Supercharged Climate Positive - Investing in Europe November 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Supercharged

Climate Positive ®

Investing in Europe

November 2020

Emmanuel DeSousa, Eric Kosmowski,

Joaquin Rodriguez Torres, Melanie Nakagawa

Contributing Authors

Jake Hansen, Scott Himmelberger, Martin Steinweg inquiries@princeville-capital.com

Supercharged Climate Positive® Princeville Capital

I. Executive Summary

—

As global technology investors we are constantly evaluating Based on our engagements with over 400 companies

trends in capital markets and governmental policies that headquartered in Europe and around the world coupled

shape technology development, adoption and growth with our analysis of Europe’s market and policy conditions,

around the world. We have been particularly focused on we believe the following technologies and tech-enabled

the extraordinary rise in climate technology companies business models are well positioned for accelerated

– whose funding has grown five times faster than overall growth:

venture capital, attracting approximately $16 billion in

2019.1 Several factors contribute to this growth - including 1. Residential clean energy solutions

macroeconomic changes, expedited policy adoption, 2. Virtual power plants and distributed energy resources

increasing demand, and access to focused capital. We 3. Digital utilities

have taken a closer look at where these factors are likely 4. Electric vehicle charging network operators

to have a prominent impact and believe that investment 5. Mobility data platforms

opportunities in technology companies addressing climate 6. Mobility-as-a-service providers

change are supercharged for delivering outsized returns 7. Intelligent building energy management

in this decade – 2020 through 2030 – and particularly in 8. Energy efficiency-as-a-service providers

Europe.

We selected these technologies and models based on

We conclude what makes this decade distinct from their high growth, capital efficiency, ability to deliver

previous years are four macrotrends: positive unit economics, and the policy pull driving

accelerated decarbonization. We also highlight green

• Advancement in enabling technologies for climate hydrogen, microgrids, electric vehicle manufacturing

solutions and improving economics for climate tech and batteries and certain ridesharing platforms that do

• Healthy early-stage climate tech start-up and venture not meet all these exacting criteria, but are exciting high-

ecosystem growth technologies and tech-enabled business models

• Europe’s Green Deal and stimulus accelerates policy that should remain a focus for investors because of the

and technology adoption macrotrends surrounding their adoption.

• Increasing consumer preferences for climate solutions

and climate leadership from corporations and financial Thanks to strong tailwinds blowing in Europe, including

institutions unprecedented government stimulus targeting climate

change, we offer our insights into why Europe’s climate-

These macrotrends are accelerating the growth in many related technology companies are primed for accelerated

leading companies at the forefront of the climate transition. growth and have become a market not to be missed by

We identified eight leading technologies and tech-enabled technology investors.

business models poised for outsized growth and returns in

sectors that green the grid, decarbonize transportation and

create a more energy efficient built environment – sectors

that are responsible for nearly 60% of Europe’s carbon

pollution.

1

PwC research. “The State of Climate Tech 2020.” Sept 2020, https://www.pwc.com/gx/en/services/sustainability/assets/pwc-the-state-

of-climate-tech-2020.pdf.

Page 1Princeville Capital Supercharged Climate Positive®

II. E ur ope’s Oppor t uni s t ic E nv ir onmen t:

Four Key Macrotrends

—

There is growing momentum in Europe for scaling Macrotrend 3:

technology companies addressing climate change.

Europe’s Green Deal and stimulus accelerating policy and

Europe has always been in a leading position on climate

technology adoption

action – whether being the first region to implement a

cap on carbon pollution in 2005 or centering its economic

growth and recovery strategy around getting to climate

Macrotrend 4:

neutrality. Europe is also home to numerous corporations, Increasing consumer preferences for climate solutions

investors, and policymakers that have been at the forefront and climate leadership from corporations and financial

of advancing climate commitments and new mechanisms institutions

to achieve them. Despite these factors, Europe trails

the United States and China in attracting venture capital These trends are making the European investment

in climate-related technologies – attracting $7 billion environment for climate technology poised for outsized

compared to the United States’ $29 billion and China’s performance. Indeed, publicly traded shares in climate

$20 billion.2 We believe investors who are shying away technology companies have outperformed nearly all other

from Europe are missing attractive opportunities to deploy categories of European public companies this year.3 Since

capital in the region as climate technology, especially in the beginning of the year, the performance of the NASDAQ

Europe, is benefitting from four key macrotrends: Clean Edge Green Energy Index, an index that tracks

publicly traded clean-energy and low-carbon technology

Macrotrend 1: companies, has been better than that of the S&P 500 or

STOXX Europe 600. Even when looking specifically at

Advancement in enabling technologies for climate

the returns of technology companies, one of the best

solutions and improving economics for climate tech

performing sectors through the COVID crisis, these climate

technology stocks have performed significantly better.

Macrotrend 2:

Healthy early-stage climate tech start-up and venture

ecosystem

Index

Index Market

Market Cap

Cap

220%

200%

180%

160%

140%

120%

100%

80%

60%

1-Jan-20 1-Feb-20 1-Mar-20 1-Apr-20 1-May-20 1-Jun-20 1-Jul-20 1-Aug-20 1-Sep-20 1-Oct-20

NASDAQ Clean Edge Index S&P 500 Tech STOXX Europe 600 Tech

S&P 500 STOXX Europe 600

2

Id.

3

S&P Capital IQ. Retrieved October 10, 2020, from S&P Capital IQ database.

Page 2Supercharged Climate Positive® Princeville Capital

M ac r o t r e nd 1 Numer of IoT Connections in the UK

70.0

Advancement in enabling technologies

for climate solutions and improving 60.0

economics for these technologies 50.0

The last decade is marked by significant advancements

40.0

in digitally-enabled technologies that underpin many of

the most promising climate solutions. This technology

30.0

maturity coupled with new economic conditions have

helped drive the significant gains in renewable energy

20.0

deployment and consumption in Europe.

10.0

Technology Maturity

The widespread proliferation of low-cost sensors 0.0

connected to the internet known as the internet of things 2016 2017 2018 2019 2020

(IoT) has benefitted many applications related to climate

technologies. The number of IoT devices has exploded, Automotive Consumer Electronics

more than quadrupling in just the last four years with Utilities Other

signs of continued acceleration.4 Many of these devices

are being deployed in sectors highly relevant to climate

technology including utility, automotive, and smart city

applications. With the now near ubiquitous data collection Improved Economics for Renewable Energy

from a huge number of distributed assets, climate-related Europe is a prime candidate for renewable adoption. Many

technology companies are finding ways to optimize their analysts expect renewables to grow significantly in Europe

operations and reduce emissions. in the future due to cost declines in solar, wind, and batteries.

Bloomberg New Energy Finance estimates that “by 2040,

The rapid and massive improvement in artificial renewables make up 90% of the electricity mix in Europe,

intelligence (AI) is another key enabler of advancements with wind and solar accounting for 80%.” This growth is

in climate technology. Complex systems that are difficult supported by reductions in capital costs, particularly steep

to model in their entirety, (mobility systems, the electric declines in costs for solar photovoltaics (PV) and battery

grid, climate models, etc.) are ideal candidates for the technologies, that is lowering the levelized costs of energy

application of AI-based algorithms. In recent years, AI has (LCOEs) for renewables. These decreasing LCOEs, along

made major strides as computing power has continued to with Europe’s high, and rising, electricity prices (compared

increase and the algorithms used to train the models have to other countries like the US), accelerates adoption of

become more sophisticated. The amount of compute used renewables and have contributed to new milestones in the

for training AI models, a figure correlated with the power deployment of renewables. For the first time, renewables

and accuracy of AI-based models, has been doubling every generated 40% of the 27 EU member states’ electricity

3.5 months for most of the last decade.5 This exponential in the first half of 2020, overtaking generation from coal,

growth means modern AI tools leverage more than 1 million oil and gas.6 (chart on next page7). For many countries,

times the computing power of models just 8 years ago. renewables are now the cheapest energy source.

These improvements have unlocked more applications

that AI-based models can address with respect to climate

change.

4

Data and source for graphic: Cambridge Consultants. (2017). Gordon Davies, “The What and When of IoT Adoption.” Cisco UK & Ireland

Blog, 19 May 2017, https://gblogs.cisco.com/uki/the-what-and-when-of-iot-adoption/.

5

Open AI. “AI Doubling Its Compute Every 3.5 Months.” Medium, 17 May 2018, https://medium.com/@Synced/ai-doubling-its-compute-

every-3-5-months-596b1b60fab.

6

Farand, Chloe. “Renewables overtake fossil fuels in EU electricity generation.” Climate Change News, 22 July 2020, https://www.

climatechangenews.com/2020/07/22/renewables-overtake-fossil-fuels-eu-electricity-generation/.

7

Chart source: Ember. https://ember-climate.org/data/global-electricity/.

Page 3Princeville Capital Supercharged Climate Positive®

Renewables Beat Fossil

Renewables Beat Fossil Energy M ac r o t r e nd 2

Generation in Europe

60

Healthy early-stage climate tech

start-up and venture ecosystem

% of total EU-27 electricity generation

50

As expected, the pandemic has delivered some contraction

40

in overall deal volume in Europe, with European venture

30 funding for the first half of 2020 declining 20% from 2019–

when it was at an all-time high. At the same time, there are

20 important trends to look for that indicate a healthy and

expanding early-stage European climate-tech start-up and

10

VC ecosystem in this reset environment that are creating

0 opportunities for investors.

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Expanding Pipeline of Companies

Fossil Fuels Renewables We are seeing healthy growth in the early-stage climate

technology company pipeline. Capital raised by so-called

Coal Wind and Solar “purpose-driven” companies doubled from $1.9 billion

Source: Ember in 2018 to $4.4 billion in 2019.9 More importantly, an

overwhelming majority of these purpose-driven companies

- 410 out of 500 companies10 - identified in the “State of

European Central Banks (ECB) have also set interest rates European Tech” report include climate action as part of the

so low that the cost of borrowing for low-risk renewables company’s core mission. And not only is climate change

projects remains at historically low levels. For renewables, the leading issue tackled by these companies, these

because a greater portion of the total cost results from companies have also attracted the highest level of capital

the upfront capex investment relative to fossil-fuel power investment,11 filling up the European climate tech pipeline

plants, the economics of these projects is particularly with companies reaching growth-stage.

sensitive to the interest rate. According to researchers

from ETH Zurich, a full 25% of the reduction in the cost of Growing Investor Diversification

wind power over the last 15 years has been because of the

There is an evolution happening in the European ecosystem

lower interest rates.8 There is little near-term expectation

that is beginning to favor financially-motivated and

of interest rates being raised again, thus paving a runway of

globally-oriented investors to help companies scale. Two

continued low-cost financing for renewable projects.

factors are coming together.

First, strategic (e.g. corporate venture capital) investors

ECBInterest

ECB Intrest Rate

Rate

have played an important role in many European deals –

7 nearly 25% of climate tech deals done included a strategic

investor.12 However, we anticipate that some of these

6

European investors are likely going to pause in their capital

5 deployment while their main businesses recover from the

4 economic downturn. This will be particularly pronounced

3 for some corporate VCs, such as those from oil and gas or

fossil fuel asset-heavy utilities, as they have undergone

2

fairly substantial cost-cutting over the last few months.

1 This pause is likely to create an opportunity for other

0 investors, especially those with strong corporate networks,

to provide a differentiated value add to these companies.

1/1/1999

1/1/2001

1/1/2003

1/1/2005

1/1/2007

1/1/2009

1/1/2011

1/1/2013

1/1/2015

1/1/2017

1/1/2019

8

Adverse effects of rising interest rates on sustainable energy transitions, Nature Sustainability

9

“The State of European Tech 2019.” atomico in partnership with Slush and Orrick, https://2019.stateofeuropeantech.com/chapter/purpose/

article/purpose-driven-investment/.

10

Based on a set of 528 unique companies identified by Dealroom. The sum of all companies per SDG is greater than that number as some

companies may be addressing more than one goal. Source: Id.

11

Id.

12

See PwC supra note 1.

Page 4Supercharged Climate Positive® Princeville Capital

Second, the European venture ecosystem is beginning slowdown in overall venture funding (for all sectors, not

to attract a more geographically diverse pool of just climate tech), investors in late stage and technology

investors. Historically, while European tech companies growth (Series C and later) remain close to Q4 2019 levels.15

have developed strong technology, relatively few have

M ac r o t r e nd 3

successfully scaled across Europe and none so far

has succeeded in becoming an international giant of

the likes of Google, Facebook, Microsoft, Apple, and

Amazon. This may be in part due to Europe’s inherently Europe’s Green Deal and stimulus

fragmented nature, but other elements include a weaker

accelerates technology adoption

growth equity environment and a historical lack of

global expansion ambition among European startups.13 Notwithstanding an abrupt economic upheaval caused by

However, there are now a growing number of European a global pandemic that could have derailed Europe from its

start-ups looking to expand globally and seeking investors ambitious climate goals, Europe remains steadfast in its

with a broader geographic footprint and larger pools of commitment to lead on climate action. Europe’s Green Deal

growth capital. Last year, for rounds $20M and above, is the policy fulcrum and growth engine for the European

33% of investors were from North America while 60% were economy. The North Star to this package is Europe’s goal

from Europe.14 We see even more opportunity for globally- to be the first climate neutral continent by 2050. To achieve

minded investors to help European companies scale their this, Europe plans to raise its 2030 emissions-reduction

ambitions. target from 40% to 55% (below 1990 levels). This level of

ambition will mean nearly every sector of the European

Europe, with its strong policy and consumer support for economy will have to ensure they are moving quickly to

climate-related technologies, remains an ideal environment decarbonize – a pull for climate innovation at a scale never

to scale climate related businesses. Given many of the seen before.

same climate-related challenges are common around the

world, there should also be ample opportunity for European

climate technology companies to become major global However, there are now a growing number

forces. Out of the roughly 25 climate-related technology of European start-ups looking to expand

focused funds we know in Europe, there are only a few globally and seeking investors with a

specifically targeting growth stage investments, with the

vast majority focused on early-stage tech companies.

broader geographic footprint and larger

We believe that the European climate tech ecosystem pools of growth capital.

is primed for growth equity investors, with a truly global

mindset, to invest in promising technology companies and

drive their expansion around the world. To date, despite a

Q2'20

European Venture Dollar Volume Through Q2’20

Total Invested Capital Per Quarter ($b)

12.0

10.0

8.0 6.6 6.4

4.4 4.7

6.0 4.4

4.0

3.6 4.0 3.6 3.4

2.0 3.1

0.0 0.9 0.9 1.0 0.8 0.7

Q2'19 Q3'19 Q4'19 Q1'20 Q2'20

Angel-Seed Early Stage Late Stage + Technology Growth

Source: Crunchbase

13

Ghosh, Shona. “7 investors and founders reveal 6 reasons Europe has never produced its own Facebook, Google, or Amazon.”

Business Insider, 30 May 2019, https://www.businessinsider.com/why-europe-has-never-produced-a-google-2019-5.

14

Teare, Gené. “European Venture Report Q2 2020: Funding Down to 2018 Levels After Record High in 2019.” Crunchbase, July 20, 2020,

https://news.crunchbase.com/news/european-venture-report-q2-2020-funding-down-to-2018-levels-after-record-high-in-2019/.

15

Gené Teare and Sophia Kunthara. “European Venture Report: VC Dollars Rise in 2019. ” Crunchbase, January 14, 2020, https://news.

crunchbase.com/news/european-venture-report-vc-dollars-rise-in-2019/.

Page 5Princeville Capital Supercharged Climate Positive®

And despite the potential for a global pandemic to knock Europe off course, European governments used this moment to

make climate change the centerpiece of its post-pandemic development plans for decades in the future. Consistent with

this vision, the European Union introduced the world’s largest “green” stimulus and committed to direct 30% of the total

recovery package toward climate protection from 2021-2027. This makes the EU’s green stimulus 10 times larger than any

other country (see chart below).

Europe Outpaces Rest of World with Green Recovery Efforts

Green Stimulus Spending ($b) Green Share of Total Stimulus

300 25.0%

249

20.2%

250

20.0%

200

15.0%

150

10.0%

100

5.0%

50

26 1.9% 2.4%

1.1%

1.4 0.8

0 0.0%

US EU China India US EU China India

Source: Rhodium Group16

While specific details and allocations remain under discussion, current estimates indicate that total green stimulus

spending from the Next Generation EU package will likely represent 20% of total EU and member state stimulus spending.

This unprecedented influx of new investment into climate policies and projects to decarbonize the power sector (e.g.

renewables/hydrogen), and programs to increase energy efficiency is likely to be an important accelerant for climate

technology solutions in Europe. Related sectors such as low-carbon transport, energy storage and batteries, infrastructure

and green buildings will also benefit from Europe’s stimulus.

The EU package, for example, includes a two-year €20 billion boost for “clean” vehicles, a target of 2 million electric &

hydrogen vehicle charging stations installed by 2025 and €10B in European Investment Bank project loans for renewable

energy and hydrogen. From this we anticipate rapid growth in demand for the companies in our pipeline that provide

advanced mobility software solutions and technology solutions to support and integrate additional distributed energy

resources into a smart grid. Relatedly, energy efficiency solutions are also well-positioned to benefit from Europe’s

“Renovation Wave Strategy” – a plan to stimulate faster building renovation and efficiency deployments in Europe.

We are optimistic regarding how these stimulus measures can serve as an accelerant to many Climate Positive® sectors.

We also recognize that political leadership and policy measures are important achievements that do not happen in a

vacuum. They require the support and investment by other stakeholders (e.g. consumers, corporations, banks) to

overcome challenges such as those created by inertia (e.g. incumbents slow to adopt new technologies) or complex and

highly fragmented sectors (e.g. energy systems).

16

Source: Kate Larsen, Pramit Pal Chaudhuri, Jacob Funk Kirkegaard, John Larsen, Logan Wright, Alfredo Rivera, and Hannah Pitt.

“It’s Not Easy Being Green: Stimulus Spending in the World’s Major Economies”, sourcing from IMF Fiscal Tracker, official government

announcements, Rhodium Group.

Page 6Supercharged Climate Positive® Princeville Capital

M ac r o t r e nd 4

Changing consumer preferences and climate leadership from corporations and

financial institutions

Rounding out the key macrotrends In In what

what areas

areas dodoyouyou see

see thethe biggest

biggest need

need forfor

driving adoption of climate change

change in in

Europe’s economies?

Europe's economies?

technology in Europe are changing

consumer preferences on Environmental sustainability 54

environmental sustainability and the Fairness of pay and wealth 51

growth in climate-specific leadership Training and qualification for future jobs 39

from European corporations and Competitiveness to US and China on tech and… 35

financial institutions announcing Gender equality 25

ambitious commitments to address Speed of innovation 23

climate change. Protection of personal data 18

Immigration of skilled workers 17

Europeans Prioritize Others 2

Sustainability

0 10 20 30 40 50 60

In a recent McKinsey survey of

Europeans, 54% of respondents Source: McKinsey and Company

indicated that environmental

sustainability is the area with the

biggest need for change in Europe’s

#European Company

society (chart at top right).17 Initiative Description

Relatedly, increasing concerns Companies Examples

around climate change are driving

GHG emission

changes in consumer preferences reduction targets

towards more sustainable

consumption. In a poll from October

(either well-below

2°C or 1.5°C 494

trajectory)

2019 of nearly 20,000 people across

28 countries, more than two-thirds

say they changed their behavior in 100% renewable

the past few years out of concern for

electricity

commitment 113

climate change.18

European Corporations Commitment to

49

use energy more

Commit to Climate Action productively to lower

GHG emissions

This consumer shift in behavior

is contributing to the dramatic

Commitment

increase we have seen in the

number of European corporations

to accelerating

transition to EVs 51

announcing climate commitments.

More than 1,500 companies with

a combined revenue of more than

$11.4 trillion announced in just science suggest that in order to meet These commitments and other

the last year their pledges to be “net the Paris Agreement temperature declarations have now positioned

zero” in emissions by 2050, including goals, the world must get to net zero corporations as major investors in

large European headquartered carbon in global carbon dioxide emissions by breakthrough climate technologies,

emitters such as BP and Shell. “Net mid-century, an effort that involves attractive potential acquirers for

zero by 2050” goals are important unprecedented changes across all the growing ecosystem of startups

commitments because the latest sectors of the economy. focused on climate solutions, and

17

McKinsey & Company. “How purpose-led missions can help Europe innovate at scale.” McKinsey & Company, 10 December 2019, https://

www.mckinsey.com/featured-insights/europe/how-purpose-led-missions-can-help-europe-innovate-at-scale.

18

Are you doing anything different in your life to combat climate change?” Ipsos, Energy & Environment, 10 March 2020, https://www.ipsos.

com/en/are-you-doing-anything-different-your-life-combat-climate-change.

Page 7Princeville Capital Supercharged Climate Positive®

as some of the largest buyers and March of this year, one of Sweden’s change. Storebrand also set a policy

developers of clean power (see chart national pension funds announced it that bans holdings in companies that

below). For a country like Ireland who was divesting from holding fossil-fuel get more than 5% of their revenue from

houses the data centers for tech giants companies as a way to manage the coal. In total, Storebrand divested

such as Google and Facebook (who financial risk posed by the low carbon $47 million from these companies–

have committed to 24/7 clean power energy transition – a move that is admittedly a mere fraction of their

and net zero by 2030, respectively), we estimated to affect approximately total assets under management –

expect a surge in renewable energy $400 million in investments.19 but sending an important signal that

deployment and advanced software divestment is reaching companies not

control solutions to manage their We anticipate that divestment efforts just because of their physical carbon

power grid. will create significant opportunities footprint, but extending to their policy

to redirect this capital into climate- and lobbying activities.

Financial Institutions aligned investments. For example,

Decarbonizing Portfolios at the end of 2019 the European We believe these macrotrends drive

In addition to European corporations Investment Bank launched a new accelerated growth for specific

driving demand for climate climate strategy that included an end European climate technologies and

technologies to meet their own to financing of fossil energy projects tech-enabled business models in this

commitments, we are encouraged by by 2021 and increasing the share of coming decade (2020-2030).

a growing set of financial stakeholders financing dedicated to climate action

and environmental sustainability to

focused on decarbonizing their

reach 50% of its operations in 2025.20

We anticipate that

own portfolios. From life insurers

to financial institutions, European We are also seeing other motivations divestment ef for ts will

investors’ appreciation of climate risk for divestment and restrictions cr eate signific ant

is growing, spurred by initiatives such on investing that translates into

oppor tunities to r edirect

more capital seeking sustainable

as voluntary commitments to disclose

investments. In August, Norwegian this c apit al into

climate risk, the introduction of

climate stress tests, and desire to limit life insurer Storebrand with about $91 climate - aligned

financial risk exposure from holding billion under management, divested investments.

stranded assets (made even more real from oil and chemical companies

during this summer’s wave of write- citing these companies’ lobbying and

downs by nearly every oil major). In advocacy positions against climate

Corporate Renewable

Corporate Renewable Energy Purchased Globally (MW)

Google 1683 1023

Facebook 671 440

Amazon 501 424

Microsoft 402 360

BHP Group 607

QTS Realty Trust 544

Wal-Mart 541

Ball Corp 227 161

Anheuser-Busch 310

Starbucks 242 50

Solar Wind

Source: BNEF NEF (2020), IEA

19

“AP1 divests from fossil fuels.” AP1, 16 March 2020, https://www.ap1.se/en/news/ap1-divests-from-fossil-fuels/; Pielichata, Paulina.

“AP1 cuts fossil fuels from portfolios” Pensions & Investments, 16 March 2020, https://www.pionline.com/esg/ap1-cuts-fossil-fuels-

portfolios.

20

“EU Bank launches ambitious new climate strategy and Energy Lending Policy.” European Investment Bank, 14 November 2019, https://

www.eib.org/en/press/all/2019-313-eu-bank-launches-ambitious-new-climate-strategy-and-energy-lending-policy.

Page 8Supercharged Climate Positive® Princeville Capital

III. Spotlight on Europe’s Climate Technology

Sector-Specific Opportunities

—

1 . G r e e ning t he E ne r g y G r id

With strong tailwinds Europe’s energy grid is undergoing According to the International Energy

significant transformation. Europe’s Agency, “utilities and grid companies

blowing in Europe to green expected new climate target of 55% in Europe (Iberdrola, Enel, Rte, and e.On)

the grid, decarbonize reduction in emissions from 1990 and in the United States (Exelon, Duke

transportation and levels by 2030 will require renewables and Edison International) reported

to reach 38-40% of total energy supply record spending on software.”22 At the

support an energy by 2030 (compared to ~19% in 2018)21 same time, Europe is experiencing a

efficient built This is creating a pivotal moment rise in customers seeking technologies

environment, this section for smarter and more resilient grids. to help them manage their energy

offers our insights into The region’s decarbonization of its supply and even become producers

energy systems and grid through themselves (e.g. residential and C&I

which technologies and the deployment of more flexible, solar solutions, batteries and energy

business models are renewable, and distributed energy storage options).

well-positioned to take assets are driving market expansion

flight. for innovative climate technology We have identified unique trends in

companies. Through our engagement the funding environment for resilient

with many leading businesses in the grid technology companies that

region, we are seeing an increase in will have an impact on the kinds of

investment and demand by utilities for exits we will see. Historically, this

intelligent solutions to manage a grid sector has been prone to M&A with

with higher volumes of intermittent corporates in the European energy

and distributed renewable power. sector actively acquiring disruptors

often fairly early in their growth cycle

(see chart below). But we anticipate a

Company European Energy-Related Acquisitions

21

Parnell, John. “EU’s New 2030 Climate Target Accelerates Renewable Deployment.” GTM, 17 September 2020, https://www.

greentechmedia.com/articles/read/eus-new-2030-climate-target-signals-accelerated-renewable-deployment.

22

Munuera, Luis (lead author) and Pablo Gonzalez (contributors), “Smart Grids.” International Energy Agency. June 2020, https://www.iea.

org/reports/smart-grids.

Page 9Princeville Capital Supercharged Climate Positive®

pause in corporate-led M&A as many of these corporates

(especially energy majors) are focusing on conserving cash EU 28 Annual Solar PV Installed

EU Installed

and the economic recovery for their core businesses. We Capacity 2000-2019

expect this will create opportunities for growth investors to

25.0

scale-up companies who are able to stay private longer and 22.2

create more value for investors.

20.0

17.2 16.6

We believe Europe will rapidly scale their renewable

deployment, transforming their grid permanently. This new 15.0 13.4

5.9

grid will shift from centralized fossil-fueled generation 10.0

10.0 8.2

towards decentralized renewable generation with an 6.5 8.2

6.8

increasing need for diverse types of distributed energy 5.7 5.8

0.8 1.1

resources (DERs). In this transformation, residential 5.0 0.2

2.1

clean energy solutions, along with large-scale solar, 0.3

1.1

0.10.2

wind, and storage will be the key asset types driving grid 0.0

decarbonization. The growing number of DERs across the

continent is already beginning to give rise to innovative

business models such as virtual power plants (VPPs)

that aggregate thousands of these resources to provide Source: Sunpower Europe 23

services to the grid. As the grid becomes more complex

and distributed, traditional utility monopoly business government subsidies (as shown in the chart below).

models are being disrupted unlike ever before, giving rise We see this growth as a continuing trend going forward,

to a new class of digital utility competitors. We describe as the economics for solar have become attractive in

these trends and the innovative models emerging in more multiple European countries.

detail below.

In terms of future solar deployment, we see residential

A. Residential Clean Energy Solutions solar as one of the keys to unlock Europe’s energy

decarbonization goals. The potential for solar rooftops

Climate Positive® Insights: Europe is poised for strong in Europe is large, with 90% of EU rooftops unused for

growth in rooftop solar and other residential clean energy solar, representing at least 600 GW of rooftop capacity

solutions due to improved solar economics that now across the EU.24 The primary drivers being high and

avoid heavy reliance on subsidies, electricity prices that rising household electricity prices (prices in Europe are

are among the highest in the world, strong consumer higher than in the US), continued decline in costs of PV

demand for clean energy solutions, and aggressive systems and batteries, and favorable policy stimulus

European decarbonization targets and associated policies. (such as policies that unlock increase distributed

Winners in this market will be those with the best unit energy resources and grid integration). When combined,

economics, a scalable and digitized business model, and research from analysis firm Wood Mackenzie finds that

a comprehensive product offering that can address a residential solar-plus-storage in Germany, Italy and

customer’s complete clean energy needs. Spain, is close to reaching grid parity (where costs per

kWh of grid power is the same or more than the cost per

kWh of the solar-plus-storage system).25 We see Europe’s

Solar installations in Europe experienced quick growth

residential solar market rapidly developing and following

during the 2007-2011 timeframe driven by strong

a path similar to the US (which has created multiple

policy stimulus, including high feed-in-tariffs. As solar

large players like Sunrun, Vivint, Sunnova and Tesla/

installations scaled during this period, many countries

SolarCity), as now all the conditions are in place for this

realized that their incentives were unsustainable (several

model to flourish.

countries faced steep increases in household electricity

prices due to surcharges coming from feed-in tariffs). As

a result, countries pulled back on their incentives, leading

to a drop in the market. In the last two years, however, with

prices of solar systems already in steep decline, solar

installations as a whole have experienced notable growth

acceleration, this time with relatively minor reliance on

23

Solar Power Europe. “EU Market Outlook for Solar Power 2019-2023.” Solar Power Europe, https://www.solarpowereurope.org/

wp-content/uploads/2019/12/SolarPower-Europe_EU-Market-Outlook-for-Solar-Power-2019-2023_.pdf?cf_id=7181.

24

Id.

25

McCarthy, Rory. “Europe Residential Energy Storage Outlook 2019-2024.” Wood Mackenzie, 24 July 2019.

Page 10Supercharged Climate Positive® Princeville Capital

Improving Customer Experience with Digital that residential solar companies can extract significant

Tools value and scale by creating a business model attached to

new homes that offers hybrid electric heat pumps, storage,

Following the growth of the residential solar market, we

smart devices, etc, This way they can deliver a more

have seen multiple startups entering this market in recent

comprehensive electrification package to the customer

years. Many of these startups are disrupting traditional

while also acquiring customers efficiently, traditionally a

residential solar business models by improving customers’

challenge in the rooftop solar industry. While we have not

experience for acquiring and owning solar systems in their

seen this business model emerge in Europe, we can expect

homes. They are offering financial innovations to offset

it will be arriving soon as residential solar penetration

the purchasing barriers created by high upfront costs.

continues to expand.

Companies like Solease (Netherlands) and Zolar (Germany)

are offering customers access to PV systems by paying a

low monthly fee that is lower or similar to what customers

B. Virtual Power Plants (VPPs) and Distributed

are currently paying for their electricity, enabling customers

Energy Resources (DERs)

to capture savings from the beginning.

Climate Positive® Insights: As countries across

Europe are moving to higher renewable penetration,

Startups like Enpal (Germany) similarly offer customers

the increased reliance on intermittent resources

the value of solar installed without the burden from a

is driving the need for, and increasing the value of,

substantial initial cost and instead offer customers fixed

flexible resources to balance the intermittent supply.

monthly payments less than or equal to their energy

savings. They have innovated on a proven business

Opportunities are arising for distributed assets and the

model by moving away from a traditional door-to-door

software that controls them to provide services to the

sales business model and taking an all-digital and virtual

electric grid. The market has historically featured many

approach to sales and marketing. According to Enpal’s

companies with good technology, but not enough assets

Founder and Chief Executive Officer Mario Kohle, “our long-

to control and a lackluster total available market to scale.

term vision is to be a complete clean energy provider to our

With renewables and DERs coming on to the grid faster

customers. Our digital tools are not only the foundation

than ever, there is now more need and opportunity for these

of this vision, but have made us more resilient throughout

companies to capitalize on these distributed resources.

the pandemic. By using digital marketing to generate leads

The winners in this market will be those businesses

and closing sales virtually, we were able to maintain strong

who can cost effectively gain operational control of a

sales through Q2 and Q3 this year.” Through Princeville

significant base of assets, aggregate them in ways to be

Capital’s investment in Enpal, we have seen how software

able to participate effectively in energy markets, and drive

tools like their automated roof evaluation and PV system

the most value so as to incentivize more asset owners to

design (leveraging satellite imagery, lidar and customer

participate.

photos) have helped drive down customer acquisition

costs, traditionally a major portion of the total cost to

serve and scale these businesses. These companies are As Europe moves toward a greater use of renewables for

also creating and deploying customer facing apps to track energy generation, we are already seeing the underlying

energy consumption and energy production of the installed weaknesses in Europe’s grid. This is reflected by the fact

PV systems. that many countries have sporadically experienced negative

energy prices (due to renewables generating too much

Expansion into Smart Home Ecosystem electricity at times of low demand), which create complex

challenges for operators trying to balance their grids.

As the European market matures, we predict growth for

Additional wind and solar power expected to be connected

these players as they move to other verticals related to

to the grid in future years will only worsen the situation

the customer’s home energy ecosystem, much like the US

and put unprecedented stress on the infrastructure. The

players have done in recent years. Players like Sunrun and

intermittent nature of renewables will create a mismatch

Tesla have leveraged their relationship with the customer

between supply of energy and demand, which the grid’s

to expand their product offering. All of the major players

infrastructure - designed for centralized fossil fueled

in the US now offer solar plus storage, access to smart

generation - is not prepared for. Further, without major

home devices that control energy use (EV chargers, smart

advances in grid flexibility, costly infrastructure upgrades

thermostats, etc) and many are thinking of the broader

and major amounts of new transmission lines will be

possibilities that arise from having a large installed base

required in order to accommodate very high levels of

of solar plus battery assets (e.g. companies are starting to

renewables.

develop and test out VPP and demand response offerings).

Beyond these service and device extensions, there is

also exciting opportunities for untapped market growth European countries will need to find new ways to balance

in Europe for those residential solar companies that can the grid with the additional wind and solar power expected

successfully attach to the new homes business. Through to be connected. As a global innovation leader, we

discussion with leading experts in this sector we learned asked Emmanuel Lagarrigue, Chief Innovation Officer

Page 11Princeville Capital Supercharged Climate Positive®

European

European VPP

VPP Market

Market Growth

Growth

16,000

3,500

14,000

3,000

12,000

2,500

10,000

MW

$ Millions

2,000

8,000

1,500

6,000

1,000

4,000

500

2,000

- -

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Capacity Market Revenue Implementation Spending

Source: Guidehouse Insights

for Schneider Electric, where he real-time, aggregated control of the • KiwiPower’s (Germany) white

thought Europe has a competitive available energy resources to meet label DER management platform

advantage in scaling distributed the ever-changing supply needs. has 1GW of energy assets under

energy resources and management? Europe’s DER capacity will outpace management and a 60MW

“Among the most uniquely positioned centralized generation capacity portfolio of battery storage in 10

opportunities are those enabling driving the growth of the VPP market, countries.

the proliferation of decentralized with analysts forecasting that the • t i k o E n e r g y ’s (S w i t z e r l a n d )

electricity generation and storage market size will reach $3 billion platform allows for the aggregation

assets. And that will be achieved annually by 2028.26 and ramping up or down of small

mostly with software, platform residential loads such as heating

business models and smart ESG With the growth of the DER market, we systems, coolers, PV systems,

financing.” Expanding on Lagarrigue’s expect to see an increasing number batteries or EV charging stations.

response, we expect energy storage of new startups entering the space,

to become a key flexible asset due and existing players scaling and But VPP endeavors are not limited to

to the plummeting technology costs. cementing their market position. We startups. Traditional utilities are also

Batteries will enable the storage of believe that there will be a greater entering this market. Earlier this year,

surplus wind and solar energy for use need for startups that leverage digital Centrica (UK) and sonnen (Germany)

at a later time. As battery storage and tools to track real time data from aggregated a network of batteries to

other distributed energy resources energy assets to optimize energy sell storage capacity when the grid

(DERs) are added to the grid, they will use. There are multiple examples is overloaded and discharge energy

drive demand for smart grid solutions of startups offering sophisticated back to the grid during periods of peak

to balance these DERs. The potential software platforms with quickly demand.27

and value of virtual power plants scalable business models. These

(VPPs) – networks of decentralized include: Similarly, in Italy, Enel X has begun

power generating, consuming, or aggregating residential energy

storing assets which can be flexibly • Moixa (UK) developed a cloud- storage systems to help balance

ramped up or down – will significantly based software platform that the grid.28 With utilities beginning to

increase. VPPs maximize the value of connects storage devices to the pilot their VPP programs, we expect

DERs and sophisticated management grid and applies AI to optimize to see significant M&A activities as

platforms are needed to provide power distribution. incumbent utilities see the threat to

26

Asmus, Peter. “The European Take on Virtual Power Plants.” Guidehouse Insights, 11 December 2019, https://guidehouseinsights.com/

news-and-views/the-european-take-on-virtual-power-plants.

27

“UK’s most advanced Virtual Power Plan announced.” Smart Energy International. 21 January 2020, https://www.smart-energy.com/

industry-sectors/storage/uks-most-advanced-virtual-power-plant-announced/.

28

Colthorpe, Andy. “Virtual power plants: Enel X’s aggregated home storage goes into action in Italy.” Energy Storage News, 16 January 2020,

https://www.energy-storage.news/news/virtual-power-plants-enel-xs-aggregated-home-storage-goes-into-action-in-it.

Page 12Supercharged Climate Positive® Princeville Capital

their existing business model and seek to protect their Frictionless Customer Onboarding Experience

positions. We anticipate, however, that with growth and Better Rates:

capital, some of these companies will be poised to

compete and win if they can control enough assets. • Customers can quickly switch to the new utility

online in only a few minutes (these utilities will

C. Digital “Challenger” Utilities manage the transition with the old supplier).

• Digital utilities allow easy access to a 100%

Climate Positive® Insights: The traditional utility

renewable energy & gas offering at lower rates than

business model is under threat from all sides. The rise

“traditional” utilities – often because the digital

of wind, solar, and other distributed resources is putting

utilities are nimble, carry less overhead, and have no

pressure on the traditional utility revenue model and a

hard asset costs that need to be recovered.

continuation of a global move towards deregulation is

loosening the grip that once dominant monopolies had

Direct Access to Energy Consumption and

on their respective markets. Customer expectations

Ability to Optimize All Energy Assets:

are also changing with consumers demanding better

customer service, digital tools, access to clean energy

• Leverage smart meters to give customers direct

options, and the ability to monetize their own distributed

access into their energy consumption and insights

energy resources. All of these factors are allowing a

into their electricity bill.

new crop of challenger utilities to enter the market.

• Provide apps and web-based sites to help customers

We have seen success with different models around the easily manage their accounts and energy bills.

world, but the common denominator across all of them

is a digitally enabled, engaging customer experience • Moving to other verticals like the electric vehicle (EV)

that gives consumers access to clean energy options. charging space. An example is OVO’s (UK) Vehicle-

The companies that are most disruptive are those that to-grid (V2G) trial where the company offers a V2G

are able to offer all of this while leveraging digital tools charger that optimizes EV charging costs by selling

themselves to reduce their operating costs below those of energy back to the grid in periods of high demand

the traditional utilities. We expect the winners to be those and charging the car when electricity is cheaper. This

that can continue to expand on their offering, adding company has also implemented an EV tariff program

additional services like home energy management and and signed a partnership with Polar’s EV charging

EV charging management, to give customers a simple and network to offer charging-as-a-service plans with

optimized clean-energy experience. 100% renewable energy.

“Utilities-in-a-Box”:

Europe is experiencing interesting developments in the

utility market, with new innovative business models

• Technology platforms that enable distributed energy

arising that challenge incumbent utilities’ grip on the

optimization for local and residential assets. For

market. It is not a coincidence that Tesla is showing

example, Germany-based GreenCom’s white label

renewed interest in the European energy market: Tesla

energy IoT platform connects residential distributed

has acquired a license to trade electricity in Western

assets and enables providers to launch digital energy

Europe and has recently conducted a survey in Germany

services that can turn these distributed energy

to gauge potential customer’s interest in a range of Tesla

assets into revenue streams, aggregated storage

energy products and services. Experts speculate that

capacity, and additional grid flexibility.

with the right partner in Europe, Tesla could launch a

material challenge to Germany’s incumbent utilities. But • Trading networks for solar and battery storage. For

Tesla is by no means the only company looking to do this. example, Social Energy’s utility model is delivering

renewable energy through a network of homeowners

In recent years, Europe has seen a rise in the number of with solar across the UK. Their smart energy platform

so-called “challenger” utilities such as OVO (UK), Bulb allows customers to generate, store and trade 100%

(UK), and Tibber (Norway). This is particularly pronounced renewable energy and get paid a market leading

in deregulated energy markets with fully open competition price for doing so. With their trading tariff, customers

among retail energy suppliers. These digitally enabled get access to lower cost green electricity.

players have challenged traditional business models by

offering customers a hassle-free way of accessing green

energy and gaining more visibility and control of their

energy consumption. Specifically, the business models

we see gaining the most traction offer some combination

of these services:

Page 13Princeville Capital Supercharged Climate Positive®

UK's Electricity

UK’s Electricity Supply Market Shares

Shares by

by Company

Company (%)

(%)

30%

25%

20%

15%

10%

5%

0%

Q1'04

Q3'04

Q1'05

Q3'05

Q1'06

Q3'06

Q1'07

Q3'07

Q1'08

Q3'08

Q1'09

Q3'09

Q1'10

Q3'10

Q1'11

Q3'11

Q1'12

Q3'12

Q1'13

Q3'13

Q1'14

Q3'14

Q1'15

Q3'15

Q1'16

Q3'16

Q1'17

Q3'17

Q1'18

Q3'18

Q1'19

Q3'19

Q1'20

British Gas EDF E.ON

npower Scotish Power SSE

Shell Energy OVO Energy Utilita

Utility Warehouse Bulb Octopus

Avro Energy Green Energy Network Small Supliers

Source: Ofgem

A prime example of the disruption “challenger” utilities have caused can be seen in the UK where the market was dominated

by its so-called “Big Six” suppliers (British Gas, EDF Energy, npower, E.ON UK, Scottish Power and SSE). New challenger

utilities like OVO (now the second largest in the UK after acquiring SSE), Bulb and Octopus have taken considerable market

share from the established utilities.

But the story playing out in the UK is happening in markets across Europe to one degree or another. We expect many

opportunities to arise in the coming years from new utilities that can best capitalize on all of these emerging trends in the

energy market.

Page 14Supercharged Climate Positive® Princeville Capital

2 . De c ar boni z in g Tr an s por t

As global climate technology investors, we have closely followed emerging regional trends that support decarbonization

in Europe’s transport sector, estimated to be approximately 24% of total greenhouse gas emissions in Europe. But more

specifically, we are focused on the trends, technologies and tech-enabled business models that reduce emissions from

road transport which is responsible for an overwhelming majority (72%) of Europe’s transport sector emissions.29

A key regional trend is the transition from carbon emitting internal combustion engine (ICE) vehicles to more Climate

Positive® electric vehicles (EVs). This is because the pace at which EVs are deployed has a direct impact on the

opportunities for associated technologies, such as EV charging, to scale faster. We believe that the pace of EV growth in

Europe in the next decade will be transformative for companies in these subsectors.

While other key EV markets in the US and China have seen dips in EV sales, Europe has experienced significant growth in

EV sales. In 2019, EV sales in Europe increased by 44%, the highest growth rate since 2016. This growth led the European

EV market to command 26% share of the global EV market as the charts below illustrate.30

Global Electric-Light-Vehicle

Electric-Light-Vehicle Sales Global Electric-Light-Vehicle

Electric-Light-Vehicle Sales

by Region by Region

100% 2.5

90%

80% 2

70%

Million Units

60% 1.5

% Share

50%

40% 1

30%

20% 0.5

10%

0% 0

2015 2016 2017 2018 2019 2015 2016 2017 2018 2019

China Europe United States Rest of World China Europe United States Rest of World

Source: McKinsey and Company

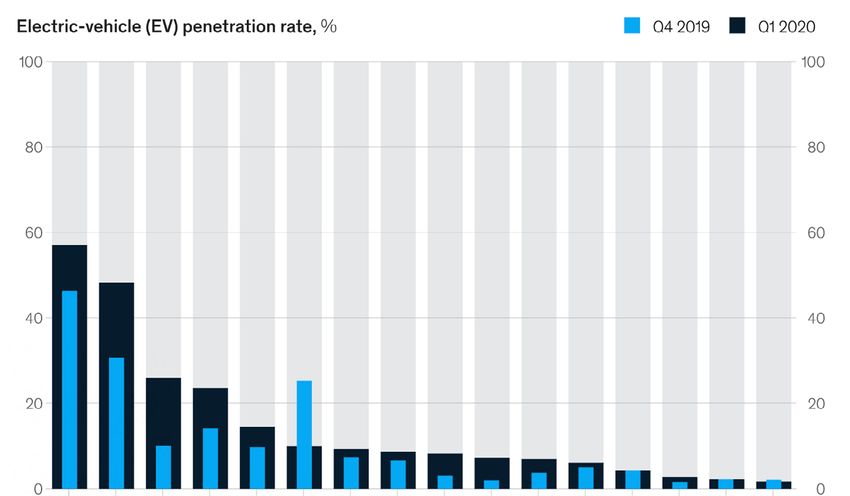

Additionally, in contrast to a slowdown in EV sales globally in the first quarter of 2020, nearly all core markets in Europe

saw significant increases in EV penetration. In the first quarter of 2020, with the exception of Hong Kong, all of the top 10

markets for EV penetration were in Europe. Overall, the EV penetration rate in Europe increased to an industry-best 7.5%

in early 2020.31

29

European Academies Science Advisory Council, “Decarbonisation of transport: options and challenges.” European Academies

Science Advisory Council. March 2019, https://easac.eu/fileadmin/PDF_s/reports_statements/Decarbonisation_of_Tansport/EASAC_

Decarbonisation_of_Transport_FINAL_March_2019.pdf.

30

McKinsey & Company Automotive & Assembly Practice. “McKinsey Electric Vehicle Index: Europe cushions a global plunge in EV sales.”

McKinsey & Company, 17 July 2020,

https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/mckinsey-electric-vehicle-index-europe-cushions-a-

global-plunge-in-ev-sales.

31

Id.

Page 15Nine of the top 10 EV penetration rates are in Europe

Princeville Capital Supercharged Climate Positive®

EVPenetration

EV PenetrationRate

Rate (%)

(%)

60

50

40

30

20

10

0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Europe Q4’19 Q1’20 Rest of the world Q4’19 Q1’20

Source: McKinsey and Company

Europe benefits from the same macro conditions that the goal of 1 million public chargers by 2030.

are driving the acceleration of EV adoption around the This is to be accomplished by offering local

world – factors including total cost of ownership (TCO) authorities and municipal enterprises a 50-60%

of EVs becoming competitive with and even surpassing subsidy on charging stations from any provider.

the TCO of ICE vehicles, maturing technologies in the EV This program has created a surge in consumer

ecosystem, and a larger influx of capital both among EV confidence in EVs, leading to a record breaking

startups and incumbent automakers that are shifting 11% EV penetration in July auto sales in Germany.

development dollars to electric models, all leading to – In France, President Macron announced an €8

greater EV deployment. However, it is Europe’s policy billion rescue plan for the local auto industry and

environment that makes its market particularly unique and set a goal of having over 100k public charging

supports EV outperformance relative to the US or China. points next year, producing 1 million EVs annually

Here are a few key policy developments (not exhaustive) by 2025, and boosting EV adoption rates. This will

that we have built into our analysis. be accomplished through a combination of EV tax

benefits to drivers (up to €5,000 for the purchase

• The European Commission’s 2020/21 emissions of used or new EV upon scraping ICE vehicle),

standard – 95g of CO2/km – went into effect on and subsidies to condominiums, workplaces, and

January 1, 2020 and is unsurprisingly boosting EV municipalities on installing charging points via

sales as it requires that 95% of the new passenger any private supplier.

vehicle fleet must meet this standard in 2020 and 100%

in 2021. Two additional key trends are adoption and growth in

• Many European cities and member states are pushing the digitalization (e.g. Information and Communication

for even more ambitious emissions reductions goals Technology) that will benefit market segments such as

independent of EU policy: the mobility sector and new policy tailwinds for these

– 19 cities have announced plans to reach zero technology-enabled mobility solutions. For example,

emissions ahead of the Green Deal’s 2050 the automotive industry is one of the most digitalized in

deadline, with Norway being the most ambitious Europe and an overwhelming majority (81%) of respondents

– resolving to have 100% of new vehicle sales be from the European automotive sector believe the digital

carbon free by 2025. economy will bring the most positive opportunities for

– In Germany, Chancellor Merkel announced a €50 growth.32 ICT applications in mobility are already on the

billion COVID recovery program, which included rise and we expect this to be accelerated due to new policy

€2.5 billion investment into EV chargers, with momentum generated by the Green Deal which explicitly

32

European Commission, “Objectives of Digital Transformation Scoreboard 2017: Evidence of positive outcomes and current opportunities

for EU businesses.” January 2017.

Page 16You can also read