U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA - November 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SOUTHERN AFRICA

SOUTHERN AFRICA

U.S. END MARKET ANALYSIS FOR

FOOTWEAR FROM EAST AFRICA

November 2020

1

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

2

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

TABLE OF CONTENTS

1. Executive Summary ................................................................................................................................ 5

II. Introduction and Scope of Report ................................................................................................ 6

III.Product Summary ................................................................................................................................... 6

IV.East Africa Footwear Exports ..................................................................................... 7

A. East Africa Footwear Exports to the World ..................................................................................... 7

B. East Africa Footwear Exports to the U.S............................................................................................... 9

V. U.S. Market Summary ........................................................................................................................... 13

A. General Market Characteristics............................................................................................................... 13

B. Market Size and growth.............................................................................................................................. 14

C. U.S. Footwear Market Segment............................................................................................................... 15

D. U.S. Footwear Market Trends................................................................................................................... 19

E. Principal Footwear Buyers in The U.S...................................................................................................... 21

F. U.S. Footwear Prices.................................................................................................................................... 21

V. Non-Tariff Requirements .................................................................................................................. 22

A. AGOA Rules of Origin.............................................................................................................................. 22

B. U.S. Footwear Import Tariffs for MFN, AGOA, and GSP ...................................................................... 22 3

C. Import Regulations...................................................................................................................................... 23

D. Standards and Certifications..................................................................................................................... 24

E. Packaging and Labeling ................................................................................................................................ 24

VII. U.S. Distribution ................................................................................................................................... 24

A. Supplier Selection ........................................................................................................................................ 24

B. Distribution Channels ................................................................................................................................ 24

C. Retail Channels ............................................................................................................................................ 25

VIII. Sales Promotion .................................................................................................................................. 27

A. Key Trade Fairs, (2019 Editions)............................................................................................................... 27

B. Key Industry Associations .......................................................................................................................... 27

IX. Competition ............................................................................................................................................ 28

A. Key Competitors.......................................................................................................................................... 28

B. Critical Success Factors .............................................................................................................................. 29

C. Prospects.................................................................................................................................................... 30

X. Bibliography ................................................................................................................................................ 30

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

ACRONYMS

AAFA American Apparel and Footwear Association

AAMA American Apparel Manufacturers Association

AGOA African Growth and Opportunity Act

CAGR Compound Annual Growth Rate

CPSC Consumer Product Safety Commission

DoD Department of Defense

FDRA Footwear Distributors and Retailers of America

FFANY Fashion Footwear Association of New York

FIA Footwear Industries of America

4 FOB Free on Board

GDP Gross Domestic Product

GSP Generalized System of Preferences

ITC International Trade Center

MFN Most Favored Nation

RoO Rules of Origin

SSA Sub-Saharan Africa

TPP Trans-Pacific Partnership

U.S. United States

USAID United States Agency for International Development

USFIA United States Fashion Industry Association

USFMA United States Footwear Manufacturers Association

USITC United States International Trade Commission

WRAP Worldwide Responsible Accredited Production

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

I. EXECUTIVE SUMMARY

W

hile the African Growth and Opportunity Act This report identifies four key market trends. First, continued strong

(AGOA), passed in 2000 and extended in 2015 growth is expected in the athletic/athleisure segment. Second, there

until 2025, provides duty-free access to the U.S. will be a more pronounced orientation toward eco-friendly products.

market for African footwear products, East African Customers are prepared to pay a premium for footwear made of

countries have for the most part struggled to take advantage of it. recycled material or which are made using more sustainable production

Although Ethiopia exported, on average, a little over $25 million in methods. Third, mass customization will offer the benefits of mass

footwear products per year to the U.S. from FY 2016-20, the rest production while allowing customers to customize certain aspects of

of East Africa generated, in the aggregate, an average of just $0.332 their footwear purchases. Finally, “experientialisation” will see the rise 5

million annually over that period. East Africa’s performance under of more brand-specific stores offering customized customer in-store

AGOA is compounded by a slowing U.S. end market. Although experiences while providing brands with more rapid feedback on their

the U.S. remains the largest footwear market in the world by a products.

wide margin, the industry has stagnated; projected to result in slow

While East African manufacturers will need to be cognizant of a variety

growth for the next five years.

of import-related regulations and standards, from packaging and

The market is segmented into four categories. The first is sneakers labeling to consumer safety measures, probably the most prominent

(also known as “athleisure” footwear) that features a sporty look of these is WRAP (Worldwide Responsible Accredited Production)

and values form over function. The second, athletic footwear, is certification, which ensures that manufacturers are employing safe,

designed for use in sports activities. Leather footwear is more lawful, humane, and ethical manufacturing practices. With respect to

closely associated with high-end fashion; while the “textiles distribution and retailing, although e-commerce has played a strong

and other footwear” category includes town role in the fashion industry, most footwear is

footwear, rubber boots, flip flops, and clogs. still sold through brick-and-mortar stores due to

customer preferences to try footwear on prior to

Textiles and other footwear is the largest “Textiles and other purchase.

segment, projected to account for 34.7% of the

market in 2025. However, with a compound footwear is the largest The U.S. footwear industry is nearly exclusively

annual growth rate (CAGR) of 4.2% from segment, projected to imports, which account for upward of 95% of all

2012-2025, it lags both sneakers and athletic consumption. Most of this comes from Asia; with

footwear. These are the least expensive shoes account for 34.7% of China recently losing share to Vietnam and, to a

on the market. Sneakers, the second largest the market in 2025.” lesser extent, Indonesia. China now accounts for

market segment, projected to account for about half of U.S. imports, while Vietnam generates

27.5% of the market in 2025, is also the fastest- about a quarter. Together they dominate the low-

growing; with a 7.9% CAGR. Athletic footwear, cost segment of the market. Imports are likely to

although projected in 2025 to remain the smallest market segment remain dominant due to the lower cost of imported product in a price-

at 18.3%, is growing quickly at 5.2% per annum. Athletic footwear sensitive industry, despite a trend toward “re-shoring” production in

has the highest price point on the market. In contrast with the order to streamline supply chains. While U.S. firms have shown broad

other categories, leather footwear has rapidly lost market share interest in geographic diversification (especially away from China), East

since 2012, when it accounted for nearly 42% of the market by African exporters will need to compensate for their higher wages and

revenue. By 2025 is projected to shrink to half that, at just 21.3%. slower speed to market through lower sourcing costs and stronger

In fact, over the 2012-2025 period, leather footwear is projected to compliance. East Africa exporters can also target high MFN tariff

contract, with a CAGR of -2.5% over that time. product groups such as protective footwear where AGOA’s duty free

tariffs will give them a cost advantage in the U.S. market.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

1I. INTRODUCTION AND aims to be the focal point in East Africa for businesses

and national governments seeking to take advantage

SCOPE OF REPORT of AGOA and those wanting to engage in two-way

trade between the U.S. and the 5 East African states

USAID Southern Africa Trade and Investment through import of goods from the U.S. including

Hub (USAID TradeHub technology and equipment. To achieve the activity

The United States Agency for International objectives, the buy-in will provide capacity building

Development (USAID) Southern Africa Trade and assistance to the private sector and state institutions

investment Hub (USAID TradeHub) is a five-year to help them understand the U.S. while creating

trade and investment program for Southern Africa. awareness of business opportunities in both the

The USAID TradeHub is expected to increase global U.S. and East Africa. The USAID TradeHub will also

competitiveness and intraregional trade and improve link enterprises and trade associations in the U.S.

food security in Southern Africa. The Hub engages with those in East Africa to promote collaboration

with partners across the region to increase sustainable and business exchange, and in addition, provide

economic growth, global export competitiveness, technical assistance for trade policy review focusing

and trade in targeted Southern African countries. on removing barriers to trade within East Africa.

It supports these objectives by increasing exports

from Southern African countries to South Africa In collaboration with national institutions, the USAID

and the United States (under the African Growth TradeHub’s East Africa buy-in activity develops and

and Opportunity Act [AGOA]), boosting capital undertakes trade-enhancing activities involving

and technology flows from South Africa to other private enterprises in sectors informed by the

Southern African countries, and providing targeted national AGOA utilization strategies formulated with

6 trade facilitation support to Zambia. The USAID the support of previous USAID Trade and Investment

TradeHub works with market actors to identify and Hub projects including undertaking U.S. end-market

resolve enterprise constraints and to implement studies for target product and building capacity of East

sustainable solutions through market-based trade and African enterprises to engage with U.S. businesses.

investment facilitation services. The USAID TradeHub This report is one such end market study, with a

partners with USAID bilateral missions through the focus on footwear.

USAID/Southern Africa Regional Economic Growth

Office in the successful delivery of its objectives. Scope of the End Market Study

The current study addresses mainly footwear

USAID TradeHub East Africa Trade Promotion products available in East Africa which have potential

and AGOA Buy-in activity for export to the United States. The report is intended

The USAID TradeHub also has an activity in East Africa to provide footwear producers in the East African

through a Buy-in arrangement, to promote economic countries of Ethiopia, Kenya, Rwanda, Tanzania, and

activity between the United States and 5 East African Uganda with some actionable intelligence on the

countries - Ethiopia, Kenya, Rwanda, Tanzania and U.S. market in a highly accessible format along with

Uganda. This 18-month activity seeks to boost two- references and resources for further research.

way trade and investment between the U.S. and East

Africa, under the U.S. Government’s Prosper Africa

Initiative, with a focus of expanding exports to the

III. PRODUCT SUMMARY

Footwear is designated HS code 64. Subheadings

U.S. under the Africa Growth and Opportunity Act

include:

(AGOA), and increasing investment and exports of

technology from the U.S. to East African firms. The

6401: Waterproof footwear with outer soles and

activity also seeks to facilitate reduction of barriers

uppers of rubber or plastics, the uppers of which are

to trade within East Africa.

neither fixed to the sole nor assembled by stitching,

riveting, nailing, screwing, plugging or similar processes

The USAID TradeHub’s East Africa Buy-in activity

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

6402: Other footwear with outer soles and uppers of IV. EAST AFRICA FOOTWEAR

rubber or plastics

EXPORTS

6403: Footwear with outer soles of rubber, plastics,

leather or composition leather and uppers of leather A. East Africa Footwear Exports to the World

Table 1 below uses ITC TradeMap data to show all

6404: Footwear with outer soles of rubber, plastics, footwear exports from East African countries from

leather or composition leather and uppers of textile 2015-2019 (the most recent year for which data was

materials. available for world exports for all countries).

Table 1: East Africa-World Footwear Exports by Country, 2015-2019 (‘000 U.S.D)

2015 2016 2017 2018 2019 Average, 2015-2019

Ethiopia $33,412 $37,118 $45,485 $26,549 $37,163 $35,945

Kenya $38,400 $34,657 $31,783 $34,569 $38,154 $35,513

Rwanda $1,677 $3,790 $3,175 $3,458 $86 $2,437

Tanzania $12,642 $127 $288 $590 $1,211 $2,972

Uganda $3,406 $3,139 $2,809 $4,047 $671 $2,814

Source: ITC TradeMap. Presentation by Report Author

7

Footwear exports from East Africa to the world have been dominated by Ethiopia and Kenya; with the

concentration increasing from an average of 89.7% from 2015-2019 to 97.5% in 2019 (see Figures 1 and 2).

Figure 1: Share of Footwear Exports from East Africa to the World, 2015-2019

3.7% 3.5%

3.1% 45.1%

44.6%

Ethiopia Kenya Rwanda Tanzania Uganda

Source: ITC TradeMap. Presentation by Report Author.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

Figure 2: Share of Footwear Exports from East Africa to World, 2019

1.6%

0.1%

0.9%

49.4% 48.1%

Ethiopia Kenya Rwanda Tanzania Uganda

Source: ITC TradeMap. Presentation by Report Author.

Despite the fact that Ethiopia and Kenya have exports went to the U.S. When Canada is accounted

8

accounted for similar export revenues over the past for, 84.5% of Ethiopia’s exports were bound for the

five years, however, their respective export portfolios North American market. Meanwhile, over 90% of

look dramaticallyEthiopia's

different. InFootwear

2018, for example (the Kenya’s footwear exports were made to regional

most recent year for which country-specific

Export Portfolio, 2018 export countries.

data was available), nearly three quarters of Ethiopia’s

Figure 3: Ethiopia’s Footwear Export Portfolio, 2018

5.6%

2.5%

2.7%

4.8%

10.9%

73.6%

U.S Canada Kenya China Hong Kong Other

Source: ITC TradeMap. Presentation by Report Author.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

Figure 4: Kenya’s Footwear Export Portfolio, 2018

s Footwear

tfolio, 2018

4.0%

8.1%

12.7% 29.8%

16.0%

29.5%

Uganda Rwanda DRC Tanzania S.Sudan Other

Source: ITC TradeMap. Presentation by Report Author.

B. East Africa Footwear Exports to the U.S.

9

Table 2 below uses USITC data to show footwear exports from East African countries to the U.S. for U.S. fiscal

years 2016 to 2020 (October to September).

Table 2: East Africa Footwear Exports to U.S. by Country, US Fiscal Year 2016-2020 (‘000 U.S.D)

5 Year

Country FY2016 FY2017 FY2018 FY2019 FY2020 Average

Ethiopia 21,844 27,147 33,783 28,367 15,713 25,371

Kenya 250 104 111 179 471 223

Rwanda - - - 2 - 0

Tanzania 6 3 1 1 1 2

Uganda 134 141 106 84 70 107

TOTAL 22,234 27,395 34,002 28,632 16,255 25,704

Source: USITC, Abstracted by USAID TradeHub.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAID

SOUTHERN AFRICA

10

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

11

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDShare of East Africa footwear SOUTHERN AFRICA

exports to U.S. average

(FY 2016-2020)

Footwear exports from East Africa to the U.S. from Fiscal Year 2016-2020 were dominated by Ethiopia (see

Figure 5). As we can see from Table 2, however, Ethiopia’s exports reached a peak of 33.78 million in FY 2018

and have been in decline ever since.

Figure 5: Share of Footwear Exports from East Africa to the U.S., FY 2016-2020

0%

0% 1%

0%

99%

12

Ethiopia Kenya Rwanda Tanzania Uganda

In FY2016-2020 Ethiopia was almost the only East African exporter of footwear to the U.S. (see Figure 6).

Besides Ethiopia, only Kenya, with a small share at 1 %, registered any exports to the U.S.

Figure 6: Value of Footwear Exports from East Africa to the U.S., FY 2020 ($’000)

Value of East 1 70

African FY 0

2020 exports

471

to U.S.

15,713

Source: USITC,

Abstracted by

Ethiopia Kenya Rwanda Tanzania Uganda USAID TradeHub.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

V. U.S. MARKET SUMMARY

A. General Market Characteristics

Sneakers and athletic shoes have become the bright spots in an otherwise slowing industry, reflecting a

trend toward health and wellness. In addition, more relaxed dress codes contributed to growth in casual,

comfortable shoes typically employed in active lifestyles.1 Imports dominate the U.S. market (an estimated 98

percent of shoes sold in the U.S. are imported2), and most of these are imported from developing countries,

where U.S. brands can take advantage of the lower cost of production.

Domestic production relative to imports may increase in the coming years, however, for two reasons. The

first is the potential for additional tariffs on imported footwear, particularly footwear from China, which

accounts for around half of all imports. The increased U.S. emphasis on pushing U.S. exports and protecting

U.S. jobs was epitomized by its withdrawal from the Trans-Pacific Partnership (TPP), which would have

reduced tariffs on goods (including footwear) sourced from countries that were party to the Agreement

(including Vietnam and Mexico). The second is the Berry Amendment, which will require the Department

of Defense (DoD) to purchase 100% of its footwear (among other items, such as food and clothing) from

domestic sources.3 There has also been a short-term decrease in imports, possibly due (at least in part) to

the impact of Covid-19.

Due to the outsourcing of the largely commoditized production function, most brands focus primarily on

high-value activities, including design, marketing, and distribution. Some major manufacturers, including Nike

and Adidas, have recently started “re-shoring” production in an attempt to streamline their supply chains; but

many of these domestic factories have struggled to stay price-competitive with production factories located

abroad.4

13

Key demand determinants include price, disposable income, brand recognition, and seasonal factors. Overall

footwear sales are dominated by individuals from 35-54 years of age (see Figure 7), who collectively make up

44.6% of all footwear purchases.

700

601

Average annual expenditure in U.S.

600 520

500 447

400 419

400

dollars

284

300 255

200

100

0

Under 25 25 to 34 years35 to 44 years45 to 54 years55 to 64 years 65 years and All consumer

years older units

1. “Footwear in the U.S.,” Euromonitor International, March 2018.

2. “Sourcing Snapshot: Global Footwear Manufacturing and Trade,” Sourcing Journal, August 2018.

3. “Shoe Manufacturing in the U.S. Industry Report”, IBIS World, March 2020. IBIS World.

4. IBIS World.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

B. Market Size and Growth

The U.S. is the largest footwear market in the world by a significant margin (see Figure 8).

Figure 8: Revenue of the Global Footwear Market by Country (Millions of U.S.$), 2019

Source: Statista

14

Figure 9: Projected Growth, U.S. Shoe Manufacturing, 2020-2025

Industry Outlook 2020-2025 The U.S. footwear manufacturing industry has

contracted over the last five years, however,

1

falling at a CAGR of 0.8% since 2015. Projected

0 growth from 2020-2025 is anticipated to be slow,

Percentage

at an annualized rate of just 0.1% p.a. (see Figure

-1

9). The industry’s contribution to U.S. GDP over

-2 that period of time, meanwhile, is projected to

shrink, due in part to high levels of competition,

-3

especially from low-cost imports. Statista project

20 21 22 23 24 25 somewhat faster growth over the same period,

Year at 1.8%, but this is still projected to lag other

Shoe & Footwear Manaufacturing source: IBISWORLD

major markets including China (5.5%), Germany

(2.8%), and the UK (2.6%).5

C. U.S. Footwear Market Segments

There are multiple ways to segment the U.S. footwear market. In Section A we presented consumer

segmentation by age. However, consumer segmentation can also be thought of in other ways (see Figure 10).

Characteristics of each are discussed briefly.6

5. “Footwear Report”, Statista, July 2020.

6. Characteristics as described by IBIS World.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Figure 10: U.S. Footwear Market by Consumer Segment, 2020

51.8% 25.5% 19.5% 3.2%

Men’s footwear Rubber and plastic Women’s footwear Other footwear

(except athletic) footwear including (except athletic)

athletic footwear

Shoe & footwear Manufacturing Source: IBISWorld

• Men’s Footwear: Characterized by slow changes Segmentation can also be considered by use.7

in style, particularly compared with women’s shoes. The footwear market can be segmented into:

• Rubber and Plastic Footwear, including Athletic

Footwear: Vulcanized, molded or cemented soles • Athletic Footwear: Designed specifically for

and fabric athletic purposes.

15

uppers. Includes children’s, women’s and men’s • Leather Footwear: Includes town footwear,

shoes, and typically includes rubber boots, canvas boots, sandals and clogs with leather uppers for

shoes, women, men

rubber sandals and galoshes. and children.

• Women’s Footwear: Characterized by rapid style • Sneakers: Also known as “athleisure”, this

changes, with the sophisticated, high-end market category features everyday footwear designed with a

serviced sporty look

by Italian imports. but where fashion outweighs function.

• Other Footwear: Includes specialized athletic • Textiles and Other Footwear: Models not made

shoes, protective coverings, work boots, water of leather and/or cannot be assigned to athletic

shoes and footwear. Town footwear with textile, rubber or

house slippers. plastic uppers as well as rubber boots, flip flops and

wooden clogs.

7. “Footwear Report”, Statista, July 2020.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

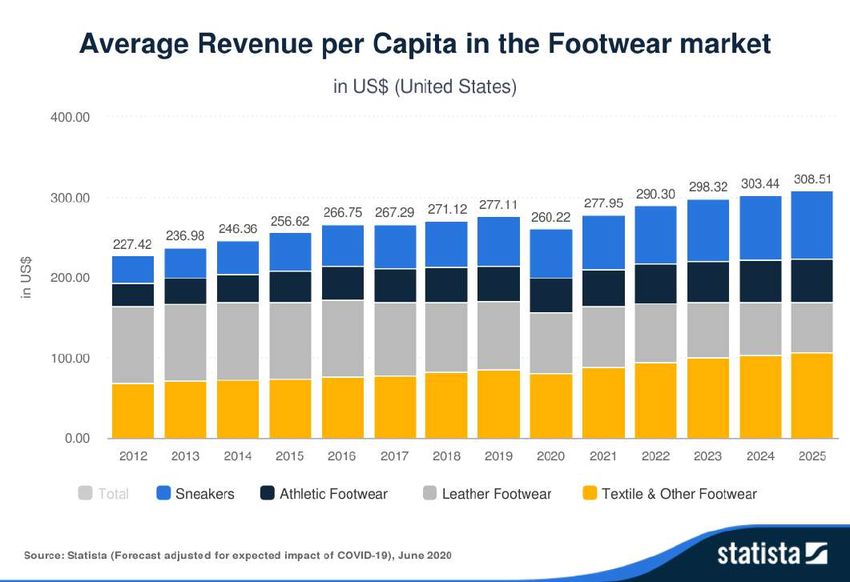

Figure 11 shows revenue per capita for each of these segments since 2012 and projected out to 2025. A

close look at the figure suggests that three of the segments represent an ever-increasing share of per capita

Figure 11:

Average Revenue per Capital in the footwear market

16

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Sneakers

Figure 12: Revenue from Sneakers Segment (Billions of U.S.$), 2012-2025

Sneakers

35

30

25

20

15

10

5

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Statista Consumer Market Outlook, 2020. Presentation by Report Author

The sneakers segment is the fastest-growing segment, with a projected CAGR of 7.9% from 2012-2025. It is

projected to be the second-largest segment by 2025, trailing only textiles and other footwear. 17

Athletic Footwear

Athletic Footwear

Figure 13: Revenue from Athletic Footwear Segment (Billions of U.S.$), 2012-2025

Athletic Footwear

20

18

16

14

12

10

8

6

4

2

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Statista Consumer Market Outlook, 2020. Presentation by Report Author.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

The athletic footwear segment is projected to grow at a CAGR of 5.2% from 2012-2025. Although

projected to be the smallest segment in 2025, it has the second-fastest growth rate and will nearly have

overtaken leather footwear by revenues by that time.

Leather Footwear

Figure 14: Revenue from Leather Footwear Segment (Billions of U.S.$), 2012-2025

Source: Statista Consumer

Leather Footwear Market Outlook, 2020.

Presentation by Report

35

Author.

30

25

20

15

10

5

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

18

The leather footwear segment is projected to grow at a CAGR of -2.5% from 2012-2025. It is the only

segment to post negative growth over this period. After its status as the largest segment in 2012, it will be

nearly overtaken by athletic footwear to be the smallest by 2025.

Textiles and Other Footwear

Figure 15: Revenue from Textiles and Other Footwear Segment (Billions of U.S.$), 2012-2025

Source: Statista Consumer

Textiles and Other Footwear Market Outlook, 2020.

Presentation by Report

40

Author.

35

30

25

20

15

10

5

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

The textiles and other footwear segment is projected to grow at a CAGR of 4.2% from 2012-2025, at which

time it is projected to be the largest segment of the market.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

D. U.S. Footwear Market Trends

There are a number of trends that will have a bearing on the development of the U.S. footwear sector in the

coming years. These include 1) continued growth in the athletic/athleisure segment; 2) a stronger orientation

toward eco-friendly products; 3) mass customization; and 4) experientialisation.

Growth in the Athletic/Athleisure Segment

According to the NPD Group, athleisure accounted for about 65 percent of new dollar value gains. Athletic

footwear sales, in turn, are being driven in large part by increases in participation in athletic activities such

as running and hiking; while the athleisure segment has been driven by an increasing trend toward casual

clothing. Trends within the athletic footwear segment include innovations in sole technology and a growing

preference for premium and customized products.8 Speed to market has also become a priority; with some

companies (such as Under Armour) employing 3-D printing technologies to produce quality footwear more

quickly.9 Athletic footwear sales, by volume, is shown in Figure 16.

Figure 16: Athletic Footwear Sales by Volume (in Millions of Pairs)

450

400 393

378

350 358

336

300 311

284

250 249

200 183

150 150

129

100 91

71

50

19

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 (e) 2019 (p) 2020 (p) 2021 (p)

Source: Statista

Mass Customization

Mass customization combines the benefits of mass production with the ability to allow the individual

consumer to customize their final product, allowing the buyer to co-create the product they purchase. This

is generally done either with an app, through a web interface, or in-store. An example of this is NikeID.10

Experientialisation

Experientialisation refers to dedicated retail outlets owned by a single brand that allows that brand more

control over the customer’s in-store experience. They typically also generate faster turnaround times as

well as more immediate customer feedback that can be incorporated into product design.11

Orientation Toward Eco-Friendly Products

Eco-friendly (or sustainable) production generally involves improved environmental practices along a

company’s manufacturing and supply chain, which may include either the final product (Nike produces

sustainable sneakers made of Flyknit material made from 50% recycled fiber)12 or more eco-friendly

production practices such as plastics recycling. Consumers are increasingly willing to pay a premium price

for a product that is perceived to be eco-friendly (see Figure 17).

8. “Top 3 Trends Impacting the Athletic Footwear Market in the U.S. Through 2020,” Technavio, August 2016.

9. “Market Analysis, Size, Share and Forecast 2018-2026,” Credence Research, October 2018.

10. “Footwear Report”, Statista, July 2020.

11. Ibid.

12. www.prnewswire.com/news-releases/sustainable-footwear-market-size-worth-11-8-billion-by-2027--cagr-5-8-grand-view-research-inc-301059115.html

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

• Textiles and Other Footwear: Models not made of leather and/or cannot be assigned to athletic

footwear. Town footwear with textile, rubber or plastic uppers as well as rubber boots, flip flops and

wooden clogs.

Figure 17: Willingness to Pay for More Eco-Friendly Apparel or Footwear Amongst U.S. Consumers,

2018

No

37%

Yes

63%

20

No Yes

Due in large part to the surge in athletic and athleisure wear, Nike holds a strong position among teens in

the U.S. market (see Figure 18).

Figure 18: Leading Footwear Brands Amongst U.S. Teens as of Fall, 2019

Source: Statista

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

E. Principal Footwear Buyers in the U.S.

Key players operating in the U.S. footwear market include Nike, Foot Locker, Skechers, Caleras, and

Wolverine World Wide, Inc. The relative size of each, by turnover, is illustrated in Figure 19 below.

Figure 19: Leading Footwear Companies in the U.S. by Turnover, 2018

Source: Statista 21

F. U.S. Footwear Prices

Footwear prices in the U.S. vary dramatically. While prices in each category have generally trended upward

since 2012 and are projected to continue doing so (see Figure 20), there are dramatic differences by cate-

gory, both in prices and in projected growth. Athletic footwear and, to a lesser extent, leather shoes enjoy

higher-end positions in the market; while sneakers are a more commoditized item. Meanwhile, while prices

are projected to climb 44.5% in textiles and other footwear and 46.3% in leather footwear between 2012

and 2025, prices for sneakers will remain relatively flat while athletic footwear is projected to increase just

12.9% over the same period.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Figure 20: Price Trends by segment of Footwear Market

V. NON-TARIFF REQUIREMENTS

22

A. AGOA Rules of Origin

The African Growth and Opportunity Act (AGOA) provides duty-free access to a wide range of products

(over 6,400, including footwear) from sub-Saharan African (SSA) nations. AGOA was originally enacted in

2000 and renewed in 2015 for an additional 10 years. Duty-free access to the U.S. market is subject to a

Rules of Origin (RoO) provision. This provision specifies that the imports to the U.S. must come directly

from an SSA nation (rather than having transited first through a third country). At least 35 percent of the

value of the product must accrue to the African nation from which it is being exported. This may include

production and/or processing. Up to 15 percent of the final value of the product may be of U.S. origin, while

inputs from other qualifying SSA countries may also contribute to meeting the 35 percent requirement.

More details on AGOA rules of origin can be found on https://agoa.info/about-agoa/rules-of-origin.html

B. U.S. Footwear Import Tariffs for MFN, AGOA, AND GSP

As noted in Part A of this section, tariffs under AGOA have been lowered to 0% for the duration of the

agreement, currently in force until 2025. Table 3. below summarizes the import tariff under Most Favored

Nation (MFN), AGOA, and the General System of Preferences (GSP) for footwear products. This is a rele-

vant consideration for East African exporters since, although AGOA can be a useful market entry mecha-

nism, tariffs after 2025 may return to their pre-AGOA levels in the event that the accord is not renewed;

making these tariffs an important strategic consideration for East African exporters as they make their

determinations about how best to enter the U.S. market.

Table 3: U.S. Import Tariffs Under MFN, AGOA, and GSP

Mechanism Import Tariff

MFN 0 to 48%; some specific rates of duty are up

to 90 U.S. cents per pair

AGOA 0%

GSP Not applicable

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Exporters from East Africa should examine categories which have high Most Favored Nation (MFN) import

tariffs, such as protective shoes, and examine how they can utilize AGOA duty-free benefits to be more

price competitive in the U.S. market, although there are several other competing tariff preference programs.

Exporters can look up the tariff rates on the USITC site https://hts.usitc.gov/

C. Import Regulations

All imports must comply with Consumer Product Safety Commission (CPSC) regulations through laws such

as the Consumer Product Safety Improvement Act of 2008 and the Federal Hazardous Substances Act.

Manufacturers may not infringe U.S. patent and trademark laws on intellectual property protection, US labor

laws, and health and safety legislation. This is described at greater length in the discussion on WRAP certifi-

cation in section (b) below.

Companies within this industry are subject to environmental and anti-dumping laws related to the discharge

of material waste of footwear inputs such as synthetic and leather made footwear.

Customs duties must be paid on imported materials. All importers must submit detailed manifests to US

customs 24 hours prior to the cargo leaving the country of origin.13

All footwear imported into the U.S. requires the following documents for clearance:

• Commercial Invoice

• Bill of Lading (Ocean Bill of Lading, Waybill, Cargo of Lading (Ocean Bill of Lading, Waybill, Cargo Receipt,

or Airwaybill)

• Packing List

In addition, standard commercial invoice requirements include the following: 23

• Must be written in English

• Invoice Date

• Name of Purchaser

• Name and address of Seller

• Name and address of actual factory. If the invoicing party is the factory, this must be clearly stated on the

invoice, for example “Factory is the invoicing party”

• Country of Origin

• Name of Buying Agent or Selling Agent

• Purchase Order Number(s), Department Number(s), Letter of Credit number (if applicable)

• Style Number from Purchase Order.

• Description of the style as detailed below under Additional Invoice Requirements

• Unit of Measure (number, pairs, dozens, etc.)

• Quantity shipped

• Net and Gross weight of the shipment

• Shipping Marks and carton count (per Corporate Logistics Routing Guide)

• Purchase price in the currency of the purchase with currency type specified. This must be shown either as

the FOB/Ex-Factory price OR a breakdown by cut-make-trim and fabric

• INCO Terms of Sale (FOB, CFR, etc.)

• All discounts, and reasons for the discounts

• All charges (packing, declaration fees, etc.)

• United States Port of Entry to which merchandise is destined

13.Source: IBIS World.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Additional invoice requirements for footwear include:

• Style name/description

• Gender of wearer/Size breakdown on Invoice

D. Standards and Certifications

Buyers of imported footwear in the U.S. generally prefer that the producing factory has some social com-

pliance certification. The most commonly used standard for sewn products is the Worldwide Responsible

Accredited Production (WRAP) Certification, which provides for safe, lawful, humane, and ethical manu-

facturing. This includes several steps, including an application (made at a cost of $1,195), a pre-audit self-as-

sessment, monitoring against WRAP’s twelve principles, evaluation, and certification. Qualifying production

facilities will then be awarded WRAP certification at either the Platinum level (Platinum facilities have passed

every audit with no corrective actions or observations and maintained continuous certification with no

gaps between certification periods), Gold level (no issues and valid for12 months) or Silver (6 months, with

minor issues that need be addressed). More detailed information about WRAP can be found at http://www.

wrapcompliance.org/certification.

E. Packaging and Labeling

According to the U.S. Customs Service, footwear must be:

1. Marked in legible English;

2. Marked permanently and indelibly such as the nature of the article will permit; and

3. If the words United States, America, USA, or any city or state of the United States appears on the foot-

wear or shoe box, but is not the country of origin, the actual country of origin must appear in close prox-

24 imity to the locality name in lettering of comparable size preceded by the “Made in,” “Product of,” or similar

wording.

A textile label sewn on an inner seam or indelible ink stamp are accepted forms of marking. Both shoes in a

pair must be marked. If a textile label is used, it cannot be folded over so that the country of origin cannot

be seen easily.

All footwear must be listed in U.S. sizes. In addition to the number of pairs shipped in each size catego-

ry (listed above), the first cost of each size category must also be included. The percentage breakdown of

external surface area of the upper and outer sole and the type of leather used on upper are also required. If

the leather is “Patent Leather,” provide the thickness of synthetic lacquer (plastic) of coating or lamination. If

waterproof, provide documentation, and if sports footwear, provide sport for which it is designed.

VII. U.S. DISTRIBUTION

A. Supplier Selection

According to a recent survey of the fashion industry , supplier selection is generally based on three consid-

erations; 1) speed to market; 2) sourcing cost; and 3) risk of compliance. The same survey suggested that

sourcing costs are driven principally by labor costs. However, cost of raw materials and shipping costs fin-

ished second and third in the same survey; pointing to the importance of logistics costs in U.S. firm sourcing

decisions. In addition, 87.5 percent of firms suggested that ethical sourcing considerations are more import-

ant than they were five years ago; and that they focus on three primary considerations, including 1) treat-

ment of workers, 2) fire safety, and 3) building safety. These three items are covered in the assessment for

social compliance certification such as for WRAP.

14. “2017 Fashion Industry Fashion Industry Benchmarking Study,” U.S. Fashion Industry Association, July 2017.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

B. Distribution Channels

42.2% of all shoes are sold directly through retail outlets. Companies such as New Balance are vertically inte-

grated and sell through their own stores. Wholesalers, which sell to retailers, are the next-largest channel ac-

counting for about half (20.6%) the sales that retailers do. Interestingly, however, women’s footwear is dispro-

portionately sold through wholesale channels. Although women’s footwear represents only about one fifth of

the total market (see Figure 10, earlier) it represents over three-fifths of the wholesale market (see Figure 21).

Figure 21: U.S. Wholesale Market Segmentation by Revenues, 2020

25

C. Retail Channels

Retail stores continue to be the dominant channel to reach consumers, due to their ability to offer a su-

perior buying experience to the customer.15 Because consumers prioritize fit, size and quality when they

make footwear purchases, their overwhelming preference is to try on products before buying. As a result,

store-based retailing, which includes both apparel and footwear specialist retailers and sports goods stores,

continues to show strong growth (see Figure 22).

Figure 22: Shoe Store Sales in the U.S., 1992-2018

15. Allied Market Research, 2015.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

make footwear purchases, their overwhelming preference is to try on products before buying.16 As a result,

store-based retailing, which includes both apparel and footwear specialist retailers and sports goods stores,

continues to show strong growth (see Figure 22).

Figure 22: Shoe Store Sales in the U.S., 1992-2018

Figure 23: Share of U.S. Consumers Shopping at Shoe Retailers as of 2019

26

While most retail sales continue to be made through brick-and-mortar stores, small online retail outlets are

growing, which has enabled small online stores to provide footwear at a range of price points. Furthermore,

some of the larger (brand) retailers are starting to move more aggressively into the e-commerce space,

where growth in the U.S. has dominated online sales. For example, 41% of all sales at Nike.com were

generated in the U.S. in 2019.17

16. Euromonitor, 2018.

17. ecommerceDB.com, 2020

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

VIII. SALES PROMOTION

A. KEY FOOTWEAR TRADE FAIRS

Key Footwear Trade Fairs, (2019 editions)

DATE TRADE FAIR DESCRIPTION LOCATION REMARK

February 4-7, 2019 Footwear Fast fashion Mandalay Bay Biannual event (February

Sourcing at footwear for men, Convention Centers, and August)

MAGIC * women, juniors and Las Vegas, Nevada,

children USA

February 5-7, 2019 FN Platform Fair for luxury to North Hall, Las

lifestyle branded Vegas Convention

footwear for men, Center, Las Vegas,

women, juniors and Nevada, USA

children

March 11-13, 2019 Transit: LA Exhibition for CMC Penthouse, Transit Footwear

Market Week fashion footwear 13th floor, B-Wing, Exhibition in Los Angeles

June 17-19, 2019 Los Angeles, takes place five times a

October 14-16, 2019 California, USA year

February 5-7, 2019 Fashion Footwear International shoe Warwick New York

Association of fair Hotel, New York,

June 4-6, 2019 New York New York, USA

August 6-8, 2019 (FFANY)

December 3-5, 2019

February 25-27, Coterie Links women’s Jacob Javits Centre, Another exhibition usually

2019 apparel, accessories New York, New held in August,

and footwear York, USA 27

designers with

retailers

February 27-28, The Materials Trade show for Portland, Oregon

2019 Show shoes and and Wilmington,

sportswear Massachusetts, USA

August 6-7, 2019

August 14-15, 2019

* Note that due to COVID-19 most of these trade shows have been cancelled or postponed. Footwear Sourcing

at MAGIC was delivered as an online trade event between September and December 2020.

B. Key Industry Associations

American Apparel and Footwear Association (AAFA)

AAFA was formed in August 2000 through the merger of the American Apparel Manufacturers Association

(AAMA) and Footwear Industries of America (FIA). AAFA advocates for the interest of the apparel and

footwear sector in the U.S., representing more than 1,000 world famous name brands, retailers and

manufacturers and is the public and political voice of the apparel and footwear industry from throughout the

United States and around the globe. AAFA works to ensure continued success and growth of the apparel

and footwear industry, its suppliers, and its customers. AAFA represents hundreds of clothing, footwear, and

sewn products companies and their suppliers and provides exclusive expertise in trade, brand protection,

and supply chain & manufacturing to help members navigate the complex regulatory environment and

lower costs. The Association provides members with several benefits including access to information and

exclusive insights on regulation and policy, and opportunities for networking and collaboration.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Footwear Distributors and Retailers of America (FDRA)

Founded in 1944, FDRA serves the full footwear supply chain and boosts the bottom lines of its members

through innovative products, training and consulting on footwear design and development, sourcing and

compliance, trade and customs, advocacy, and consumer and sales trend analysis for retailers selling shoes

around the world. Members include the majority of U.S. footwear manufacturers, brands, retailers and

importers. In all, FDRA supports nearly 500 companies and brands worldwide, representing 90% of total U.S.

footwear sales. In 2020, FDRA took over management of the Fashion Footwear Association of New York

(FFANY).

United States Fashion Industry Association (USFIA)

The United States Fashion Industry Association (USFIA) represents brands, retailers, importers, and

wholesalers based in the United States and doing business globally. Founded in 1989, USFIA works to

eliminate tariff and non-tariff barriers that impede the fashion industry’s ability to trade freely and create

jobs in the United States. Headquartered in Washington, D.C., USFIA is the voice of the fashion industry in

front of the U.S. government as well as international governments and stakeholders. With constant, two-

way communication, USFIA seeks to stay ahead of current and future regulatory challenges. Through its

publications, educational events, and networking opportunities, USFIA also connects with key stakeholders

across the value chain including U.S. and international service providers, suppliers, and industry groups.

United States Footwear Manufacturers Association (USFMA)

United States Footwear Manufacturers Association (USFMA) is a nonprofit 501(c)(6) association founded

28 in 1986 to protect and enhance the footwear industry’s manufacturing base in the United States. USFMA

members include both domestic footwear manufacturers as well as domestic suppliers. As a whole, the

domestic footwear manufacturing industry employs more than 12,000 workers.

IX. Competition

A. Key Competitors

Competitors to East African footwear are numerous including the U.S. footwear manufacturing industry

which employs 12,000 workers. China remains the dominant producer of imported footwear in the U.S.,

accounting for nearly half of all U.S. imports. However, it has been losing market share to Vietnam (up from

16.1% in 2015 to 25.8% in 2020. This is probably due in part to natural diversification away from China, but

has probably also been spurred by increased tariffs (and/or the threat of increased tariffs) on Chinese-origin

products. Indonesia, meanwhile, has also picked up market share (from 5.3% to 6.2% over the same period),

although Vietnam remains the primary beneficiary due to its low labor and materials costs. Italy retains

a small share but on the basis of a very distinct market position; relying on its reputation for high quality

and strong brand recognition rather than low costs. Figure 24 shows the leading source countries for U.S.

footwear.

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

Figure 24: U.S. Import Value of Footwear 2019, by Country of Origin

B. Critical Success Factors

As noted earlier in the report, sourcing decisions are made largely on the basis of three factors; speed to

market, sourcing cost, and risk of compliance. The following table was compiled by the U.S. Fashion Industry

Association in its 2017 report. It presents a rough idea of how the Sub-Saharan Africa region-AGOA

(SSA-AGOA) is viewed relative to other common sourcing alternatives. Five asterisks indicate performance

that is far above average; three asterisks average performance; and one asterisk performance well below

average.

29

SOURCING BASE SPEED TO MARKET SOURCING COST RISK OF COMPLIANCE

USA ***** ** ****

Mexico **** *** ***

CAFTA-DR **** *** ***

China *** **** ***

Vietnam *** **** ***

Cambodia ** **** **

Indonesia ** **** ***

Sri Lanka ** **** ***

India ** **** **

SSA - AGOA ** **** ***

Bangladesh ** ***** *

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

C. Prospects categories offering maximum duty differential

against MFN imports and focus on those.

The East Africa footwear sector will continue Finally, niche footwear products using styles and

to face substantial competition from Asian materials unique to East Africa, with superior

producers, although U.S. domestic production workmanship, and timely delivery will enable

is unlikely to represent an imminent threat due East Africa to expand its exports in spite of

to its higher costs. The current trade tensions strong competition.

with China is probably helpful to East Asian

producers, as U.S. footwear firms are more likely

to diversify their production locations. The U.S. X. Bibliography

withdrawal from the Trans Pacific Partnership

(TPP) may benefit East African exporters, as “Footwear Market in the U.S.”, Statista, June

Vietnam was a signatory, and would have 2020.

presented even greater price competition to

30 East African exporters. “Footwear in the U.S.,” Euromonitor

International, March 2018.

As we can see from Table 5. above, the region

as a whole features competitive sourcing costs “Footwear Report”, Statista, July 2020.

and average compliance risk, but below average

speed to market. While this is partly a function “Market Analysis, Size, Share and Forecast

of the region’s distance from the U.S. market, 2018-2026,” Credence Research, October 2018.

it is also partly a function of sub-standard

logistics. Because the region’s speed to market “Shoe Manufacturing in the U.S. Industry

will always likely be lower than average due to Report”, IBIS World, March 2020.

its landlocked geography and distance from the

U.S. market, it will need to compensate through “Sourcing Snapshot: Global Footwear

lower sourcing costs and high reliability on Manufacturing and Trade,” Sourcing Journal,

compliance. Additionally, East African exporters August 2018.

will need to review and adjust their current

focus on leather footwear exports. These are “Sustainable Footwear Market Size, Share &

particularly prominent in Ethiopia, which is Trends Analysis Report By Type (Athletic, Non-

probably the regional country best-positioned athletic), By End User (Men, Women, Children),

to compete with Asian firms given its low labor By Region, And Segment Forecasts,

costs and access to local leather as raw material. 2020 – 2027”, Grandview Research, May 2020.

Other countries can seek to identify tariff

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

31

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDSOUTHERN AFRICA

For more information,

contact:-

32 USAID TradeHub

East Africa Buy-In Activity

Email: EastAfricaTrade@dai.com

SOUTHERN AFRICA

U.S. END MARKET ANALYSIS FOR FOOTWEAR FROM EAST AFRICA USAIDYou can also read