STATE OF THE MARKET - Renewable Energy Buyers Alliance

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

STATE OF THE MARKET

Thank you to the Supporters of REBA and the Sponsors

of REBA Connect: Virtual Member Summit

Thank you to all our REBA members!

REBA Leadership Circle Platinum Members

AT&T Microsoft

QTS Target VMware

Gold Members

Adobe Micron Technology

Anheuser-Busch InBev Nestle

Atlassian Nike

Autodesk PayPal

Bloomberg PepsiCo

Cargill Starbucks Corp

Cisco VF Corporation

Cummins Inc. 174 Power Global

eBay Bank of America Merrill Lynch

Equinix Covington & Burling LLP

Freeport-McMoRan CustomerFirst Renewables

IBM Morgan Stanley Capital Group

Iron Mountain Orsted

McDonald's USA, LLC Wilson Sonsini

Acknowledgements

Authors Third Party Data Sources

Bryn Baker CDP

Miranda Ballentine Electric Reliability Council of Texas

Priya Barua Energy Information Administration

Katherine Kerr National Renewable Energy

Camorah King Laboratory

Alex Klonick RE100

Mark Porter Science Based Targets

Laura Vendetta S&P Global

4

Agenda

The Buyers Journey

US Market Overview and Key Trends

Unlocking Future Procurement Options

Leadership Trends

5

Agenda

The Buyers Journey

US Market Overview and Key Trends

Unlocking Future Procurement Options

Leadership Trends

6

The Buyers Journey

From planning to action

ACTION

• Pursuing goals with

COMMITMENT RECs, PPAs, project

• Setting carbon ownership and more

TRANSPARENCY reduction targets • Restarting the process

• Accounting for your • Pledging to clean for supply chain, 24/7

carbon footprint energy goals renewables, etc.

• Mapping your energy

consumption

FEEDBACK LOOP

7

The Buyers Journey

From planning to action

ACTION

COMMITMENT

TRANSPARENCY

• Accounting for your

carbon footprint

• Mapping your energy

consumption

FEEDBACK LOOP

8

The Buyers Journey – Transparency

Reporting is a key first step to managing a path forward

9,000

Companies disclosing to CDP

to CDP

to CDP 8,000

7,000

Disclosing

6,000

Companies Disclosing

5,000

Companies

4,000

3,000

Total

2,000

Total

1,000

0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: https://www.cdp.net/en/companies/companies-scores

9

The Buyers Journey

From planning to action

ACTION

COMMITMENT

• Setting carbon

TRANSPARENCY reduction targets

• Pledging to clean

energy goals

FEEDBACK LOOP

10The Buyers Journey – Commitments

Increases in goal setting with both an emissions and energy focus

Science Based Targets Companies RE100 Companies

400 70

800

60

RE100 Companies

200

SBT Companies

RE100Companies

Companies

300

Total RE100 Companies

50

Companies

Companies

Companies

600

150

40

200

SBTSBT

400

RE100

SBT

30 100

TotalTotal

New

New New

New

20

Total

100 200 50

10

0 0 0 0

2015 2016 2017 2018 2019 2020 YTD 2014 2015 2016 2017 2018 2019 2020 YTD

Source: https://sciencebasedtargets.org/companies-taking-action/# Source: http://there100.org/companies

11The Buyers Journey

From planning to action

ACTION

• Pursuing goals with

COMMITMENT RECs, PPAs, project

ownership and more

TRANSPARENCY • Restarting the process

for supply chain, 24/7

renewables, etc.

FEEDBACK LOOP

12The Buyers Journey – Action

Consistent growth in voluntary market sales

NREL Voluntary Green Power Sales

Total Green Power Sales (MWh)

Source: https://www.nrel.gov/docs/fy20osti/74862.pdf

13Agenda

The Buyers Journey

US Market Overview and Key Trends

Unlocking Future Procurement Options

Leadership Trends

14Announced Corporate Renewable Deals in the U.S.

10.0 9.33

8.0

6.39

GW of Capacity

6.0

4.0

3.22

2.76

2.0 1.54 1.76

1.20

0.0

2014 2015 2016 2017 2018 2019 2020

Over 26GW announced in the last 10 years

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

15Announced Corporate Renewable Deals in the U.S. by Quarter

GW of Capacity

Over 15GW announced in the last 2 calendar years

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

16Announced Corporate Renewable Deals in the U.S. by Quarter

GW of Capacity

Q1 2020 is down for a few reasons

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

172019 Announced Corporate Renewable Deals in the U.S. by Week

GW of Capacity

~3 GWs announced within 8 days in September

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

18Announced Corporate Renewable Deals in the U.S. by Quarter

GW of Capacity

Q2 2020 to date has already surpassed Q2 2018

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

19Market Expansion: New Buyers

Cumulative Unique Buyers

New Buyers

Over 100 companies have transacted in utility-scale renewable energy market since 2008

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

20Market Expansion: New Energy Providers

Cumulative Unique Energy Providers

New Energy Providers

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

21Increase In Unknown Deal Counterparties

10.0 9.33

8.0

6.39

GW of Capacity

6.0

4.0

3.22

2.76

2.17

2.0 1.54

1.20

0.0

2014 2015 2016 2017 2018 2019

In 2019, 2+ GWs from ~12 announced deals did not make energy provider public

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

22Technology Evolution

* This does not include ~800 MWs of deals in which the technology is not known

GW of Capacity

Solar

Wind

At least 2.5 GW of ~5 GW of solar announced in 2019 was in ERCOT

A s of A pril 24, 2020. Publicly announced contracted capacity of corporate P ower P urchase Agreements, Green P ower P urchases, G reen Tariffs, and Outright P roject Ownership in the US, 2015-2020 by quarter. Excludes on-site generation (e.g., rooftop

solar P V ) and deals with operating plants. (#) indicates number of deals each year by individual companies. Copyright 2020 Re newable E nergy Buyers Alliance. P roduced in part using data from S &P G lobal Market Intelligence, Copyright © 2020.

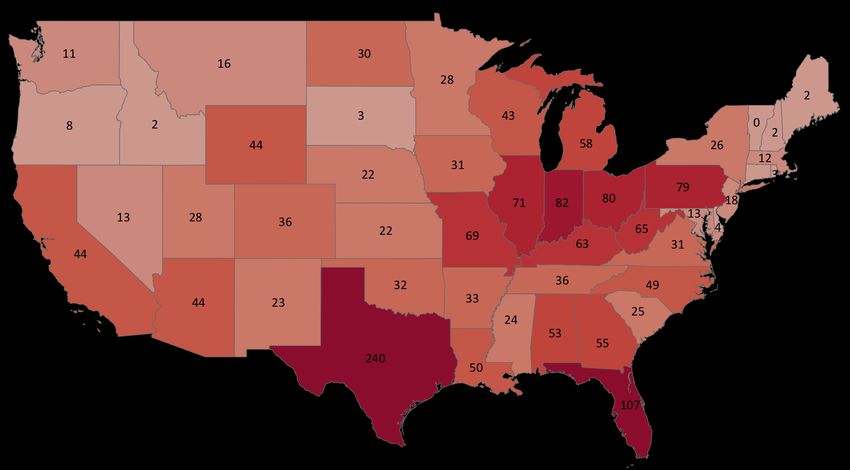

23Where are Corporates Signing Deals? – Until 2020YTD

Count of deals

1 25+

24CO2 Emission Factors From Electric Power

Emissions factor (metric tons/MWh)

0.01 0.95

Source: 2017 Total Electric Industry Power Data – EIA.com

25CO2 Emissions From Electric Power

Source: 2017 Total Electric Industry Power Data – EIA.com

26Battery Capacity in the ERCOT Interconnection Queue

Now Exceeds Gas Capacity

100%

2,847 3,012 Numbers on

3,265 3,501

4,121 3,957 3,971

4,200

bars represent

4,453 MWs of each

5,628

75% 7,215

tech category

7,790 8,965 9,978 10,380

Battery

50% Gas

10,825 10,529 10,537 10,103 9,740

9,737 9,283

8,207

7,405

7,445

25% 5,898 5,607 5,607 5,507 5,749

0%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Source: http://mis.ercot.com/misapp/GetReports.do?reportTypeId=15933&reportTitle=GIS%20Report&showHTMLView=&mimicKey

27Agenda

The Buyers Journey

US Market Overview and Key Trends

Unlocking Future Procurement Options

Leadership Trends

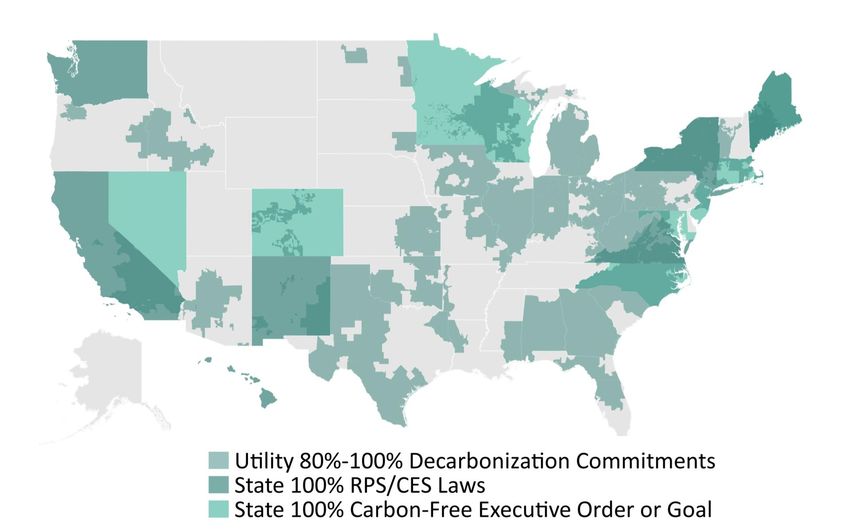

28Pathway 1: Greening the Grid for All

States Driving Decarbonization

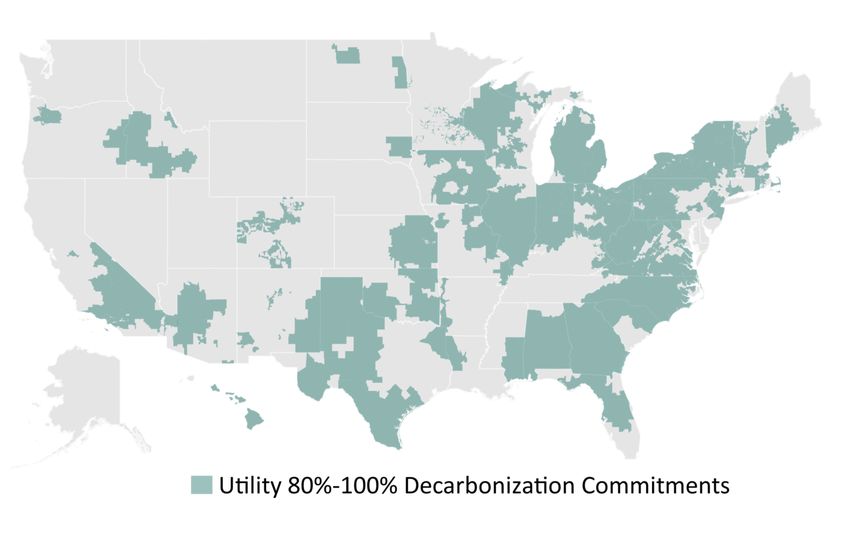

29Pathway 1: Greening the Grid for All

Utilities Setting Decarbonization Commitments

30Pathway 1: Where is the Grid Greening for All?

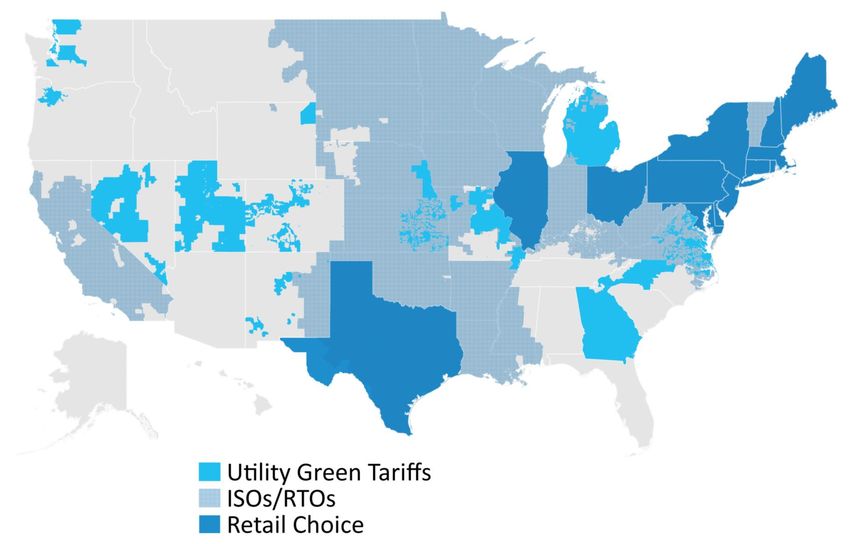

31Pathway 2: Increase and Improve Customer Options

RTO Expansion

Source: isorto.org

32Pathway 2: Increase and Improve Customer Options

States with Green Tariffs Approved and Used

17 states have green tariffs available, 14 have active C&I customers

Data from REBA Green Tariff tracking and only includes deals that involve build of new generation and corporate commitments

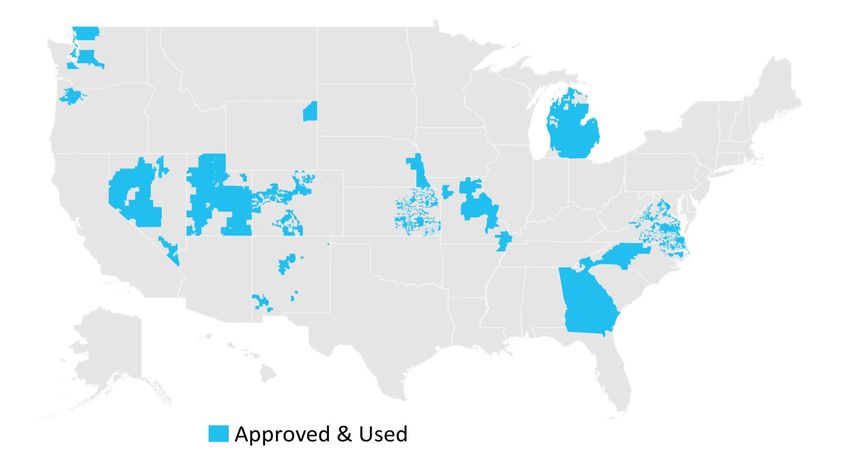

33Pathway 2: Increase and Improve Customer Options

Utility Territories with Approved Green Tariffs Used by Corporates

Narrowing deployed green tariffs to utility service territories further highlights their limited availability

Data from REBA Green Tariff tracking and only includes deals that involve build of new generation and corporate commitments

34Pathway 2: Increase and Improve Customer Options

Where do customers have options?

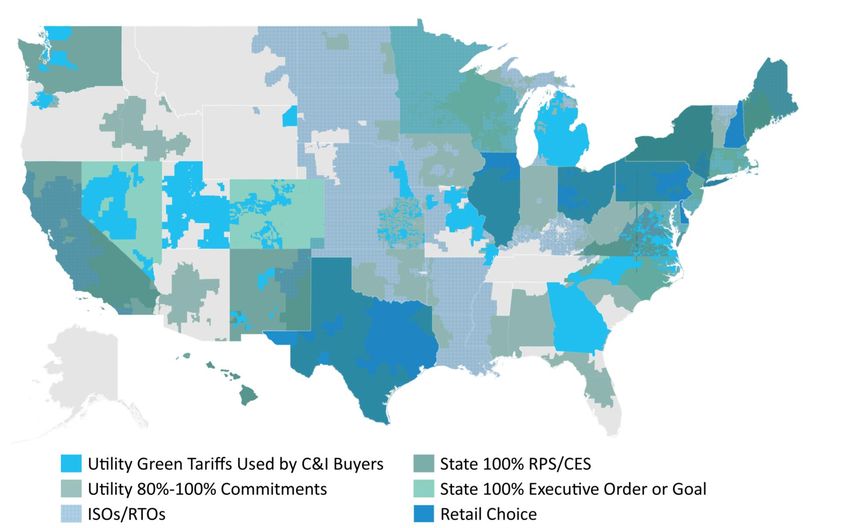

35Bringing It All Together...

36Bringing It All Together...

42%

8% 29%

28% 2%

22% 33%

% of Electricity

52% 10% Consumption that is

Renewable

4%

17%

Based on EIA 2017 data

4%

37Agenda

The Buyers Journey

US Market Overview and Key Trends

Unlocking Future Procurement Options

Leadership Trends

38Trends Where Large Energy Consumers Want to Lead

1 2

Transitioning from 100% RE goals New/Additional Material Impact

to Projects Projects

24-7/365 zero carbon

source: Google source: WattTime

3 4 5 6

Policy & Regulatory More International Focus on Supply Impact Beyond

Engagement Procurement Chain Partners Carbon

39Thank you!

40You can also read