CFA Institute Research Challenge - Hosted by

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge

Hosted by

CFA Society Taiwan

National Taiwan University

The CFA Institute Research Challenge is a global competition that tests the equity research and valuation, investment report writing, and

presentation skills of university students. The following report was prepared in compliance with the Official Rules of the CFA Institute Research

Challenge, is submitted by a team of university students as part of this annual educational initiative and should not be considered a professional

report.

Disclosures:

Ownership and material conflicts of interest:

The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company.

The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the

content or publication of this report.

Receipt of compensation:

Compensation of the author(s) of this report is not based on investment banking revenue.

Position as an officer or director:

The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subject company.

Market making:

The author(s) does not act as a market maker in the subject company’s securities.

Disclaimer:

The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be

reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information

is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment

advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by

any individual affiliated with CFA Society Taiwan, CFA Institute or the CFA Institute Research Challenge with regard to this company’s stock.

This report is published for educational purposes

only by students competing in The CFA Institute National Taiwan University

Research Challenge.

Equity|TWSE|Consumer Products|Consumer Staples 10 December 2018

Recommendation: Gourmet Master Co., LTD (2723 TT)

SELL When the Bakery Café Bakes in Caffeine Fading

We initiate coverage of Gourmet Master (GM) with a SELL rating and NT$190 target

Target Price NT$190

price, implying a 20% downside based on 20x 2019E P/E. Our 2019E EPS is 17%

Current Price (7 Dec.) NT$237 below the Street consensus.

Downside -20%

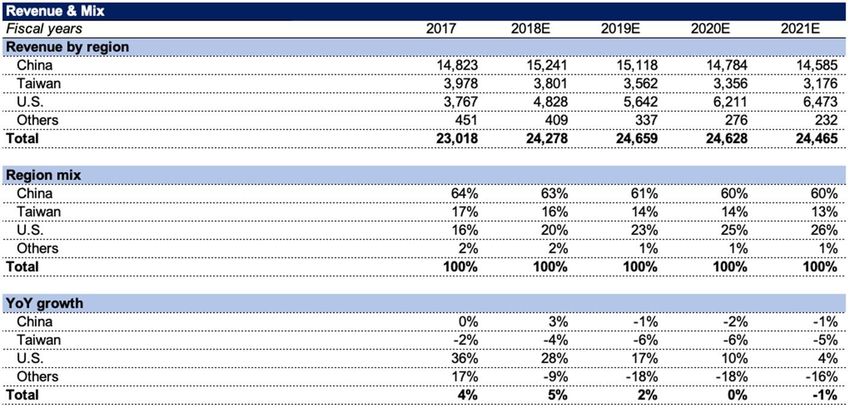

China (63% of total 2018E revenue): Pressures on revenue and operating margins

The China revenue growth has decelerated to 3% in 2018E from c.7% in 2016/17. We

Company Profile

expect revenue to further dip by -1%/-2% in 2019/20E in view of fading upsides from

NT$ 183.0 -

52-Weeks Price Range remodeling, online delivery competition, and China’s slower retail sales growth. We

NT$ 397.6

forecast GM’s per store sales decline in China will enlarge to 7% in 2019-20E, vs. 4%

Shares Outstanding 180M

in 2017-18E. Furthermore, start-up coffee brands like Luckin Coffee emerges as new

Market Cap. NT$ 42.7B threats to GM, as Luckin rapidly increases online visibility through heavy digital

USD/TWD (7 Dec.) 30.84 channel investment. We forecast the company’s operating margin in China will thus

Dividend Yield 2.3% decrease to 6% in 2019-20E, from c.10% in 2017-18E.

2018 P/E 24.8x

The US (20%): Slower store expansion due to aggressive competitors

Source: Bloomberg After stores increased from 40 to 55 in the US, GM’s US per store sales decreased by

c.12% over 2017-18E. We expect GM’s per store sales in the US to keep declining

Valuation Methodology Price (NT$) c.10% in 2019-20E due to elevating competition and cannibalization. Like GM, Paris

P/E 190 Baguette (PB) is an Asian bakery café in the US that aims to triple their US exposure

DCF 189 to 300+ stores by 2020E. We believe not only PB but further new entrants that

Target price 190 replicate GM’s business strategy will end up eroding GM’s market and slowing the

revenue growth almost half to 10% in 2020E, from 28% in 2018E.

Source: Team estimates

Taiwan (16%): Revenue to shrink amid fiercer competition

Since store format upgrade has ended in 1Q18, and organic growth loses its

Operating Margin and EPS Forecast

momentum, we expect GM’s per store sales in Taiwan to decrease by 9%/8% YoY in

15.0% 13

2019-20E, from 11%/9% in 2017-18E. Among the fierce competition, GM posts the

11 fewest registered members despite ongoing expansion. Compared with Taiwan coffee

10.0%

9 industry sales growing at 4% CAGR from 2012-17, we believe GM’s revenue growth

5.0% will fall to c.6% in 2019-20E because of failure to boost retention rates, from c.4% in

7

2017-18E.

0.0% 5

Initiate with NT$190 P/E-derived TP and SELL rating

We set GM’s one-year target price at NT$190, based on 20x 2019E EPS (at the lower

OPM (%; LHS) EPS (NT$; RHS)

end of P/E band), implying a 20% downside and cross-checked with DCF valuation. We

Source: Company data, Team estimates believe 20x P/E is fair due to GM's earnings downtrend in 2019E. We project that OPM

(peaked out in 3Q17 at 12.7%) would be 8.4%/7.0% in 2019/20E, and would result in

Stock Price Movement a -2% earnings growth in 2019E. Although the share price has undergone huge

12,000 500 correction this year, we believe the worst has not come yet, as the market has not

10,000 400 priced in vanishing competitive advantage due to rising engagement by other players

8,000

300 and the absence of moat.

6,000

200 Gourmet Master’s Key Financials

4,000

2,000 100 Year 2017 2018E 2019E 2020E 2021E 2022E 2023E

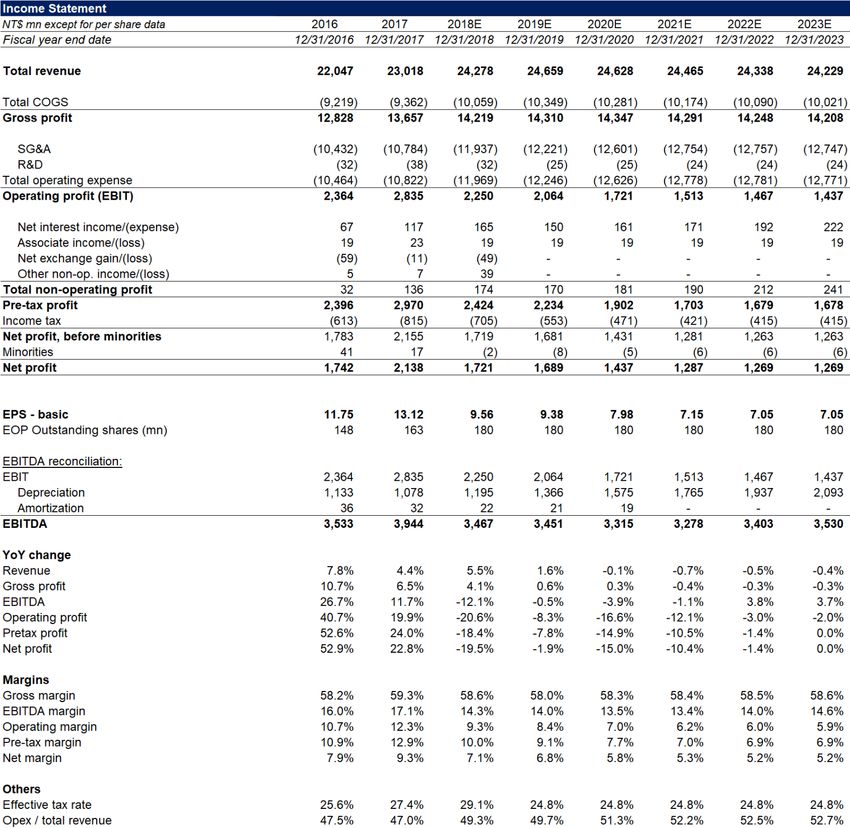

0 0 Revenue (NT$mn) 23,018 24,278 24,659 24,628 24,465 24,338 24,229

Revenue YoY (%) 4.4 5.5 1.6 -0.1 -0.7 -0.5 -0.4

Gross profit margin (%) 59.3 58.6 58.0 58.3 58.4 58.5 58.6

Operating margin (%) 12.3 9.3 8.4 7.0 6.2 6.0 5.9

TWSE (LHS)

Net income (NT$mn) 2,138 1,721 1,689 1,437 1,287 1,269 1,269

Gourmet Master TWSE (LHS)

Net income YoY (%) 22.8 -19.5 -1.9 -15.0 -10.4 -1.4 0.0

Source: Bloomberg Earnings Per Share (NT$) 13.12 9.56 9.38 7.98 7.15 7.05 7.05

Dividend Per Share (NT$) 5.4 4.3 4.2 3.6 3.2 3.2 3.2

Dividend yield (%) 1.5 1.8 1.8 1.5 1.4 1.4 1.4

P/E (x) 18.1 24.8 25.3 29.7 33.2 33.6 33.6

Source: Company data, Team estimates

National Taiwan University 1

Figure 1 Sales Breakdown by Region Business Description

Company Overview

Gourmet Master Co. Ltd. (GM), the holding company of 85°C Café, is a bakery café

providing a variety of food products including bread, beverage, and cake. By regions,

63% of sales come from China, 20% from the US, 16% from Taiwan and 1% from

Australia and Hong Kong (Figure 1).

Expansion Track Overview and Current Expansion Plan

GM started selling cakes and beverages in Taiwan, and through its franchise model, it

has broadened its reach to 443 stores by 3Q18. In contrast, GM embraces the self-

owned business model to manage food safety, for a consistent marketing strategy in

Source: Company data

China. GM positions itself as a bakery café to capture the rapidly growing Chinese

market. GM has 607 self-owned stores in operation. After expanding in China, GM

Figure 2 Product Mix by Region

100% landed on the US as an Asian bakery specialist. Following China's operating experience,

25% 30% 30% GM expands its market with self-owned business model and runs 49 stores. Overall,

80%

60% 20% beverage accounts for 55% revenue in Taiwan, bread for 55% revenue in the US, and

30% a more balanced product mix in China (Figure 2 and Figure 3).

40% 55%

55%

20% 40%

15% Aside from the three major markets, GM also extended its footprint to Australia in

0%

2007 and Hong Kong in 2012 by forming joint ventures with local enterprises. GM

USA China Taiwan

Bread Beverage Cake

bought back 50% ownership from Café de Coral in 2014 and directly ran all stores in

Hong Kong thereafter.

Source: Company data

Figure 3 Store Numbers by Region Recent Regional Strategies

26

In the US, GM will open two new central kitchens in Northern California and Texas to

1,200 24

15

40 49 support its store expansion. It also makes inroads into delivery services through

12 13

25

900 9

14 17 443 partnership with DoorDash at select branches.

7 400 429

332 350

600 341

In China, GM will focus on 2nd generation store remodeling and slow its expansion

300 489 502 538 580 607

pace. By 3Q18, the proportion of 2nd generation stores reached 77%, and GM will

410

- refurbish the rest in following years. In addition, GM wants to target young females

2013 2014 2015 2016 2017 9M18 through its new store format and plans to expand into inland China by opening new

China Taiwan US Others stores in lower tier cities.

Source: Company data

In Taiwan, GM has completed all the remodeling projects in 1Q18. Furthermore,

Figure 4 Shareholder Structure as of 3Q18 facing the trend of online food delivery services, GM has recently launched an in-

house 85 Café app, which allows customers to order online and collect points.

Others

12% In Australia, GM announced changes in the local management team (but still owning

Chairman 51% of the Australian entity) starting from 3Q18. GM aims to take more active control

QFIIs

Wu and his of the business, hoping to see more positive performance.

family

37%

51%

Shareholder Structure

Chairman Wu, the founder of Gourmet Master, and his family hold 51% of equity

Source: Company data

directly and indirectly via investment vehicles (Figure 4), having a strong commitment

in senior management and board of directors (Appendix 8). Between 2015 and 2017,

foreign ownership gradually increased from 30% to 40%. However, as the stock price

Table 1 Corporate Governance

started to fall and foreign ownership dropped to 37%, we believe it is a signal that

GM Peers foreign institutional investors are doubtful about GM’s prospects.

Executives

Number of Executives 5 10 Corporate Governance

Avg. Tenure (Years) 7 5

In order to justify the efficiency and credibility of its management, we compare GM

Remuneration (% of PBT) 0.58 6.25

to its peers (Appendix 8). GM operates in a relatively small group of management with

Directors

longer average tenure and high attendance rate (Table 1). The board of directors

Number of Board Members 7 10

Independent Directors 3 3 consists of 7 people and 3 of them are independent directors. Considering

Avg. Meeting Attendance % 97 90 management’s remuneration, even though GM has experienced a robust growth in

Remuneration (% of PBT) 0.95 3.35 recent years, executives’ and directors’ pay and performance related bonus remain

Source: Company data stable and remuneration-to-profit-before-tax (PBT) ratio is lower than its peers

(include President Chain Store Corp., BreakTalk, and etc).

National Taiwan University 2

Figure 5 Revenue Growth by Region Investment Summary

40% 36% We issue a “Sell” recommendation on Gourmet Master, with a target price of

28% NT$190 due to falling revenue growth and OPM in China, the US and Taiwan (Figure

30%

20%

17% 5 and Figure 6).

10%

10% 4%

4% 5% 2% We analyze the company by breaking down to major operating regions:

0% 0% -1% 0%

3% -1% -2% -1% 1) China: Growth ceiling given declining benefits from remodeling projects, weaker

-2%

-10% -4% -6% -6% -5% consumer demand, and fiercer competition.

2017 2018E 2019E 2020E 2021E

China Taiwan US Overall 2) US: Softer outlook in face of aggressive expansion by competitors.

Source: Company data, Team estimates 3) Taiwan: Lack of imminent catalysts and failure to boost retention rates.

Figure 6 OPM by Region China (63% of total 2018E revenue): Pressures on revenue and OPM

16.0% 14.4% The rectification effect of 2nd generation stores on revenue

13.5%

13.5% The forward momentum brought by 2nd generation stores will lose gas along with the

13.0% 13.0% 13.0%

12.0% 12.3% 11.0%

10.5% increased ratio of 2nd generation stores. GM’s revenue growth has decelerated to 3%

11.4% 9.3% 8.0% in 2018E from c.7% in 2016/17, when remodeling initiatives rolled out. We expect GM

8.0% 8.4% 6.7%

8.3% 7.0% to finish remodeling all of its stores in 2022E (Figure 7), which will result in a -1%

6.2% revenue growth. 2nd generation stores help extend customers’ stay and raise the

6.8%

4.0% 5.2% 4.5% higher-margin beverage mix to 30% from 25%, due to enlarged seating areas. We

2017 2018E 2019E 2020E 2021E

China Taiwan US Overall

believe that GM’s per store sales growth in China will fall to -7% in 2022E from 4% in

Source: Company data, Team estimates 2014.

Figure 7 Expected Remodeling Schedule Challenge by weakening consumer market

800 100% China’s retail sales YoY growth has declined to 8.1% in 11M18 from 10.7% in 1M14,

700 and we do not expect the trend to reverse in near future given an undesirable

600 80%

500 60%

macroeconomic condition in China (Figure 8). As purchasing power continues to slow

400 down, consumers may be less willing to spend on aspirational goods such as pastries

300 40%

and coffee, dragging GM’s revenue.

200 20%

100

0 0% Lagging behind in online delivery hurts GM’s OPM

Online delivery services are heating up in China, but GM is shying away from the

Gen 1 opportunity, instead increasing it’s operating expense by 4% in 2018 to fund

Gen 2 traditional promotion pipelines. We believe it will increase by c.6% in 2019-20E. GM

Ratio of Gen 2 Stores intentionally holds back on sales through online delivery, which is 10% of total

Source: Team estimates revenue in 2018E, compared to competitor Luckin Coffee’s 50% (Figure 10). The

competition became fiercer when the leading traditional chain store, Starbucks,

Figure 8 China Retail Sales YoY Growth stepped into the battle in September 2018. Moreover, 48% of Luckin Coffee’s

12% customers are 24 and below, vs. 26% of GM’s customers (Appendix 16), attracted by

11% the convenience of online delivery services. This coincides with GM’s target

customers group, hindering GM’s promotions efforts (Figure 9). With this in mind, we

10%

forecast the company’s operating margin in China to thus decrease to 6% in 2019-20E,

9%

from c.10% in 2017-18E.

8%

Jun-15

Nov-15

Dec-17

Jul-17

Oct-18

Apr-16

Sep-16

Feb-17

May-18

Jan-15

Figure 10 Coffee brands online delivery timeline and sales proportion

Source: National Bureau of Statistics of China

Figure 9 SG&A Expense in China

NT$ mn

8,200 8,081 8,050 8,095 8,094 56.0%

55.5%

8,000 54.8%

54.0%

7,800 7,658 53.2%

53.0%

7,600

52.0%

51.7%

7,400

7,200 50.0%

2017 2018E 2019E 2020E 2021E

SG&A SG&A/Revenue(%; RHS)

Source: Company data, Team estimates Source: Company data

National Taiwan University 3

Figure 11 GM’s Store Number & Per Store The US (20%): Slower store expansion than aggressive competitors

Sales in the US Elevating competition and reined expansion to weigh on revenue growth

NT$ mn After stores increased from 40 to 55 in the US, GM’s US per store sales decreased by

160 100

116

c.12% over 2017-18E. We expect GM’s per store sales in the US to keep declining

120 102 80

90

c.10% in 2019-20E due to elevating competition and cannibalization (Figure 11). In

82 60

80 75 order to meet its mid-term target of 100 stores by 2022E in the US, GM expects a

40 smaller central kitchen to commence operation in 1Q19, and we expect the company

40 20

40 55 70 82 91 to pencil in construction of another central kitchen in Texas in 2Q20-3Q20E. However,

0 0 site selection for central kitchens will rein expansion to the West and thus result in

2017 2018E 2019E 2020E 2021E

cannibalization.

Store number in the US (LHS)

Per store sales in the US (RHS)

Source: Company data, Team estimates Like GM, Paris Baguette (PB) is an Asian bakery café in the US that aims to target more

Asian communities and to triple their US exposure to 300+ stores by 2020E, vs.

Figure 12 Paris Baguette and 85 Café US estimated GM store addition of 15/12 stores in 2019/20E. We render GM will miss

Store Location growth opportunity from pent-up demand for Asian bread, given its slower expansion

pace than competitor. In addition to focusing on corporate growth in California and

New York, PB has already established footholds in Texas, Illinois, and New Jersey,

where large Asian communities reside (Figure 12).

We believe that PB will not be the only player aiming for rapid expansion in the US

Asian bakery market, due to a low entry barrier. PB, along with possible new entrants

who replicate GM’s business strategy, will end up eroding GM’s market and cut its

revenue growth nearly in half to 10% in 2020E, from 28% in 2018E.

Source: Company data

Taiwan (16%): Revenue to shrink amid fiercer competition

Figure 13 GM’s Store Number & Per Store Declining per store sales due to settled refurbishment and under-monetized

Sales YoY in Taiwan expansion

500

-3% Since store format upgrade has ended in 1Q18, and organic growth loses momentum

474

467 480 in a competitive market, we expect GM’s per store sales to decrease by 9%/8% YoY in

-5% 458

446 -7% 460 2019-20E (Figure 13). Similar to refurbishment in China, GM introduced the 2 nd

-7%

-9% 429 -8% 440 generation stores in Taiwan in 2013-14, leading to an SSSG uptick after the initial

-9% -9% launch and refurbishment each year. However, with refurbishment complete in 1Q18

-11% -11% 420

and no strategies for a next revamp round, we thus do not envisage any construction

-13% 400

2017 2018E 2019E 2020E 2021E

stimulus to the topline.

Store number in Taiwan (RHS)

GM has been unable to retain its customers amongst this fierce competition. Its

Per store sales YOY in Taiwan (%; LHS)

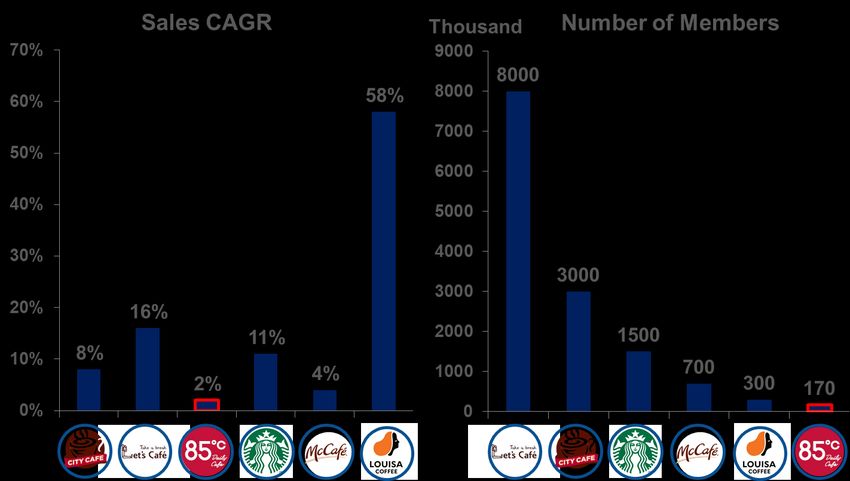

Source: Company data, Team estimates registered customer members are at 170,000, the fewest among competitors, and

almost half of rival Louisa Coffee. Although GM will continue to steadily expand its

Figure 14 Taiwan Coffee Shops Recent 5- store number to 474 in 2021E from 429 in 2017, its failure to defend amid fiercer

year Sales CAGR & Number of Members competition has already reflected on its 2% sales CAGR in 2012-2017, indicative of

Thousand under-monetized expansion (Figure 14). We thus believe GM’s revenue growth will

8,000 60%

fall to c.6% in 2019-20E because of failure to boost retention rates, from c.4% in 2017-

6,000 40% 18E.

4,000

2% 20%

2,000

0 0%

number of members (LHS)

5YR Sales CAGR (RHS)

Source: Company data, Team estimates

National Taiwan University 4

Valuation

Table 2 Target Price Table P/E valuation is our primary methodology

Valuation Methodology Price (NT$) Our 12-month target price of NT$190 is based on 20x 2019E EPS, implying a 20%

P/E 190 downside. We reason that P/E multiple is an appropriate metric since it helps us

DCF 189 capture the sustained earnings growth that the company will achieve.

Target price 190

Source: Team estimates In our sampling horizon, P/E mean of 25x is representative of average growth outlook

in China’s 2nd generation store era and accelerating topline growth in the US (Figure

15). We believe our target multiple of 20x is fair, considering: 1) The company’s

Table 3 P/E Summary operation has hit a ceiling, with escalating competitive pressure and slower store

2018E 2019E expansion, and we forecast earnings to grow -2%/-15% in 2019/20E, much lower than

Gourmet Master 19.8x 20.2x the market consensus 15%/26%; 2) The last time GM traded at the lowest end of our

Taiwan 27.6x 25.6x P/E band was at the time when CNY depreciated acutely against TWD.

Greater China 39.4x 29.8x

Asia Pacific 27.9x 24.7x Peer comparison

The US 26.6x 23.1x We also turn to P/E multiple comparison with global peers (Table 4). Our comparable

Source: Bloomberg, Team estimates companies are mostly from Taiwan, Greater China, and the US, where GM runs the

majority of their business. In Pan Asia, we choose the most representative public

companies from the space of retailers and food and beverage manufacturers based

on similar product mix (bread, coffee, or tea). Some of comparable companies are

restaurants, like Haidilao, since they provide alike two-way services (dine-in and

takeout). In the US, on top of coffee vendor Starbucks, our comparable peers are

mostly quick service restaurants, like McDonald’s and Yum!, as GM has a more

takeout-centric business there.

Since GM's earnings growth of -2% in 2019E is lower than most of the peers', we argue

that GM does deserve a discount to the average P/E multiple in its major business

regions (vs. 25.6x/29.8x/23.1x in Taiwan/Greater China/the US) (Table 3). Our 20x

multiple is also reasonable given its earnings growth in Asia Pacific region scope. GM

is now traded at 25x 2019E EPS, and we think the current valuation premium comes

from excess optimism about GM’s growth story overseas, while the market overlooks

potentially vanishing competitive advantage due to rising engagement by other

players and the absence of moat.

Figure 15 Gourmet Master’s Forward P/E Band

500 OPM dilution from CK in

the US

400

34x

300 29x

25x (Mean)

200 20x

16x

100 Gen 2 remodeling in China

and fast growth in the US

0

1/2/2016 7/2/2016 1/2/2017 7/2/2017 1/2/2018 7/2/2018

Source: Bloomberg, Team estimates

National Taiwan University 5

Table 4 Gourmet Master’s Comp Table

Market EPS (LC) NI YoY P/E (x)

PX_Last

Ticker Com pany nam e Cap

(LC) 2017 2018E 2019E 2018E 2019E 2018E 2019E

(US$m n)

Taiw an

2723 TT Gourmet Master 236.5 1,400 13.12 9.56 9.38 -20% -2% 19.8 20.2

1216 TT Uni-President 68.9 12,537 7.01 3.09 3.29 -56% 6% 22.0 20.7

2912 TT President Chain Store Corp 313.0 10,406 29.83 9.89 10.75 -67% 9% 31.2 28.7

5903 TT Taiw an FamilyMart 213.0 1,564 6.30 7.30 7.89 15% 9% 29.6 27.4

Average (excl. GM) 27.6 25.6

Greater China

6862 HK Haidilao 17.2 11,734 n.a. 0.32 0.50 66% 57% 47.3 30.2

601933 CH Yonghui Superstores 7.3 10,871 0.19 0.17 0.24 -13% 42% 46.2 33.0

Table 5 WACC Assumption 345 HK Vitasoy 31.4 4,044 0.56 0.67 0.80 20% 20% 44.6 37.5

603866 CH Toly Bread 47.8 3,099 1.14 1.38 1.68 25% 22% 32.9 27.0

WACC Assumptions 1579 HK Yihai 19.9 2,590 0.27 0.46 0.61 78% 35% 37.0 27.9

Risk-free Rate 10yr TW Gov’t Bond Yield 603711 CH Xiangpiaopiao 19.1 1,273 0.74 0.73 0.90 14% 27% 28.6 23.2

Average 39.4 29.8

TWSE Total Return Index to

Asia Pacific

Capture Dividend Yields and WOW AU Woolw orths Group 29.2 26,708 1.23 1.25 1.36 7% 9% 23.0 21.2

Market Return

Capital Gains over 5-yr CPALL TB CP All 71.5 19,033 2.14 2.31 2.62 5% 14% 29.9 26.4

Horizon DFI SP Dairy Farm 9.1 12,242 0.30 0.36 0.40 21% 11% 25.3 22.4

Monthly Returns to Regress MAKRO TB Siam Marko 33.0 4,753 1.29 1.20 1.26 -6% 5% 26.9 25.7

Beta against TWSE Index’s over 5- 2212 JP Yamazaki Baking 2,411 4,404 114.41 73.94 86.49 -36% 17% 29.8 25.5

SSG SP Sheng Siong Group 1.1 1,161 0.05 0.05 0.05 1% 11% 22.1 20.4

yr Horizon

BREAD SP BreadTalk Group 0.9 332 0.04 0.02 0.03 -46% 26% 38.6 31.2

Cost of Equity CAPM Model

Average 27.9 24.7

Weighted Average Borrowing U.S.

Cost of Debt Rate By Tranches Based on MCD US McDonald's 183.0 131,271 6.67 7.74 8.23 12% 3% 22.0 20.7

3Q18 Disclosures SBUX US Starbucks 65.5 75,131 2.67 2.42 2.73 6% 3% 25.0 22.2

Weighted Average Tax Rate YUM US Yum! Brand 90.4 27,177 4.23 3.72 3.80 14% -2% 23.4 22.9

Tax Rate YUMC US Yum China Holdings 35.0 12,233 1.50 1.51 1.62 6% 6% 21.4 20.0

Based on Regional Earnings %

CMG US Chipotle Mexican Grill 467.4 10,721 6.26 8.52 11.94 26% 39% 45.3 32.3

Source: Team estimates

DNKN US Dunkin' Brands Group 71.6 5,115 2.28 2.83 2.99 7% 2% 21.9 20.7

WEN US Wendy's 17.1 3,552 0.42 0.55 0.66 29% 9% 27.3 22.7

Table 6 WACC Calculation Average 26.6 23.1

WACC Calculation

Source: Bloomberg, Team estimates

Cost of Equity 7.3%

Risk Free Rate 1.0% Using DCF valuation to support

We also apply DCF valuation approach to cross-check our valuation methodology. We

Beta 0.96

ration that DCF is suitable to provide valuation support because GM tends to generate

Market Risk Premium 6.5% predictable, positive cash flows. In addition, DCF model incorporates our long-term

Cost of Debt (after tax) 2.4% view of the company’s growth sustainability and the impact of potential risks on

bottom-line.

Cost of Debt 3.2%

Tax Rate 25% Our model factors in our earnings forecast up to 2023E and a terminal growth rate of

Debt-to-Total-Capital Ratio 2.1% 1.5% thereafter, roughly in-line with long-term GDP growth. We consider our terminal

WACC 7.2%

growth assumption reasonable since the company operates in a mature industry, and

the characteristic of low entry barrier as well as possible material consumer

Source: Bloomberg, Team estimates

preference change in bakery & café can alter competitive landscape and thus result in

value depletion. Our WACC comes in at 7.1%, which assumes a risk-free rate of 1.0%,

Table 7 Equity Value Calculation a market risk premium of 6.5% and an equity beta of 0.96x (calculated by regressing

NT$ Million

monthly excess return against TAIEX’s over a five-year time frame), with cost of debt

of 3.2%, a targeted debt-to-capital ratio of 2.1%, and a 25% effective tax rate.

Enterprise Value 29,182

Cash and Equivalents 2,138 DCF valuation echoes our call

Total Debt 903 Our DCF-based target price of NT$189 for GM is derived from our two-stage DCF

model, after rounding, and echoes our call. Overall, we factor China’s disrupted

Equity Value 33,994

business in the presence of new retail mode and weaker macroeconomic conditions,

Shares Outstanding 180 fiercer competition from other Asian bakery participants in the US, and revenue

Value Per Share 189 downtrend in Taiwan into our forecast. See Table 6 and Appendix 7 for DCF

assumption and calculation.

Source: Bloomberg, Team estimates

National Taiwan University 6

Figure 16 Per Capita Coffee Consumption Industry Overview and Competitive Positioning

by Country Because Gourmet Master runs bakery café business in China, Taiwan and the US, we

kgs

15 focus on bread and beverage in China, bread in the US, and beverage in Taiwan

10 according to revenue proportion.

5 0.1kg

China industry overview and positioning (Bread/Beverage: 40%/30% of revenue in

0 China)

Low penetration of coffee and bakery market in China

If we look into industry data, penetration of the coffee and bakery market is low in

Per Capita Coffee Consumption China. According to Euromonitor, China’s current annual baked goods consumption

Source: International Coffee Organization per-capita is only 7kg, far below 9/23/40 kg in Taiwan/Japan/the US. The same story

occurs in Chinese coffee market. According to International Coffee Organization (ICO),

Figure 17 Shares of Major Coffee Brands in China’s current annual coffee consumption per-capita is only 0.1kg (Figure 16), far

China by Volume below 2.2/3.6/5.4kg in Taiwan/Japan/the US, indicating that the Chinese are not used

Others Gourmet Master to drinking coffee in their daily lives.

15% 2%

Pacific

3%

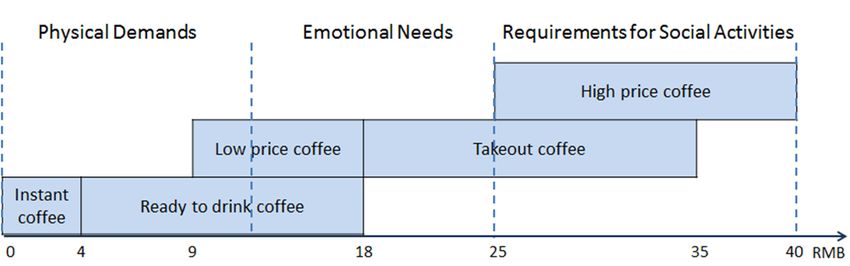

Budget fresh coffee cannot reap benefits

Cross Straits Starbucks Our team believe that budget fresh coffee suppliers like 85°C Café, whose price ranges

4% 51% from Rmb 10 to 15, will not gain meaningful market share from the secular trend of

Costa McCafe consumption upgrade. According to iResearch, drinking coffee can bring three stages

6% 6%

of mental satisfaction: 1) to meet physical demand or refreshing; 2) to satisfy

ShangDao

13% customer’s emotional needs; and 3) to fulfill the requirements for social activities.

Source: iResearch Unlike high-priced coffee vendors such as Starbucks, which has already established

image of networking space, low-priced fresh coffee brings mostly first-stage

Figure 18 China Coffee Brand Delivery satisfaction. We render that GM’s budget coffee will not gain significant market share

0 Service Launch Time (Figure 17) in era of ongoing premiumisation, while customers would rather turn to

much cheaper, more accessible instant coffee for satiating refreshing demand

(Appendix 14).

Fiercer competition from customer habits to online food delivery

Traditional business model has been challenged since more competitors aggressively

focus on food delivery services in recent years (Figure 18), including Luckin Coffee and

Source: Company data

Coffee Box. The proportions of orders submitted through food delivery platforms in

Tier 1 and Tier 2 cities are 20% and 40%, respectively, according to Meituan. New

Figure 19 China Baked Goods Market retail model has proliferated and helps startups nibble market share in recent years

RMB mn by deep involvement in promotions and delivery service. We expect the new business

400,000 CAGR 12.3% 13%

model to mature in 5 years, thanks to rising food delivery service penetration and high

300,000 internet user base (Appendix 23). The number of entrants embracing new business

12%

200,000 model will rise, and comparables will stimulate sales throughout heavy promotion

11% and advertisement. We expect the scenario will undermine the effectiveness of

100,000

traditional market share gain strategy through store expansion, especially in inland

0 10% cities.

Fragmented market weakens brand power of large industrial bakeries

Baked goods Retail Value

YoY (%; RHS) Although China’s bakery market is growing (Figure 19), the market is still fragmented.

Source: Euromonitor According to Euromonitor, Toly Bread occupied the most market share in 2017, 10%

(Figure 20), while any other brand did not account for over 6%. Consumer preference

Figure 20 Market Share of China Bakery is the main reason why well-known brands cannot enlarge their market share.

Brands According to iResearch, consumers prefer to buy featured goods, made by

independent stores or artisanal producers. In addition, standardized goods produced

Toly 10%

by central kitchens cannot satisfy different customer taste in the vast expanse of China.

6%

Others

4%

75% 2%

2%

Toly Fujian Dali Group

Panpanfood Garden Group

Yatai International Group Others

Source: Euromonitor

National Taiwan University 7

Figure 21 US Bakery Café Market, 2017 The US industry overview and positioning (Bread/Beverage: 55%/20% of revenue in

the US)

Low-single digit CAGR of bakery goods market

Others Starbucks The total consumption for bakery products will reach US$67.7 billion in 2022E, with

36% 28% 5-yr CAGR of 3%. The US bakery café market is one of the largest in the world, with

Dunkin total sales revenue amounting to US$59 billion. However, three major players take

Brands over 50% market share, which means new brands will have a difficult time competing

Panera 29% with market leaders (Figure 21). GM relies on its brand recognition being a seller of

7% unique Asian bread as well as competitive pricing of bread ($1.5-$2 per unit) to snatch

Source: Euromonitor a piece of market share in the US. If we look into the strategy of its Asian bread

competitors in the US like Paris Baguette, aiming to reach 300+ stores by 2020E and

Figure 22 US Fresh Coffee Market, 2017 1,000 stores by 2030E, we expect Paris Baguette may end up weighing on GM’s

operation.

Others Starbucks Mild growth in the coffeehouse-dominated coffee market

38% 40% In the US, the total coffee revenue will reach US$16 billion by 2022E with 5-yr CAGR

of 4%. Per capita consumption of coffee in 2017 grew to 4.8 kilograms from 4.2

Dunkin’ kilograms in 2012, and the figure was still relatively low, compared to several

22% European countries. In addition, large coffeehouse chains dominate coffee market in

Source: IBISWorld the US, with more than 60% of share (Figure 22). We reason it will be tough for GM

to strengthen its foothold in US coffee market due to American dietary habit and

Figure 23 Taiwan Fresh Coffee Market presence of chain giants.

NT$ mn

4,000 CAGR 14.6% 20%

Taiwan industry overview and positioning (Beverage/Bread: 55%/15% of revenue in

3,000 Taiwan)

2,000 10% Fresh coffee market faces saturation

The current market size of fresh coffee is NT$1,799.2 million (US$58.3 million), with

1,000

YoY growth expected to decline gradually to 11.7% from 18.2% between 2018E and

0 0% 2022E (Figure 23). Convenience store (CVS) continues to dominate this space with

high visibility and standardized offerings. Specialist coffee shops also enjoy rapid

Coffee Retail Value YOY (%; RHS) growth thanks to better return per square meter and featured themes catering to

Source: Euromonitor specific customers (Figure 24). Market saturation is in progress and the sector is very

competitive. We render that market share gain and customer retention will be key

Figure 24 Store Numbers of Taiwan Coffee factors to watch for GM since demand growth will moderate in coming years.

Shops

# of stores The rise of supermarkets poses threat to artisanal bakeries

14,000 12,454 12,955 13,546 Taiwan’s consumption of baked goods, amounted NT$32,732 million (US$1,061

12,000 11,506 11,998 million) in 2017, is growing slowly at low single digit in next 5 years (Figure 25).

11,053

10,000 Independent and chained artisanal bakeries continue to dominate the distribution of

8,000

baked goods, thanks to their smaller scale of production, which allows for greater

6,000

customization and more-innovative products that are needed in order to stand out in

4,000

2,000 a very competitive sector. However, rising engagement in artisanal baked goods by

0 supermarkets to drive growth, which leverage well-known retail names, marketing

2012 2013 2014 2015 2016 2017 capabilities, and good access to capital, has pose threat to distribution share of

Let's Café (FamilyMart) City Café (PCSC) individual bakeries.

Specialist Coffee Shops Cafés

Source: Company data, Euromonitor

Figure 25 Taiwan Baked Goods Market

NT$ mn CAGR 2.3%

40,000 3%

35,000

2%

30,000

1%

25,000

20,000 0%

2017 2018E2019E2020E2021E2022E

Baked goods Retail Value(LHS)

YoY(%; RHS)

Source: Euromonitor

National Taiwan University 8

Figure 26 Total Store Number Financial Analysis

800 Softer revenue outlook due to peers and cautious development

646 674

580 616 After posting multi-year double-digit revenue growth, GM is now at the crossroad as

600 538 its China business began losing traction. While new entrants utilize online platforms

446 458 467

400 429

to bolster brand equity to gain market shares from brick-and-mortar businesses,

400

deliberate control on delivery service amid fierce competition undermines traditional

200 82

expansion and weighs on per store sales, falling 4%/6%/7% YoY in 2018-20E.

40 55 70

25

0

Furthermore, we believe store addition guidance in China will be revised downward

2016 2017 2018E 2019E 2020E

after the political incident to reflect a more cautious management, and thus forecast

China Taiwan US

a net store addition of 36/30/28 in 2018-20E (Figure 26), lower than the pattern

Source: Company data, Team estimates guided (~40 per year). We forecast revenue in China to falter by 1-2% YoY.

Figure 27 Per Store Sales and YoY Growth Growth momentum in the US remains in our view, thanks to stretched reach into

by Region more Asian clusters. We forecast central kitchens in Northern California and Texas to

NT$ mn complete construction in 4Q18E-1Q18E and 2Q20E-3Q20E respectively, and a net

store addition of 15/15/12 in 2018-20E respectively (Figure 26). We estimate per

100

store sales in the US to falter 12%/11%/9% in 2018-20E and do not see the trend

80

reverse due to competition and cannibalization (Figure 27). Revenue growth in the

60

US will thus moderate to 10% in 2020E from 36% in 2017.

40

20 Topline growth in Taiwan lacks construction catalyst after refurbishment cycle ended

0 in 1Q18, and relatively low customer retention in a very competitive sector bodes ill

for the company. We forecast per store sales to drop 9%/9%/8% YoY in 2018-20E

2018E

2019E

2020E

2018E

2019E

2020E

2018E

2019E

2020E

(Figure 27), dragging revenue in Taiwan by 4%/6%/6% YoY.

US China Taiwan

Source: Company data, Team estimates Deteriorating operating margin in view of selling and marketing cost pressure

Boycott online and offline after the political incident in August put an end to the

Figure 28 OPM by Region significant OPM rally in China since it hit the trough in 2013-14, and 3Q18 OPM came

16.0% 14.4% in at 5% (-7% YoY, -6% QoQ). Unfavorable operating leverage will take time to climb

13.5%

13.5% 13.0% 13.0% 13.0% back to pre-incident level after the resumption of food delivery service in late

12.0% 12.3% 11.0%

10.5% September, but the progress should be slower than company expected (3-6 months),

11.4% 9.3% 8.0% in our view, due to overall economy slowdown and softening consumption demand.

8.0% 8.4% 6.7%

7.0%

Moreover, rising new retail model will disrupt the ongoing OPM recovery, as

8.3%

6.2% competitors accelerate their investment in marketing to build up brand awareness.

6.8%

4.0% 5.2% 4.5% We believe OPM will be deteriorated because of promotional burden to sustain

2017 2018E 2019E 2020E 2021E

market share and thus forecast OPM to be 8.3%/6.8%/5.2% in 2018-20E (Figure 28).

China Taiwan US Overall

Source: Company data, Team estimates High start-up cost and unfavorable capacity utilization will weigh on operating

leverage after GM undertakes central kitchen addition in the US, and thus depress

Figure 29 Capital Expenditure regional OPM before new production base ramps up. 3Q18 OPM came in at 11.5%.

NT$ mn With central kitchens in place in 4Q18E-1Q19E and 2Q20E-3Q20E, we think OPM of

2,500

2,099 these two periods will dip ~2% QoQ as a result. While broadening Asian customer

1,919 1,995

2,000 1,790 base through expansion bodes well for GM’s operating leverage in the near term, we

1,598

1,500 1,331 reason that comparable Asian chained bakery cafés undertaking rapid expansion will

dilute GM’s regional OPM and forecast OPM to be 11.0%/10.5%/8.0% in 2018-20E.

1,000

500 In Taiwan, the wide adoption of franchise model shifts headcount and operating cost

0 burden to franchisees, and hence GM enjoys a relatively more stable and higher OPM.

2016 2017 2018E 2019E 2020E 2021E We expect the trend in Taiwan to continue and forecast a 13% OPM onwards.

Source: Company data, Team estimates

Cash flow analysis

GM has a stable, sufficient cash flow to support its expansion thanks to its retail

business nature, and the cash conversion cycle is -12 days in 3Q18, which represents

a low liquidity risk. Expansion of self-owned stores and central kitchen construction

are the primary capital expenditure items for GM. Capex has increased since 2016 and

we think it will reach a peak in 2018E. Capex will edge lower onwards mainly due to

slower expansion in China, but buildout of another central kitchen in Texas will result

in capex similar to 2019E level (Figure 29).

National Taiwan University 9Figure 30 Risk Matrix Investment Risks

We evaluate the risks of Gourmet Master and describe the impact and likelihood of

investment risks in Figure 30 and Table 8.

Higher GDP growth in China and the US

According to Euromonitor, 2019E GDP growth in China and the US are estimated to

decline by 0.5 ppt to 6.1%/2.4% from 6.6%/2.9% in 2018E (Figure 31). However, if the

trade tension between China and the US eases, a rebound in consumer confidence

will lead to an acceleration in economic activities and GDP growth. In that case, GM

would benefit from both markets and hence generate higher revenue than we expect.

Source: Team estimates

Stronger pricing power in the US

Table 8 Risk Factors and Impact The states of California and Washington claimed minimum wage would increase from

2018 to 2020 at 10% CAGR which would pressure the whole retail industry. To relieve

Risk Impact the impact of increasing wages, the entire industry could raise unit prices. Based on

Benefit from GDP

Higher GDP growth in

growth and hence our research (Appendix 24), GM’s product pricing is lower than that of other

China and the US

increases revenue competitors in the US, which means GM has more room in adjusting its price and

Stronger pricing power keeping competitive advantage. We believe the overall OPM would remain stable with

OPM remains stable

in the US effective pass-through, which would change our forecast of the target price.

High probability of tax Net income

reduction in China increases High probability of tax reduction in China

In September 2018, the Chinese government announced the “Individual Income Tax

Better reported

Appreciation of CNY and Reform,” and it would take effect from 2019. Individual tax exemption has been raised

profit due to

USD against TWD

translation gain to Rmb 60,000 from Rmb 42,000 per year. This new regime affects almost 60 million

Higher-than-expected Momentum for taxpayers to be exempted from individual income tax. To further stimulate the

performance of 3rd future revenue

generation stores growth economy and restore investors’ confidence, the Chinese government is planning to

Source: Team estimates lower levies on enterprises. In the US, tax deductions boosted enterprises’ profits up

16% on average from FactSet research. If the Chinese government dramatically cuts

Figure 31 GDP Growth in China and the US the corporate tax rate in 2019, GM’s net income would rise as a result and affect our

target price (Table 9).

Appreciation of CNY and USD against TWD

As GM uses CNY, USD and TWD as its functional currencies and TWD as its reporting

currency, any significant appreciation in CNY or USD against TWD will drive GM’s

reported profit due to translation gain. Owing to the heating trade war in China, the

exchange rate of CNY/TWD has depreciated since 3Q15 (Figure 32). If the exchange

rate of CNY/TWD changes from depreciation to appreciation in following years (Table

10), GM may report a better profit than our projection. However, since GM manages

all its businesses locally and not by importing from other countries, we believe the

Source: Euromonitor impact of foreign exchange has been minimized.

rd

Figure 32 FX Effect on China's Revenue Higher-than-expected performance of 3 generation stores

Growth GM is currently preparing to launch its 3rd generation remodeling, testing the kiosk

15% 5.1 setups and optimizing ordering processes. If the 3rd generation stores can successfully

5.0 maximize asset utilization and attract more customers, it is highly possible the

10%

4.9

execution of 3rd generation remodeling will become the momentum of future revenue

5% growth.

4.8

0%

4.7

-5% Table 9 Sensitivity of China/US Tax Rate Table 10 Sensitivity of FX Rate against TWD

4.6

-10% US Tax (Federal + State) USD / TWD

4.5

-15% 4.4 NT$ 19% 24% 29% 34% 39% NT$ 29.5 30.5 31.5 32.5 33.5

China Corporate Tax

15% 211 208 205 203 200 4.1 194 193 193 192 192

CNY / TWD

20% 203 200 198 195 192 4.3 192 192 191 191 190

FX Effect Real Growth(QoQ)

25% 195 192 190 187 184 4.5 191 190 190 189 189

CNY/TWD(RHS)

Source: Team estimates 30% 187 184 182 179 177 4.7 189 188 188 187 187

35% 179 176 174 171 169 4.9 187 187 186 186 185

Source: Team estimates Source: Team estimates

National Taiwan University 10Appendix: Table of Contents

Appendix Page

1 Income Statement 12

2 Quarterly Income Statement Forecast 13

3 Balance Sheet 14

4 Cash Flow Statement 15

5 Revenue Forecast by Region 15

6 Operating Margin by Region 16

7 Discounted Cash Flow Analysis 16

8 Corporate Governance 16

9 Five-force Analysis 17

10 Gourmet Master’s Competitors Analysis 18

11 Asian Population Proportion of Select Cities Where 85C Café Operates 19

12 Demographic Breakdown of Gourmet Master Customers in the US 20

13 Asian Population by States in 2017 20

14 The Hierarchy of Drinking Coffee 21

15 Demand for Instant Coffee and Fresh Coffee in China 21

16 Age Breakdown of Luckin Coffee Customers in China 21

17 85C Café in China by Yicai City Tier System 22

18 Taiwan Major Coffee Vendors Membership Program 23

19 Luckin Coffee Promotional/Advertising Program Snapshot 23

20 Financial Statement Forecast Assumptions 24

21 Glossary 25

22 Historical Stock Price Performance Recap 25

23 Chinese Mobile Internet Users 26

24 Average Selling Price (ASP) of Beverage and Baked Goods in the US, 2017 26

25 GM’s 5-yr Forward P/E band 26

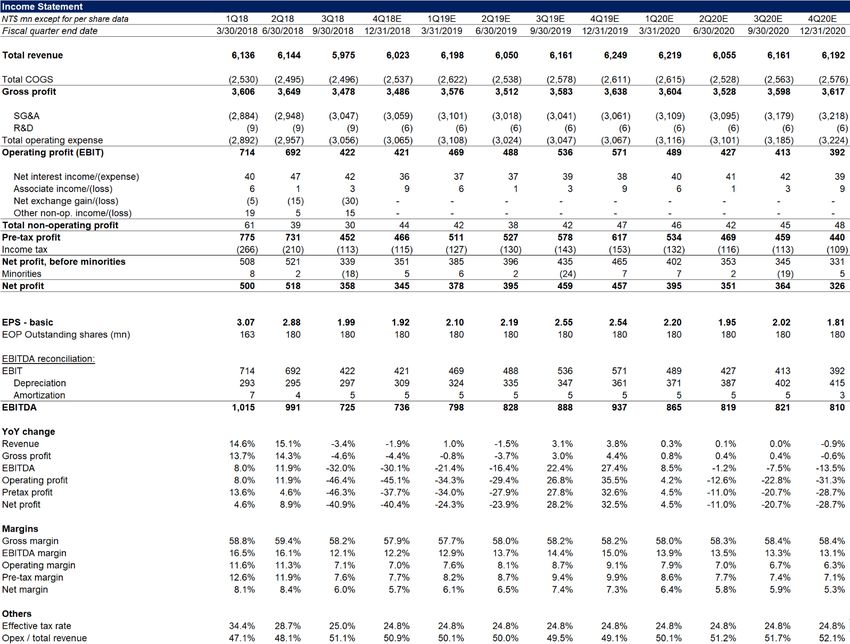

National Taiwan University 11Appendix 1: Income Statement Source: Company data, Team estimates National Taiwan University 12

Appendix 2: Quarterly Income Statement Forecast Source: Company data, Team estimates Source: Company data, Team estimates National Taiwan University 13

Appendix 3: Balance Sheet Balance Sheet NT$ mn except for per share data 2016 2017 2018E 2019E 2020E 2021E 2022E 2023E Fiscal year end date 12/31/2016 12/31/2017 12/31/2018 12/31/2019 12/31/2020 12/31/2021 12/31/2022 12/31/2023 Cash & equivalents 3,151 2,795 2,243 2,716 2,923 3,657 4,645 5,980 Short-term securities 2,448 3,868 3,599 3,599 3,599 3,599 3,599 3,599 Accounts receivables 297 358 331 343 340 337 335 332 Inventory 707 768 697 660 651 643 637 629 Prepaid expense 275 465 436 442 452 449 447 443 Other current assets 137 199 133 137 136 135 134 133 Total current assets 7,015 8,454 7,438 7,898 8,102 8,821 9,797 11,116 Net PP&E 5,058 5,593 6,657 7,209 7,629 7,461 7,100 6,376 Net intangibles 64 46 40 19 - - - - Total long-term investments 418 698 1,243 1,262 1,282 1,301 1,320 1,340 Other long-term assets 882 1,018 897 897 897 897 897 897 Toal non-current assets 6,421 7,354 8,836 9,387 9,807 9,659 9,317 8,613 Total assets 13,436 15,808 16,275 17,285 17,909 18,480 19,114 19,728 Short-term debt 187 1,024 745 745 745 745 745 745 Accounts payable 1,230 1,273 1,185 1,219 1,203 1,188 1,178 1,163 Tax payable 182 176 138 183 130 124 124 123 Accrued expenses 1,262 1,560 1,663 1,665 1,750 1,749 1,744 1,731 Deferred revenue 1,048 1,360 1,415 1,437 1,393 1,350 1,312 1,268 Other current liabilities 27 48 48 50 31 31 37 30 Total current liabilities 3,935 5,441 5,195 5,298 5,251 5,188 5,138 5,060 Long-term debt 615 155 159 159 159 159 159 159 Other long-term liabilities 218 285 449 449 449 449 449 449 Total liabilities 4,768 5,881 5,802 5,906 5,859 5,795 5,746 5,668 Share capital 4,163 4,163 4,170 4,170 4,170 4,170 4,170 4,170 Retained earnings 4,523 5,920 6,656 7,570 8,247 8,888 9,577 10,275 Other common equity (95) (228) (381) (381) (381) (381) (381) (381) Total common equity 8,590 9,855 10,445 11,359 12,036 12,676 13,366 14,064 Minority interest 77 72 28 19 14 8 3 (3) Total shareholders' equity 8,668 9,927 10,472 11,379 12,050 12,685 13,369 14,061 Total liabilities & equity 13,436 15,808 16,275 17,285 17,909 18,480 19,114 19,728 Days sales outstanding, DSO 5 6 5 5 5 5 5 5 Days of inventory, DIO 28 30 25 23 23 23 23 23 Days payables outstanding, DPO 49 50 43 43 43 43 43 42 Cash conversion cycle, CCC (16) (14) (13) (15) (15) (15) (15) (14) Source: Company data, Team estimates National Taiwan University 14

Appendix 4: Cash Flow Statement Cash Flow Statement NT$ mn except for per share data 2016 2017 2018E 2019E 2020E 2021E 2022E 2023E Fiscal year end date 12/31/2016 12/31/2017 12/31/2018 12/31/2019 12/31/2020 12/31/2021 12/31/2022 12/31/2023 Net Profit 1,742 2,138 1,721 1,689 1,437 1,287 1,269 1,269 Minorities add-back 41 17 (2) (8) (5) (6) (6) (6) Depreciation 1,133 1,078 1,195 1,366 1,575 1,765 1,937 2,093 Amortization 36 32 22 21 19 - - - Associate (income)/loss (19) (23) (19) (19) (19) (19) (19) (19) Net (inc)/dec in working capital 339 294 227 118 (43) (49) (38) (61) Other non-cash items 14 (57) 696 - - - - - Cash flow from operations 3,285 3,479 3,839 3,166 2,963 2,978 3,142 3,276 Capital expenditure (1,331) (1,790) (2,099) (1,919) (1,995) (1,598) (1,575) (1,370) ST securities (1,271) (1,627) (432) - - - - - LT securities (1) (0) (652) - - - - - Other items 50 (58) 94 - - - - - Cash flow from investments (2,553) (3,474) (3,090) (1,919) (1,995) (1,598) (1,575) (1,370) Cash dividends paid (353) (741) (978) (775) (760) (646) (579) (571) Equity issuance/(repurchase) - - - - - - - - Debt issuance/(paydown) (83) 365 (431) - - - - - Other items (72) 52 107 - - - - - Cash flow from financing (508) (324) (1,301) (775) (760) (646) (579) (571) Total cash flows 225 (319) (552) 473 207 734 988 1,335 FX impact (129) (37) 0 - - - - - Net change in cash 96 (357) (552) 473 207 734 988 1,335 Cash balance, BOP 3,055 3,151 2,795 2,243 2,716 2,923 3,657 4,645 Cash balance, EOP 3,151 2,795 2,243 2,716 2,923 3,657 4,645 5,980 Source: Company data, Team estimates Appendix 5: Revenue Forecast by Regions Source: Company data, Team estimates National Taiwan University 15

Appendix 6: Operating Margins by Regions

20%

15%

10%

5%

0%

2017 2018E 2019E 2020E 2021E

-5%

-10%

-15%

-20%

China Taiwan US Others Overall

Source: Company data, Team estimates

Appendix 7: Discounted Cash Flow Analysis

DCF calculation

Fiscal year 2019E 2020E 2021E 2022E 2023E

Fiscal year end date 12/31/2019 12/31/2020 12/31/2021 12/31/2022 12/31/2023

EBIT 2,064 1,721 1,513 1,467 1,437

Less: EBIT x tax rate (511) (426) (374) (363) (356)

NOPAT 1,553 1,295 1,138 1,104 1,081

Add: Depreciation 1,366 1,575 1,765 1,937 2,093

Add: Amortization 21 19 - - -

Less: Increase/(decrease) in net working capital 118 (43) (49) (38) (61)

Less: Capital expenditure (1,919) (1,995) (1,598) (1,575) (1,370)

Free cash flow to firm 1,139 851 1,256 1,427 1,744

% growth -25% 48% 14% 22%

Terminal value 31,227

Total FCFF 1,139 851 1,256 1,427 32,970

Discount time factor - 1.0 2.0 3.0 4.0

Discounted FCFF 1,139 794 1,094 1,159 24,995

Source: Company data, Team estimate

Appendix 8: Corporate Governance

1. Shareholder Structure

The top 10 shareholders account for 57.8%, in which 90% is insider related.

Holding %

Infinity Emerging Markets Limited 23.0

Wu Cheng-Hsueh (Chairman) 14.5

Henderson I Yield Growth 8.8

Zhang Hua Ting 1.9

Karst Peak Asia Master Fund 1.9

Zhang Hua Ting Trust Account 1.8

Zhang Hua Ting Trust Account 1.8

Buena Vista Opportunities Master Fund Ltd. 1.6

Macquarie Asia New Stars Fund Investment Account 1.3

Macquarie Asia New Stars Fund 1.3

Top 10 Total 57.8

Management Total 14.5

Director Total 46.3

Source: Company data

National Taiwan University 162. Corporate Governance

The table summarizes Gourmet Master’s governance in corporate. Peer companies include Breadtalk, President Chain Store and

La Kaffa. It is clearly that Gourmet Master operates in a relatively small group of management with longer tenure and controlling

directors with significant shareholdings. In terms of executives’ and directors’ remuneration, even though under a robust growth

in recent years, total salary and directors’ fee remain stable.

Gourmet Master Peer Companies

Executives

Number of Executives 5 10

Average Tenure (Years) 7 5

Remuneration (% of net profit before tax) 0.6 6.3

Board Members

Number of Board Members 7 10

Directors Owing Shares 3 4

Shares Held (%) 46.3 26.3

Non-employee Directors 3 8

Average Meeting Attendance % 97.1 90.4

On Board of Other Companies 3 3

Average Tenure (Years) 5 7

Remuneration (% of net profit before tax) 1.0 3.4

Source: Company data

Appendix 9: Five-force Analysis

Threat of New Entrants

5

4

3

2 Bargaining Power of

Threat of Substitute Products

1 Suppliers

0

Bargaining Power of

Competition in the Industry

Customers

Source: Team estimates

Bargaining Power of Suppliers: Global demand and supply affect the price of raw ingredients

Historically, Gourmet Master has a steady gross margin, thanks to diversified local procurement strategy. Considering the jump in

gross profit margin to 58% in 3Q18, from 52% in 1Q10, and variance less than 2 ppts QoQ, we estimate 1 point in “Bargaining

Power of Suppliers.”

Competition in the industry:

Gourmet Master’s competitors in the US and China are ambitious on their store expansion plan. For example, Paris Baguette aims

to run 300+ stores in the US by 2020, and Tous Les Jour targets 1,000 stores in China. Based on the faltering PSD of Gourmet Master

stemming from simultaneous aggressive expansion of Breadtalk as well as other local peers in China within 2012 and 2014, we

ration that the expansion of Paris Baguette and Tous Les Jour should significantly weigh on the performance of Gourmet Master

and thus assign 5 points to “Competition in industry.”

Bargaining Power of Buyers:

Myriads of alternatives are on shelves for bread and coffee in Greater China, ranging from tea to steamed buns, in our view, and

the availability of choices cause consumers to be sensitive to price hike. Therefore, Gourmet Master launches new products every

quarter to differentiate their products so as to minimize consumer’s price sensitivity and bargaining power. However, since

Gourmet Master has positioned itself at competitive pricing, it is fairly difficult for the company to embrace higher price while

keeps the original customer base in Greater China. As a result, we estimate 3 points in “Bargaining Power of Buyers.”

National Taiwan University 17Threat of Substitutes: Although there are many substitutes for baked goods and coffee, such as pastries, tea, and soft drinks, the substitution effect on the products of Gourmet Master should be smaller than that of pure beverage providers or bakeries, thanks to the company’s one- stop feature. We hence assign 2 points to “Threat of Substitutes.” Threat of New Entrants: Many Chinese new entrants show up and heighten the competition in China due to low enter barriers in the bakery and coffee industry. Some latecomers opt to leverage e-Commerce channels or trigger price war to nibble market share, on the back of venture capital funding. Moreover, low entry barriers and huge pent-up demand in the US market not only attract international bakery and café brands, but also entice small-sized bakery players to join the hunt for economic profit. New entrants are emerging threats to Gourmet Master, but Gourmet Master’s first-mover advantage and centralized production, which in turn brings economies of scale, could still create a few edges. We estimate 3 points in “Threat of New Entrants.” Appendix 10: Gourmet Master’s Competitors Analysis Paris Baguette: Headquarter: Seongnam, South Korea Paris Baguette is a bakery brand under the SPC Group, a large food chain in South Korea. It specializes in French bread, sandwiches, cakes, coffee, and etc. Currently, it owns more than 6,000 chain stores in Korea, the US, France, China, Singapore and Vietnam. Paris Baguette attempts to increase its US exposure by a store unit objective of 300+ in 2020E. Paris Baguette’s expansion strategy would bring threat to Gourmet Master in light of the similarity of these two companies on price positioning and store type (bakery café) in the US. BreadTalk: Headquarter: Singapore Breadtalk is a brand under BreadTalk Group (BREAD SP), whose business segments include bakery, restaurants, and food atrium. For its bakery business, it currently operates more than 950 stores in 17 countries, 48% of which are in Singapore. BreadTalk is a direct competitor for Gourmet Master in China because a large proportion of its stores worldwide is located in China (32%) and Hong Kong (11%), and they both exhibit high similarity in terms of site selection. Furthermore, when Gourmet Master accelerated its stretch into China during 2012-14, BreadTalk’s simultaneous expansion indeed exerted crowding out effect on Gourmet Master. Panera Bread: Headquarter: Missouri, USA Panera Bread is a chained bakery café/fast casual restaurants in the US and Canada. Product offerings include soups, salads, pasta, sandwiches, specialty drinks, and baked goods. The company was listed on NASDAQ exchange (Before delisted: PNRA US) before an equity buyout led by JAB Holding Company, a German private equity fund in consumer field, in 2017. Panera current has over 2,000 locations in the US. In May 2018, Panera Bread announced that it would now provide nationwide delivery service at all stores in the US. Tous Les Jour: Headquarter: Seoul, South Korea Tous Les Jours is a South Korean bakery franchise owned by CJ Foodville, a subsidiary of CJ Group (001040 KS). Tous Les Jours is an "Asian-French" bakery serving a selection of bakery goods and beverages. It has more than 1,300 branches in Asia and the US. City Café: Headquarter: Taipei, Taiwan City Café is a coffee brand owned by President Chain Store Corporation (PCSC, 2912 TT), a convenience store operator, and sells quality fresh coffee at a relatively lower price than others. PCSC now owns more than 5,000 stores in Taiwan, and its density is much higher than convenience store players (c.50% in market share term by unit). On top of coffee, City Café also makes inroads into tea drink market in order to offer customers with more beverage choices. McCafé: Headquarter: Illinois, USA McCafé is a coffee-house-style food and beverage brand, owned by the fast food conglomerate McDonald's (MCD US), and runs together with fast food restaurants. Currently, McDonald’s has over 35,000 stores worldwide, and it plans to add 2,000 more restaurants in China over next five years. McCafé poses a direct threat to Gourmet Master, given similar competitive pricing strategy and high store visibility. National Taiwan University 18

Louisa Coffee:

Headquarter: Taipei, Taiwan

Founded in 2006 by Ming Xian (Chris) Huang, Louisa Coffee is a coffee specialist shop brand in Taiwan. Louisa offers budget coffee

at premium quality as well as fresh food in order to cater customers’ appetite. The brand now eyes a store number target of 400

by the end of 2018, which will put itself behind 85C Café and Starbucks in Taiwan. Apart from membership program, Louisa also

addresses “lifestyle” by introducing different concept stores, such as library-alike and workspace-oriented, to bolster customer

loyalty.

Let’s Café:

Headquarter: Taipei, Taiwan

Similar to City Café, Let’s Café is also a chained coffee brand owned by the convenience store operator, FamilyMart (5903 TT),

which now runs at more than 3,000 locations in Taiwan. Business strategy of Let’s Café is akin to City Café as well, by providing

fresh quality coffee at competitive price and leveraging the high visibility of FamilyMart to lower customer acquisition cost. In

addition, Let’s Café taps into tea drink segment through cooperation with Twinings, a British tea marketer.

Starbucks:

Headquarter: Seattle, USA

Starbucks (SBUX US) is the biggest coffeehouse company in the world which has more than 28,000 stores in operation across 75

countries by the end of 2017. Its main products include coffee, tea and bakery goods. Among all the coffee brands mentioned,

Starbucks is the brand enjoying the highest price and brand equity.

Luckin Coffee:

Headquarters: Beijing, China

Luckin Coffee, founded in 2017 by Zhiya (Jenny) Qian, is representative of China’s “new retail” model, thanks to cheap delivery and

prevalence of online ordering in China. With more than 660 stores opened in 13 provinces within just a few months, it is now the

second largest coffee brand in China and a powerful threat to Starbucks and other coffee brands. Luckin completed a GIC-led Series

A funding worth of $200 million in June 2018 and joined “unicorn”, the start-up hall of fame, at $1 billion post-money valuation.

The company has been utilizing strong capital support to propel breakneck expansion via frequent online promotional activities.

RTD (Ready-to-drink coffee):

RTD refers to packaged coffee sold in stores and is prepared ready for consumption. The global RTD coffee market is expected to

reach $9.7 billion in 2018. RTD coffee are distributed mainly through modern trade channels, such as supermarkets and

convenience stores, and the brand equity of it is relatively lower.

In conclusion, Gourmet Master is now facing mounting competition pressure from other players: 1) Paris Baguette, Tous Les Jour

and Panera in the US; 2) McCafé, Luckin and BreadTalk in China; 3) City Café, Let’s Café, and Louisa Coffee in Taiwan.

Appendix 11: Asian Population Proportion of Select Cities Where 85C Café Operates

Cupertino Milpitas Cerritos Daly City Alhambra

(CA) (CA) (CA) (CA) (CA)

63.5% 61.8% 61.0% 58.4% 52.0%

Irvine Garden Grove Torrance Hacienda Heights San Jose

(CA) (CA) (CA) (CA) (CA)

43.3% 38.6% 38.2% 36.8% 34.5%

Cypress Chino Hills Buena Park Gardena Newark

(CA) (CA) (CA) (CA) (CA)

31.7% 30.7% 28.0% 27.8% 26.7%

Fullerton Berkeley Sacramento Plano National City

(CA) (CA) (CA) (TX) (CA)

24.0% 22.8% 21.2% 18.2% 17.8%

Glendale Bellaire Richardson Balboa Mesa Pasadena

(CA) (TX) (TX) (CA) (CA)

15.9% 15.4% 15.1% 14.7% 14.4%

Los Angeles Mira Mesa Korea Town West Covina Tukwila

(CA) (CA) (CA) (CA) (WA)

12.8% 44.3% 32.2% 25.6% 16.6%

Source: Company data, US Bureau of Labor Statistics

National Taiwan University 19You can also read