and Tatua have created value, on average, over the last seven

years and Fonterra and Westland have not.

The cost of the capital employed is lowest when companies operate at the low-risk end of the risk

spectrum, which means that the required return on the capital employed to compensate for this cost is

also lowest at that point. For milk processing companies, the low-risk end is the commodity-production

end because the margin earned by the processors is relatively constant, as the processors are able to

pass the majority of the commodity=price risk back to the farmer suppliers.

Risk increases as a company moves up the value chain because:

• production is more capital intensive;

• production is more difficult;

• the margin earned becomes more variable, as increases in milk prices take time to be passed

through to the consumer, while the consumer expects immediate relief when milk prices

decrease;

• stock becomes obsolete as tastes change; and

• there is a constant need to invest in research and development.

OCD is the closest example there is in New Zealand to a commodity product manufacturer (ie, a

company at the low end of the value chain) and it has successfully created value. Tatua is probably the

company that has positioned itself furthest away from the commodity end and therefore is probably

21the riskiest of the processors and it similarly has successfully created value. Synlait is somewhere

between the two in terms of risk and it has created value. Fonterra and Westland are probably similar

to Synlait in terms of overall average position on the value chain, but they have lost value, on average,

over the last seven years. In other words, moving up the value chain involves taking more risk and there

is no guarantee that it will add value for shareholders, or the economy.

Rather than seeking to promote so-called “high value” or “low value” products, the government’s role

is to create an environment that allows dairy companies to adopt the strategies that best meets their

objectives, manages their risks and makes the best risk-adjusted return possible for their

suppliers/shareholders.

The current regulations, appropriately, do not appear to provide any strong incentive or disincentive for

companies to move up or down the value chain.

3.6 Does the DIRA regulatory objective of ensuring “contestability for the

supply of milk from farmers” remain fit-for-purpose?

3.6.1 Incentives

The key competition concern with a company such as Fonterra having such a dominant position in the

market for farmers’ raw milk is that it could have the incentive and ability to operate to the detriment

of the long-term dynamic efficiency of the broader dairy industry. By declining applications for new

supply, paying inefficiently high milk prices to existing suppliers and retaining the value of the exiting

supplier’s capital contributions for as long as possible after they ceased to supply milk, it could “lock in”

its suppliers. Such actions would create significant barriers to entry for those seeking to compete for

farmers’ raw milk and allow Fonterra to operate inefficiently, but nevertheless remain in business.

To address this concern, the DIRA requires Fonterra to operate an open entry and exit regime. This

means that Fonterra must accept all milk-supply offers from dairy farmers in New Zealand and allow

relatively costless exit from the co-operative, upon the request of farmer-shareholders. These

requirements ensure that Fonterra cannot “lock in” its farmer-suppliers, and, as a consequence, Fonterra

faces strong commercial incentives to pay efficient prices for farmers’ raw milk and the capital invested

in Fonterra.

The Commerce Commission reviewed the state of competition in New Zealand dairy markets and

released its final report in March 2016. The Commission concluded at that time there was not sufficient

competition at either the farm gate or the factory gate to consider full deregulation.

Since the last Commerce Commission review, there have been a number of additional processing

capacity investment or announcements by the competing processors:

• OCD has built a new processing plant in Horotiu (Waikato) with milk processing due to

commence for the 2018/19 season;

• Mataura Valley Milk has built a new plant in McNab (Gore, Southland) with milk processing due

to commence for the 2018/19 season;

• Oceania (Glenavy, South Canterbury) intends to increase its capacity by 50 percent, although

the timing of this expansion is not clear;

22• Synlait has announced the purchase of land to build a second processing plant – to be located

in Pokeno (north Waikato). The plan is for this plant to be processing milk for the 2019/20

season; and

• Happy Valley Milk has announced the construction of a new plant to be built in Otorohanga.

The company has received land use consent and the plant could be ready for the 2020/21 milk

season.

It is not clear exactly how much additional capacity is implied by these announcements, but we estimate

that it could be around 1 billion litres of milk, which equates to approximately 4.5 percent of New

Zealand’s total milk production.

We are not suggesting that this additional capacity necessarily represents sufficient additional

competition such that the Commerce Commission might conclude differently to what it did in March

2016. However, on the assumption that there isn’t any increase in milk production in the next three

years and, in order for these plants to be full, Fonterra is most at risk of losing milk supply. To the

absence of (particularly) the base milk price contestability provisions, Fonterra would have a strong

incentive to transfer profits into the FGMP in order to retain milk. The Fonterra shareholders who would

be most affected by such a transfer would be the 12 percent of shareholders who are not also suppliers.

Shareholder-suppliers are not affected at all by this transfer because, in total, they would still receive

the same amount of cash from Fonterra with the increase in milk price, offsetting a decrease in the

dividend.

We note that the milk-price principles in Annexure 1 of Fonterra’s constitution require the milk price to

be the maximum it can be.

3.6.2 Farm gate competition

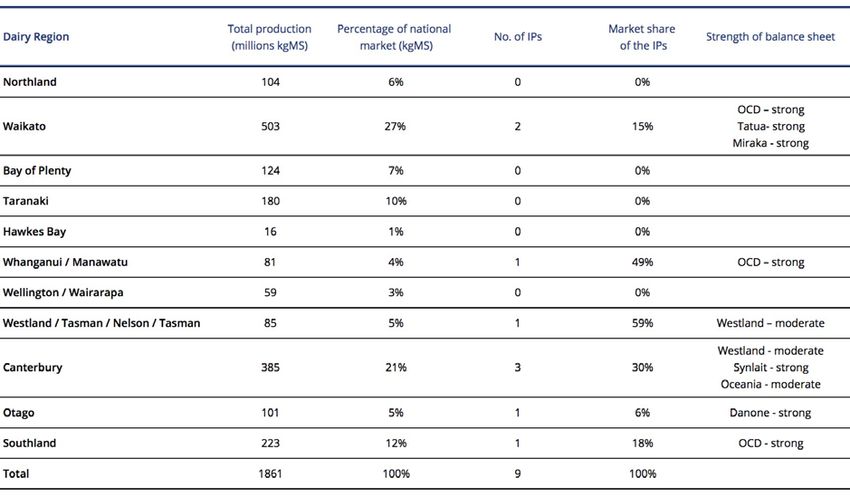

Table 4, below, is our estimate of where there is farm gate competition in New Zealand. The points to

note are:

• there are two regions where there are more than one IP competing with Fonterra at the farm

gate – the two biggest producing regions in New Zealand: Waikato and Canterbury;

• 5 of the 11 regions have no direct competition at the farm gate (including West Coast, where

Westland is currently the only processor); and

• while there is direct farm gate competition in the regions where 74 percent of New Zealand’s

milk is produced, the current capacity of the IPs limits their immediate competition to

approximately one quarter 13 of that milk.

13

18% / 74% = 24%.

23Table 4: Farm gate competition

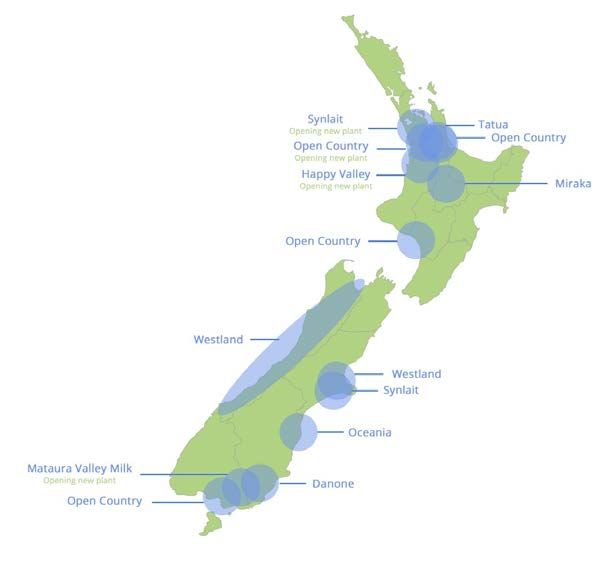

Figure 7, below, shows the location of the existing IPs, the intended locations of their new processing

plants (Synlait in Pokeno, OCD in Horotiu, and Oceania in Glenavy) and the yet-to-be built IPs (Happy

Valley Milk (Otorohanga) and Mataura Valley Milk (Gore)). As can be seen, the most intensive

competition is in Waikato. This is set to escalate, with Waikato being the location of three of the five

new processing plants.

Figure 7: Farm gate competition

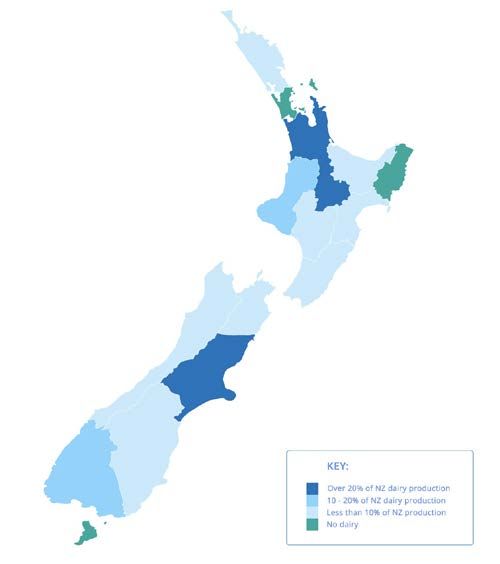

24Figure 8, below, illustrates regional milk production, with Waikato and Canterbury both producing in

excess of 20 percent of New Zealand’s milk and together accounting for almost half of New Zealand’s

milk. Taranaki and Southland each produce more than 10 percent of New Zealand’s milk and together

account for almost a quarter of New Zealand’s milk. The other seven milk producing regions each

produce less than 10 percent of New Zealand’s milk and there are three regions that produce no milk

at all (Auckland, Poverty Bay, and Stewart Island).

Figure 8: Milk production by region

An emerging issue for the industry is excess capacity, partly as a result of Fonterra deciding to increase

capacity in order to give itself “production optionality” at the peak of the season. We estimate that

excess capacity is currently probably at least 10 percent and will rise to at least 15 percent if all the

announced additional capacity comes online. Excess capacity will become more of a problem if total

milk production decreases.

3.7 If so, what changes, if any, are required to ensure that the individual

provisions of the DIRA contestability regime remain fit-for purpose and

are consistent with the Government’s wider policy objectives?

3.7.1 Contestability provisions

As per the Act, the key contestability provisions are:

• open entry / exit and, as part of that, Fonterra being limited to offering one-year supply

contracts except under certain conditions;

• the right for Fonterra suppliers to supply up to 20 percent of their weekly production to an

independent processor;

25• the setting of the base milk price; and

• no discrimination between suppliers.

As per the Regulations and subject to certain constraints, Fonterra must supply raw milk to independent

processors.

All of these provisions (other than arguably the 20 percent rule) appear to have been crucial to the

competitive development of the industry.

The contestability provisions that remain crucial until there is effective competition are:

• open exit and, as part of that, Fonterra being limited to offering one-year supply contracts

except under certain conditions;

• the setting of the base milk price;

• no discrimination between suppliers; and

• raw milk supply.

The 20 percent rule (anecdotally) appears to have been used very sparingly by farmers and because the

benefit attached to the 20 percent rule has been very small, its cost has also been very small for Fonterra.

There is a reasonable argument that the 20 percent rule could be used more in the future, as farmers

seek to cash in on the premiums being offered for A2 and grass-fed milk e.g., by those IPs that have the

ability to segregate milk for processing. On the basis of the potential benefit and the small cost of the

20 percent rule, our recommendation is that it be retained.

3.7.2 Open entry (and re-entry)

We contend that open entry (and open re-entry) should be phased out. To be clear, by open entry and

re-entry we mean milk from new dairy conversions. We do not mean that Fonterra could choose not to

collect milk from an existing supplying dairy farm. Open entry has contributed to the development of

marginal farming land so we would be happy to have that area closed to entry. We do not want to see

a situation whereby any famer doesn’t have his/her milk picked up.

It might reasonably be argued that the open-entry provisions of DIRA have contributed to worse

environmental outcomes, with land being converted to dairy that probably should not have been and

otherwise probably would not have been. For example, land in the Mackenzie Country. The open entry

provisions require Fonterra to accept all the milk that farmers want to supply it, which means that

farmers could have converted cheap (and therefore, by definition, marginal) land into dairy if it was

economical to do so, knowing that Fonterra would have to collect it.

Fonterra would reasonably argue that the open-entry provisions have increased its costs to the extent

that it has extended its milk catchment area and therefore Fonterra’s collection costs.

Fonterra might also argue that the open-entry provisions have frustrated its value-add strategy by

obliging it to invest its limited capital in stainless steel instead. We contend that this argument is

unreasonable for the following reasons:

• while total milk production in New Zealand has increased by 60 percent since Fonterra was

established, Fonterra’s milk collections have only increased by 37 percent. In the absence of

26You can also read