THE TOTAL FEED BUSINESS - FORFARMERS N.V. ROADSHOW PRESENTATION 1H 2017 - FORFARMERS GROUP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

the total feed business ForFarmers N.V. Roadshow presentation 1H 2017

NOTIFICATIONS AND DISCLAIMER REPORTING STANDARDS PUBLICATION 2017 HALF-YEAR REPORT The 2017 half-year report (incl. condensed consolidated interim financial statements) will be available from 17 August 2017 on the ForFarmers website (www.forfarmersgroup.eu). REPORTING STANDARDS The results in this presentation are derived from the ForFarmers 2017 half-year financial statements, which have not been audited by the external auditor, and have been drawn up in accordance with the International Financial Reporting Standards as adopted by the EU (IFRS). General remark: percentages are presented based on the rounded amounts in million euro SUPERVISION In view of the fact that shares are freely tradable on EURONEXT Amsterdam, ForFarmers operates under the supervision of the Financial Markets Authority (AFM) and the company acts in accordance with the prevailing regulations for share-issuing companies. IMPORTANT DATES 09-11-2017 Publication Q3 2017 Trading Update 13-03-2018 Publication 2017 annual results 26-04-2018 Annual General Meeting 03-05-2018 Publication Q1 2018 Trading Update 16-08-2018 Publication first half-year 2018 results FORWARD-LOOKING STATEMENTS This presentation contains forward-looking statements, including those relating to ForFarmers legal obligations in terms of capital and liquidity positions in certain specified scenarios. In addition, forward-looking statements, without limitation, may include such phrases as “intends to”, "expects“, “takes into account”, "is aimed at“, ''plans to”, "estimated" and words with a similar meaning. These statements pertain to or may affect matters in the future, such as ForFarmers future financial results, business plans and current strategies. Forward-looking statements are subject to a number of risks and uncertainties, which may mean that there could be material differences between actual results and performance and expected future results or performances that are implicitly or explicitly included in the forward-looking statements. Factors that may result in variations on the current expectations or may contribute to the same include but are not limited to: developments in legislation, technology, jurisprudence and regulations, share price fluctuations, legal procedures, investigations by regulatory bodies, the competitive landscape and general economic conditions. These and other factors, risks and uncertainties that may affect any forward-looking statements or the actual results of ForFarmers, are discussed in the last published annual report. The forward-looking statements in this presentation are only statements as of the date of this document and ForFarmers accepts no obligation or responsibility with respect to any changes made to the forward-looking statements contained in this document, regardless of whether these pertain to new information, future events or otherwise, unless ForFarmers is legally obliged to do so. 2

The European leader in Total Feed solutions

Overview ForFarmers’ products, clients and species

#1 European Total Feed solutions provider Compound

Servicing over 25,000 farmers feed Ruminant

Total Feed volume of 9.3mT1)

Specialties On-farm

Total

Completed 9 acquisitions since 2012 advisory All farm

Feed Swine

and sizes

Approx. 2,273 employees2) Dry Moist solution

support

Liquid (DML)

− 632 commercial functions3)

• c. 400 on site advisors Poultry

Crop

ForFarmers’ core markets Sustainable growth on the back of acquisitions

Locations (42) EURm EURm

Dutch GAAP IFRS

Headquarter

450 424 407 150

401 390 394

Acquisitions 94

300 86 90 100

81

69

NL UK GE BE 150 114 119 50

30 34

Volume1): 46% 32% 22%

1) Total Feed volume 2016 in million metric tonnes (mT)

0 0

2) FTEs as at year-end 2016, excludes dealers 2010 2011 2012 2013 2014 2015 2016

3) As at 31/12/2016

Source: ForFarmers

Gross profit EBITDA (RHS)

3

Executive committee

Yoram Knoop Arnout Traas

Chief Executive Officer Chief Financial Officer

Dutch, age 48 Dutch, age 58

CEO ForFarmers since January 2014 CFO ForFarmers since August 2011

Previous experience includes Previous experience includes

− 2011, MD Cargill − 2009, M&A FrieslandCampina

− 2007, MD Provimi − 2001, Finance Campina

− 2001, MD Quest − 1994, Finance Vendex

− 1993, GM Owens Corning − 1983, Arthur Andersen

4/10 6/16

Steven Read Stijn Steendijk

Purchasing, Pricing & FormulationOperations and supply Chain Strategy & Organisation

Since June 2014 Since July 2014

Functions

Previously BOCM PAULS Previously Provimi, Unilever

31/31 3/8

Adrie van der Ven Iain Gardner Jan Potijk

COO Germany, Belgium and new markets COO United Kingdom COO the Netherlands

Countries

Since January 2016 Since July 2012 Since September 2000

Previously Louis Dreyfus, Nutreco, Previously BOCM PAULS With the company since 1983

Cargill

2/8 29/29 34/34

1) Including years at BOCM PAULS

x/x Years with the company1)/Years active in the industry Source: ForFarmers

4

From regional compound feed cooperative to leading

European listed Total Feed company

1896 1901 2000 2003 2005 2006 2012 2014 2016

Expansion Back to International

Foundation

in the value chain the core expansion

Organisation

Incorporation of Several cooperative mergers, Launch of the ‘Equity Separation cooperative Listing on

cooperative including the merger of ABC on Name’ (VON) and business Euronext

and CTA into ABCTA initiative operations; Amsterdam

new name ‘ForFarmers’

Focus on

Total Feed solutions

Various acquisitions: Various divestments:

Business

Purchase and sales Cefetra Cefetra (2012) International expansion in

organisation Plukon Plukon Belgium, Germany and the UK

Esbro Esbro

Nutreco partnership in

Specialties and Micros

Feed volume sold

100% 85% 15%

to members

Source: ForFarmers

5

Ownership

At year end 2016, the cooperative FromFarmers had a direct stake in ForFarmers of 20.8% and a controlled stake of 59.4%¹)

The directly controlled stake of 20.8% will be reduced to approximately 17.5%, allocating the last final tranche of equity to

individual members mid 2017

The allocated equity is held by individual members in the form of a position on Participation Accounts (PAs) or in Depositary

Receipts (DRs), which were tradable on a Multilateral Trading Facility until 23 May 2016

Since the listing of ForFarmers on Euronext Amsterdam on 24 May 2016, PAs and DRs can no longer be traded. Holders of PAs and

DRs can convert their positions into Shares at their full discretion and without involvement of ForFarmers or FromFarmers.

Third parties held 34.7% as at year end 2016.

Development

ownership structure Average daily traded volume more than tripled (from approx. 40,000 per day on trading platform) on Euronext Amsterdam

(**??on the basis of double counting??)

100% 4.7% 5.8% 9.4%

5.9% 23.6%

30.7% 34.9% 36.3% 35.6% 32.5%

80% 37.8%

8.1%

60% 12.4%

17.5% 82.5%

25.9%

95.3% 94.2% 31.1% 39.0%

84.7% 46.8%

40%

68.3%

56.9%

47.5%

20% 37.8%

31.1% 25.4% 20.8% 17.5%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cooperatie Other2 Members participation accounts Total 3rd party

1) This consists of 20.8% direct control Shares, 32.5% Shares for which Participation Accounts have been issued) and 6.1% voting instructions on the Depositary Receipts of members (as per 31/12/2016).

In addition, FromFarmers can also give voting instructions in relation to DRs which are held by others than members

2) Consists of Members with certificates, Lock up shares employees, and third parties

6

ForFarmers addresses increasing need

for sustainable food production

Vision

We aim to be the leading livestock nutrition company in Europe by supplying economic and

sustainable Total Feed solutions on farm

Mission

‘For the Future of Farming’ is ForFarmers’ promise to farmers: we work side-by-side with our

customers for the long-term good of their farms and of the sector as a whole.

Core values

Ambition Sustainability Partnership

We drive for next level results We are here to stay We believe in win-win

7

8

Key investment highlights #1 Total Feed solutions provider to farmers in Europe with leading positions Active in resilient markets with growth opportunities Central position in value chain to farmers Focussed strategy to further enhance and expand business: Horizon 2020 Clear and proven M&A strategy to drive further expansion Sustainability is a vital element in business model Attractive financial performance and profile 9

Complete portfolio to support our trusted advisor role

Product Description Application Examples Value add

Compound feed

Mix from various

raw materials Finished products to be fed as a Compound feed

and premix and complete feed to animals Blends

additives

Specialty feed additives Premixes

Additives (e.g. Selko)

Specific Dairy Speciality (Translac)

Specially designed for home mixing,

(complex)

nutrients

young animals and animals in transition Piglet feed (VIDA)

Calf milk replacers (e.g. VITAMILK)

Concentrates (e.g. MIXX, Blendix)

DML

Rapeseed meal (D)

Feedmix RV (D)

Dry, Moist and

Beet pulp (M)

Liquid (DML) co- Supplemental to rations

Corngold® (M)

products

Citrocell (M)

DGS Protiwanze® (L)

Crop

Broad product Seeds (Topgrass)

Nutrient planning, cultivation

portfolio to Silage additives

techniques, crop protection, rotations,

support crop Crop protection

variety choice, etc.

production Fertilisers

Source: ForFarmers

10Total Feed solutions tailored towards key species

Focus on key species Volumes in core countries per key species and products (2016)1)

Total per species Total per product

Dairy

Ruminant

Beef, Goat, Sheep

Ruminants Compound feed

Swine Specialties

Key species

9.3mT 9.3mT

Sows and piglets Poultry DML

Swine

Fatteners Other Crop

Other

Layers

Poultry Netherlands Belgium/Germany United Kingdom

Broilers

4.3mT 2.0mT 3.0mT

Organic feeds produced for all species

Other species

(e.g. horses, turkeys)

Other

Crop

4.3mT 2.0mT 3.0mT

1) Excludes intercompany sales

Source: ForFarmers

CAGR 15E-20F: 1.0% CAGR 15E-20F: 0,1% CAGR 15E-20F: 0,4%

11Focussed on feed solutions delivered on farm

Additives producers Premix producers

Distributors

Dairy processing,

Livestock Retail &

slaughterhouse &

Feed mills and farmers consumers

Grains & Commodity egg packers

oilseeds traders/ specialty feed

growers processors producers

Focussed Non-listed Listed

Access to farm gate

players (illustrative)

Companies

active

in multiple

segments of

the value

chain

ForFarmers’ position in value chain has advantages

Direct access to the farm

Integrated solution provider to the farmers

No channel conflicts

12 Source: ForFarmersLeading market positions in ForFarmers’ markets

Feed production volumes of the largest producers in Europe (2014-15, mT)1) Leading positions in core countries (2015)2)

Aqua feed

Netherlands

ForFarmers 6.4 Company Compound feed production (mT) Total feed

#1 Agrifirm 2.7

De Heus 6.0 #2 ForFarmers 2.6 #1

Nutreco #3 De Heus 2.0

3.9 2.0

#4 Fuite 0.7

DLG Group 4.5

United Kingdom

Agrifirm Feed 4.3 Company Compound feed production (mT) Total feed

#1 AB Agri 2.2

Agravis Raiffeisen 4.1

#2 ForFarmers 2.1 #1

Avril Group 3.4 #3 2Agriculture3) 0.7

#4 Noble3) 0.7

Veronesi 3.2

Belgium

Deutsche Tiernahrung 2.8 Company Compound feed production (mT) Total feed

#1 Aveve 1.3

InVivo 2.7

#2 VandenAvenne 0.6 #3

Danish Agro Group 2.4 #3 ForFarmers 0.5

#4 Quartes 0.4

AB Agri 2.2

Germany

Triskalia 2.0 Company Compound feed production (mT) Total feed

#1 Agravis 3.6

Broring 1.7

#2 DTC 2.4 #4

Aveve 1.6 #3 Bröring 1.5

#4 ForFarmers 1.1

1) WattAgNet (latest available data); comprises poultry, pig, ruminant, pet, horse and aqua feed, compounds, premixes, additives, integrators and vendors and may include volumes outside EU

2) ForFarmers’ estimates

3) Noble and 2Agricullture are vertically integrated players; ForFarmers is #1 amongst the non-vertically integrated players

Source: ForFarmers, WattAgNet

13Resilient markets with growth opportunities

Provides potential for increasing usage of

data recording systems 5 1 Provides for changing customer needs

Share of ForFarmers’ dairy customers using data Distribution of swines by farm size in

recording systems by country (in %) ForFarmers countries of operations2)

1 Farm size in LSU1)

NL 57%

Over 500 32% 36% 42% 50%

UK 25%

Increased use

of data in Shift in farm 57%

DE 16% farm size 100-500 55% 50%

5 management

44%

2 Less than 100 11% 9% 8% 6%

BE 5%

2005 2007 2010 2013

Changing

industry

More home

trends and

mixing

consumer Investment of larger farms into home-mixing provides

Feed industry provides solutions for 4 preferences 2 opportunities to leverage the Total Feed Business portfolio

Split of total feed demand by product type, in the Dutch swine

1. Non-GMO demand by retail segment (in % of total)

More

2. Support of higher number of piglets per sow with demanding

milk replacers 4 legislation Premix

3 Moist & Liquid co-products

Dry co-products 51% 56%

Young animal feed

Concentrates

Requires new solutions from feed industry 3

1. Minimise ammonia (NH3) and phosphorus (P) Compound feed

emission (in the Netherlands from 2017)

2. Specialised feed to reduce aggressiveness of

chickens

2015 2020

1) Live stock unit (LSU, a Eurostat definition) - measure of economic value of each animal type. 1 LSU = 1 cow or c. 143 broiler chickens or 2 breeding sows

2) Aggregate of BE, NL, DE and UK

14Central position in value chain to farmers

ForFarmers’ From Feed To Farm approach

ForFarmers: Dairy processors,

Raw materials Retail &

Production, supply and application of Farmers slaughterhouses &

suppliers Consumers

Total Feed solutions egg packers

Formulation, Logistics &

On-farm feed solution advisory Feed milling

Nutrition & Procurement delivery

Source: ForFarmers

15Partner and deliver the Total Feed Business portfolio

Case study: an integrated Total Feed proposition for dairy

Delivering customer value

Integrated approach - tool for integral farm optimisation

Milking Transition Rearing Roughage

High & healthy milk Improvement health Optimal life-start More production

productions & fertility & high quality

Modular portfolio

structured along core

farm processes

TRANSITION Roughage

Optifeed CRV Mineral

Support tools to Checklist plan Checklist plan Fertilizing

Dietplan

deliver the best

solution & monitor

results

Monitoring: animal feed profit & animal analysis

On-farm application On-farm advisory and support is delivered by advisor

Source: ForFarmers

16Strategy Horizon 2020: further enhance & expand business in Europe+ Source: ForFarmers 17

Clear and proven M&A strategy to drive further expansion

Likely to be more frequently occurring acquisitions One-off nature

Fine-tune NL & UK Strengthen BE & DE Expand beyond home-markets

Ongoing initiative to further build on Ongoing initiative to increase market Tap into fast growing, large &

strong existing positions access, volumes and efficiency attractive markets in Europe-Plus

Rationale for leading market share Several elements may be driving one-off expansion opportunities

Sourcing

Leverage sales force and organise it by species

Wider application Proven nutritional knowledge

Optimise production capacity with dedicated plants by

Scale of ForFarmers’ Track record in logistics optimisation

species Function expertise: specie strategies, sales excellence,

capabilities

Leverage overhead and R&D functions go-to-market approached

Leverage overhead functions

Add capabilities or segments to the portfolio Perspective of Nutrition and innovation

synergies Go-to-market strategies

Portfolio − Capabilities: DML, Crop, specialties

Overall best practice sharing

− Segments: e.g. sow, piglets, poultry or dairy

Faster growing markets with local/regional consolidation

Region/country

opportunities

specific aspects Sizeable free markets with attractive specie characteristics

Regional market High regional market shares in order to optimise logistics

Proper and detailed risk analysis (political, compliance,

share Direct access to the farmer with plants located near by Risk assessment currency)

Source: ForFarmers

18Strengthen positions in Belgium and Germany

Strong logistical & production expertise and high market shares drive economies of scale

Local/regional market share is an important driver of profitability Lower levels of consolidation may provide opportunities1)

7% The UK

NL

6%

EBIT margin (2016)

5% c. 150 Top 3 The Netherlands

UK players

4% c. 90

3% players Top 3

DE/BE

2%

1%

0%

Germany

0% 5%

Market 10% feed (2016) 15%

share compound

Top 3

Feed production has been stable and moderately growing (in mT) Belgium c. 300

players

CAGR

c. 50 Top 3

2004-14

players

6.2 0.3%

6.0 Top 3

6.0

23.1 1.8%

19.3 20.0

2004 2009 2014

Sources: Feed production volumes Germany, the United Kingdom, the Netherlands and Belgium from FEFAC industrial compound feed production data, market share top 3 and number of players in

Netherlands and Belgium ForFarmers’ estimates, number of German players based on Deutscher Verband Tiernahrung data, number of players in UK based on AG Industries estimate. Includes feed for

poultry, cattle and pig categories, as defined by FEFAC (other categories such as pet food, are not included

19Sustainability is a vital element in business model Source: ForFarmers 20

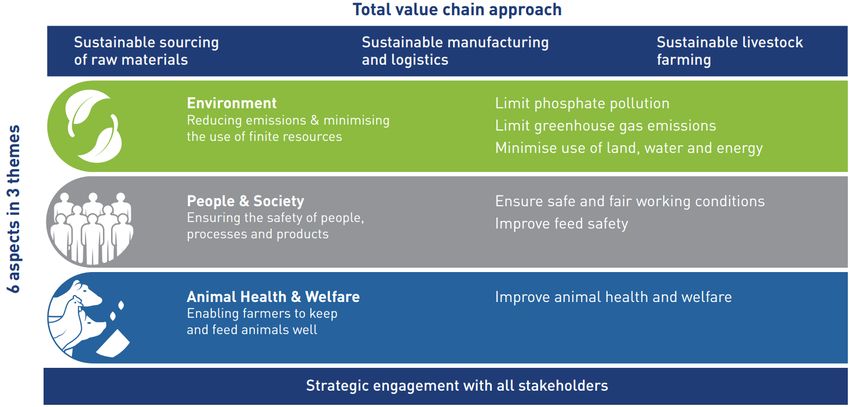

Sustainability: key element in Horizon 2020 strategy

Theme Material Aspect KPI

Limit phosphate pollution 1) % phosphate efficiency on farm in NL

(dairy and swine farmers)

Environment

Limit greenhouse gas emissions 2) GHG emissions in metric tons of CO₂

equivalent

Minimise the use of land, water and energy 3) % sustainable soy bean meal and palm oil

Ensure safe and fair working conditions 4) Number of Lost Time Incidents

People and society

Improve feed safety 5) Total number of feed incidents of non-

compliance with regulations and voluntary

codes

Improve animal health and welfare Improve animal health and welfare is deemed

an integral part of Total Feed solutions for

which no KPI is specifically set

Animal health and welfare

Source: ForFarmers

21FINANCIALS H1 2017 22

Highlights

First half-year 2017

Recovery agricultural sector, particularly on the Continent ForFarmers performance per cluster

- Financial position farmers improved due to higher milk and swine NL : 17.6% growth underlying EBITDA1

prices; egg prices on Continent better than in 1H 2016, in UK still

under pressure G/BE: 3.8% growth underlying EBITDA

- Ruminant: slight volume growth NL, impact phosphate measures UK: 27.5% decrease underlying EBITDA

limited; G/BE growth, volume decrease in United Kingdom (‘UK’) (including 9.5% negative currency translation )

due to reduced herds

Group

- Swine: volume increase due to Vleuten-Steijn (NL); G/BE growth; overhead: Decrease of costs realised of €1.1m

UK volume stable despite reduced herds

- Poultry: volume growth to broiler farmers in all clusters, particularly 14.8% growth underlying EBITDA at constant currencies

in G/BE; increase volume to layer farmers in NL and G/BE,

UK volume stable

Growth in Total Feed volume (3.6%) - Share buy-back programme: repurchased for €23.6 million

Higher growth compound feed (6.2%) mainly due to acquisition

- Supply chain optimisation plan (UK): steady progress

Gross profit: 0.4% increase (incl. negative currency translation

impact of 3.2%); like-for-like increase: +2.8% - Sustainability:

Melk€fficient helps farmers reduce phosphate production

Feed2Milk forms base for new dairy range in UK

AMR2 meetings organised in UK

(1)EBITDA excluding incidentals

(2) AMR = Anti Microbial Resistance

23Solid growth underlying EBITDA1

Total Like-for-

(in €m) 1H 17 1H 16 Currency M&A2 Explanation

Change Like3

Volume Total Feed 4,725 4,562 3.6% - 2.6% 1.0% Growth in NL and G/BE, decrease in UK

Growth in NL and G/BE: higher volumes, better

Gross profit 207.3 206.5 0.4% -3.2% 0.8% 2.8% product mix & formulation; decrease in UK: fewer

animals, lower-value feed

Other operating income 0.5 2.4 1H16: incl. incidental gain from land sale and Leafield

NL and G/BE higher due to strengthening organisation,

Employee benefit expenses -75.4 -77.0 UK: lower (reorganisation effect)

Effect of €1.1m due to extension depreciation term

Depreciation and amortisation -12.7 -13.2

(mainly plants & machinery)

Continent: more volume related production costs, UK:

Other operating expenses -81.0 -85.9 savings, (net) release €1.1m provision bad debts. 1H16

incl. €1.5m for listing

Total Operating expenses -169.1 -176.1 -4.0% -3.4% -0.1% -0.5% 1H16 incl. €1.6m for reorganisation UK

Operating profit (EBIT)

38.7 32.8 18.0% -2.5% 5.2% 15.3%

incl. incidental items

EBITDA 51.5 46.0 12.0% -2.9% 4.3% 10.6%

Centralisation back office activities. 1H16:

Incidental items 0.3 0.3 reorganisation costs (UK) largely compensated (sale of

land and Leafield)

Underlying EBITDA 51.7 46.3 11.7% -3.1% 4.3% 10.5%

Translation-effect 1.4 Devaluation Pound sterling

Underlying EBITDA at

53.1 46.3 14.8%

constant currencies

General remark: percentages are presented based on amounts rounded in million euro and additions may lead to small differences due to rounding

(1) EBITDA excl. Incidental items; (2) M&A means net effect acquisitions/divestments;

(3) like-for-like is excl. currency and effect of acquisitions/divestments

24Solid profit improvement

(in €m) 1H 2017 1H 2016 Explanation

Operating profit 38.7 32.8

Interest charges UK lower due to one-off payment into

Net finance costs -0.8 -2.0

closed pension fund

1H16: contribution warehouse activities HaBeMa negatively

Share of profit of equity-accounted investees,

1.8 1.5 impacted on lower trading volumes due to decreasing

net of tax

commodity prices

Income tax expense -9.1 -7.2

Profit for the period 30.6 25.1 Up by 21.9%

Adjustment tax rules in NL on innovation subsidies and

Effective Tax Rate (in %) 24.2% 23.3%

relative share UK results were lower

Non-controlling interests -0.2 -0.1

Profit attributable to owners of the company 30.4 25.0 Up by 21.6%

Basic earnings per share up 22.0%

Basic earnings per share (in €) 0.288 0.236

underpinned by share buy-back programme

General remark: percentages are presented based on amounts rounded in million euro

25Healthy capital structure

Condensed consolidated balance (In €m) 30-06-2017 31-12-16

(In €m) 30-06-17 31-12-16 Solvency ratio1 52.2% 55.3%

ROACE2 23.6% 21.1%

Non-current assets 336.9 333.6

Net Working capital 111.1 119.9

Current assets Other current assets 296.7 289.8

- Cash and cash equivalents 147.7 152.9 Other current liabilities 185.7 170.0

- Other current assets 296.7 289.8

Overdue receivables 15.2% 18.6%

Total assets 781.3 776.3

Net Debt / (Cash) (36.5) (61.5)

Equity 407.8 429.0

Equity: impact of share buy-back programme

Non-current liabilities

- Loans and borrowings 44.7 45.6 Other non current liabilities comprise a.o. pension

- Other 76.6 86.2 liabilities; early January one-off payment €11.7m in

closed fund UK

Current liabilities

- Bank overdrafts 66.5 45.5 (1) Solvency ratio is total equity divided by total assets

- Other current liabilities1 185.7 170.0 (2) ROACE means underlying EBITDA/average capital

employed on 12 months rolling average

Total equity and liabilities 781.3 776.3

(1) incl. current loans and borrowings

Additions may lead to small differences due to rounding

26Growth Return on Average Capital Employed (ROACE)1

Increasing return on consolidated average capital employed (ROACE) ROACE per geographic cluster for 1H 2016 & 1H 2017

24%

1H 2016 1H 2017

23%

46.2%

44.2%

22%

21%

23.6%

20%

21.6% 15.1%

21.1% 13.1% 12.7%

20.5% 11.1%

19% 20.0%

19.2%

18%

2014 2015 2015 2016 1H 2016 1H 2017 NL D/BE VK

1) ROACE up to 2015: Underlying EBITDA/average capital employed (begin – end year); ROACE varies significantly amongst clusters:

as of 2016: Underlying EBITDA/average capital employed on 12 months rolling average; NL assets based on historical value, assets G/BE and UK on market

2015 adjusted to enable comparison, Reference made to Note 27 Financial Statements value on moment of acquisition

2016

27Total Feed volume development

Volume Total Feed: +3.6% (4.7 mT) Total Feed volume development per cluster

- Compound feed +6.2% (3.3 mT) 4,725

1H 16 1H 17 4,562

The Netherlands: + 8.4% (2.2 mT)

- volume growth in ruminant and poultry

- strong volume growth in swine resulting from Vleuten-Steijn

acquisition (excl. VS: small decline)

- higher increase compound feed than Total Feed 2,222

2,051

- significantly higher volume increase organic feed

(Reudink) 1,535 1,475

977 1,027

Germany/Belgium: +5.2% (1.0 mT)

- significant volume growth in layers (poultry)

- volume growth in ruminant, swine and broilers (poultry)

- higher growth in compound feed than Total Feed NL G / BE UK Total

United Kingdom: -3.9% (1.5 mT) 1H 2017 Volume split per cluster

- impact divestments, like-for-like decline 1.8%

- volume decrease in ruminant

- volume to swine farmers stable UK

- volume growth to poultry farmers NL

31%

- decline in volume compound feed in line with Total Feed 47%

G / BE

Development percentages are presented based on actual 22%

(non-rounded) volumes in tonnes

28Gross profit: growth NL and G/BE larger than decrease UK

Total

Currency Like-for-like2

(in €m and %) Reported Difference M&A1

impact movement

2016 – 2015 2016 vs 2015

Gross profit 207.3 206.5 0.8 0.4% -6.7 -3.2% 1.6 0.8% 5.9 2.8%

Gross profit per cluster Gross profit

1H16 1H17

The Netherlands: + €11.8 million (12.0%)

206.5 207.3

- Higher volumes (like-for-like & by means of acquisitions)

and growth organic feed

- More high-quality feed & better formulation

110.2

(optimal use of ingredients in feed) 98.4

- Increase gross profit Reudink (organic) and Pavo (horse feed) 73.4

60.8

- Vleuten-Steijn acquisition per 1.10.2016 34.5 36.1

Germany / Belgium: + €1.6 million (4.8%)

- Higher volumes (direct and through attracted new dealers) NL G / BE UK Total(1)

- Better product mix and further improvement formulation

(1) Incl. Group/eliminations (0.2) for

both 1H16 and 1H17

United Kingdom - €12.6 million (-17.2%)

- Negative currency translation effect of €6.7 million

- Lower volumes on cattle and swine herds (number of animals have not

yet recovered)

- Divestment effect non-core activities Wheyfeed and Leafield

- Cattle farmers continued to buy lower value feed

- Margin pressure in swine sector due to ongoing consolidation

Additions may lead to slight differences due to roundings; (1) M&A means net effect acquisitions/divestments;

(2) Like-for-like means excluding currency impact and net effect acquisitions & divestments

29Results per cluster

(in €m) The Netherlands Germany/Belgium United Kingdom Group/Eliminations Consolidated

1H-2017 1H-2016 1H-2017 1H-2016 1H-2017 1H-2016 1H-2017 1H-2016 1H-2017 1H-2016

Total Feed Volume (k tonnes) 2,222 2,051 1,027 977 1,475 1,535 - - 4,725 4,562

Revenue 560.0 501.6 267.8 261.4 315.7 339.1 -32.9 -31.6 1,110.6 1,070.5

Gross profit 110.2 98.4 36.1 34.5 60.8 73.4 0.2 0.2 207.3 206.5

Operating profit 34.3 28.91 4.7 4.8 5.5 8.4 -5.8 -9.3 38.7 32.8

EBITDA 38.0 33.11 6.6 6.7 11.0 14.0 -4.2 -7.9 51.5 46.0

Incidental items -0.1 -0.9 0.4 - - 1.2 - - 0.3 0.3

Underlying EBITDA 37.9 32.21 7.0 6.7 11.0 15.2 -4.2 -7.9 51.7 46.3

Currency translation effect - - - - 1.4 - - 1.4

Underlying EBITDA

37.9 32.21 7.0 6.7 12.4 15.2 -4.2 -7.9 53.1 46.3

at constant currency

EBITDA/gross profit ratio 34.4% 32.8% 19.3% 19.5% 18.2% 20.7% - - 24.9% 22.4%

Additions may lead to slight differences due to rounding

(1) Operating expenses in 2016 have been adjusted for comparative purpose, due to refinement of overhead costs allocation on cluster level

30Horizon 2020 – Activities update Focus on attractive segments • CRM system operational in all clusters, transition of sales approach initiated • Strong growth in organic (ecological) feed solutions (Reudink) Partner and deliver the Total Feed Business portfolio • Total Feed Support implementation in NL on course • Portfolio optimisation and harmonisation projects on track in all species • Strategic partnership with Chr. Hansen on silage additives successful in NL 31

Horizon 2020 – Activities update

Acquisitions

• Vleuten-Steijn (October 2016): positive contribution to swine sector in NL and G

• Small dealer (Wilde Agriculture, May 2017) in UK (with which business was already

done)

One ForFarmers: functional excellence & leverage scale

• Health & Safety: continuous focus leads to improvement of awareness

• New purchasing department (across countries by commodity categories/buyers):

project initiated ‘do more with less suppliers’

• Opening new central office Bury St Edmunds (UK) May 2017

• Steady progress supply chain optimisation plans (UK)

• Completion new plant Exeter (UK) Q4 2017, slightly later than planned

32Horizon 2020 – Deliverables update

Employee development

• Employee survey confirms high engagement and progress on identified issues; still work to do

• Management XL meeting: 250 senior staff, update & implementation Horizon 2020

• Poultry Academy started

• ‘Farming for non-farmers’ employee training initiated

• Approximately 25% of total staff shareholder ForFarmers

Total nutrition solutions

• Total Feed approach helps dairy farmers in NL deal with phosphate challenges

• Vleuten-Steijn swine feed approach integral part of ForFarmers portfolio

• Feed2Milk also introduced in UK, first findings by customers very positive

Results 1H 2017

• Underlying EBITDA at constant currencies: +14.8% to €53.1m

• Underlying EBITDA/gross profit: 24.9% (1H16: 22.4%)

• Earnings per share: +22.0% to €0.288

33Outlook 2017

• Geopolitical developments: in 2H 2017 also of influence on ForFarmers’ markets

• Volatility in raw material prices and on currency markets difficult to predict

• Devaluation Pound sterling affects consolidated results

• Demand for dairy products: continued steady growth

• Swine prices have started limited decline from historically high levels:

- increase international competition for European export market

- growth Chinese swine production

• Increasing demand for poultry

• 2H 2017 expected to show lower percentage growth underlying EBITDA than solid increase in 1H 2017:

- Vleuten-Steijn: contribution of one quarter instead of two (acquisition date October 2016)

- 2H 2017 impact phosphate measures (per 1-03-2017) in NL likely larger than in 1H 2017, but on annual

basis likely lower than earlier pronounced 5% negative impact on NL dairy volumes

- Uncertainty UK farmers over Brexit, size of cattle and swine herds not yet recovered;

our recovery in UK taking longer than planned

- Fipronil case poultry (NL): volume in NL and B expected to be impacted; at this moment expectation is

marginal volume impact on group level

• Reconfirmation guidance: for the medium term an on average annual underlying EBITDA growth in the mid

single digits at constant currencies, barring unforeseen circumstances

• Confirmation full use of authorised amount (€60 million) share buy-back programme

34Summary

Improvement result on Healthy like-for-like gross Underlying EBITDA (at constant

contribution from all pillars profit growth (2.8%) currencies): +14.8%

Horizon 2020 strategy Growth in NL and G/BE larger Profit: 21.6%

than decrease in UK EPS: 22.0%

Steady progress supply chain For 2H 2017 less strong % Reconfirmation guidance: on

optimisation plans in UK increase underlying EBITDA average annual underlying

than in 1H 2017 expected EBITDA growth in mid single

due to a.o challenging digits at constant currencies

situation UK

35Contact Caroline Vogelzang Director Investor Relations & Communications Mobile: +31 6 10 949 161 Landline: +31 573 288 194 Caroline.Vogelzang@forfarmers.eu ForFarmers N.V. Kwinkweerd 12 7241CW Lochem The Netherlands 36

37

You can also read