LINK Mobility Group ASA - CEO Den store selskapskvelden 6.juni 2018 Arild E.Hustad - AksjeNorge

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LINK Mobility Group ASA

Den store selskapskvelden 6.juni 2018

Arild E.Hustad

CEO

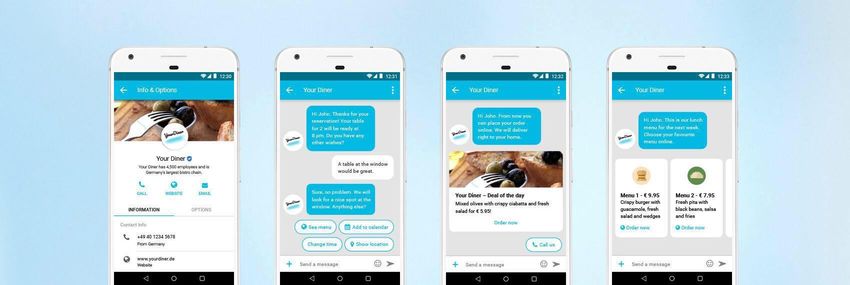

LINK Mobility What does Link do?

Link makes businesses mobile across all

messaging platforms

– the undisputed, How?

Linking businesses to consumers,

sending 6 billion B2C messages in

2017, reaching +200 million unique

mobile users on behalf of more than

market leading mobile

16,500 customers

Where?

Link is in 15 European countries, and

messaging and solution the market leader in in the Nordics,

Germany, Spain and Poland

What next?

provider Execute ambitious M&A and organic

growth strategy, attain scaling synergies

and drive profitability

Copyright 2017 LINK Mobility 2

LINK Mobility key figures

2018 outlook

15

2.7bn revenue

(54% growth)

…

…

18 countries with

leading positions

acquisitions … 1

400m EBITDA

(14.8% margin)

since 2014

1

… 1

1

…

… 1

1

320 >17,000 24% 1

customers average

organic

1

employees 1

across 15 growth L8Q

countries

1) Pro forma guidance for 2018 revenue and EBITDA, including full year effect of acquisitions. Revenue growth relates to growth versus 2017 pro forma figures. The above outlook for 2018 is calculated on LINK’s best estimate based on

information available to LINK, and views and assessment of LINK, as of the date of this report. LINK’s growth assumptions may deviate from the outcome resulting in material or immaterial deviations from the outlook. Further, LINK’s

assumption relating to successfully acquire further businesses during 2018 is to a great extent outside the control of LINK. LINK’s ability to successfully acquire new businesses at fair value, or at all, could materially affect the outlook

figures correspondingly. Investors must therefore make their own calculation in relation to valuing LINK based on their own analysis and judgement

Copyright 2017 LINK Mobility 3

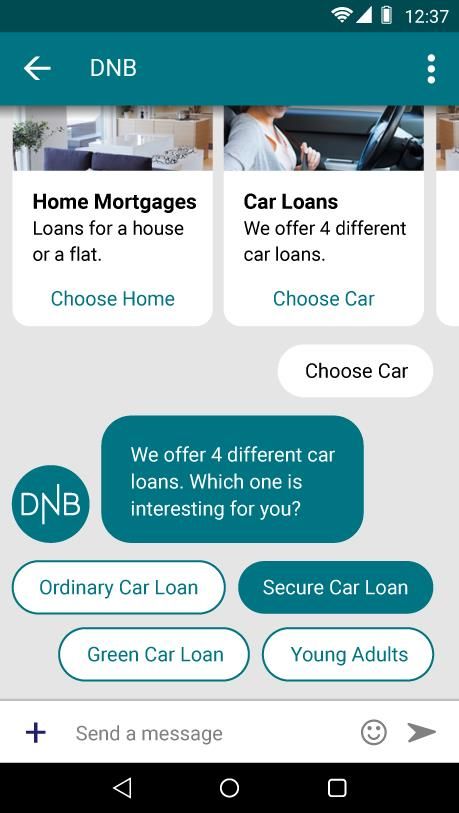

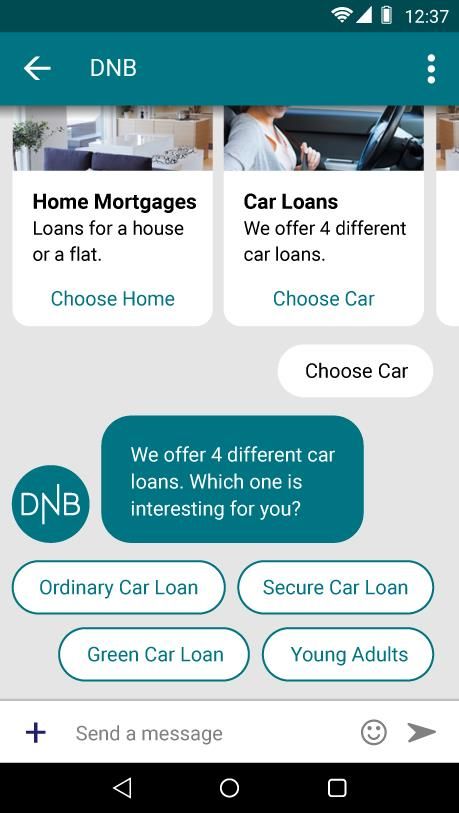

Successfully LINKing enterprises with consumers

Appointments

…but businesses are struggling to navigate

through the increased complex mix of

Polls

devices, platforms, technologies and

…revenue

regulations

growth… Loyalty

programs

…customer Parcel

interaction & notifications

loyalty…

Enterprise use Alerts

mobile solutions

to increase…

…customer Chat

satisfaction…

Payments

…cost Link provides a platform agnostic,

Updates

savings… integrated messaging solution that

seamlessly finds the most efficient

Invoices communication platform to fit the

customer’s requirements

Copyright 2017 LINK Mobility 4

Fully integrated services and solutions offering driving growth

Product description Business model Share of revenues1 COGS

Enriched mobile Monthly messaging Fee to mobile

86%

messaging and omni platform license fee operators and

1 channel solutions Revenue per Double-digit growth rate other channel

message owners

Recurring, scalable

revenue

Mobile Mobile Mobile payment and Monthly license fee 14%

Limited

3 Intelligence Messaging 1

licenses Revenue per mobile

Customer club, mobile solution transaction

2

invoice, notifications,

Recurring and sticky

authentication and

revenue, high margins,

Mobile Joyn

Solutions highly scalable

2 Making mobile Revenue from 2018 Limited

3 messaging more

powerful by data

harvesting and analysis

Copyright 2017 LINK Mobility 5

Strong organic growth combined with M&A

Revenue growth 2013 – 2018E

NOKm 2,700

Reported revenue Estimated

annualized

Proforma effect

M&A effect3

Estimated

1,754 organic growth

Revenue run-

rate end 2017

2007-2012 1 294

622

361

161

136

2013 2014 2015 2016 2017PF 2018 Est

1) Reported revenue growth from 2013 to 2017. Organic growth based on average organic growth across the period

2) 2018 outlook represents year-end revenue run-rate based on the assumptions of organic growth of 25% on the 2017 pro forma revenue run-rate and acquisitions representing NOK ~500m in full year revenues. Note that a term sheet to

acquire SMS.it was disclosed in late January and is not included in the 2017 pro forma revenue run-rate

3) Please note that Link Mobility has signed terms sheets with SMS.it and Allterco regarding the Teracomm assets, i.e. the acquisitions are not closed

Copyright 2017 LINK Mobility 6

Nordic innovation driving European sales

Early adopters Late majority

Travel Financials Retail TMT Travel Financials Retail TMT

+ +

Public Logistics Industry Other Public Logistics Industry Other

Norway historically been an early

adopter of technology

Significant potential from

Status and vertical penetration

maturity of

the mobile

messaging Market development in other

market European countries assessed to be

~4 years behind Norway Market development in the Nordics

assessed to be ~1-2 years behind

Norway

Source: Management estimates

Copyright 2017 LINK Mobility 7

Significant revenue potential from increased market penetration

Number of mobile messages per capita (NOK)1 Market size ’17E Population2 Market potential

Norway 362 NOK ~700m 5.1m NOK ~1.3bn

Spain 48 Volume increase NOK ~500m 46.4m NOK ~3bn

Germany 37 NOK ~1.3bn 82.1m NOK ~11bn

Denmark 213

Sweden 181

Finland 109

Poland 74

Austria

Nordics ahead in B2C messaging penetration

71

compared to Europe. Substantial revenue potential

France 68

from volume growth across existing Link markets

Italy 54

Switzerland 48

Bulgaria 39

1) Company input and Mobilesquared Global A2P messaging traffic 2018

2) Worldometers European Countries by population 2018 (http://www.worldometers.info/population/countries-in-europe-by-population/)

Copyright 2017 LINK Mobility 8

Mobile messaging market expected to continue growing in double digits

Global and Western European messaging volume SMS is still the preferred and superior B2C solution

Billion messages sent per year1

SMS 98 % read rate, compared to email, Facebook and

Worldwide Western Europe

tweets with 20%, 12% and 29%, respectively

2 381

CAGR

22%

90% opened within 3 minutes

2 127

1 923 CAGR

1 697 14% 67

60

Average response time 90 seconds

1 432

53

46

41 Reliable – independent of platform, network, device,

875 35 apps, internet access.

More than 6.1bn frequent users

Safe communication platform

17E 18E 19E 20E 21E 22E 17E 18E 19E 20E 21E 22E

1) Mobilesquared Global A2P messaging forecast by country 2017-2022

9

Copyright 2017 LINK Mobility 9

Geographically diversified, low customer concentration and insignificant churn

Geographically diversified Low customer concentration Insignificant churn

Revenue by geography, Q4 2017 Top 30 customers percent of gross margin, 20171 Norway: Loss of recurring revenue to total revenue (%)2

Norway 29%

Germany 21%

Spain 14% 2,2% 2,3%

Sweden 10%

24% 0,6%

Poland 8%

Denmark 7%

2015 2016 2017

France 5%

Finland 4%

Bulgaria 2%

Baltics 0%

Link gateway solutions are

Low customer concentration implemented in customer’s CRM

Over 17 000 customers across and well-diversified across

15 countries in Europe system, creating high switching

sectors and geography costs

1) Average of the top 30 customers across four quarters for 2017

2) Churn measured for the 100 largest customers in Norway

Copyright 2017 LINK Mobility 10Market dynamics favour market leaders

LINK is the unrivalled European market leader

1 As the market leader, LINK is in a highly attractive

position with several competitive advantages

Market visibility Broader service offering

1

1 R&D competence and technologic Facilitating for multinational clients

leadership

1 Leverage to suppliers

Technology sharing

1

1

1 Significant economies of scale realised by leveraging the position as market leader

with >6bn messages sent¹

1 Attractive position towards new clients with a demonstrated track record of

working with large and reputable regional and international clients

Substantial cost synergies across subsidiaries and geographical markets

1

1

1) Pro forma including full year effect of companies acquired in 2017

Copyright 2017 LINK Mobility 11Innovation driving revenue and differentiation

New and innovative services Next generation messaging Upgrade SMS with rich media

+

RCS1 Early Access Program

1) Early Access Program from Google for RCS business messaging. RCS business messaging uses RCS (Rich Communication Services) to upgrade business SMS with rich media, interactivity, branding and better analytics

Copyright 2017 LINK Mobility 12LINK Conversations to be launched in July 2018

Release 1.0 – Ultimo June 2018 Release 1.x – Q3 2018

• Channels: RCS via Googles RBM API, depending on coverage in Europe, Web Client

• Business Information Page • Carousels of Rich Cards

• Text (bi-directional)

• Suggestions • Media (inbound)

• Suggested actions (e.g. create calendar item, location request, phone call, …)

• Media (outbound: picture, video, audio) • Mobile invoice (Release 2.0 - 2019)

• Rich Cards

Copyright 2017 LINK Mobility 13LINK Mobile Invoice

• Great interest for LINK mobile invoice in

several of our markets; Spain, Bulgaria,

Germany as well as the Nordics

• Strong growth in number of transactions

• 36 contracts signed to date and a strong

salespipe of 120 prospects

• Agreement with BankBridge to enable direct

customer account debiting throughout

Copyright 2017 LINK Mobility 16

EuropeLINK drives European consolidation

Significant experience acquiring assets across W. Europe Established acquisition criteria and structure

Limited competition for targets, due to lack of Strong local market position

companies with scale and well developed Cash positive, i.e. no turnaround cases and cash

platforms flow to LINK from day one

Solid, well-diversified customer portfolios

Churn below 3%

Proven value-creating

acquisition strategy

~80% overlapping technology

Strong telecom operator relationships

All companies acquired have

been purchased at attractive

multiples (average of ~6.2x

EV/EBITDA) Typical financing structure

Attractive synergy potential

utilized, driving strong margin

expansion

Historically financing has consisted of

1/3 cash, 1/3 seller’s credit and 1/3

LINK

Cash shares in LINK Mobility Group ASA1

shares

Proven successful

integration Seller’s Shares and cash settled at closing

Credit while sellers credit has historically

had a tenor of 3 years

1) The financing structure for future acquisitions will be tailored and optimized to each specific situation

Copyright 2017 LINK Mobility 17Significant benefits gained from consolidation and scaling

COGS savings

One LINK Messaging • Consolidate local

Annual recurring

Platform platforms and solutions synergies of NOK

• 50-70m from end of

+ •

Terminate local products

and services

Joint support, operations

2019

and routing

Delivered NOK 17m

One LINK Services in 2017

Application Platform

Plan to deliver NOK

30-40m in 2018

Capex savings

• Common products and

services EBITDA margin

One LINIK Common • Cost efficient Bulgarian

contribution of 2-3

Routing Team development hub p.p

Copyright 2017 LINK Mobility 18Strong revenue and profitability performance

Revenue evolution Organic growth evolution EBITDA evolution 1

Reported revenue (NOKm) Y-o-y growth Organic growth y-o-y Adjusted EBITDA (NOKm) EBITDA margin

53% 58% 43% 115% 107% 126% 129% 89% 9.1% 13.7% 8.0% 11.7% 7.3% 10.8% 10.8% 12.5%

486 61

30% 29%

25% 25%

23%

22%

20%

298 19%

281

256 32

229 30 30

125 130 17 17

111

10 10

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17 Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17

1) Adjusted for costs related to acquisitions, one-off costs and share based compensation

Copyright 2017 LINK Mobility 19Continued strong growth in revenues in Q1

Operating revenues

(NOKm)

– Revenues of NOK 467 (23% organic growth & 104% total 104%

486

growth) 467

281 298

– An adjusted EBITDA of NOK 51m (10,9%) up from NOK 17 229

25% 23% 22% 25% 23%

– 1,6 billion transactions and interaction with more than

205 million unique mobile phones Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018

= Organical growth QonQ

– 17 000 customer and signed 658 new contracts of which Adjusted EBITDA

(NOKm)

61

384 new customers 51

– High acquisition activity 30 32

17

– Continued strong performance in all our markets 7,3% 10,8% 10,8% 12,5% 10,9%

Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018

= Adjusted EBITDA margin

subsidiaries as reported in first quarter in 2017. Acquired business inlude the acquisition of Didimo-Jet Group, GMS, Voicecom,

Copyright 2017 LINK Mobility 20Considerable scale advantages visible in Q1 2018

Adjusted EBITDA% development

QonQ Substantial scale advantages in business model

0,2 %

1,4 %

§ +4.3 percentage points increased margin from scale advantages

offsetting gross margin reduction of -2.0 percentage points in

4,3 %

10,9 % existing markets

§ High organic growth is expected to drive scale advantages going

-2,0 %

7,3 %

-0,3 %

forward

Q1 17 GM1 pr market GM1 mix Delta OPEX Delta OPEX Margin effect Q1 18

Existing markets Group Aquired § Future acquisitions will further strengthen scale advantages

functions entities

Existing markets are defined as the subsidiaries as reported in first quarter in 2017. Acquired business inlude the acquisition of Didimo

Adjusted EBITDA 61

(NOKm)

51 Scale advantages counteract gross margin reduction

32

§ High growth from large enterprises customers drives scalability

30

further, positive gross profit and no additional OPEX

17

§ Dilutes gross margin in existing markets as large enterprise

7,3% 10,8% 10,8% 12,5% 10,9% customers have lower margins than SME customers

Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018

§ Acquired entities have lower gross margin than existing markets

= Adjusted EBITDA margin

n 2017. Acquired business inlude the acquisition of Didimo-Jet Group, GMS, Voicecom,

Copyright 2017 LINK Mobility 21Asset light business model

Low working capital requirements Low investment requirements High cash conversion

Net working capital and share of revenue1 (NOKm) Quarterly capital investments and share of revenue2 (NOKm) Cash conversion: Average last three years3

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17 19,9

-2%

- -4% -

-7% -6% -6%

-7%

- 14,5

-17,9 -11% -

- -14%

-27,9 -

-32,9 10,7

-

- 8,6 9,1 8,7

- -42,6 87%

6,9

-

- -53,9

3,9 1,9%

-62,6 -

- -65,7 1,4% 1,5% 1,6% 1,5%

1,2%

1,0% 1,0%

- -

-79,3

- -

Q1'16 Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17

Net working capital Share of revenue CAPEX Share of revenue

1) Net working capital: (trade receivables – trade payables – tax payables)

2) CAPEX: Investments excl. acquisitions

3) Cash conversion: Net cash flow from operations to adjusted EBITDA (average FY’15-FY’17)

Copyright 2017 LINK Mobility 22Delivering on the 2018 outlook

LTM Revenue evolution 2018 Outlook (NOK)2

LTM per. quarter, NOKm 3

2 700

1 065

1 294

1 754

€ 2,700m

740 897 25%

+500m in Pro forma revenue

445 485 622 organic

acquisitions

236 289 361 400 growth

198

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q4

2017 2018

2015 2016 2017 Pro

forma

Organic

growth

M&A outlook 400m

Pro forma EBITDA

LTM Adjusted EBITDA1 evolution

LTM per. quarter, NOKm

400

25%

Organic growth

209

140

87 109 25% organic growth

49 51 54 52 67 74 Acquisitions

33 40 48

3%-p margin

improvement

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q4

2017 2018 8bn

2015 2016 2017 Pro outlook Mobile messages

forma

1) Adjusted for costs related to acquisitions, one-off cost and share based compensations

2) Pro forma revenue and EBITDA outlook figures. Includes full year effect of acquisitions. The above outlook for 2018 is calculated on LINK’s best estimate based on information available to LINK, and views and assessment of LINK, as of the date of this report.

LINK’s growth assumptions may deviate from the outcome resulting in material or immaterial deviations from the outlook. Further, LINK’s assumption relating to successfully acquire further businesses during 2018 is to a great extent outside the control of LINK.

LINK’s ability to successfully acquire new businesses at fair value, or at all, could materially affect the outlook figures correspondingly. Investors must therefore make their own calculation in relation to valuing LINK based on their own analysis and judgement

3) Please note that Link Mobility has signed terms sheets with SMS.it and Allterco regarding the Teracomm assets, i.e. the acquisitions are not closed

Copyright 2017 LINK Mobility 23Key investment highlights

The #1 European mobile messaging and mobile solutions company – well protected by high

1 barriers to entry

Annual organic growth of 20+%, backed by strong underlying market growth through increased

2 European mobile messaging penetration

The European consolidator with a proven roll-up acquisition model in a fragmented market with

3 attractive benefits of scale

Highly scalable and asset light business model with ~90%+ recurring revenues and ~90% cash

4 conversion

5 Experienced management team ready to take LINK Mobility to the next level

Copyright 2017 LINK Mobility 24Thank you www.Linkmobility.com

You can also read