A Latent-Factor System Model for Real-Time Electricity Prices in Texas

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

applied

sciences

Article

A Latent-Factor System Model for Real-Time Electricity Prices

in Texas

Kang Hua Cao 1 , Paul Damien 2, * and Jay Zarnikau 3

1 Department of Economics, Hong Kong Baptist University, Hong Kong, China; kanghuacao@hkbu.edu.hk

2 Department of Information, Risk and Operations Management, McCombs School of Business,

University of Texas in Austin, Austin, TX 78712, USA

3 Department of Economics, University of Texas in Austin, Austin, TX 78712, USA; jayz@utexas.edu

* Correspondence: paul.damien@mccombs.utexas.edu

Abstract: A novel methodology to model electricity prices and latent causes as endogenous, multi-

variate time-series is developed and is applied to the Texas energy market. In addition to exogenous

factors like the type of renewable energy and system load, observed prices are also influenced by

some combination of latent causes. For instance, prices may be affected by power outages, erroneous

short-term weather forecasts, unanticipated transmission bottlenecks, etc. Before disappearing, these

hidden, unobserved factors are usually present for a contiguous period of time, thereby affecting

prices. Using our system-wide latent factor model, we find that: (a) latent causes have a highly

significant impact on prices in Texas; (b) the estimated latent factor series strongly and positively

correlates to system-wide prices during peak and off-peak hours; (c) the merit-order effect of wind

significantly dampens prices, regardless of region and time of day; and (d) the nuclear baseload

generation also significantly lowers prices during a 24-h period in the entire system.

Keywords: energy prices; renewable energy; system modelling; unobservable factors

Citation: Cao, K.H.; Damien, P.; JEL Classification: Q02; Q04; Q41; Q42

Zarnikau, J. A Latent-Factor System

Model for Real-Time Electricity Prices

in Texas. Appl. Sci. 2021, 11, 7039.

https://doi.org/10.3390/app11157039 1. Introduction

Information about energy prices is known in the day-ahead market, but actual real-

Academic Editor: Andreas Sumper

time prices will deviate from the day-ahead prices for many “hidden” reasons; see [1]. For

example, an error in load forecasts, wind forecasts, solar output forecasts, or the outage of

Received: 18 June 2021

a power plant or transmission line, and many other unforeseen events will cause real-time

Accepted: 27 July 2021

prices to deviate from day-ahead prices. These latent factors are difficult to measure and

Published: 30 July 2021

adjust in real-time, and yet their impact on prices can be significant. This reveals itself in

the fact that the new real-time price is set at most every five minutes.

Publisher’s Note: MDPI stays neutral

A typical approach to explaining real-time prices is to start with the ex-post day-ahead

with regard to jurisdictional claims in

price, and model deviations of the real-time price from the day-ahead price as a function

published maps and institutional affil-

iations.

of forecasting errors. While this approach may be helpful, it fails to consider the myriad

of unobserved latent factors. Also, system-wide hidden factors are difficult to forecast in

single-equation models that are used to explain real-time prices.

One of the two main aims of this paper is to present a novel methodology that uses

unobserved latent factors and exogenous variables to explain energy prices in Texas by

Copyright: © 2021 by the authors.

modeling these prices as endogenous, multivariate time-series. This system-wide approach

Licensee MDPI, Basel, Switzerland.

then leads to estimating the attendant merit-order effects of baseload generation (nuclear

This article is an open access article

energy) as well as renewable energy generation (wind and solar).

distributed under the terms and

conditions of the Creative Commons

The hourly real-time market (RTM) energy price used in our analysis originates from

Attribution (CC BY) license (https://

the 5-min real-time energy prices based on the real-time operation of the Electric Reliability

creativecommons.org/licenses/by/

Council of Texas (ERCOT). ERCOT uses a security-constrained economic dispatch model

4.0/). (SCED) to simultaneously manage energy, system power balance, and network congestion,

Appl. Sci. 2021, 11, 7039. https://doi.org/10.3390/app11157039 https://www.mdpi.com/journal/applsci

Appl. Sci. 2021, 11, 7039 2 of 15

yielding 5-min locational marginal prices (LMPs) for each electrical bus within the market.

The SCED process seeks to minimize offer-based costs, subject to power balance and

network constraints. The zonal settlement price for a load-serving entity’s real-time energy

purchase is a load-weighted average of all 5-min LMPs in a load zone, which is converted

to 15-min values or hourly values by ERCOT.

Economic merit order effects attributable to renewable energy generation have been

analyzed for many of the world’s competitive wholesale markets using linear regression

models. These include studies of the market in Spain [2], Germany [3–6], Denmark [7,8],

Italy [9], Australia [10], Ireland [11], the U.S. mid-continent or MISO [12,13], Texas [14–16],

PJM [17], the Pacific Northwest [18,19], and California [20]. Also, quantile regression ap-

proaches have been employed to study merit-order effects in Turkey [21] and Germany [22].

Methodological Contribution. We explore this topic using hourly real-time price data for

the years 2015–2018 from the ERCOT market. Divided into eight zones—North, Houston,

South, West, Austin Energy, CPS Energy, Lower Colorado River Authority, and Ray-

burn Electric Cooperative—ERCOT serves the electrical needs of the largest electricity-

consuming state in the U.S.; it accounts for about 8% of the nation’s total electricity gen-

eration, and is repeatedly cited as North America’s most successful attempt to introduce

competition in both generation and retail segments of the power industry (Distributed En-

ergy Financial Group, 2015). In the interests of brevity, we report the findings for Houston,

Austin, and West regions, since the results from the other regions are similar.

To the best of our knowledge, this study is the first attempt at developing a latent-

factor system-wide model for estimating the merit-order effects of baseload and renewable

energy generation. While we use the Texas energy market to exemplify the methodology,

the models developed here are readily applicable to other markets as well. Moreover, while

we focus on real-time prices, the methodology readily lends itself to the study of day-ahead

prices as well.

Section 2 describes the data and variables used in the study. The system-wide latent

factor model for prices is detailed in Section 3. Section 4 provides the results, followed by a

discussion and conclusion in Section 5.

2. Data and Variables

This section describes the data used in the analytic models, including the geographical

scope and sample period.

2.1. Geographical Scope

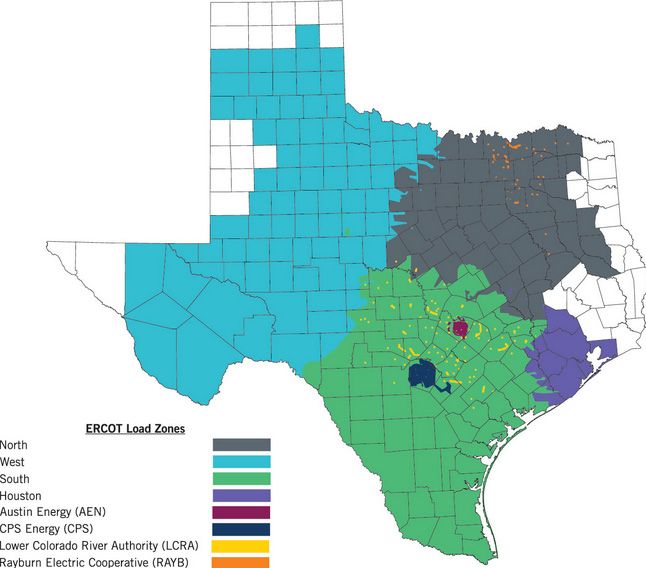

The current ERCOT market with its eight zones is the focus of the paper; see Figure 1

for a map of ERCOT. The North and Houston zones account for about 37% and 27%,

respectively, of ERCOT market energy sales, while the South and West zones contribute

12% and 9%. Further, these four zones account for nearly all of the state’s retail competition,

and most of the competitive generation resides within these zones.

Appl. Sci. 2021, 11, 7039 3 of 15

Appl. Sci. 2021, 11, 7039 and the other two correspond to peak hours. There is nothing special about the specific

3 of 15

hours we chose to work with; a similar analysis with other hours yields the same overall

conclusions reported here.

Figure 1. The eight ERCOT zones (Source: www.ercot.com, accessed on 18 July 2020).

Figure 1. The eight ERCOT zones (Source: www.ercot.com, accessed on 18 July 2020).

TablePeriod

2.2. Sample 1 provides the summary statistics for the prices ($/MWH) for the three hours

and Variables

andThe

the sample

three zones, respectively. The corresponding

period starts on 1 January 2015 and ends time-series plots of2018.

on 31 December the nine series,

Thus, we

shown

have in red,

a very appear

large insince

dataset Figureall2.the

Ineight

the analysis, however,

price series we work

will appear withasthe

together natural log

endogenous

of the price

variables data.

in the multivariate response matrix.

As noted earlier, we discuss at length the results for the following three zones: Hous-

Table

ton, 1. Summary

Austin, statistics

and the of the hourly prices

West. Additionally, ($/MWH)

we examine theformerit-order

Houston, Austin,

effectsand the West.

stemming from

three hours in a 24-h cycle: 4:00 a.m., 12:00 p.m.

Mean S.D. and, 4:00 p.m.Min

The first is off-peak

Maxand the

other two correspond to peak hours. There is nothing special about the specific hours we

Houston

chose to work with; a similar analysis with other hours yields the same overall conclusions

4:00 a.m. 16.40 5.83 −14.83 75.66

reported here.

12:00 p.m. 31.13 47.95 9.59 1110.26

Table 1 provides the summary statistics for the prices ($/MWH) for the three hours

4:00three

and the p.m.zones, respectively.

47.54 99.10

The corresponding 0.24 plots of the1348.34

time-series nine series,

Austin

shown in red, appear in Figure 2. In the analysis, however, we work with the natural log of

4:00data.

the price a.m. 16.14 6.31 −14.89 97.65

12:00 p.m. 27.00 18.18 6.72 338.09

Table 4:00 p.m. statistics42.38

1. Summary of the hourly prices85.96 0.11 Austin, and the

($/MWH) for Houston, 1348.11

West.

West

Mean S.D. Min Max

4:00 a.m. 17.79 14.82 −15.56 132.71

12:00 p.m. 27.55 Houston

23.43 −16.88 408.91

4:00 a.m. 16.40 5.83 −14.83 75.66

4:00 p.m. 43.23 88.60 −15.67 1384.76

12:00 p.m. 31.13 47.95 9.59 1110.26

4:00 p.m. 47.54 99.10 0.24 1348.34

One of the insights we hope to gain Austin

is to see how the one-hour-ahead in-sample esti-

mates ofa.m.

4:00 the latent factor time series track6.31

16.14 −14.89

the price plots in Figure 2. If we can show that

97.65

12:00

there is ap.m. 27.00between the estimated

strong correlation 18.18 6.72 series and the338.09

latent factor price series,

then4:00

thatp.m.

bodes well for42.38

the estimation of85.96

merit-order effects0.11

from alternative1348.11

energy and

West

baseload generation. On17.79

4:00 a.m.

the other hand, if14.82

there is a very weak relationship between

−15.56 132.71

latent

factors and

12:00 p.m. the price series,

27.55 then exogenous

23.43factors should suffice

−16.88 in understanding

408.91 the

fluctuations

4:00 p.m. in the price43.23

data. 88.60 −15.67 1384.76

Appl. Sci. 2021, 11, 7039 4 of 15

Appl. Sci. 2021, 11, 7039 4 of 15

-20 0 20 40 60 80

Price ($/MWH)

1000

Price ($/MWH)

5000

500 1000 1500

Price ($/MWH)

0 50 100

Price ($/MWH)

-50 0

0 100 200 300 400

Price ($/MWH)

500 1000 1500

Price ($/MWH)

0

-50 0 50 100 150

Price ($/MWH)

0 100 200 300 400

Price ($/MWH)

500 1000 1500

Price ($/MWH)

0

Figure 2. Time-series

Figure 2. Time-series plots

plots of

of the

the actual

actual prices

prices (solid

(solid red

red line)

line) and

and model

model predicted

predicted prices

prices (dash

(dash grey

grey line)

line) in

in Houston,

Houston,

Austin, and the West for the hours 4:00 a.m., 12:00 p.m. and 4:00 p.m.

Austin, and the West for the hours 4:00 a.m., 12:00 p.m. and 4:00 p.m.

A brief

One of discussion of we

the insights eachhope

of the

toindependent variables

gain is to see how thenow follows. Thesein-sample

one-hour-ahead variables

were

estimates of the latent factor time series track the price plots in Figure 2. If we cantables,

selected based on careful data exploration via summary plots/correlation show

practical

that thereconsiderations of data size,

is a strong correlation modeling

between aims, and computational

the estimated complexities.

latent factor series Ad-

and the price

Appl. Sci. 2021, 11, 7039 5 of 15

series, then that bodes well for the estimation of merit-order effects from alternative energy

and baseload generation. On the other hand, if there is a very weak relationship between

latent factors and the price series, then exogenous factors should suffice in understanding

the fluctuations in the price data.

A brief discussion of each of the independent variables now follows. These vari-

ables were selected based on careful data exploration via summary plots/correlation tables,

practical considerations of data size, modeling aims, and computational complexities. Addi-

tionally, price formation in the ERCOT market has been analyzed in a variety of antecedent

studies using many of the same data sources and variables employed in this study [14–16].

The exogenous variables used in this study are split into those that appear in the

observation and latent factor equations, respectively; these equations are detailed in the

next section.

Observation Equation Exogenous Variables. Wind generation, nuclear generation, solar

generation, the Henry Hub gas price, and a dummy variable for spikes in prices that

exceed $500 MWH are the exogenous variables. ERCOT analysts have noted that industrial

customers tend to significantly scale back when prices exceed USD 500. So, a binary

dummy variable for extreme price spikes is used. The solar generation variable and the

dummy variable do not appear in the 4:00 a.m. equations. We downloaded daily natural

gas prices for Henry Hub from the DOE/EIA (See: http://www.eia.gov/dnav/ng/hist/

rngwhhdd.htm. Last accessed 18 July 2020). We use the Henry Hub price instead of the

local natural gas price (e.g., Houston Ship Channel) since the Henry Hub price is highly

correlated with the local natural gas price (r > 0.95). Finally, the latent factor variable, which

is estimated from within the system endogenously, appears as an exogenous variable in

the observation equation. All variables are on the natural log scale except, of course, the

dummy variable.

Latent Factor Equation Exogenous Variables. Recall that the latent factors are unobserved

variables; there is no data for them. The parameters corresponding to these variables are

recursively estimated from within the system at each point in time, which leads to the

following intuition: if one could observe these latent causes, then they are most likely

going to be related to load and prices. For instance, power outages, erroneous short-

term weather forecasts, unanticipated transmission bottlenecks, etc., would most certainly

impact demand and price distributions across ERCOT. Therefore, we use system-wide

load (MWH) and lagged weighted price ($/MWH) across all eight zones as the exogenous

factors that could likely associate with the unobserved factor variables. Additionally, a

first-order autoregressive process for the latent factor is used. This allows us to capture

the potential lingering effects of hidden variables over time. As described in the next

section, while we could use higher-order lags, we do not do so in the interests of parsimony.

Also, the lagged weighted prices do capture some of the previous time period’s effect

on the latent factor. Note that the system-wide load is, in one sense, endogenous to the

observation equation via the latent factor. Finally, we work with the natural logs of all

these variables.

3. The Latent Factor Systems Model

Following [23,24], suppose there are k endogenous variables. Let n f < k denote the

number of unknown or hidden latent factors. Then, the system of equations that represent

the prices in the k = 8 zones in ERCOT with n f = 1 is given by:

yt = λft + βxt + ut ft = δzt + ρft−1 + wt , (1)

where the first equation is called the observation equation and the second is termed the

latent factor equation. The dimensions of the various quantities in Equation (1) are: yt is

a k × 1 vector of endogenous variables; λ is n f × n f ; ft is n f × n f ; β is a k × n x vector of

parameters; xt is an n x × 1 vector of exogenous variables; ut is a k × 1 vector of random

errors that are assumed to be normally distributed with mean zero and unknown standard

deviation σu ; δ is an n f × nz of parameters; zt is an nz × 1 vector of exogenous variables;

Appl. Sci. 2021, 11, 7039 6 of 15

ρ is an n f × n f matrix of parameters; and wt is an n f × 1 vector of random errors that is

normally distributed with mean zero and unknown standard deviation σw .

It is possible to introduce another Equation in (1) that represents an autoregressive

structure for the observation error ut . However, this leads to a larger number of parameters

than is dictated in most applications. Moreover, convergence issues abound when the

parameter space and the sample size are large. As it is, the class of models contained

in (1) is quite rich. By appropriately restricting n f , p and q, we can obtain Zellner’s

Seemingly Unrelated Regression model, Vector Autoregressive models; Dynamic Factors

with Errors models, etc; see, for example [25,26]. Williamson et al. [1] developed an

alternative Bayesian latent factor model, using nonparametric methods, that complements

the latent factor model in Equation (1).

We could also add higher-order latent factors (n f > 1), but again we err on the side of

parsimony. Indeed, we could also increase the dimension of the autoregressive component

of the latent factor vector ft which we have set as an AR(1) process. But we refrain from

doing this since we also include the lagged weighted price of all the zones as an exogenous

variable in the vector zt ; i.e., we allow the weighted values of lagged prices from the eight

zones to guide the hidden factors that could drive each zone’s price in the observation

equation where these prices are endogenous in the system given in (1).

Thus, yt is the endogenous matrix of prices from the eight zones; xt contains the

exogenous variables wind, nuclear and solar generation, where the last one appears only

in the sunlight hours; the Henry Hub gas price; and a dummy variable for real-time prices

exceeding USD 500, which will not appear in the night and early morning hours since prices

do not rise to very high levels at these times. The endogenous factor variable ft also appears as

an exogenous input in the observation equation. The implication is that these hidden factors

could influence prices throughout the day. In the latent factor equation, the exogenous

variables in zt use system-wide load (MWH) and lagged weighted price (USD/MWH)

across all eight zones; these are contemporaneous in time. Additionally, we assume the

latent factor follows a first-order autoregressive process. Since we separate our analysis for

each hour of the day, the lagged variables are the variables of the previous day. Since ft

enters the observation equation exogenously, the system-wide load affects system-wide

prices via ft . Lastly, the AR(1) specification for ft in the second equation captures the lagged

nature of hidden factors; for example, poor weather forecasts, which could be one of the

latent factors, tend to be contiguous over time.

The maximum likelihood estimates (MLEs) for all the parameters (including δ and ρ)

are found via an iterative method that combines the two algorithms developed in [27,28].

All analyses were conducted in STATA.

4. Results

Here, we report and discuss the results for three regions: Houston, Austin, and West;

details on all other regions are available on request. Where appropriate, we highlight the

empirics from the other regions as well. For the three regions, we report the results for

4:00 a.m., 12:00 p.m., and 4:00 p.m.; these are representative of the other off-peak and peak

hours. Thus, we estimate Equation (1) nine times since we have nine models in total. We

have the following major results.

Wald Test. This test has a chi-square distribution. It tests the null hypothesis of whether

or not all the unknown parameters in the observation and latent factor equations are jointly

significant; this is similar to the F-test in multiple linear regression. For all nine models, the

Wald Statistic soundly rejects the null hypothesis at any significance level (p < 0.00001).

Actual versus predicted price series. Consider Figure 3 which shows the actual and pre-

dicted series. As expected, there are some outliers in the data, especially during the 4:00 p.m.

hour for all three zones. Also, again consider Figure 2. Note that the predicted time series,

shown in grey, track the original price series in red quite well for the three different hours,

barring the time points corresponding to the outliers.

Appl. Sci. 2021, 11, 7039 7 of 15

Appl. Sci. 2021, 11, 7039 7 of 15

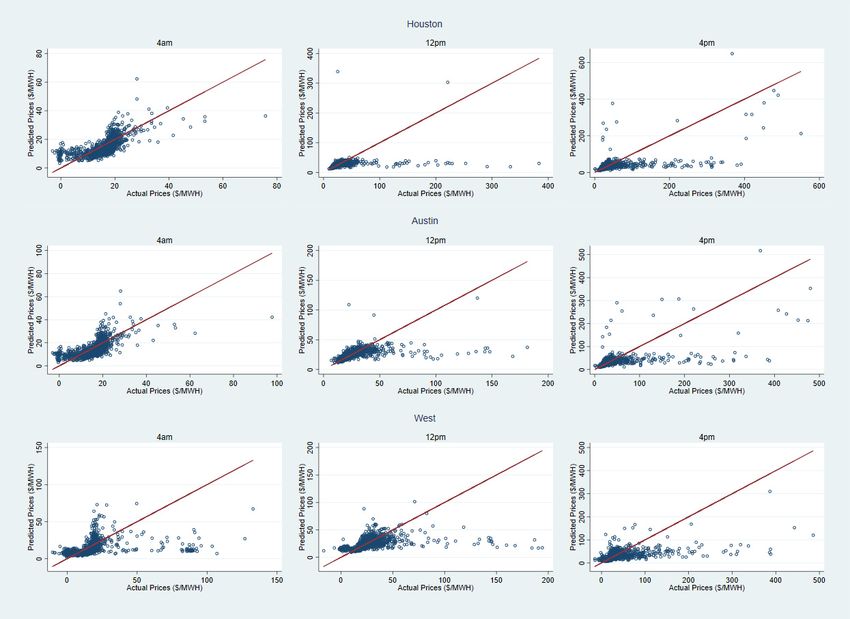

Figure 3. Scatter plots of actual and predicted prices, along with 45-degree lines, in Houston, Austin, and the West for the

Figure 3. Scatter plots of actual and predicted prices, along with 45-degree lines, in Houston, Austin, and the West for the

hours 4:00 a.m., 12:00 p.m., and 4:00 p.m.

hours 4:00 a.m., 12:00 p.m., and 4:00 p.m.

Correlations

Correlationsbetween

betweenactual

actualprice

priceseries

seriesand estimated

and estimated factor series

factor series. Table 2 shows

ft . Table 2 showsthethe

corre-

cor-

lations between each of the price series from all eight zones for the

relations between each of the price series from all eight zones for the three hours. They arethree hours. They are all

positively correlated to the predicted latent factors. We highlighted

all positively correlated to the predicted latent factors. We highlighted the correlations for the correlations for the

regions Houston,

the regions Houston, Austin, and West

Austin, in Table

and West 2 in 2order

in Table to emphasize

in order to emphasize two points. First,First,

two points. note

that the West zone has the weakest correlation during the peak

note that the West zone has the weakest correlation during the peak hours of 12:00 p.m.hours of 12:00 p.m. and 4:00

p.m., compared

and 4:00 to other regions.

p.m., compared Thisregions.

to other is because of the

This larger impact

is because of theoflarger

wind generation

impact of in windthe

West duringinthese

generation the hours, compared

West during theseto hours,

other zones.

compared Second, to consider

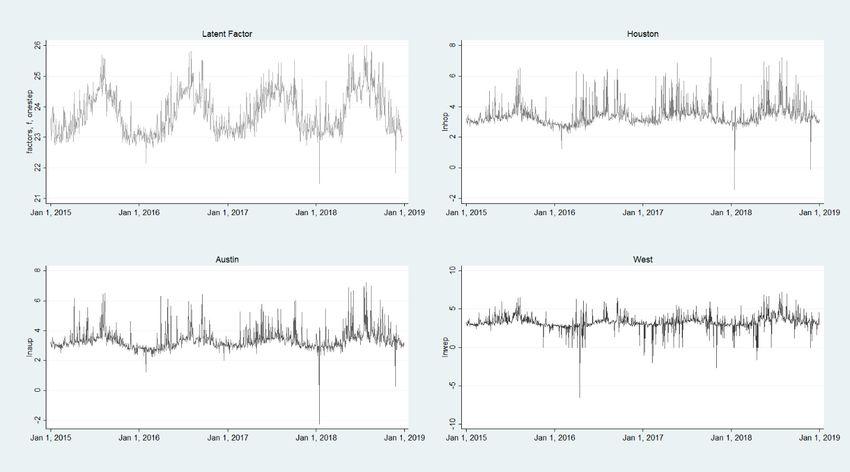

other zones.Figures 4–6. Each

Second, com-

consider

prises

Figures four

4–6.plots.

EachFor the sake of

comprises clarity,

four plots.letFor

us the

focus on of

sake justclarity,

Figurelet 6 corresponding

us focus on justtoFigure

the 4:00 6

p.m. hour. The top left plot is the latent factor one-step-ahead estimated

corresponding to the 4:00 p.m. hour. The top left plot is the latent factor one-step-ahead time series. The other

three plots time

estimated in each of theThe

series. panels

otherare the actual

three plots inprice

each series

of the forpanels

Houston,are Austin,

the actualandprice

West. The

series

corresponding

for Houston, Austin,correlations between

and West. Thethe latent factor series

corresponding and these

correlations three price

between seriesfactor

the latent from

Table

series 2and

are:these

0.587,three

0.591, andseries

price 0.457,from

respectively. It is 0.587,

Table 2 are: evident that and

0.591, the latent

0.457,factor series struc-

respectively. It is

turally

evidentevolves

that thelikelatent

the three

factorprice series,

series which are

structurally representative

evolves like the three of price

the price series

series, for are

which the

entire ERCOT system.

representative The presence

of the price series forofthe

outliers inERCOT

entire the pricesystem.

series isThe

unavoidable

presencein ofthe ERCOT

outliers in

data. Thisseries

the price wouldisexplain why some

unavoidable in theof ERCOT

the correlations

data. This arewould

not as high

explain as one

whymight

someexpect.

of the

correlations

We are not

experimented as high

with as one might

higher-order lags in expect. We experimented

the autoregressive error with higher-order

structure lags

for the latent

in the series

factor autoregressive

in Equation error

(1).structure

But suchfor anthe latentin

increase factor

model series in Equation does

dimensionality (1). But

notsuch

change an

increase

the overallin conclusions

model dimensionality does not

by much. Hence, wechange

err on the theside

overall conclusions by much. Hence,

of parsimony.

we err on the side of parsimony.Appl.

Appl. Sci.

Sci. 2021,

2021, 11,

11, 7039

7039 88 of

of 15

15

Appl. Sci. 2021, 11, 7039 8 of 15

Table 2. Correlations between the actual price series and estimated factor series for all zones.

Table 2. Correlations between the actual price series and estimated factor series for all zones.

Table 2. Correlations between the actual price series and estimated factor series for all zones.

Austin Houston LCRA North RAYB CPS South West

Austin Austin Houston

Houston LCRA LCRANorth North RAYB RAYB CPS CPS SouthSouth West

West

4:00 a.m. 0.343 0.323 0.343 0.339 0.318 0.344 0.338 0.346

4:004:00

12:00 a.m.a.m. 0.343 0.3430.3230.323 0.343

p.m. 0.532 0.473 0.5310.343 0.541

0.3390.339 0.318

0.318 0.344

0.517 0.344

0.504 0.338

0.338

0.428 0.346

0.346

0.365

12:00 p.m. 0.532 0.473 0.531 0.541 0.517 0.504 0.428 0.365

12:00 0.532

p.m. 0.591 0.473 0.531 0.541 0.517 0.504 0.428 0.365

4:004:00

p.m.p.m. 0.5910.5870.587 0.5940.594 0.6180.618 0.593

0.593 0.559

0.559 0.533

0.533 0.457

0.457

4:00 p.m. 0.591 0.587 0.594 0.618 0.593 0.559 0.533

Note: Certain values are bold in order to better understand the Figure 6 discussion. 0.457

Note: Certain values are bold in order to better understand the Figure 6 discussion.

Note: Certain values are bold in order to better understand the Figure 6 discussion.

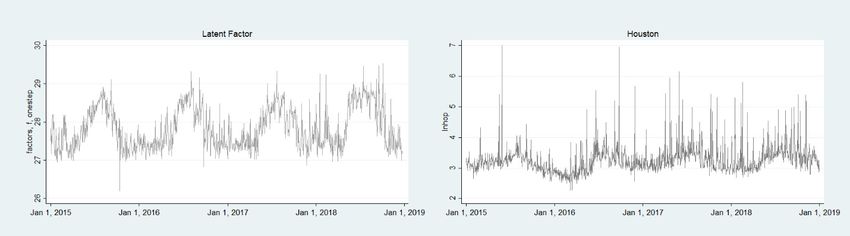

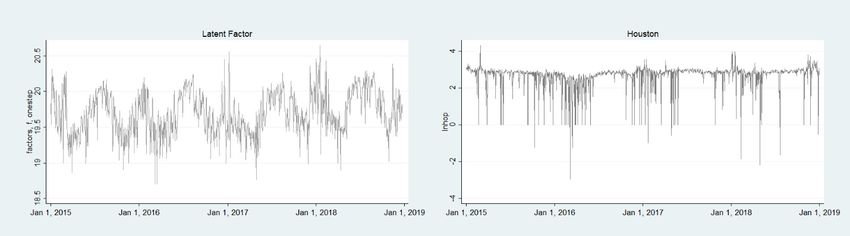

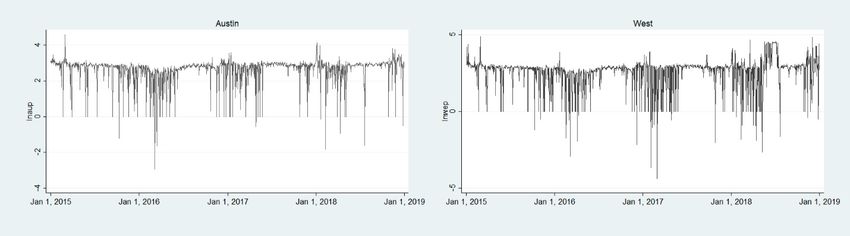

Figure 4. 4:00 a.m.—Latent Factor and Houston series (top left and right); Austin and West (Bottom left and right).

Figure 4. 4:00 a.m.—Latent Factor and Houston series (top left and right); Austin and West (Bottom left and right).

Figure 4. 4:00 a.m.—Latent Factor and Houston series (top left and right); Austin and West (Bottom left and right).

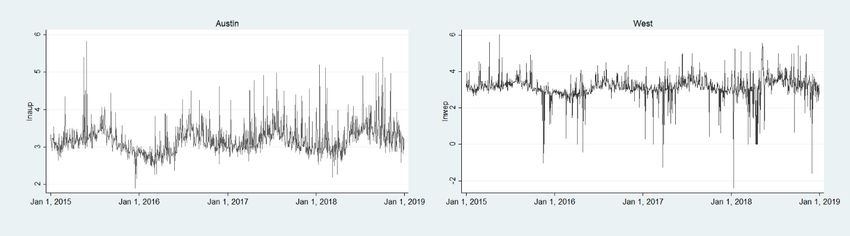

Figure 5. 12:00 p.m.—Latent Factor and Houston price series (top left and right); Austin and West (Bottom left and right).

Figure 5.

Figure 12:00 p.m.—Latent

5. 12:00 p.m.—Latent Factor

Factor and

and Houston

Houston price

price series

series (top

(top left

left and

and right);

right); Austin

Austin and

and West

West (Bottom

(Bottom left

left and

and right).

right).Appl. Sci. 2021, 11, 7039 9 of 15

Appl. Sci. 2021, 11, 7039 9 of 15

Figure 6. 4:00 p.m.—Latent Factor and Houston price series (top left and right); Austin and West (Bottom left and right).

Figure 6. 4:00 p.m.—Latent Factor and Houston price series (top left and right); Austin and West (Bottom left and right).

Significance

Significance of the latent

of the latent factor

factorcoefficient.

coefficient.From

From Table

Table3,3, the

the endogenous

endogenous latent

latent factor

factor

variable,

variable, ft,, when

whenititappears

appearsasasanan exogenous

exogenous variable in the

variable observation

in the equation

observation is sta-

equation is

tistically significant for all the nine models (p < 0.00001). This result confirms

statistically significant for all the nine models (p < 0.00001). This result confirms one of one of the

principal

the principalassertions in this

assertions in paper, namely

this paper, namelythat that

therethere

are hidden, unobserved

are hidden, factors

unobserved that

factors

influence the distribution of real-time prices throughout a 24-h cycle across

that influence the distribution of real-time prices throughout a 24-h cycle across all zones. all zones. Da-

mien

Damienet al. [29][29]

et al. dodonotnot

useuselatent factors

latent factorsinintheir

theirsystem-wide

system-widepricepriceand

anddemand

demand ERCOT

ERCOT

model.

model. ItIt is

isevident

evidentfrom

from this

this research

research that

that latent

latent factors

factors play

play aa significant

significant role

role in

in ERCOT’s

ERCOT’s

pricing

pricing structure.

structure.

Table 3.

Table Coefficients for

3. Coefficients for the

the Latent

Latent Factor

Factor ft ..

AustinAustin

HoustonHouston

LCRA LCRANorth NorthRAYB RAYB CPSCPS South

South West

West

4:004:00

a.m.a.m. 0.571 0.571

0.532 0.5320.5810.581 0.5330.533 0.510

0.510 0.550

0.550 0.541

0.541 0.621

0.621

12:00 p.m.

12:00 p.m. 0.266 0.266

0.284 0.2840.2730.273 0.2230.223 0.204

0.204 0.272

0.272 0.268

0.268 0.292

0.292

4:00 p.m. 0.433 0.430 0.441 0.427 0.425 0.423 0.412 0.461

4:00 p.m. 0.433 0.430 0.441 0.427 0.425 0.423 0.412 0.461

Note: All coefficients have p-values < 0.00001. The latent factor is a vector quantity; hence it appears in bold font

Note: All coefficients

to be consistent with thehave p-values

notation < 0.00001.

in Section 3. The latent factor is a vector quantity; hence it appears

in bold font to be consistent with the notation in Section 3.

The marginal effects of the exogenous variables. Consider Tables 4–6 which show the max-

imum likelihood

The marginal estimates (MLEs)

effects of the for coefficients

exogenous that appear

variables. Consider in the

Tables 4–6observation

which showand

the latent

max-

equations in (1); the corresponding p-values;

imum likelihood estimates (MLEs) for coefficients that appear in the observation and for

factor and the 95% confidence intervals la-

Hours

tent 4:00equations

factor a.m., 12:00inp.m., andcorresponding

(1); the 4:00 p.m., respectively,

p-values; for

andthe

thethree

95% zones.

confidence intervals

for Hours 4:00 a.m., 12:00 p.m., and 4:00 p.m., respectively, for the three zones.

Table 4. ML coefficients for the 4:00 a.m. hour.

Coefficient p-Value 95% Confidence Intervals

Latent Factor Equation

0.1681 0.0030 0.0579 0.2783

SystemLoad 1.6092 0.00001 1.3573 1.8610

Lag(WtPr) −0.1248 0.1660 −0.3015 0.0518

Houston Equation

0.5331 0.00001 0.5117 0.5545Appl. Sci. 2021, 11, 7039 10 of 15

Table 4. ML coefficients for the 4:00 a.m. hour.

Coefficient p-Value 95% Confidence Intervals

Latent Factor Equation

ft −1 0.1681 0.0030 0.0579 0.2783

SystemLoad 1.6092 0.00001 1.3573 1.8610

Lag(WtPr) −0.1248 0.1660 −0.3015 0.0518

Houston Equation

ft 0.5331 0.00001 0.5117 0.5545

Wind −0.3570 0.00001 −0.4027 −0.3112

Nuclear −0.7034 0.00001 −0.9073 −0.4995

Henry Hub 1.1530 0.00001 0.9328 1.3733

Austin Equation

ft 0.5709 0.00001 0.5502 0.5917

Wind −0.3674 0.00001 −0.4143 −0.3204

Nuclear −0.7780 0.00001 −0.9948 −0.5612

Henry Hub 1.1212 0.00001 0.8919 1.3505

West Equation

ft 0.6207 0.00001 0.5831 0.6583

Wind −0.5517 0.00001 −0.6190 −0.4845

Nuclear −0.7153 0.00001 −0.9645 −0.4662

Henry Hub 1.1317 0.00001 0.8288 1.4345

Table 5. ML coefficients for the 12:00 p.m. sample.

Coefficient p-Value 95% Confidence Intervals

Latent Factor Equation

ft −1 0.2240 0.00001 0.1412 0.3067

SystemLoad 2.0997 0.00001 1.8646 2.3348

Lag(WtPr) −0.2542 0.0430 −0.4999 −0.0085

Houston Equation

ft 0.2845 0.00001 0.2713 0.2977

Wind −0.0943 0.00001 −0.1151 −0.0736

Nuclear −0.5532 0.00001 −0.6576 −0.4487

Solar 0.0243 0.0630 −0.0013 0.0500

Henry Hub 0.6154 0.00001 0.4786 0.7522

Dummy 2.4006 0.00001 2.1030 2.6982

Austin Equation

ft 0.2661 0.00001 0.2559 0.2763

Wind −0.1432 0.00001 −0.1603 −0.1261

Nuclear −0.4445 0.00001 −0.5392 −0.3497

Solar 0.0090 0.4140 −0.0126 0.0307

Henry Hub 0.6454 0.00001 0.5272 0.7636

Dummy 1.2841 0.00001 1.0444 1.5237

West Equation

ft 0.2916 0.00001 0.2684 0.3148

Wind −0.2826 0.00001 −0.3155 −0.2497

Nuclear −0.3945 0.00001 −0.5201 −0.2689

Solar 0.0093 0.6340 −0.0292 0.0478

Henry Hub 0.5949 0.00001 0.4013 0.7885

Dummy 0.9767 0.00001 0.4842 1.4692Appl. Sci. 2021, 11, 7039 11 of 15

Table 6. ML coefficients for the 4:00 p.m. sample.

Coefficient p-Value 95% Confidence Intervals

Latent Factor Equation

ft −1 0.1326 0.0010 0.0571 0.2080

SystemLoad 1.8513 0.00001 1.6365 2.0661

Lag(WtPr) 0.2243 0.0010 0.0899 0.3587

Houston Equation

ft 0.4302 0.00001 0.4117 0.4487

Wind −0.1761 0.00001 −0.2085 −0.1438

Nuclear −0.7292 0.00001 −0.8540 −0.6043

Solar 0.0703 0.00001 0.0413 0.0993

Henry Hub 0.3608 0.00001 0.2006 0.5211

Dummy 2.0212 0.00001 1.8419 2.2004

Austin Equation

ft 0.4334 0.00001 0.4169 0.4499

Wind −0.2222 0.00001 −0.2520 −0.1924

Nuclear −0.6829 0.00001 −0.8060 −0.5599

Solar 0.0482 0.00001 0.0211 0.0752

Henry Hub 0.3430 0.00001 0.1933 0.4927

Dummy 1.8556 0.00001 1.6916 2.0195

West Equation

ft 0.4615 0.00001 0.4307 0.4922

Wind −0.4326 0.00001 −0.4827 −0.3825

Nuclear −0.5835 0.00001 −0.7351 −0.4319

Solar 0.0473 0.0320 0.0040 0.0906

Henry Hub 0.5272 0.00001 0.2893 0.7651

Dummy 1.2448 0.00001 0.9629 1.5268

Since we are dealing with the natural logs of all the variables, the MLEs represent

elasticities. We first describe some overarching conclusions from all three tables here,

saving for later the discussion of the merit-order effects.

First, from the latent factor equations for all three hours and zones, system-wide

load (SystemLoad) positively and significantly impacts the hidden factors. Second, lagged

weighted price (LagWtPr) is not significant in the off-peak hour but is significant during

the peak hours. Interestingly, it impacts the hidden factors negatively at the noon hour

and positively at the 4:00 p.m. hour. Third, the lagged latent factor variable is positive and

statistically significant at all three hours for all three zones in the latent factor equation. In

conjunction with the plots shown in Figures 4–6, this further confirms the importance of

the latent factor dynamics on energy prices in all eight zones. Fourth, from the observation

equation for the three zones, during all three hours, as expected, wind generation and

nuclear generation have negative elasticities, and Henry Hub gas has positive elasticity.

Fifth, solar generation is a mixed bag, largely because this resource is still growing in Texas,

and as such its data are non-stationary. Thus, solar generation is not significant at 12:00 p.m.

and its elasticities are positive and weak at 4:00 p.m. Finally, the impact of extreme spikes

in real-time prices (the dummy variable) at 12:00 p.m. and 4:00 p.m. is highly significant in

all three zones.

System-wide merit-order effects. To best understand the merit-order effects shown as

elasticities in Tables 4–6, consider the price boxplots shown in Figure 7. The top, middle

and bottom panels, corresponding to hours 4:00 a.m. 12:00 p.m., and 4:00 p.m., respectively,

have three boxplots in each panel. On the X-axis, the box titled “Before Price” is the

group of mean prices in the eight ERCOT zones before accounting for any merit-order

effect. The second and third boxes are the change in mean prices after accounting for

merit-order effects in wind and nuclear generation, respectively. The Y-axis represents

the mean price values ($/MWH). Each value on this axis is the mean price from each of

the eight zones during the years 2015–2018. Focus on the 4:00 a.m. panel at the top. The

interquartile range (IQR) of the mean prices of the eight zones in ERCOT at this hour is

$16.18 to $16.61; see the left-most box in blue. Next, assume wind generation increasesAppl. Sci. 2021, 11, 7039 12 of 15

by 10%. Using the MLE estimates of the price elasticities for wind generation for each of

Appl. Sci. 2021, 11, 7039 the eight zones from our latent-factor system model, we adjust the mean prices in the 12 blue

of 15

box and construct the resulting change in prices due to increased wind generation. The

corresponding distribution of the adjusted mean prices in ERCOT is shown as the second

box

in in From

red. red. From the caption,

the caption, the for

the IQR IQRtheforprices,

the prices,

after after accounting

accounting for increased

for increased windwind

gen-

generation, is between $15.59 and $16.07. Finally, we do a similar adjustment to energy

eration, is between $15.59 and $16.07. Finally, we do a similar adjustment to energy prices

prices using the parameter estimates for nuclear generation; this is shown as the green box

using the parameter estimates for nuclear generation; this is shown as the green box in the

in the top row of Figure 7. The IQR is between $14.98 and $15.42. Observing the three

top row of Figure 7. The IQR is between $14.98 and $15.42. Observing the three panels, it

panels, it is also interesting to note that there is less volatility in the mean prices in the

is also interesting to note that there is less volatility in the mean prices in the entire ERCOT

entire ERCOT system during the off-peak hour.

system during the off-peak hour.

Figure 7. ERCOT merit-order effects for wind and nuclear generation.

Figure 7. ERCOT merit-order effects for wind and nuclear generation.

Consider

Consider the

the middle

middlepanel

panelwhich

whichcorresponds

correspondstotothe

the12:00 p.m.

12:00 p.m. hour. While

hour. the the

While re-

duction in energy prices is less now, wind and nuclear generation still have a measurable

reduction in energy prices is less now, wind and nuclear generation still have a measurable

impact on real-time prices in ERCOT as a whole. Also, there is more volatility in real-time

prices during this peak hour.

Finally, the bottom panel shows the impact on prices due to the merit-order effects

at 4:00 p.m. Nuclear generation is much more influential than wind at this hour of the day;

its boxplot barely intersects with the boxplot from wind generation. Also, the volatility in

ERCOT’s prices is lesser at 4:00 p.m. when compared to 12:00 p.m.Appl. Sci. 2021, 11, 7039 13 of 15

impact on real-time prices in ERCOT as a whole. Also, there is more volatility in real-time

prices during this peak hour.

Finally, the bottom panel shows the impact on prices due to the merit-order effects at

4:00 p.m. Nuclear generation is much more influential than wind at this hour of the day;

its boxplot barely intersects with the boxplot from wind generation. Also, the volatility in

ERCOT’s prices is lesser at 4:00 p.m. when compared to 12:00 p.m.

5. Conclusions

This paper demonstrated the relevance of latent factors on real-time energy prices

using a system-wide approach. The ERCOT system served as the case study. Using

energy prices from eight inter-connected zones as endogenous variables, we found that

hidden factors significantly impact the merit-order effects of baseload and renewable

energy generation.

The latent-factor approach developed here can be improved and extended.

Damien et al. [29] use a hierarchical Bayesian approach to compare the impact of day-

ahead and real-time prices on wholesale demand in ERCOT. However, they do not model

latent factors. This paper clearly shows the importance of accounting for such factors. A

Bayesian latent factor system-wide model for prices and/or demand is possible in principle;

see [30]. However, the challenges are formidable. First, since the parameter space is very

large, convergence issues will be a difficult problem to overcome. Concurrently, while

studying energy prices or demand, the attendant datasets tend to be very large, as in this

paper. This too will add to convergence issues since the likelihood function will have to be

evaluated many-fold in any Markov chain Monte Carlo scheme that is required to obtain

posterior distributions.

Another future topic for research that this paper proposes is to model the system of

equations in Equation (1) via non-normal errors. For example, Williamson et al. [1] use a

nonparametric error distribution—the Indian Buffet Process—to develop a new class of

latent factor models. But with large datasets, such nonparametric approaches are even

more computationally involved compared to parametric formulations.

Why should a non-normal error structure matter in the context of energy prices,

and in the estimation of merit-order effects? Recent studies [21,22] have shown that

prices have asymmetric distributions with large kurtosis. Subsequently, error distributions

from normal linear models tend to be non-normal heteroscedastic and autocorrelated.

Hence, quantile regressions have been proposed and exemplified in the energy literature.

However, there is a trade-off. Because of the mathematics underlying them, quantile

regressions are essentially single-equation models. Thus, the prices of each of ERCOT’s

eight zones can be modeled separately using quantile regressions; see [31]. But the results

in this paper clearly demonstrate the importance of treating the eight zones as part of

an interconnected system so that we can better understand how latent factors influence

prices jointly. This leads to an open question: how should one construct a system-wide,

latent-factor quantile regression model that is equivalent to Equation (1) in this paper? This

is a very challenging problem for multiple reasons. For example, consider a bivariate time-

series that represent prices from, say two of ERCOT’s eight zones. Further, suppose the error

term in the observation model in Equation (1) follows a bivariate skew-t distribution since

this distribution allows for varying degrees of skewness. How should one jointly model

the quantiles of this bivariate distribution as functions of latent factors and exogenous

variables? The answer is not at all evident even in this simple bivariate setup. Therefore,

instead of multivariate quantile regression systems, we believe, as a first step, it may be

easier to recast Equation (1) using nonparametric prior distributions. Indeed, this could

also lead to stronger correlations between the factor and price series since nonparametric

priors can better treat outliers. The resulting estimation of the merit-order effects in energy

markets would be a useful advancement.Appl. Sci. 2021, 11, 7039 14 of 15

Author Contributions: Conceptualization, P.D. and J.Z.; methodology, P.D.; software, K.H.C.; valida-

tion, K.H.C., P.D. and J.Z.; formal analysis, K.H.C. and P.D.; investigation, P.D. and J.Z.; resources, J.Z.;

data curation, K.H.C. and J.Z.; writing—original draft preparation, K.H.C., P.D. and J.Z.; writing—

review and editing, K.H.C., P.D. and J.Z.; visualization, K.H.C.; supervision, P.D. and J.Z.; project

administration, K.H.C. and P.D. All authors have read and agreed to the published version of

the manuscript.

Funding: This research received no external funding.

Institutional Review Board Statement: Not Applicable.

Informed Consent Statement: Not Applicable.

Data Availability Statement: Data presented in this study are available from the third author

upon request.

Conflicts of Interest: The authors declare no conflict of interest.

References

1. Williamson, S.; Zhang, M.; Damien, P. A new class of time-dependent latent factor models with applications. J. Mach. Learn. Res.

2020, 21, 1–24.

2. Gelabert, L.; Labandeira, X.; Linares, P. An ex-post analysis of the effect of renewable and cogeneration on Spanish electricity

prices. Energy Econ. 2011, 22, 559–565. [CrossRef]

3. Sensfuß, F.; Ragwitz, M.; Genoese, M. The merit-order effect: A detailed analysis of the price effect of renewable electricity

generation on spot market prices in Germany. Energy Policy 2008, 36, 3086–3094. [CrossRef]

4. Ketterer, J.C. The impact of wind power generation on the electricity price in Germany. Energy Econ. 2014, 44, 270–280. [CrossRef]

5. Cludius, J.; Hermann, H.; Matthes, F.C.; Graichen, V. The merit order effect of wind and photovoltaic electricity generation in

Germany 2008–2016: Estimation and distributional implications. Energy Econ. 2014, 44, 302–313. [CrossRef]

6. Paraschiv, F.; Erni, D.; Pietsch, R. The impact of renewable energies on EEX day-ahead electricity prices. Energy Policy 2014, 73,

196–210. [CrossRef]

7. Munksgaard, J.; Morthorst, P.E. Wind power in the Danish liberalized power market–Policy measures, price impact, and investor

incentives. Energy Policy 2008, 36, 3940–3947. [CrossRef]

8. Jacobsen, H.K.; Zvingilaite, E. Reducing the market impact of large shares of intermittent energy in Denmark. Energy Policy 2010,

38, 3403–3413. [CrossRef]

9. Clo, S.; Cataldi, A.; Zoppoli, P. The merit-order effect in the Italian power market: The impact of sola and wind generation on

national wholesale electricity prices. Energy Policy 2015, 77, 79–88. [CrossRef]

10. Cutler, N.J.; MacGill, I.F.; Outhred, H.R.; Boerema, N.D. High penetration wind generation impacts on spot prices in the Australian

national electricity market. Energy Policy 2011, 39, 5939–5949. [CrossRef]

11. Denny, E.; O’Mahoney, A.; Lannoye, E. Modelling the impact of wind generation on electricity market prices in Ireland: An

econometric versus unit commitment approach. Renew. Energy 2017, 104, 109–119. [CrossRef]

12. Quint, D.; Dahlke, S. The impact of wind generation on wholesale electricity market prices in the midcontinent independent

system operator energy market: An empirical investigation. Energy 2007, 169, 456–466. [CrossRef]

13. Zarnikau, J.; Tsai, C.H.; Woo, C.K. Determinants of the wholesale prices of energy and ancillary services in the US Midcontinent

electricity market. Energy 2020. [CrossRef]

14. Zarnikau, J.; Woo, C.K.; Zhu, S.S. Zonal merit-order effects of wind generation development on day-ahead and real-time electricity

market prices in Texas. J. Energy Mark. 2016, 9, 17–47. [CrossRef]

15. Zarnikau, J.; Woo, C.K.; Zhu, S.S.; Baldick, R.; Tsai, C.H.; Meng, J. Electricity market prices for day-ahead ancillary services and

energy: Texas. J. Energy Mark. 2018, 12, 1–32. [CrossRef]

16. Zarnikau, J.; Woo, C.K.; Zhu, S.S.; Tsai, C.H. Market price behavior of wholesale electricity products: Texas. Energy Policy 2019,

125, 418–428. [CrossRef]

17. Gil, H.A.; Lin, J. Wind power and electricity prices at the PJM market. IEEE Trans. Power Syst. 2013, 28, 3945–3953. [CrossRef]

18. Woo, C.K.; Zarnikau, J.; Kadish, J.; Horowitz, I.; Wang, J.; Olson, A. The impact of wind generation on wholesale electricity prices

in the hydro-rich Pacific Northwest. IEEE Trans. Power Syst. 2013, 28, 4245–4253. [CrossRef]

19. Woo, C.K.; Moore, J.; Schneiderman, B.; Olson, A.; Jones, R.; Ho, T.; Toyama, N.; Wang, J.; Zarnikau, J. Merit-order effects of

day-ahead wind generation forecast in the hydro-rich Pacific Northwest. Electr. J. 2015, 28, 52–62. [CrossRef]

20. Woo, C.K.; Moore, J.; Schneiderman, B.; Olson, A.; Jones, R.; Ho, T.; Toyama, N.; Zarnikau, J. Merit-order effects of renewable

energy and price divergence in California’s day-ahead and real-time electricity markets. Energy Policy 2016, 92, 299–312. [CrossRef]

21. Sirin, S.M.; Yilmaz, B.N. Variable renewable energy technologies in the Turkish electricity market: Quantile regression analysis of

the merit-order effect. Energy Policy 2020, 144, 111660. [CrossRef]

22. Maciejowska, K. Assessing the impact of renewable energy sources on the electricity price level and variability–A quantile

regression approach. Energy Policy 2020, 85, 104532. [CrossRef]Appl. Sci. 2021, 11, 7039 15 of 15

23. Geweke, J. The dynamic factor analysis of economic time series models. In Latent Variables in Socio-Economic Models; Aigner, D.J.,

Goldbergered, A.S., Eds.; North–Holland: Amsterdam, The Netherlands, 1977; pp. 365–383.

24. Watson, M.W.; Engle, R.F. Alternative algorithms for the estimation of dynamic factor, MIMIC and varying coefficient regression

models. J. Econ. 1983, 23, 385–400. [CrossRef]

25. Bernanke, B.S.; Jean, B.; Pitr, E. Measuring the effects of monetary policy: A Factor-Augmented Vector Autoregressive (FAVAR)

approach. Q. J. Econ. 2008, 120, 387–422.

26. Zagaglia, P. Macroeconomic factors and oil futures prices: A data-rich model. Energy Econ. 2010, 32, 409–417. [CrossRef]

27. De Jong, P. The likelihood for a state-space model. Biometrika 1988, 75, 165–169. [CrossRef]

28. De Jong, P. The diffuse Kalman filter. Ann. Stat. 1991, 19, 1073–1083. [CrossRef]

29. Damien, P.; Fuentes-García, R.; Mena, R.H.; Zarnikau, J. Impacts of day-ahead and real-time market prices on wholesale electricity

demand in Texas. Energy Econ. 2019, 81, 259–272. [CrossRef]

30. Petris, G.; Petrone, S.; Campanogli, P. Dynamic Linear Models with R; Springer: New York, NY, USA, 2009.

31. Ekin, T.; Damien, P.; Zarnikau, J. Estimating marginal effects of key factors that influence wholesale electricity demand and price

distributions in Texas via quantile variable selection methods. J. Energy Mark. 2020, 13, 1–30. [CrossRef]You can also read