Unmanned Aircraft Systems - FAA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Unmanned Aircraft Systems

Over the last 5 years, unmanned aircraft sys- FAA will continue to enable the thriving UAS

tems (UAS) have been experiencing healthy industry, with the safe integration of UAS into

growth in the United States and around the the NAS.

world. UAS consists of the unmanned air-

craft platform and its associated elements--

including communication links, sensors, soft- Trends in Model Aircraft and Forecast

ware and power supply-- that are required for

the safe and efficient operation in the na- The FAA’s online registration system went

tional airspace system (NAS). While the in- into effect on Dec. 21, 2015. This required

troduction of UAS in the NAS has opened up all UAS weighing more than 0.55 pounds

numerous possibilities, it has also brought (250 grams) and less than 55 pounds to be

operational challenges including safe inte- registered using the on-line system

gration into the NAS. Despite these chal- (https://www.faa.gov/uas/get-

lenges, the UAS sector holds enormous ting_started/registration/) or by using the ex-

promise. Uses may include modelers exper- isting (paper-based) aircraft registry. In May,

imenting with small UAS (sUAS), performing 2017, a U.S. Appeals Court Order caused a

numerous functions including aerial photog- temporary halt in UAS registration. Subse-

raphy and personal recreational flying. At quently, the registration requirement for all

the same time commercial operators may be model aircraft owners was reinstated in De-

experimenting with package and medical cember 2017 with the 2018 National Defense

supply delivery and providing support for Authorization Act (NDAA). Despite the tem-

search and rescue missions. porary halt, registration’s pace continued be-

yond May, 2017. The latest FAA reauthoriza-

This section provides a broad landscape tion codifies the requirement [see

covering model and non-model aircraft 12 and https://www.faa.gov/news/up-

their recent trends as gleaned from trends in

dates/?newsId=91844 for more details].

registration, overall market and operational

information. Using these trends and insights With the continuing registration, more than

from industry, the FAA has produced several 900,000 owners had already registered with

areas of forecasts for UAS. Forecasts re- the FAA by Sept. 2018. Monthly owner reg-

ported in this section are driven primarily by istration averaged around 8,000-9,000 dur-

the assumption of continuing evolution of the ing Jan.-Dec., 2018, with some expected

regulatory environment (i.e., unconstrained peaks during the holiday season and sum-

environment), the commercial ingenuity of mer.

manufacturers and operators and underlying

demand, including business models. The

12These are also called, interchangeably, hobby notes including other documents of the Agency,

and non-hobby UAS, respectively. In previous these terms are often interchanged.

41

Unlike non-model counterparts, the registra-

tion rules do not require modelers to register

each individual aircraft; only owners are reg-

istered. Each owner registers, and each

owner might have multiple UAS. Exceptions

may be registered modelers with no owned

equipment. Notwithstanding these chal-

lenges, there is information available for both

industry and academia, allowing us to under-

stand aircraft ownership. Furthermore, un-

The pace of registration in 2018 slowed con- der the sponsorship of the UAS Integration

siderably compared to 2016 and 2017. Research Plan, the Agency has launched

Monthly owner registration now stands at various research activities to understand the

half of what was observed a year ago. possible magnitude of the sector as well as

implications for likely aircraft that may be

Model registration and thus ownership of used for model flying and safety implications

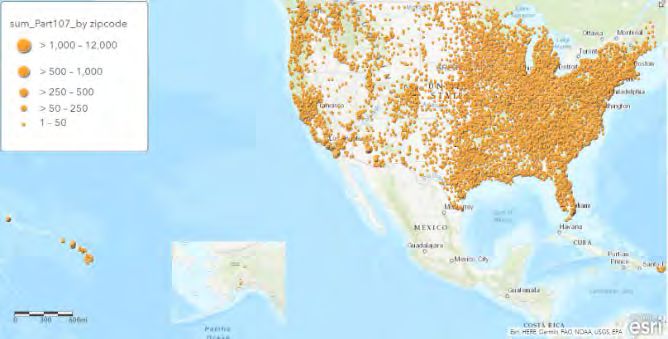

sUAS is distributed throughout the country. for the UAS fleet from gradual integration into

Using the data as available in Sept 2018, a NAS. The forecasts presented use all avail-

spatial distribution of ownership by zip code able resources to analyze and forecast both

below demonstrates that sUAS continue to model and non-model activities in the U.S.

be distributed throughout the country with

denser ownership mapping closely against With over 900,000 modelers registered as of

the population centers of the country, as ex- December 31, 2018, we estimate that there

pected. are around 1.25 million drones distinctly

identified as model aircraft. Comparing with

industry sales and other data noted above,

we conclude that model aircraft is almost 40

percent higher than ownership registration 13.

A comparison of last year’s data with this

year’s (2018) shows that the annual growth

rate to be around 13 percent. This continues

to be substantial growth as anticipated from

the introduction of drones as a recreation ac-

tivity facilitated by falling equipment prices

and improved technology, such as built-in

cameras and relatively easy maneuvering.

13 This calculation involves taking into account re- we expect this rate to change dynamically over

tirement, redundancy, and loss of craft corre- time.

sponding to ownership registration. As craft be-

comes sturdier and operators situationally aware,

42

However, like in all other technologies includ- model on registration trends. Using these,

ing hobby items, (e.g., cell phones and video we forecast that the model fleet will likely

game consoles; and prior to that, video cam- (i.e., base scenario) attain its peak over the

eras, and video players), the trend in model next 5 years, climbing from the present 1.25

aircraft is likely to slow as the pace of falling million units to around 1.39 million units by

prices diminishes and the early adopters 2023. The high/optimistic scenario may be

begin to experience limits in their experi- estimated at 1.66 million units over the next

ments or simply eagerness plateaus. 5 years. As evident, the growth rates under-

lying these numbers are fairly steady in the

Total Recreation/Model Fleet initial years but are diminishing faster in the

(Million sUAS Units) last 2-3 years. The gradual saturation that is

year Low Base High projected in 5 years and beyond in the model

aircraft fleet parallels other consumer tech-

2018 1.25 1.25 1.25

nology products.

2019 1.29 1.31 1.35

2020 1.31 1.35 1.44

2021 1.31 1.37 1.52

2022 1.32 1.38 1.59

2023 1.32 1.39 1.66 Survey of Non-Model Aircraft Owners

Before we describe non-model sUAS trends

Given the trend in registration and market de- and forecasting in the next section, we pro-

velopments, we forecast that the model air- vide a brief overview of results from a proto-

craft market will saturate at around 1.4 million type survey that the FAA undertook during

units. However, there are still some upside June-July, 2018. The results provide likely

uncertainties due to further changes in tech- growth path in the near future. The survey,

nology and the likely event of continuously based on a well-tested questionnaire, was

falling prices. This yields to some upside un- sent by the FAA to individuals registered by

certainty in the forecast. We do not antici- December 31, 2017 and conducting activities

pate similar symmetry in low side as it paral- under Part 107 (i.e., non-model or commer-

lels to the growth in the base projection. cial activities) in that year. The response rate

Nevertheless, we provide a forecast base to the survey was approximately 8 percent

(i.e., likely) with high (or optimistic) and low (7,400 responses from 89,000 contacted).

(or pessimistic) scenarios, provided in the ta- The survey was designed primarily to get a

ble above. The FAA projects, unlike in pre- snapshot of non-model/commercial mission

vious years, that this sector may have ex- characteristics including location, types of

hausted downside risks; i.e., decline in regis- aircraft used, and altitude flown. In addition

tration beyond saturation as captured by to providing the FAA key data in understand-

base forecast. ing operational characteristics of non-model

activities throughout the country, these key

We use the trend observed in registrations,

metrics are also important for understanding

particularly over the past year, expert opin-

trends in non-model activities and likely

ions collected in TRB annual workshops, re-

growth trajectory in the near future.

view of available industry forecasts, mar-

ket/industry research, and a time-series

43

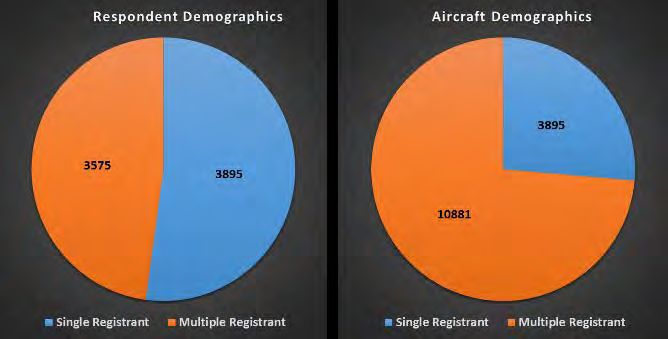

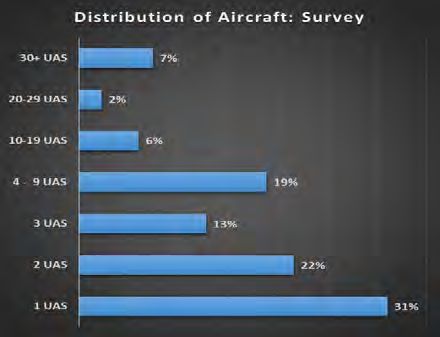

Registrants with one aircraft and those who

owned/operated multiple aircraft responded

almost equally as the figure above shows. Turning to distribution of ownership, we ob-

The average number of aircraft among multi- serve that almost 1 in 3 survey respondents

ple registrants was around 3 with a margin of used one sUAS compared to 55 percent from

error of + 0.2. Survey sample was repre- the population (i.e., the Registry). For those

sentative when checked against the popula- who operate multiple sUAS, a large group

tion from the Registry. (54 percent) falls into the category of operat-

ing 2-9 sUAS, as compared to only 1 in 3 in

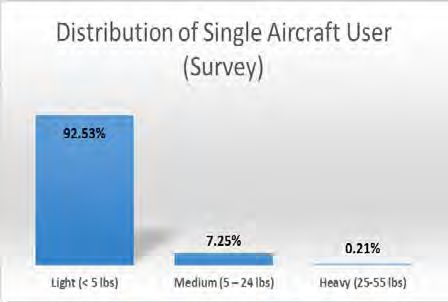

The survey reveals that most of the non- that category from the Registry or population

model UAS are light UAS, those weighing 5 counts. For operators with over 10 sUAS,

lbs or less. This result was the same as in survey response (15 percent) were closer to

the Registry. The figure below shows the what we observe in the Registry (12 percent).

distribution among the responses from single This distribution provides valuable infor-

sUAS users: mation regarding the use intensity of sUAS

by both single and multiple owners.

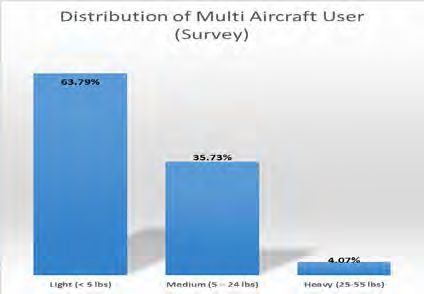

A similar distribution is reflected in responses

from multiple aircraft owners, although the

weight of the classes are skewed more to-

Bigger variations are observed between sin-

wards the medium (5-24 lbs) and heavy (25-

gle and multiple sUAS when asked about in-

55 lbs):

44

tensity of operations as captured by the num-

ber of missions 14 in 2017. It is apparent from

the table below, the more one operates (i.e.,

multiple owners) sUAS, the more missions

they fly during the year; i.e., over twice as

many as the single operator. On average,

while a single operator flies 32 mis-

sions/year, multiple owner/operators flew

more than twice that number (82 missions,

on average):

Trends in Non-Model Aircraft and Fore- pace accelerated to 14,600 registrations a

cast month during the last year (2018). The non-

model sector is primarily commercial in na-

Unlike model ownership, rules for non-model

ture. It is dynamic and appears to be at an

registration require owners to register each

inflexion point of demonstrating powerful

sUAS, thus giving a one-to-one correspond-

stages of growth. Unlike the model sector,

ence between registration and aircraft. For

we anticipate that the growth rate in this sec-

the calendar year 2018, more than 175,000

tor will continue to accelerate over the next

non-model owners/operators registered their

few years. Since initiation of Part 107, there

equipment. The pace of monthly registra-

has been proposed rule changes (see

tion, almost 15,000, is nearly 3-times higher

https://www.federalregister.gov/docu-

than the pace at which non-model aircraft

ments/2019/02/13/2019-00732/operation-of-

owners registered their craft during the same

small-unmanned-aircraft-systems-over-peo-

time last year. While the pace of model reg-

ple. The requirements would address oper-

istration ownership has slowed down consid-

ations over people, operations at night with-

erably, interestingly, the pace of registration

out waivers and possibilities for waivers in-

is accelerating for non-model counterparts.

cluding enhancement of operational efficien-

By the end of 2018, there were more than

cies. They would also address more com-

277,000 non-model aircraft registered since

mercial uses that will likely facilitate further

registration opened.

growth. Notably, a single point for submis-

Since the registration process has been sion of all operational information, including

available through Dec 2017, over 4,600 air-

craft per month have been registered. This

14Missions were described as a job or economic

activity consisting of many take-offs/landings.

45

registration, authorization, and accident log- fell short by almost 80 percent for 2018 (or

ging, helps facilitate this growth further 277,000 actual aircraft vs 158,900 that we

[https://faadronezone.faa.gov/#/]. projected last year). The significant growth

in this sector over the past year demon-

strates the uncertainty and potential of the

market.

Given the trend observed in the registrations,

information from the survey, review of avail-

able industry forecasts, and internal re-

search, together with market/industry re-

search, we project that the non-model fleet

by 2023 will likely (i.e., base scenario) be

As in the case of model UAS ownership, non-

three times larger than the current number of

model sUAS are distributed across the coun-

non-model aircraft 15. As the present base

try. A spatial distribution of equipment regis-

(i.e. cumulative total) gets larger, we antici-

tration (using data for September 2018)

pate the growth rate of the sector will slow

demonstrates that non-model sUAS are dis-

down over time. Nevertheless, the sector will

tributed throughout the country with denser

be much larger than what we understood as

activities mapping closely against the eco-

recently as last year. Given the accelerated

nomic or commercial activities of the country.

registration over the last year, we now project

the non-model sUAS sector will have over

835,000 aircraft in 2023 (i.e., end of 5-year

period). Important to note here is that last

year’s forecasted sUAS for 2022 (452,000

units) will be surpassed sometime towards

the later part of 2019 or early 2020 if the pre-

sent registration trend continues. This will

shorten the forecast outcome period by al-

most 2-3 years.

Last year, we forecasted that the non-model

sector would have around 229,400 sUAS in In order to understand the growth trajectory

2019, a growth rate exceeding 44 percent of the sector better, we divide the non-model

from the year before (2018). Actual data far sector into two types of UAS aircraft: con-

exceeds that trend with over 277,000 aircraft sumer grade and professional grade. The

already registered by the end of 2018. Our consumer grade non-model aircraft are

forecast of non-model sUAS last year thus priced in a wide range, somewhere below US

15Last year, this ratio (from base year of forecast

to end-year of forecast) was 4-times; i.e., we pro-

jected forecast to be 4-times the base year’s

(2017) numbers in 5-year.

46

$10,000 with an average unit price of around ther enhanced by, for example, the Low Alti-

$2,500. The professional grade is typically tude Authorization and Notification Capability

priced above US $10,000, with an average (LAANC) system 17, which began authoriza-

unit price assumed to be around $25,000 16. tion in May, 2018. LAANC is designed to al-

For both consumer grade and professional low considerable flexibility in sUAS opera-

grade aircraft, the average price has been tions and facilitate non-modelers’ use of the

falling over time, particularly over the last NAS. While most of the near-term growth in

three years. Currently, the consumer grade non-model sUAS will continue to come from

dominates the non-model sector with a mar- consumer grade (over 90 percent), we antic-

ket share approaching 95 percent. However, ipate a significant part will come from profes-

as the sector matures and the industry be- sional grade non-model sUAS as well.

gins to consolidate, the share of consumer

grade non-model aircraft is likely to decline As non-model aircraft become operationally

but will still be dominant. By 2023, FAA pro- more efficient and safe, battery life expands

jects this sub-sector will have around 85 per- and integration continues, new business

cent share of the overall non-model sUAS models will begin to develop, thus enhancing

sector. robust supply-side responses. These re-

sponses, in turn, will pull demand forces

Starting from a low base of around 13,000 (e.g., consumer responses to receiving com-

aircraft in 2018, professional grade non- mercial packages; routine blood delivery to

model sUAS sub-sector stands to expand hospitals, search-and-rescue operations,

rapidly over time, especially as newer and etc.) that are somewhat latent and at the ex-

more sophisticated uses are identified, de- periment stage, at present. Unlike a devel-

signed, and operationally planned and flown. oped sector such as passenger air transpor-

If, for example, professional grade sUAS tation, it is impossible to put a marker on “in-

meets feasibility criteria of operations, safety, trinsic demand” (or core demand), primarily

regulations, and satisfies economics and driven by economic and demographic fac-

business principles and enters into the logis- tors, underlying this sector. Nevertheless, an

tics chain via delivering small packages, the attempt has been made to capture the low-

growth in this sector will likely be phenome- range to the projected demand. Hence, we

nal. This growth trajectory may even be fur- provide the likely or base scenario together

with the enormous potential embodied in the

16 Because of this wide range in prices between FAA approved UAS Service Suppliers (USS) are

types of sUAS in commercial activities, start-up checked against airspace data in the FAA UAS

cost for a business may vary somewhere be- Data Exchange such as temporary flight re-

tween $2,500 and $25,000.

17 Low Altitude Authorization and Notification Ca-

strictions, NOTAMS and the UAS Facility Maps

(UASFM). Approved requests thus provide the

pability [https://www.faa.gov/uas/programs_part-

FAA ATO visibility into where and when planned

nerships/uas_data_exchange/] or LAANC auto-

drone operations will take place.

mated the application/approval process for air-

space authorizations. Requests submitted via

47

“high” scenario, representing cumulative an- next. Increasingly, state and local govern-

nual growth rates of 25 percent and 36 per- ments are using sUAS for emergency ser-

cent, respectively. In the event of unfore- vices including search-and-rescue opera-

seen slowdown or obstacles, “low” scenario tions and presently employ around 3 percent

projects a cumulative growth rate of around of all non-model sUAS. As the sector grows,

17 percent annually. we anticipate there will be many more uses

of non-model sUAS as they are increasingly

Total non-Model Fleet evident from the participants’ activities, for

(no. of '000 units) example, under the Integration Pilot Program

year Low Base High (IPP). In May, 2018 the FAA awarded 10

2018 277 277 277 communities, among a pool of 149 applica-

2019 369 400 426 tions, [https://www.faa.gov/uas/pro-

2020 460 545 638 grams_partnerships/uas_integration_pi-

2021 552 711 932 lot_program/awardees/] to participate in the

2022 588 789 1,112 IPP. IPP applications and preliminary data

2023 603 835 1,290 indicate that awardees overwhelmingly plan

to undertake numerous commercial and pub-

Non-model sUAS are presently used for nu- lic interest activities.

merous purposes. The survey of non-model

One way of identifying early trends of non-

sUAS aircraft owners reveals their present

model sUAS uses is to analyze the waiver

uses as follows:

applications granted to non-model sUAS op-

erators. Both the magnitude and relative

composition of waiver types may indicate the

direction of the non-model sUAS sector as a

whole. A breakdown of the waiver requests

granted in December 2018 is shown in the

chart below:

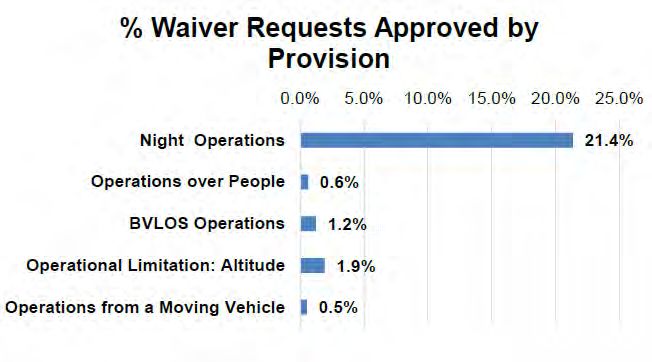

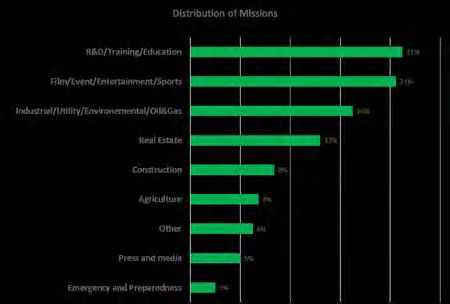

Non-model sUAS are used extensively in

carrying out research and development

(R&D), and in training-education missions

(21 percent), followed by filming events in-

cluding weddings, entertainment and sports

(21 percent), industrial/utility and in environ- Beyond what is presently allowed under ex-

mental projects such as aerial inspection (16 isting Part 107, expanding non-model appli-

percent) followed by real estate (13 percent) cations further would require waivers, to a

and in construction activities (8 percent). Ag- large extent, for night operations, (1 in 5

riculture (7 percent) including crop inspec- waivers) and operating limitations of altitude

tion; and press and media (5 percent) come (1.9 percent). Many of these waivers are

combined, and hence, total waivers granted

48

(over 2100 in December 2018) exceed 100

percent. The Agency issues these waivers

to facilitate commercial activities by non-

model sUAS while preparing for the next

round of regulations. New regulations seek

to amend the present waiver requirements.

(See https://www.federalregister.gov/docu-

ments/2019/02/13/2019-00732/operation-of-

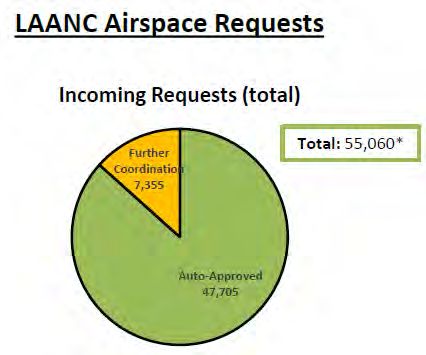

small-unmanned-aircraft-systems-over-peo- Finally, LAANC continues to routinely pro-

vide auto-approval. It has provided, so far,

ple for current notice of proposed rulemaking

(NPRM) on operations of small unmanned over 47,000 auto-approvals for airspace ac-

aircraft over people in certain conditions and cess requests, while sending over 7,000 for

further coordination. LAANC authorizations

operations of small UAS at night without ob-

are facilitated by combining UAS facility

taining a waiver). Analysis of these waiver

applications allows us to understand the in- maps (UASFM)

dustry trends, one of many metrics essential [https://faa.maps.arcgis.com/apps/webappvi

for understanding and projecting both the tra- ewer/in-

jectory, course corrections, and growth dex.html?id=9c2e4406710048e19806ebf6a

06754ad] that provide maximum allowed al-

trends of the sector.

titudes around airports where the FAA may

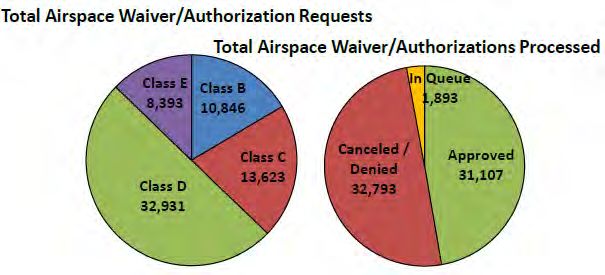

Almost 50 percent of airspace authorizations authorize Part 107 UAS operations without

and waivers were approved for the controlled additional safety analysis. The UASFMs are

airspaces at the end of December, 2018. used to inform requests for Part 107 airspace

While over half of them were for class D air- authorizations and waivers in controlled air-

space (i.e., smaller airports with control tow- space.

ers), other classes were also requested and

regularly flown.

Survey responses show that while most of

the respondents routinely fly in Class G air-

space (almost 60 percent), there are quite a

few users, who fly within controlled airspace Remote Pilot Forecast

facilitated by the airspace waivers.

An important final metric in non-model sUAS

is the trend in remote pilot (RP) certifications.

RPs primarily facilitate non-model sUAS

49

flights for commercial activities. As of De- the base of 116,027 RPs in 2018, non-model

cember 2018, more than 116,000 RP certifi- activities may require almost 350,000 RPs in

cations have been issued 18. Over 90 percent 5 years, a three-fold increase, providing tre-

of those who took the exam passed and ob- mendous opportunities for growth in employ-

tained RP certification. The RP forecasts ment associated with commercial activities of

presented below are based on using two UAS. Potential for RPs may enhance even

data sources: (a) trends in total RPs; and (b) more if larger UAS are used in commercial

trends in non-model sUAS registration and activities and urban air mobility becomes a

forecasts of fleet. Given the trends in regis- reality in the near future.

tration and our forecast of non-model fleet,

we assume that one pilot is likely to handle Urban Air Mobility

2.4 units of non-model sUAS. In Sept 2017, NASA launched a market

study for a segment crossing over some

Using these assumptions and combined with

functions of UAS discussed above. This seg-

the base scenario of non-model sUAS fore-

ment of autonomous vehicles broadly called

cast, we project RPs in the graph below. Last

Urban Air Mobility (UAM) is defined as “a

year, we projected RPs to be around

safe and efficient system for air passenger

106,000 by the end of 2018; which fell short

and cargo transportation within an urban

by 10,000 by the end of 2018. However, the

area, inclusive of small package delivery and

registration of non-model sUAS far ex-

other urban unmanned aircraft systems

ceeded, as noted earlier, what we projected

(UAS) services, which supports a mix of

last year.

onboard/ground-piloted and increasingly au-

tonomous operations” (see

https://www.nasa.gov/aero/nasa-embraces

urban-air-mobility). Studies sponsored by

NASA were undertaken by two consulting

firms and are presently under review from ex-

pertise within the government and academia.

Executive summaries of the two reports sug-

gest (https://www.nasa.gov/uamgc), broadly

speaking, the following: (a) UAS may play a

significant role in transforming short-haul ur-

Given these, we made the adjustment to RPs ban air transportation, e.g., airport shuttle, air

per non-model aircraft, thus increasing it by taxi, air ambulance, last-mile parcel delivery,

one more unit than last year. Despite this ad- etc.; (b) substantial financial and business

justment, RPs are set to experience tremen- opportunities exist, but there are significant

dous growth following the growth trends of technological, operational, and regulatory

the non-model sUAS sector. Starting from challenges including issues involving public

18In our accounting of RPs, we take pilots who manned pilots who took online training in lieu of

passed the initial knowledge test plus current the knowledge tests.

50perceptions and acceptance; and (c) gradual of GCs, will be to “promote public confidence

integration of sUAS into the overall system in UAM safety and facilitate community-wide

may facilitate integration of UAM by around learning while capturing the public’s imagina-

2030. tion” (see https://www.nasa.gov/uamgc for

more details).

In order to understand and address the chal-

lenges identified by the studies, the new As the sector grows and new initiatives are

Grand Challenge (GC) has been initiated, taken, the Agency is keeping a keen eye on

under which NASA will host UAM ecosys- understanding the overall trends.

tem-wide challenges in 2020. Under GC,

participants will be required to execute sys-

tem level safety and integration within oper-

ationally robust and relevant environments.

The goal of the first GC (GC-1), from a series

51You can also read