The Big Picture 2019 outlook: war, inflation, recession? Quarterly update For professional/qualified/accredited investors only - Invesco Europe

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Big Picture 2019 outlook: war, inflation, recession? Quarterly update For professional/qualified/accredited investors only 18 November 2018 Data as of 31/10/18 unless stated otherwise

The Big Picture

2019 outlook: war, inflation, recession?

In considering the outlook for 2019 we take a step back and analyse the long-term backdrop.

This reaffirms an ongoing preference for equity-like assets despite diminished long-term

growth potential. Events that typically cause a divergence from that path are: war, inflation

and/or recession. Though all are possible during 2019 (we assign a 25% probability to

recession), our central scenario remains one of modest global growth and inflation. This

leaves us expecting better returns on equity-like assets but we examine alternative scenarios.

Model asset allocation

In our view:

Equities offer good returns but are volatile and correlated to other assets. We remain slightly Underweight.

Real estate has the potential to produce the best returns. We stay at Maximum.

Corporate high-yield (HY) now looks more interesting. We remain Overweight.

Corporate investment-grade (IG) preferred to government debt. We remain Overweight.

Government debt better than it was but still unattractive. We remain Underweight.

Emerging markets (EM) is still the sovereign space with the best potential. We stay at Maximum.

Cash returns are low but stable and de-correlated. We stay at Maximum.

Commodities have not bottomed. We remain Zero-weighted.

No currency hedges.

Assets where we expect the best returns

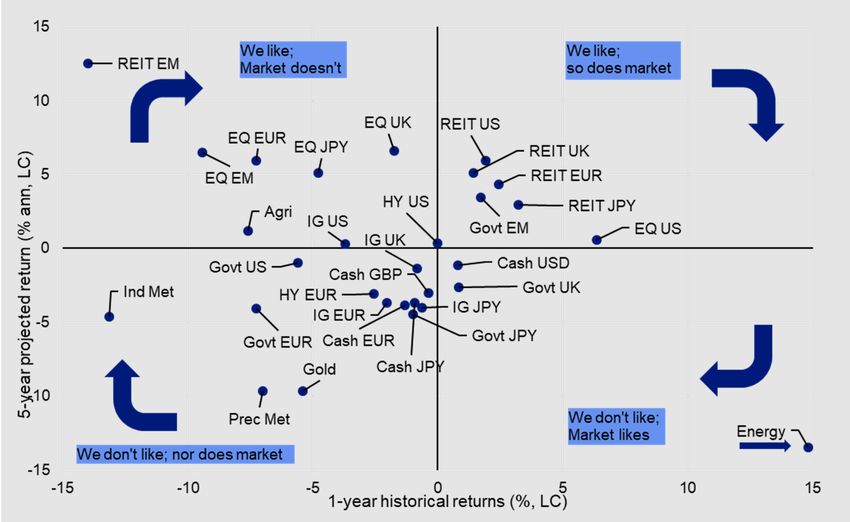

Japanese equities – estimated 15% 5yr annualised total return in USD

EM real estate – estimated 14% 5yr annualised total return in USD

US IG – estimated 4% 5yr annualised total return in USD

USD cash – estimated 3% 5yr annualised total return in USD and good in a crisis

Figure 1 – Projected 5-year returns for global assets and neutral portfolio

12% 1.2

10% 1.0

8% 0.8

6% 0.6

4% 0.4

2% 0.2

0% 0.0

-2% -0.2

-4% -0.4

Returns Risk-Adjusted (RHS)

-6% -0.6

Returns are annualised in local currency. Risk-adjusted returns are projected returns divided by historical 5y standard deviations. See

appendices for definitions, methodology and disclaimers. There is no guarantee that these views will come to pass. Source: Invesco

November 2018 For professional/qualified/accredited investors only 1

Table of contents Summary and conclusions: war, inflation, recession? ....................................................................................... 3 Model asset allocation ............................................................................................................................................ 5 The long-term outlook............................................................................................................................................. 6 Medium term issues ............................................................................................................................................... 8 The outlook for 2019: war, inflation, recession? ................................................................................................ 10 A year in politics – hard to imagine war ............................................................................................................... 10 The risk of higher inflation .................................................................................................................................... 12 No recession in 2019 ........................................................................................................................................... 13 We need to talk about Jerome ............................................................................................................................. 17 Farewell Mario (and Mark); welcome Yi .............................................................................................................. 19 Behind the projections -- valuations remain a limiting factor ............................................................................... 20 The US equity conundrum ................................................................................................................................... 21 Projections for 2019 and beyond ......................................................................................................................... 23 Optimisation favours cash and real estate........................................................................................................... 24 Hope versus reality .............................................................................................................................................. 26 Sectors ................................................................................................................................................................. 27 What if we are wrong? Five scenarios for 2019 ................................................................................................. 28 Model Asset Allocation: adding to UK; reducing EM ........................................................................................ 30 Where do we expect the best returns? ............................................................................................................... 32 Appendices ............................................................................................................................................................ 33 Appendix 1: Consensus economic forecasts ....................................................................................................... 33 Appendix 2: Global valuations vs history ............................................................................................................. 34 Appendix 3: Asset class total returns................................................................................................................... 35 Appendix 4: Expected returns (%) ....................................................................................................................... 36 Appendix 5: Key assumptions ............................................................................................................................. 37 Appendix 6: Optimised allocations for global assets for different currency bases .............................................. 38 Appendix 7: Methodology for asset allocation, expected returns and optimal portfolios ..................................... 40 Appendix 8: Sector multiple regression model methodology............................................................................... 41 Appendix 9: Definitions of data and benchmarks ................................................................................................ 42 Important information ........................................................................................................................................... 44 November 2018 For professional/qualified/accredited investors only 2

Multi-asset research

The Big Picture

Summary and conclusions: war, inflation, recession?

Another tough year 2018 has been a difficult year and we expect more of the same in 2019. However, we

ahead but we expect expect neither war, rapid inflation nor recession and therefore believe equity-like assets

equity-like assets to

will stay on their outperforming trend. Among such assets we enter the new year

continue outperforming

Overweight real estate and high-yield (HY) but slightly Underweight equities (entirely

because of the US). We are also Overweight investment-grade credit (IG), which we

expect to produce better medium term returns than government debt (Underweight). We

remain fully allocated to cash and zero-weighted to commodities (including gold).

Will long-term equity risk Over the very long-term our analysis suggests that equities have outperformed other

premium continue? assets by quite a large margin (we suspect the same applies to real estate) and we see

no evidence that they are out of line with those long-term trends. Reasons to expect a

different outcome could include a belief that long-term growth potential is lower than it

was or that a short-term shock could provoke an equity bear market.

Growth potential is We do believe that long-term growth potential is diminished (demographics, debt and

diminished but equity-

impotent central banks) and allow for this in our forecasts. Nevertheless, our five-year

like assets still expected

to offer best returns projections still suggest the best returns will accrue to real estate and equities, with those

on fixed income assets broadly close to zero (especially in the eurozone and Japan).

We expect negative returns on commodities (except agriculture). See Figure 1.

2019 threats Shortening the time horizon to 2019, our research suggests that equity bear markets are

often associated with war, inflation and/or recession. The good news is that we expect

neither but the risks are growing.

War?

War could be provoked by a worsening of geopolitical tensions and potential flashpoints

include the Ukrainian presidential election at end-March (given the tensions with Russia

and the potential for Western involvement if Russia intervenes). Though we believe the

belligerent attitude of President Trump has doubled the risk of a serious military conflict

somewhere in the world, we put the probability at only 20% (versus the normal 10%)

Ciao Mario, hello Yi ECB President Mario Draghi will be replaced in November and Mark Carney’s successor

at the BOE should be known by year-end. But, PBOC Governor Yi Gang could become

increasingly important to global markets: can the PBOC offset the negative effect of

declining QE activity among developed world central banks?

Inflation? Indeed, we think it probable that core inflation, interest rates and bond yields will rise

during 2019. This will reduce fixed income returns (we expect negative returns on many

eurozone and Japanese bonds over one and five-year horizons). However, we do not

expect this to-spill over into equity markets: the correlation between US equities and

bond yields remains largely positive, the tipping point is often a 10-year yield around 5%.

Recession? We think Recession could change all of that. The risk is growing by the day and we put the

not

probability at 25%, versus 15% a year ago. However, we are encouraged by US profit

and investment spending trends and do not believe that Fed policy is yet restrictive. We

suspect that global GDP growth will ease to 3% during 2019 (from 3.6% in the year to

mid-2018). If this is correct, we believe it will be enough to keep equity-like assets in

outperforming mode. Our US equity bear market indicator is currently 65%, the wrong

side of normal (50%) but below the 75%-80% that would scare us (see Figure 28).

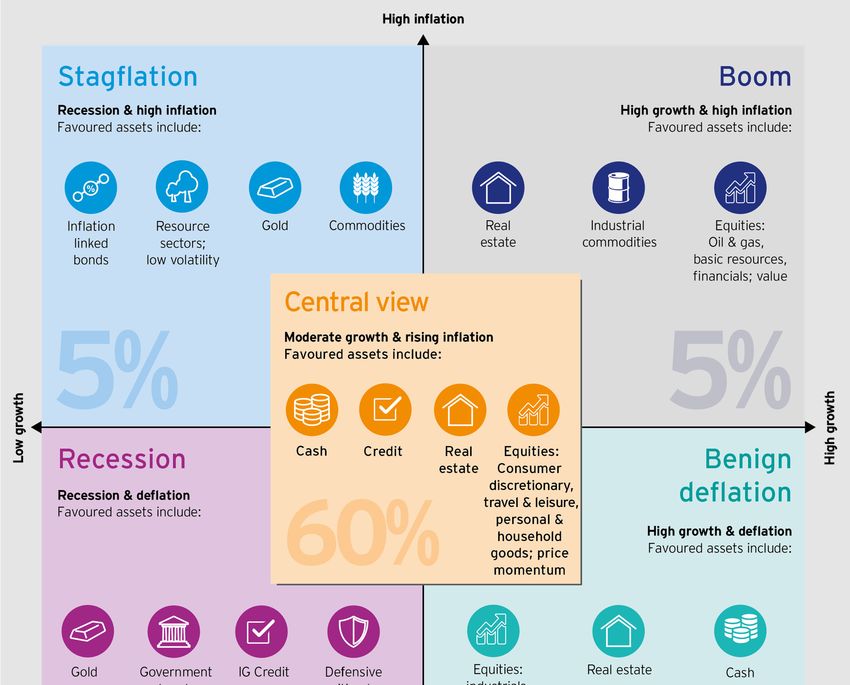

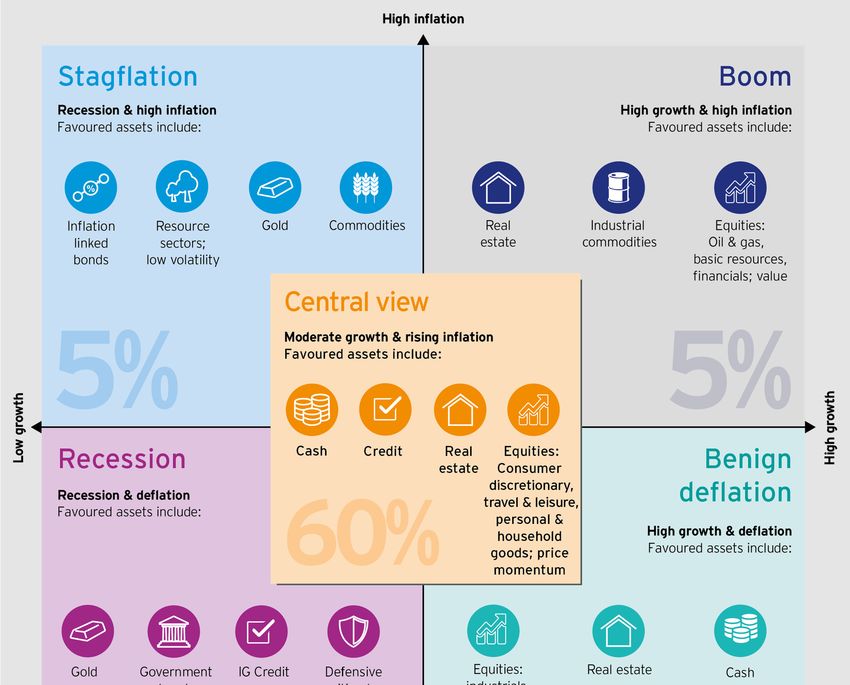

What if we are wrong? Of course, we may be wrong. As suggested by Figure 2 we assign a probability of 60%

to that central scenario, 25% to recession and 5% to each of boom, benign deflation and

stagflation. The growing risk of recession is one reason to listen when our optimiser tells

us to be Underweight equities (we implement this by being Underweight US equities –

see Figure 3). We also hold the most cash that we allow ourselves but continue to give

the maximum allocation to real estate and are Overweight HY (though only in the US).

Among less volatile fixed income assets, we prefer IG (Overweight) to government debt

(Underweight) and remain zero-weighted in commodities (since they are broadly well

above historical norms in real terms).

November 2018 For professional/qualified/accredited investors only 3

Multi-asset research

The Big Picture

No big asset allocation We make no changes to the broad asset class allocations but are making some

changes but adding to adjustments within the various groups. We are adding to UK equities and UK real estate

UK and slightly reducing (taking them to Neutral on the belief that a lot of Brexit bad news is in the price). We are

EM equities also adding to Japanese equities on the back of strong earnings and dividend growth,

taking them to the maximum allowed, financed by reducing Japanese real estate to zero.

The financing of UK additions is achieved by reducing the extent of the Overweight in

EM equities (EPS growth has stalled).

Our diversified selection of four assets where we expect good returns during 2019 is:

EM real estate, Japanese equities, US IG and USD cash.

Figure 2 – Five scenarios for 2019 and our favoured assets (percentages reflect assigned probabilities)

See appendices for definitions, methodology and disclaimers. Source: Invesco

November 2018 For professional/qualified/accredited investors only 4

Multi-asset research

The Big Picture

Model asset allocation*

Figure 3 – Model asset allocation (18/11/2018)

Neutral Policy Range Allocation Position vs Neutral Hedged Currency

Cash 5% 0-10% 10%

Cash 2.5% 10%

Gold 2.5% 0%

Bonds 45% 10-80% 44%

Government 30% 10-50% 20%

US 10% 14%

Europe ex-UK (Eurozone) 8% 0%

UK 2% 2%

Japan 8% 0%

Emerging Markets 2% 4%

Corporate IG 10% 0-20% 16%

US Dollar 5% 10%

Euro 3% 2%

Sterling 1% 2%

Japanese Yen 1% 2%

Corporate HY 5% 0-10% 8%

US Dollar 4% 8%

Euro 1% 0%

Equities 45% 20-70% 40%

US 25% 8%

Europe ex-UK 7% 13%

UK 4% ↑ 4%

Japan 4% ↑ 8%

Emerging Markets 5% ↓ 7%

Real Estate 3% 0-6% 6%

US 1% 2%

Europe ex-UK 1% 1%

UK 0.5% ↑ 1%

Japan 0.5% ↓ 0%

Emerging Markets 0% 2%

Commodities 2% 0-4% 0%

Energy 1% 0%

Industrial Metals 0.3% 0%

Precious Metals 0.3% 0%

Agriculture 0.3% 0%

Total 100% 100%

Currency Exposure (including effect of hedging)

USD 49% 47%

EUR 21% 18%

GBP 8% ↑ 10%

JPY 14% 11%

EM 7% ↓ 14%

Total 100% 100%

*This is a theoretical portfolio and is for illustrative purposes only. It does not represent an actual portfolio and is not a recommendation of any

investment or trading strategy. Cash is an equally weighted mix of USD, EUR, GBP and JPY. Currency exposure calculations exclude cash.

Arrows show direction of change in allocations. See appendices for definitions, methodology and disclaimers. Source: Invesco

November 2018 For professional/qualified/accredited investors only 5

Multi-asset research

The Big Picture

The long-term outlook

Equities outperform over Investment is a simple process if we don’t try to predict every twist and turn in markets.

the long-term. Can we

Over the very long-term equities (stocks) and real estate tend to outperform fixed income

find reasons why that

may not be the case in assets, while commodities give the same return as bonds but with the same volatility as

the future? stocks (see Figure 4). If we were to draw an efficient frontier it would run from cash to

stocks, with investment-grade grade credit (IG) the closest of the other assets shown.

Not surprisingly, and as we outlined in Asset allocation in pictures (November 2017),

optimal portfolios based on this data set would be dominated by stocks, IG and cash (the

exact balance depending on one’s appetite for risk).

Figure 4 – Risk and reward on US assets 1915-2017 (CPI adjusted, %) *

*Based on calendar year data from 1915 to 2017. Area of bubbles is in proportion to average correlation with

other assets. Calculated using: spot price of gold, Global Financial Data (GFD) US Treasury Bill total return

index for cash, our own calculation of government bond total returns (Govt) using 10-year treasury yield, GFD

US AAA Corporate Bond total return index (IG), Reuters CRB total return index until November 1969 and then

the S&P GSCI total return index for commodities (CTY) and Robert Shiller’s US equity index and dividend data

for stocks. Indices are deflated by US consumer prices. Past performance is no guarantee of future results.

Source: Datastream, Global Financial Data, Reuters CRB, S&P GSCI, Robert Shiller, Invesco

Surprisingly, US equities The problem with such an analysis is the critical importance of the start and end-dates.

do not seem out of line Equities may look so good in Figure 4 simply because they are at the end of an

with long-term trends.

unsustainable bull-run. Figure 5 offers some evidence that US equities are not out of

line with long-term trends, while the commodities bubble seems to have deflated.

Figure 5 – US real total return indices (Sep 1914 = 100, logarithmic scale) *

*30/09/1914 to 31/10/2018. Calculated using: spot price of gold, Global Financial Data (GFD) US Treasury Bill

total return index for cash, our own calculation of government bond total returns (Govt) using 10-year treasury

yield, GFD US AAA Corporate Bond total return index (IG), Reuters CRB total return index until November

1969 and then the S&P GSCI total return index for commodities (CTY) and Robert Shiller’s US equity index

and dividend data for stocks. Indices are deflated by US consumer prices. Past performance is no guarantee

of future results. Source: Datastream, Global Financial Data, Reuters CRB, S&P GSCI, Robert Shiller, Invesco

November 2018 For professional/qualified/accredited investors only 6

Multi-asset research

The Big Picture

But there are good Looking for reasons why our long-term projections could differ from that historical

reasons to suppose precedent, there are some structural issues that we believe could depress growth and

long-term growth inflation, thereby weakening the prospects for equities and real estate:

potential is not what it

was

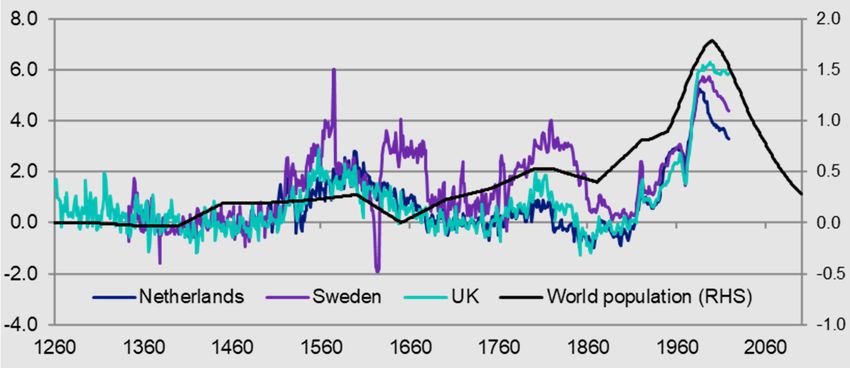

Global demographics were extremely favourable in the fifty years that followed

WW2, with population growth at levels not seen in the post-1000 era (see Figure 6).

As we discussed in Pictures of distress, we believe this supported global economic

growth and boosted inflation (as hinted at in Figure 6). Now that population is

decelerating in most countries and regions, we believe economic growth and

inflation will be lower than during the post-war era. Hence, we assume that dividend

and rental growth will be lower than in recent decades but also that central bank

interest rates and bond yields will be lower.

Debt is now so high that we suspect it will be a constraining factor, whereas prior to

the financial crisis the accumulation of debt supported growth in many parts of the

world (for instance, the BIS estimates that US debt/GDP doubled from 125% in 1953

to 251% in 2017). As we have explained on many occasions, we believe that debt is

largely a developed world problem, with most emerging economies enjoying much

lower debt ratios (China and South Korea being obvious exceptions). See The

stabilisation of global debt.

Full normalisation of central bank polices will not have occurred until interest rates

are more in line with economic fundamentals and balance sheets have returned to a

more normal level in relation to GDP. History suggests this will be a multi-decade

process and we see no reason to expect otherwise this time around (with retreat

away from normalisation during periods of recession). We believe that such

normalisation will represent an ongoing drag on economies and financial markets.

Most major central banks have been running extreme policies since the financial

crisis and would appear to have exhausted much of their ability to offset the next

recession. The PBOC is a notable exception, with plenty of scope to loosen policy in

an economy where there is abundant demand for credit. Among developed world

central banks that have used extreme policies, the US Fed is perhaps the only one

that has built up some cushion to loosen policy when the next recession arrives,

though it is still operating with a bloated balance sheet. The BOE, BOJ, ECB and

SNB risk impotence during the next recession. This, added to the high level of

government debt in many countries suggests that policy makers will find it difficult to

offset a big recession, which should dampen our long-term growth forecasts.

Figure 6 – World population growth and consumer prices in selected countries

(annualised rolling 50-year changes, %)*

*Annual data from 1260 to 2100. Historical world population data comes from Global Financial Data. Forecast

population data (from 2015) is an interpolation of United Nations forecasts (which is in five year intervals).

Consumer price indices supplied by Global Financial Data and the rolling 50-year changes end in 2018 and

start in 1260 (UK), 1340 (Sweden) and 1500 (Netherlands). Source: Global Financial Data, United Nations and

Invesco

November 2018 For professional/qualified/accredited investors only 7

Multi-asset research

The Big Picture

Our long-term growth Our long-term interest rate and growth assumptions take account of the above factors

assumptions are but we otherwise assume a large degree of convergence to historical norms (credit

reduced accordingly, as spreads, default rates, real commodity prices, real exchange rates etc.).

are our inflation and

policy rate forecasts

Another long-term factor will be the impact of technology such as robotics and

automation. We do not believe that unemployment will increase as result of such

innovations: after all, there have been many technological revolutions over the centuries

(agricultural and industrial) and despite concerns at the time, labour was always re-

deployed to other uses. It is not hard to imagine periods during which there could be

disruption in the labour market and a short-term rise in unemployment but history

suggests that new jobs will eventually appear.

The greater question for us is whether these technological advances will bring a leap in

total factor productivity. For the moment, any such enhancement is hard to detect but,

should it arrive, it could take long-term growth above our assumptions. To be seen.

Medium term issues

We assume there will be Shortening the time horizon, we assume there will be a recession in the next two to three

recession in the next two years. When that recession comes it is easy to think of factors that could aggravate it:

to three years and it

could be deep.

First, the above mentioned high levels of debt could render economies more

vulnerable, with recession provoking abnormal levels of default.

Second, as already mentioned, central banks may find themselves unable to play

their usual stabilising role. The same could be said for governments

Third, If the common perception about the fragility of the Chinese economy proves

correct, this would have a negative effect on the global economy.

Finally, in the absence of fiscal union, we believe eurozone countries are vulnerable

to speculative attack during recession, which could endanger the eurozone and EU.

History suggests the US

It is hard to know the medium-term stock market implications of the US mid-term

political backdrop will elections. Markets do not usually like congressional gridlock (Figure 7 shows that

not favour equities over Republican presidents confronted by a mixed Congress are associated with poor stock

the coming years (after market returns – note that the first two years of President Trump’s term followed the

the mid-terms) usual pattern of strong returns for a president with a friendly Congress).

Figure 7 – Annualised US equity gains during US presidencies since 1853 by type

of Congress (%)*

* Based on the S&P 500 index since 1957 and comparable indices as derived by Robert Shiller prior to that

(see details in Appendix 8). The analysis starts at the beginning of the presidency of Franklin Pierce on 04

March 1853 and ends on 06 November 2018 (the date of the recent mid-term elections). “Friendly Congress” is

when both houses are of the same party as the president; “Weak Friendly Congress” is when both houses

support the President for most of his full term; “Mixed Congress” is when both parties have an equal stake in

Congress; Weak Hostile Congress” is when both houses are predominantly against the president and “Hostile

Congress” is when both houses are against the president throughout his term. Past performance is no

guarantee of future results. Source: 270towin, Robert Shiller, Global Financial Data, Bloomberg, Datastream,

Wikipedia and Invesco

November 2018 For professional/qualified/accredited investors only 8

Multi-asset research

The Big Picture

The initial market reaction after the elections was positive, perhaps in the belief that

there may now be less action from President Trump. Time will tell whether this is a good

or a bad thing.

Our five-year return

projections suggest real

estate and equities offer

Taking the above into account, we formulate five-year projections for interest rates,

the best medium-term yields and the growth of dividends and rentals. We then generate five-year expected

potential, though cash returns for each asset class. Figure 8 shows a summary of the results, with the full

and credit categories regional detail shown in Appendix 4 and assumptions in Appendix 5.

look good on a risk-

adjusted basis. Figure 8 – Projected 5-year total returns for global assets and neutral portfolio*

Returns are annualised total returns and expressed in local currency. Risk-adjusted returns are projected

returns divided by historical 5y standard deviations. See appendices for definitions, methodology and

disclaimers. There is no guarantee that these views will come to pass. Source: Invesco

Overall, the results are as expected – more volatility is associated with better expected

returns (except for gold and broad commodities). Hence, the return advantage of real

estate and equities is diminished if we take account of volatility (projected return divided

by historical standard deviation of returns). The attraction of cash now becomes

apparent and investment-grade credit (IG) also receives a leg-up from a risk-adjusted

approach (IG has similar volatility to government debt but higher returns, we believe).

We believe that The low return that we project for commodities is because many appear expensive

commodities are compared to historical norms (in real terms). We assume that over the medium/long-

expensive in real terms term they will return to those norms (as they have done over long cycles – see Figure 9,

which shows that US oil tends to return to the $20-$60 range in today’s prices).

Figure 9 – Real US oil price since 1870 (US$ CPI adjusted)

Monthly data since January 1870. As of 31 October 2018. Source: Global Financial Data, Datastream, Invesco

November 2018 For professional/qualified/accredited investors only 9Multi-asset research

The Big Picture

The outlook for 2019: war, inflation, recession?

What could upset the Shortening the horizon to 2019, our previous work suggests that three outcomes could

apple cart in 2019?

provoke an equity bear market, thus disturbing the long-term uptrend: war, a sharp rise

in inflation and/or recession (see Figure 10).

Figure 10 – What causes equity bear markets (1915-2016)? *

*Items in bold are conditions that were true at the start of the calendar year. Others are conditions met during the

year. “-ve EPS momentum” refers to negative earnings per share momentum. “Yld” is yield and “Yld gap” is

inverse of Shiller PE minus 10-year yield. Horizontal axis measures proportion of equity bear markets for which

stated condition was present. Hit rate is the proportion of times the stated condition occurred and was associated

with negative equity returns (or equities being in lowest third of assets). Based on the 27 years from 1915 to 2016

when US equity total returns were negative or when equities ranked among the bottom third of assets. See

appendices for definitions. Source: Robert Shiller, Global Financial Data, St. Louis Fed, Datastream and Invesco

A year in politics – hard to imagine war

The presidential election

The calendar of elections for 2019 lacks a real blockbuster but there will still be plenty to

in Ukraine promises to

be the most interesting keep us occupied (see Figure 11 for our selection of the most important).

set-piece political event

of 2019 Figure 11: Selected elections during 2019

16/02/2019 Nigeria President, Senate, House of Representatives

31/03/2019 Ukraine President

14/04/2019 Finland Parliament

17/04/2019 Indonesia President, House of Representatives

20/04/2019 Afghanistan President

02/05/2019 UK Local

13/05/2019 Philippines Senate, House of Representatives

18/05/2019 Australia Federal (on or before this date)

26/05/2019 Spain Local and regional

26/05/2019 Belgium Federal

31/05/2019 India General (in April or May)

17/06/2019 Denmark General (on or before this date)

28/07/2019 Japan Upper House (probably in July)

04/08/2019 South Africa General (must be held by this date)

20/10/2019 Switzerland Federal

21/10/2019 Canada Federal

27/10/2019 Argentina President, National Congress

05/11/2019 Israel Knesset (on or before this date)

Source: International Foundation for Electoral Systems, Wikipedia, Invesco

Perhaps the most interesting on the global geo-political scale will be the presidential

election in Ukraine, given the strained relationship with Russia. Opinion polls are

November 2018 For professional/qualified/accredited investors only 10Multi-asset research

The Big Picture

currently suggesting that former Prime-Minister Yulia Tymoshenko will become

president, although things could change before the election on 31 March. She has

antagonised Russia in the past and her desire that Ukraine join the EU and NATO is

unlikely to play well in Moscow. Depending on the reaction of Vladimir Putin, there is the

possibility of more tension between Russia and the West.

Who will dare to take on Otherwise, perhaps the most intriguing election-related activity could be the

President Trump in the announcement of candidates for the 2020 US presidential race. We know that President

2020 elections? Trump intends to seek re-election but there have been no firm declarations of intent from

anybody who could mount a serious challenge. Though President Trump’s popularity

ratings are low, he defied the opinion polls in 2016 and anybody who confronts him is

likely to face a bruising battle. This may deter potential candidates, though if the

economy deteriorates over the coming 12 months they may be encouraged to raise their

heads above the parapet.

India remains the largest democracy and opinion polls over recent months suggest it is

heading for a hung-parliament. The NDA alliance of Narendra Modi looks as though it

will remain the biggest parliamentary grouping but without the current degree of control.

Argentina’s elections had looked as though they would result in the re-election of

President Macri but recent economic turmoil (recession, inflation at 40% and currency

depreciation) render the outcome uncertain. Likewise, recession in South Africa may

render the ruling ANC party less popular but for now opinion polls suggest it will be the

largest party in parliament, with close to, if not more than 50% of seats. This suggests

that President Ramaphosa will be selected by parliament to continue in his post.

We will be keeping an eye on Spain’s local and regional elections, just in case there is a

replay of Catalonian dissent. If so, this could add to volatility in European markets.

In Europe, there are also three non-election political developments that we shall be

following closely: the conclusion of the Brexit process; the battle between Italy and the

EU and the durability of Angela Merkel’s Chancellorship.

Brexit still has the The UK and EU have now published the text of their Brexit agreement and, not

potential to

surprise/disappoint

surprisingly, the EU got its way on most points. The political reaction in the UK has been

furious and it is not clear the deal will be acceptable to the UK parliament (it must also be

accepted by all other EU parliaments). If not, finding an alternative in time for the 29

March 2019 exit now looks impossible. Although we think this was the only deal

available, the political reaction leads us to believe the probability of both extreme

outcomes has increased: a no-deal Brexit or no-exit (via a second referendum). We

must also consider the possibility of a leadership challenge to Theresa May and, if

parliament rejects the deal, a general election (and the risk of a Labour government).

We still believe the most likely outcome is that the proposed deal will be accepted by the

UK parliament (it is detested but the alternatives are collectively unpalatable to even

bigger numbers). However, we need to balance the negative risk of no-deal and Labour

government scenarios against the positive risk of no-exit. We think it is finely balanced.

Will Italy consider As previously noted, the populist government in Italy has been received with suspicion

leaving the EU? by financial markets (despite its policy programme bearing a striking resemblance to that

of President Trump -- see The good, the bad and the ugly). Fiscal orthodoxy reigns in

the markets (and at the credit rating agencies), whereby it is believed that fiscal deficits

are bad. However, as originally suggested by Keynes, we believe there are

circumstances in which fiscal expansion makes sense, especially when central banks

find themselves in liquidity traps (as was the case after the financial crisis) and when

fiscal multipliers are high (as they proved to be in the case of Greece in the last 10

years). If any country needs fiscal expansion and deregulation, it is Italy (in our opinion)

and if the markets were not anchored on the EU’s fiscal rules, they wouldn’t be worried

about Italy’s budget proposal. Unfortunately, the EU (and importantly Germany) does

not have the same opinion and this battle could rumble on and become very serious for

eurozone markets if Italy is pushed to reconsider its EU membership.

November 2018 For professional/qualified/accredited investors only 11Multi-asset research

The Big Picture

Germany risks On the topic of Germany, Angela Merkel’s announcement that she will not seek re-

becoming a source of election as Chairperson of the CDU party at the December conference and will not seek

instability any political role when her chancellorship ends in 2021 raises uncertainty in Germany,

the EU and the world. Seen as a leader within the EU and a foil to President Trump, the

question is who will replace her in not only Germany but also on the European and world

stages. Though she wants to stay until 2021, there is a real possibility that she will be

gone before then (traditionally, the leader of the CDU takes the role of chancellor when

they are in power). Once the new CDU leader is in place, there will be constant pressure

for change and, if the coalition crumbles, there could be new elections. Given that

Germany has been a force for stability, this could bring unwanted uncertainty (though a

change of German government could bring a more flexible EU approach to Italy).

What will he do next?

Finally, the presidency of Donald Trump brings the risk of new geo-political surprises.

Though settlement was reached with Canada and Mexico, the US continues to wage

trade disputes with China and the European Union and we wouldn’t be surprised to see

Japan targeted. At some stage, even the biggest school bully will suffer if he picks too

many fights: there is a risk that the US and global economies will be further weakened.

Trade disputes are one thing but history suggests that military conflict would have a

more dramatic effect on markets. Our analysis of important conflicts over the last 100

years or so (starting with WW1) suggests that war is often associated with losses on US

equities, though the bottom is usually felt within the first 12 months and indices tend to

have recovered lost ground within 18 months (on average).

It is hard to imagine the outbreak of a military conflict serious enough to shake global

markets during 2019 but we reckon that the belligerence of President Trump has

doubled the probability to 20% (we identified 10 such conflicts over a 100-year period).

Iran and North Korea are likely to continue to be recipients of US attention, especially as

the US presidential race gets underway and a stand-off is always possible between the

US and Russia and/or China as a result of tensions centred on Crimea, Syria and North

Korea, for example.

The risk of higher inflation

Tightening labour Figure 10 shows that many of the periods of poor US equity market performance have

markets in many also been periods when inflation has been on the rise (see horizontal axis). We have

countries suggest wage been anticipating a rise in global inflation for some time due to tightening labour markets

pressures should be

building

in many parts of the world, especially Japan and the US. Hence, the concern at the

apparent acceleration of wages in the US (see Figure 12).

Figure 12 – US unemployment and average hourly earnings *

*Monthly data from January 1985 to October 2018. Hourly earnings are for private sector, non-farm, non-

supervisory staff. Source: Datastream and Invesco

November 2018 For professional/qualified/accredited investors only 12Multi-asset research

The Big Picture

Which could be a A rise in wage inflation poses a dual problem for equity markets: first, if it is not matched

problem for equity by a rise in selling prices, it will squeeze profit margins and, second, if it does cause a

markets rise in selling prices it will boost core inflation and could provoke higher central bank

interest rates and bond yields. It is also possible that we experience a mix of the two

(depressed margins and higher rates). Either way, it is a warning signal for equity

investors.

But so far it has not That sounds scary but there has so far been no noticeable uptick in core inflation (see

translated to a pick-up in Figure 13), perhaps because broad monetary growth has remained subdued. Either

core inflation way, there is no sign yet that core inflation is moving to a sustainably higher path.

Figure 13 – Core CPI by region (% yoy) *

*Monthly data from January 2000 to September 2018. Source: Datastream and Invesco

We expect at least three Nevertheless, we doubt the Fed will wait for definitive signs of inflation before continuing

Fed hikes between now with its policy normalisation. We expect a further three or four rate hikes between now

and end-2019 and the end of 2019 (one next month and two or three during 2019), taking policy rates

to the 3.00%-3.25% range (see Figure 30 for the full set of forecasts).

But, don’t panic –

Despite the fact we expect global core inflation to rise gently during 2019 (to 3%), there

equities tend to continue

doing well while the Fed

are reasons for equity investors to remain calm: first, the vertical axis of Figure 10

is tightening suggests that rising inflation does not always provoke poor equity market performance

(far from it); second, as written here, stocks tend to continue outperforming bonds

throughout the entirety of Fed tightening cycles and, third, the correlation between bond

yields and equity prices has been largely positive throughout this century (rising yields

associated with rising equity prices) and our analysis suggests that a switch to a

negative correlation typically happens when US 10-year yields are closer to 5% than 3%

(see What’s in a correlation published on 27 February 2018).

We do not expect inflation to be a problem for equity markets during 2019.

No recession in 2019

Recession is what we We still believe the most likely cause of an equity bear market will be recession,

fear the most particularly a US recession. This is the one phase of the economic cycle when our

historical analysis suggests it is better to be in defensive assets such as gold, cash and

government debt.

And most economies Figure 14 shows our view of where the world’s 10 largest economies are within their

are in the late-expansion economic cycles (it also shows our interpretation of what history tells us about which

phase with more assets tend to perform the best at each stage of the cycle). We believe that the large

deceleration to come, economies are spread across the mid to late-cycle phase but we do not think any of

we think, but not them are in recession and we do not expect them to be during 2019. This said, we do

recession believe there will be some deceleration, in both the US and farther afield, with global

growth slowing to more like 3% (from around 3.6% in the year to mid-2018).

November 2018 For professional/qualified/accredited investors only 13Multi-asset research

The Big Picture

The consensus economic forecasts shown in Appendix 1 suggest an expectation of

slight global GDP deceleration in 2019 and 2020 (from 3.8% in 2018 to 3.6% and 3.2%,

respectively) with headline inflation relatively stable at just above 3%. After an

acceleration in the US economy in 2018, the consensus expects a deceleration there

and elsewhere, partially balanced by acceleration in Brazil and India.

Equity-like assets tend Not surprisingly, given the information in Figure 14, we suspect the best returns will still

to continue doing well at be on equity-like assets (equities, real estate and high-yield credit) and this is borne out

this stage of the cycle by the return projections discussed earlier. Implicit in those projections is the

assumption that a global recession will occur in the next five years but, importantly, we

do not expect it during 2019. This said, recession in 2020 could still damage equity-like

assets during 2019 if anticipated by financial markets.

The UK is at the most We suspect the UK economy is the most susceptible to recession during 2019, largely

risk of recession, we because of the potential negative effect of the Brexit process (rise in uncertainty and a

think loss of investment and jobs). The UK economy has underperformed since the Brexit

vote (despite the depreciation of sterling) and we suspect that will continue.

And the eurozone has It is also apparent that the eurozone economy has been among the most disappointing

lost momentum

during 2018 (economic surprise indices make it very clear). That may be a spill-over

from the UK’s Brexit woes and could also reflect the deceleration of global exports, in

part due to President Trump’s actions (the eurozone is a very open economy and

therefore vulnerable to any such trade slow-down). More recently, the volatility in Italian

markets may have dampened confidence. We were not expecting this weakness in the

eurozone and still believe that it is too early in its economic cycle for recession to occur

but the signs have not been good. We hope to see better data over the coming months

and quarters. If not, we may have to revisit our views on the region.

Figure 14 – The economic and asset class roller coaster

Chart shows our view of the cyclical positioning of the world’s largest economies. The selection of preferred assets is based on our research

published in “Asset allocation in pictures” in November 2017. See appendices for definitions, methodology and disclaimers. Source: Invesco

November 2018 For professional/qualified/accredited investors only 14Figure 15 – Fed policy rates versus nominal GDP growth (%)

Note: based on monthly data from July 1954 to October 2018 (except for GDP data which is quarterly and is up

to 2018 Q3). Synthetic policy rate is the actual policy rate adjusted for Fed asset purchases using the

“Bernanke rule of thumb” whereby each $150bn-$200bn of asset purchases is equivalent to a 25bp rate cut

(the same now applies in reverse). Source: Datastream and Invesco

Playing devil’s advocate, what signs should alert us about US recession? Many

Are there any worrying

signs from the US commentators focus on an inversion of the yield curve but we view that as a symptom,

economy? rather than a cause of recession. In more normal times, the yield curve inverts when the

Fed has raised rates enough to depress the economy and inflation expectations. The

curve may now be inverting because of the lingering impact of Fed QE on long rates,

rather than the fact that policy rates are high enough to staunch growth. Yes, new home

and auto sales have flattened but they no longer make big contributions to GDP.

Based on the evidence in Figure 15 we doubt that Fed policy is yet choking the US

We think the Fed

economy. At 2.25%, Fed policy rates are well below nominal GDP growth (5.5% in Q3).

remains accommodative

Even if the Fed raises rates in December (18-19) and nominal GDP growth settles back

down to around 4.5%, there would still be a two-percentage point gap between the two,

which is hardly indicative of a tight policy stance (in our opinion). Even better, if we

share the Fed’s opinion that it is the stock of its assets that counts (rather than the flow),

then Fed policy remains super accommodative. Using the Fed’s own rule for calculating

a synthetic rate that adjusts policy rates for what has happened to the balance sheet, we

derive a rate that remains negative (-2.4% in October). We do not know at what point

Fed rates will dampen activity but we suspect it will not be until they are closer to 4%. Of

course, recent dollar strength may dampen net exports (which were very weak during

2018 Q3) but, even then, the dollar is hardly at an extreme valuation (see Figure 38).

Figure 16 – Components of US GDP before and after the onset of recessions*

*Note: components of GDP (in constant prices) are shown in the four quarters before and five quarters after

that in which recession starts (all components are indexed to 100 in that quarter). The chart shows the average

path of each component across the eight GDP recessions since 1950. Source: Datastream and Invesco

November 2018 For professional/qualified/accredited investors only 15Multi-asset research

The Big Picture

Investment and profits We have previously written on the topic of economic downturns (see The anatomy of a

play a key role in US recession) and Figure 16 shows why we focus on profits -- investment seems to play

economic downturns a key role in the onset of recession in the US. We identified three indicators that are

and they are still almost always present either before or during a US recession: falling profits, falling

trending upward

investment and a falling equity market. President Trump’s tax cuts could help to prolong

the profit and investment cycles and Figure 17 shows that all three of those indicators

are still trending upward, which is a good sign (though be aware that the data is quarterly

and thus excludes the S&P 500 dip during October and that investment was down a

touch in Q3 if we exclude inventories, having been strong in the previous three quarters).

Figure 17 – US Profits, investment and the S&P 500 during this economic upswing

*Note: the chart shows the path of investment, profits and the S&P 500 since the US economic cycle bottomed

in 2009 Q2 (all components indexed to 100 in that quarter). Data is quarterly. Horizontal axis shows number of

quarters since 2009 Q2. Investment is gross private domestic investment (in constant prices). Profits are from

the national accounts (profits after taxes with inventory valuation adjustment and capital consumption

adjustment) and are in current prices. As of 2018 Q3. Source: Datastream and Invesco.

When it comes to the global picture, Figure 18 is relatively comforting. Global profit

growth compares well to that of recent years, with impressive growth in Japan but

deceleration in the eurozone and EM. Chinese industrial profits have decelerated in

recent months (to 4% y-o-y in September), along with the economy, though GDP growth

in the 6.50%-7.00% range is not too alarming. It is hard to disentangle the structural and

cyclical elements of the Chinese deceleration and we remain relatively optimistic about

China’s ability to deal with a slowdown (see More pictures of China).

As are profits in the rest Hence, though we can see why the US and global economies should decelerate during

of the world 2019, we do not believe recession will occur. We suspect that can wait until 2020/21.

Figure 18 – Earnings per share growth (% yoy)

Note: monthly data from January 2012 to October 2018. Based on Datastream indices.

Source: Datastream and Invesco

November 2018 For professional/qualified/accredited investors only 16Multi-asset research

The Big Picture

We need to talk about Jerome

But the lack of central Even without war, inflation or recession during 2019, financial markets will be challenged

bank asset purchases by the behaviour of central banks. Fed tightening will be the main cause for concern but

may limit portfolio

other developed world central banks will play a role. Figure 19 shows how we expect

returns

the aggregate balance sheet of the QE5 to develop through to the end of 2019 (the QE5

is the group of central banks that have used quantitative easing in a meaningful way:

The Fed, ECB, BOE, SNB and BOJ). Unfortunately, the combination of Fed balance

sheet reductions and tapering by the ECB should bring the aggregate balance sheet into

negative growth territory over the coming months (if the BOJ continues buying at the

same pace as during the last 12 months, which is about half of its stated plan).

Things could get worse 2018 has already proven more difficult for investors than the previous year and Figure

in 2019

19 suggests 2019 could be even worse. In recent years there has been a reasonable

correlation between the growth of that aggregate balance sheet and the returns provided

by a global multi-asset portfolio (represented by our Neutral allocation, as shown in

Figure 3). Based on that historical relationship, and given our assumptions about the

behaviour of these central banks, we fear that portfolio returns could be limited and

perhaps negative over the next 12-18 months.

Figure 19 – QE5 balance sheet* and asset returns

* Aggregate balance sheet of Fed, ECB, BOE, BOJ and SNB, in USD and rebased to 100 in May 2006. The

forecast considers the plans of the Fed and ECB (assuming ECB makes no further asset purchases after

December 2018). It is also assumed SNB and BOE make no further purchases and that BOJ continues buying

in line with the rate over the last 12 months (around half the rate of its stated plan). The multi-asset benchmark

is a fixed weighted index based on our Neutral asset allocation (see Figure 3). From January 2010 to

December 2019. Past performance is no guarantee of future results. Source: BOE, Datastream and Invesco

We expect fixed income Volatility around a rising trend is one thing but volatility around a flat-to-declining trend is

assets to feel the most quite another -- we are preparing ourselves for many periods of doubt during 2019. Our

pain

gut instinct would push us away from equity-like assets (to dampen volatility) but we

continue to believe the major pain caused by the retreat from QE should be felt in those

assets that were the major beneficiaries of central bank purchases, namely developed

world fixed income markets.

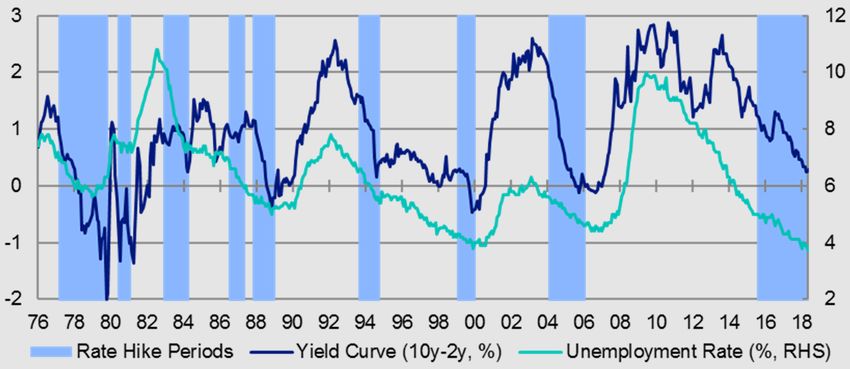

We don’t fear Fed rate It is only natural to believe that equity-like assets will suffer along with bonds but we do

hikes not think that will be the case. We have written extensively on the topic over the years,

including this published in October. Put simply, our research suggests that US equities

usually continue to outperform bonds until the Fed stops raising rates, which is usually at

about the time that unemployment bottoms (see Figure 20). Also, though the yield curve

continues to flatten over that same period, short-maturity bonds tend to continue

outperforming long-maturity counterparts until the Fed has finished its work.

November 2018 For professional/qualified/accredited investors only 17Multi-asset research

The Big Picture

Figure 20 – Fed rate hikes, the yield curve and unemployment

Note: monthly data from June 1976 to October 2018. Past performance is no guarantee of future results.

Source: Datastream and Invesco.

Surprising things Other conclusions from our work on Fed hiking periods include:

happen when the Fed Volatility remains overall quite low (it rises once recession comes).

tightens The dollar may strengthen but the evidence is patchy (it has not yet recovered all the

losses endured since the Fed started tightening in December 2015).

Fed rate hikes increase bond yields elsewhere, even if other central banks ease.

There is no systematic evidence that Fed rate hikes weaken EM currencies, in fact

quite the opposite (see Figure 21 which shows a tendency for our EM currency

index to strengthen during Fed rate hike periods).

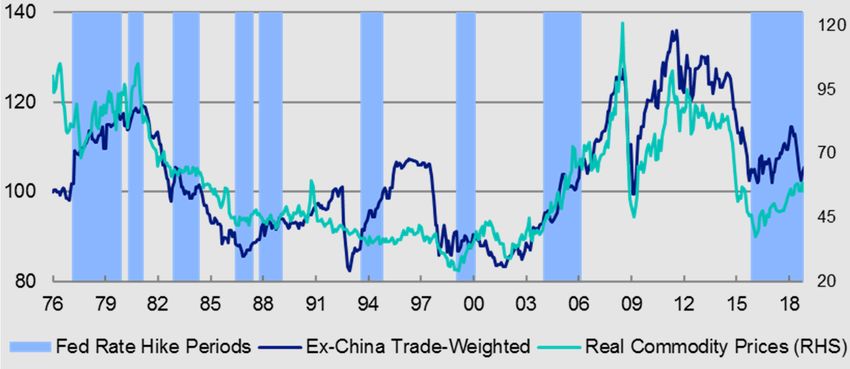

We suspect (hope?) the On the topic of emerging markets, we wrote in September (see The Big Picture) that the

worst is over for EM biggest problem so far during 2018 was currency weakness (underlying asset

currencies performance was not too bad in their local currencies). Further, we concluded that

currency markets had been quite surgical in their approach – the main currency

weakness was related to countries that had already shown signs of financing stress

(rising external debt servicing cost to export ratio) and that most other countries did not

have such problems (except for Indonesia). Now that our EM FX index has returned to

its historical norm, we suspect the worst is over and believe that EM assets will prove

rewarding over the medium term (and during 2019).

Figure 21 – Real EM FX and commodities

Emerging currency indices are trade weighted averages of national currencies versus US dollar (trade weights

are based on total trade flows for each country). There are 18 currencies in the EM basket – those of South

Korea, Mexico, India, Russia, Singapore, Malaysia, Brazil, Thailand, Poland, Turkey, Indonesia, Czech

Republic, South Africa, Hungary, Nigeria, Chile and Philippines (ordered by size of trade flows). Real

adjustments use national CPI indices versus that of the US. “Real Commodity Prices” is the GSCI Spot Index in

USD deflated by US CPI. All indices rebased to 100 as of June 1976. As of October 2018. Source: IMF,

OECD, Oxford Economics, GSCI, Bloomberg L.P., Datastream and Invesco.

November 2018 For professional/qualified/accredited investors only 18Multi-asset research

The Big Picture

Farewell Mario (and Mark); welcome Yi

BOJ is the last man

We believe the BOJ will be the only major central bank still buying assets during 2019 (it

standing

is only buying at half its stated rate) but expect very little in terms of interest rate hikes

outside of the Fed. Indeed, we fear the US central bank will be alone in having returned

policy rates to something like normal by the time of the next recession.

The Bank of Japan has yet to discuss formal tapering, let alone talk about rate hikes (we

feel the 2% inflation target is unrealistic). We expect no rate increases from Tokyo

during 2019 (see the full set of forecasts in Figure 30).

Who will take over at the The Bank of England wants to raise rates and has done so twice since the Brexit

BOE and will rates rise? emergency cut to 0.25% in August 2016 (most recently in August). However, it is now

constrained by anaemic growth and Brexit uncertainty. As it is hard to know the shape of

Brexit, we assume no change in BOE rates during 2019. Also on the agenda next year

will be the replacement of Governor Mark Carney, who serves until 31 January 2020.

Front-runners include BOE insiders Andrew Bailey (now CEO of the Financial Conduct

Authority) and Dave Ramsden (Deputy Governor, Markets and Banking). The choice

lies with the Chancellor of the Exchequer.

Will Mario raise rates Departing even sooner will be Mario Draghi, whose term as President of the ECB ends

before he leaves and

on 31 October 2019. The architect of the ECB’s “whatever it takes” approach may want

will we finally get a to complete the process by putting ECB rates on the path to normalisation. Hence, we

German as head of the

ECB?

expect one small ECB rate hike before Draghi leaves. Perhaps more important will be

the identity of his successor. It was originally thought that Bundesbank President Jens

Weidmann would be favourite and that he would adopt a more orthodox Bundesbank-

type approach (higher interest rates and smaller balance sheet). However, during the

summer it was rumoured that Angela Merkel was more interested in having a German

appointed as President of the European Commission. If Weidmann is not chosen,

potential candidates include Erkki Liikanen (Finland), Francois Villeroy de Galhau

(France) and Philip Lane (Ireland), along with the IMF’s Christine Lagarde (France).

Our new best friend, Yi

Apart from the Fed, the PBOC may be the most influential central bank during 2019 (and

Gang beyond). First, it is easing and we suspect it will continue to do so (Figure 22 shows the

potential for further reductions in the reserve requirement ratio, which could balance to

some extent the reduction of global liquidity due to the ending of developed world QE).

Second, if China’s current account continues recent trends, it will soon be in deficit,

which could render China’s debt situation more problematic, hence the importance of

Chinese bonds attaining full representation in global bond indices. Third, as countries

seek non-US dollar settlement systems (to avoid US sanctions etc), the reserve currency

status of the CNY can only grow. PBOC Governor Yi Gang may be our new best friend.

Figure 22 – China’s monetary policy settings (%)

Monthly data, from January 1980 to October 2018. As of 31 October 2018. RRR is the reserve requirement

ratio applied to bank deposits. Source: Peoples Bank of China, Datastream and Invesco

November 2018 For professional/qualified/accredited investors only 19You can also read