ECONOMIC OUTLOOK: DON'T LOOK UP! - ALLIANZ RESEARCH 13 January 2022 - Newseria BIZNES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Photo on Shutterstock ALLIANZ RESEARCH ECONOMIC OUTLOOK: DON’T LOOK UP! 13 January 2022 04 Advanced economies will continue to outpace emerging markets in 2022 14 Regional outlooks 23 Capital markets: still benign but rising uncertainty

Allianz Research

Global growth should remain robust but uneven, with rising divergence between

advanced and emerging market economies. We expect omicron-related

EXECUTIVE uncertainty to shave off (only) up to -0.3pp of GDP growth in advanced economies

in Q1, due to increase disruptions in terms of labor and global trade. However, just

SUMMARY like in the eponymous movie, whose title we borrowed for this report, current

growth dynamics might keep us from looking up during the current phase of the

recovery. Advanced economies will continue to drive more than half of global GDP

growth (+2.2pp in 2022 and +1.6pp in 2023) while emerging markets lag — for the

first time since the global financial crisis (GFC). Our 2022 GDP forecast remains

broadly unchanged, with the Eurozone and the US expected to grow by +4.1% and

Ludovic Subran, Chief Economist +3.9%, respectively, while growth in China slows to +5.2% due to ongoing disrupti-

+49 (0) 1 75 58 42 725 ons in the real estate sector and the government’s focus on financial stability.

ludovic.subran@allianz.com

China’s lowest contribution to global GDP growth since 2015 is likely to have

negative spillover effects on emerging markets whose recovery will be shallower

Ana Boata, Global Head of Economic Research compared to past crises.

ana.boata@eulerhermes.com

Andreas Jobst, Global Head Macroeconomic and Global trade is expanding once again above the long-term average but will be

Capital Markets Research disrupted by labor and supply chain bottlenecks, amplified by omicron. We expect

andreas.jobst@allianz.com

global trade in volume to grow by +5.4% in 2022 and +4.0% in 2023. In the short

Eric Barthalon, Head of Capital Markets Research run, the omicron outbreaks will keep disruptions and cost pressures high. During

eric.barthalon@allianz.com

the next two to four months, we expect some lost value added in hard-hit sectors

Jordi Basco Carrera, Senior Investment Expert with low (or no) telework possibilities and higher supply chain driven-inflation due

jordi.basco_carrera@allianz.com

to production shortfalls in China to account for about one-third of elevated inflati-

Pablo Espinosa-Uriel, Capital Markets Research Analyst on at 1.5pp to 2.0pp in the Eurozone, the US and the UK. But we still expect a turn-

pablo.espinosa-uriel@allianz.com

ing point during the second half of this year due to: (i) a cooling of consumer spen-

Alexis Garatti, Senior Economist for ESG and Public Policy ding on durable goods, given their longer replacement cycles and the shift towa-

alexis.garatti@eulerhermes.com

rds sustainable consumption behaviors; (ii) lower input shortages as inventories

Françoise Huang, Senior Economist for APAC and Trade return to (or even exceed) pre-crisis levels in most sectors and (iii) shorter delivery

francoise.huang@eulerhermes.com

times as higher capacity eases shipping constraints.

Patrick Krizan, Senior Economist for Italy and Greece,

Fixed Income

We continue to expect pervasive supply-demand imbalances to keep inflation

patrick.krizan@allianz.com

high until the end of the first half of 2022 in both advanced and emerging

Ano Kuhanathan, Sector Advisor and Data Scientist markets. Inflation is likely to decelerate this year as the recovery becomes entren-

ano.kuhanathan@eulerhermes.com

ched, mainly reflecting the phase-out of transitory factors, fading catch-up effects

Selin Ozyurt, Senior Economist for France and Africa of goods demand and declining energy prices during the second half of the year.

selin.ozyurt@eulerhermes.com

Amid continued uncertainty about the scale and duration of inflationary pressures,

Patricia Pelayo-Romero, Expert Insurance central banks are shifting towards a more hawkish monetary stance to prevent

patricia.pelayo-romero@allianz.com

inflation from becoming embedded in expectations. We have identified 10

Manfred Stamer, Senior Economist for Emerging Europe emerging countries that are most at risk from a faster-than-expected US monetary

and the Middle East

tightening given their elevated liquidity risk and cyclical weaknesses: Argentina,

manfred.stamer@eulerhermes.com

Brazil, Chile, Egypt, Hungary, Nigeria, Romania, South Africa, Turkey, and Ukraine.

Katharina Utermöhl, Senior Economist for Europe

The fiscal impulse in Europe will be stronger than in the US this year but diminish

katharina.utermoehl@allianz.com

quickly as most countries start their consolidation path. Most emerging market

countries are reducing budget deficits and re-building fiscal space, but commodity

exporters remain vulnerable to slowing external demand from China.

2

13 January 2022

Gradually rising rates will continue to provide a benign but increasingly fragile

capital market environment. Unchanged or even lower risk premia, declining

real interest rates and excess savings have supported favorable financing condi-

tions and helped risky assets outperform while fixed income assets have strugg-

led amid rising inflation expectations. However, the positive risk sentiment un-

derpinning historically high valuations in equity markets comes with rising mar-

ket volatility and remains dependent on the continued growth momentum and

the gradual removal of crisis-related policy measures.

What could go wrong? Despite the emergence of yet another Covid-19 mutati-

on, the economic impact of the pandemic is generally weakening. We estimate

that potential disruptions to labor markets due to sanitary restrictions could put

2-3% of the value added at risk in advanced economies. In addition, tighter fi-

nancial conditions or a premature withdrawal of policy support could undermi-

ne the recovery and increase private and public sector vulnerabilities, with the

potential for cliff-edge effects in some countries. Greater divergence of fiscal

and monetary policy normalization across countries could further increase im-

balances and disrupt the recovery of international trade. As the gap between

monetary and fiscal policy stances in Europe and the US is bound to widen, there

is a rising risk of decoupling, which could feed into capital market dislocations.

The spillover effects of higher capital outflows and FX volatility as the US begins

to tighten financing conditions, the (largely) self-inflicted currency crisis in Turkey

and rising uncertainty about the implications of slowing external demand from

China could weigh on the outlook for emerging markets.

+4.1%

Global GDP growth forecast for 2022

3

Allianz Research

ADVANCED ECONOMIES WILL CONTINUE TO

OUTPACE EMERGING MARKETS IN 2022

The post-crisis recovery remains robust 2022, China will make its lowest contri- crisis trend is likely to be considerable,

but continues to be uneven, with rising bution to global GDP growth since especially in emerging markets. Ad-

divergence between advanced and 2015 in 2022 (+0.9pp, excluding 2020). vanced economies will continue to

emerging economies. Despite renewed Vaccination rates, the unwinding of drive more than half of global GDP

concerns about the evolving virus dy- supply bottlenecks and policy choices growth (+2.2pp in 2022 and +1.6pp in

namics, growth momentum has been will critically influence the scale of 2023) while emerging markets are lag-

held up by resilient consumption, rising catch-up as policy support is gradually ging the pace of the global recovery —

investments and strongly rebounding withdrawn. However, just like in the for the first time since the GFC. We ex-

global trade. We expect global output eponymous movie whose title we bor- pect this divergence to continue over

to increase by +4.1% in 2022 before rowed for this report, current growth the medium term as the still low vac-

converging to trend growth at +3.2% in dynamics might keep us from looking cination rates will keep the global

2023. The Eurozone and the US will up during the current phase of the re- economy exposed to high volatility and

grow broadly in line with the global covery. While output is expected to delays in the recovery due to the risk of

economy at +4.1% and +3.9%, respec- reach its potential level until the end of further Covid-19 variant developments.

tively. With a growth rate of +5.2% in 2022, output loss relative to the pre-

Figure 1: Global GDP growth forecast (2021-23)

2019 2020 2021 2022 2023

World GDP growth 2.5 -3.4 5.4 4.1 3.2

United States 2.3 -3.5 5.6 3.9 2.8

Latin America 0.2 -6.9 6.3 3.0 2.1

Brazil 1.4 -4.1 4.8 1.5 1.2

United Kingdom 1.4 -9.9 7.1 4.4 2.6

Eurozone members 1.5 -6.5 5.2 4.1 2.3

Germany 1.1 -4.9 2.7 3.7 2.3

France 1.8 -8.0 6.7 3.6 1.9

Italy 0.3 -8.9 6.3 4.5 2.1

Spain 2.1 -10.8 5.0 5.7 3.2

Russia 2.0 -3.0 4.0 3.0 2.5

Turkey 0.9 1.8 10.7 1.5 4.2

Asia-Pacific 4.0 -1.0 5.8 4.7 4.4

China 6.0 2.3 7.9 5.2 5.0

Japan 0.0 -4.7 1.9 2.5 1.6

India 4.1 -7.3 8.5 7.1 6.9

Middle East 0.4 -4.1 3.1 3.7 2.5

Saudi Arabia 0.3 -4.1 3.0 4.7 2.4

Africa 1.7 -2.6 2.9 3.5 3.8

South Africa 0.3 -6.4 4.4 2.0 1.4

Sources: Euler Hermes, Allianz Research

Note: fiscal year for India

4

13 January 2022

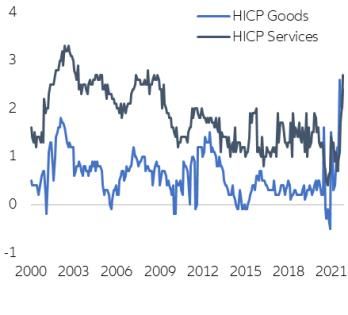

Inflation is likely to decelerate this year parts of the labor market are becom- omicron variant, it may well take until

as the recovery becomes entrenched, ing exceedingly tight, especially in sec- mid-2022 to get a better grasp on the

mainly reflecting the phase-out of tran- tors that already experienced labor stickiness of key inflation drivers, in-

sitory factors and declining energy shortages before the pandemic. The cluding supply-chain disruptions, ele-

prices in H2. The ECB and the Fed still release of pent-up demand has result- vated energy prices and the healing of

deem rising inflation to be non- ed in some overheating of Covid- the labor market3. We expect the Brent

structural but acknowledge that it is exposed sectors, such as construction, oil price to decline to USD75/barrel by

now lasting longer and has a more with limited local production capaci- the end of the year before decreasing

uncertain future path than initially ex- ties, resulting in significant price pres- by close to 10% to USD69/barrel until

pected1. While inflation expectations sures. These are particularly high in the end of 2023. Overall, we expect

have remained well-anchored, catch- countries that have closed the output average annual inflation this year to

up effects have morphed into perva- gap already2. Pockets of elevated in- remain high in 2022 at 4.4% and close

sive supply-demand imbalances push- flation are also visible in sectors with to 3% in the US and Eurozone, respec-

ing up inflation almost everywhere for stronger pricing power (automotive, tively, before declining to levels broad-

much longer than originally expected. building materials and, to some extent, ly in line with the respective inflation

Supply chains remain clogged, energy in retail and warehouse services). In the targets in 2023.

prices are still stubbornly high and context of rising uncertainty due to the

Table 2: Inflation rate forecast, %

2021 2022f 2023f

United States 4.7 4.4 2.0

Eurozone 2.6 2.8 1.8

Germany 3.2 3.1 2

France 2.0 2.6 1.9

Italy 2.0 2.4 1.3

Spain 3.1 3.9 1.8

United Kingdom 2.5 3.8 2.2

Japan -0.3 0.8 0.9

China 0.9 2.5 2.0

Sources: Markit, Euler Hermes, Allianz Research

1

For Q3 2021, the US PCE deflator declined to annualized rate of 5.3% q/q (down from 6.5% in the previous quarter) amid broadening wage pressures, but the cost of employment index has risen

to a decade-high. This raises doubts over whether inflation is still running persistently below the Fed’s longer-run 2%-inflation goal, given the accelerating catch-up during the Covid-19 crisis. The

PCE level is above target even with a 10-year look-back window.

2

Inflation prints during the last quarter of last year confirm this concern, with particularly high inflation data in Germany and the Netherlands.

3

So far, wage pressures are more pronounced in the US and spotty in the Eurozone.

5

Allianz Research

Despite negative real purchasing pow- support to spending despite declining most European countries is still signifi-

er, excess household savings will con- real purchasing power until the end of cantly below pre-crisis levels, including

tinue to support consumption in 2022- the year. Since excess savings are ac- Spain (-8%), Italy (-3.5%) and Germany

23, notably in Europe. Despite the re- cumulating in the higher net income (-2%). However, it has (almost) caught

newed Covid-19 outbreaks, pent-up bracket and the elderly, which tend to up with pre-crisis levels in Belgium

demand that turned into additional have a lower propensity to consume, (+0.2%), France (-0.9%) and the Nether-

consumption reached EUR20bn in Italy we expect that only between 20% and lands (-0.8%). We expect the consump-

(+1.2pp of GDP) and EUR5.4bn in the 40% of pent-up demand has been ab- tion recovery to lose steam in early

Netherlands (+0.8pp of GDP) in 2021. sorbed in 20214. 2022 amid tightening mobility re-

In France, Belgium and Germany, the strictions. The household spending

release of pent-up demand during In the US, consumer confidence in- preference on (durable) goods rather

summer boosted GDP by about creased by more than expected in De- than services (Figure 1) is likely to con-

+0.5pp. We expect consumer confi- cember on account of a tight labor tinue but goods-intensive catch-up de-

dence to remain positive and broadly market. The labor differential—the mand will slow. At the same time, virus

unchanged as the fear factor has re- difference between the percentage of concerns will delay the rotation of de-

duced significantly. While the saving respondents saying jobs are plentiful mand back to services, barring re-

rate reached its pre-crisis level in the and those saying jobs are hard to newed mobility restrictions due to fur-

US at end-2021, it remains +6pp above get—remains near all-time highs. As ther virus outbreaks.

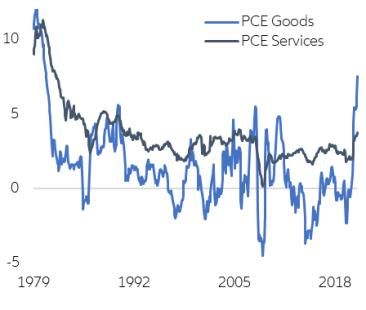

at 19% in the EU. This should provide opposed to the US, consumption in

Figure 1: Advanced economies—Domestic household consumption Figure 2: Europe—Consumer confidence indicator

(100 = average over 2010-2019)

140

135 Belgium Germany Spain

130

France Italy Netherlands

125 Total domestic household consumption 120

Durable goods

Non-durable goods 110

115

100

105 90

80

95

70

85

10 11 12 13 14 15 16 17 18 19 20 21 60

07/20

01/19

03/19

05/19

07/19

09/19

11/19

01/20

03/20

05/20

09/20

11/20

01/21

03/21

05/21

07/21

09/21

11/21

Source:s Refinitiv, Euler Hermes, Allianz Research Source:s Eurostat, Euler Hermes, Allianz Research

Note: To make the series comparable, we first mean-centered them as

of 1998 (first observation available for Italy) and rebased to 100 and

impose standard deviation to be the same as the French series.

4

We calculate the scale of dis-saving supporting consumption in hard-hit, contract-intensive sectors (wholesale & retail trade, transport, accommodation & food services) as the deviation

from underlying trend growth.

6

13 January 2022

Figure 3: Pent-up consumption in Covid-exposed sectors Figure 4: Supply-side disruptions’ contribution to inflation

(October or November 2021, pp)

10% Pent up consumption in Q2-Q3 (EUR bn, rhs) 25

7

Pent up consumption Q2-Q3 2021 (% GDP) 6

8% 20

5

Total pent up demand that could be absorbed (%

6% GDP) 15 4

4.7% 3

4% 10 2

2.9% 1

2.4%

2% 2.0% 5

1.3% 1.5% 0

1.2%

0.8% US Euro UK

0.4% 0.4% 0.3% 0.5%

0% 0

Disruption RMB Oil Others (including salaries)

France

Italy

Netherlands

Belgium

Spain

Germany

Sources: Eurostat, Euler Hermes, Allianz Research Sources: Datastream, Euler Hermes, Allianz Research

Households will increasingly allocate tial for catch-up effects this year, given point during the second half of this

their Covid-19 savings to real assets favorable funding conditions and ele- year due to three factors: (i) a cooling

(real estate, financial investments). vated corporate cash positions. Most of consumer spending on durable

Inflows into equity markets have con- companies have delayed investment goods, given their longer replacement

tinued to push up asset valuations (see decisions due to supply-chain bottle- cycles and the shift towards sustaina-

next section on the capital markets necks and input shortages. We expect ble consumption behaviors; (ii) less

outlook) and some areas of the real global capex expenditures to grow by input shortages as inventories return to

estate market are showing signs of +4.3% in volume terms this year, with (or even exceed) pre-crisis levels in

over-heating. For instance, the price-to- resilient margins, thanks to (i) to above- most sectors and (iii) declining delivery

rent ratios in France and the UK have trend demand allowing to pass-on times and transportation costs as high-

reached record highs. While some higher input prices; (ii) fixed costs being er capacity eases shipping constraints.

countries, such as France, have new amortized on greater volumes; (iii) high Shipping congestions should be less

macroprudential policies coming into liquidity (partly supported by govern- acute in H2 2022 as capacity is increas-

action (strict debt service-to-income ment guarantees, such as in France ing: global orders for new container

ratio since January this year) this is un- and the UK), and (iv) price-pressure ships have reached record highs over

likely to meaningfully slow the pace of relief on some inputs (e.g. energy). the past few months (to 6.4% of the

appreciation in the real estate sector. Cash buffers are particularly large in existing fleet). The USD17bn port infra-

the US (USD650bn) and the Eurozone structure plan in the US should also

Investment is slowly recovering, espe- (USD760bn). reduce global pressures. Container

cially in the US. Investment picked up prices (Asia to Europe, Asia to North

significantly in the US during the sec- Global trade is expanding above the America) are declining (-11% in No-

ond half of last year due to greater long-term average, once again. We vember 2021 vs peak for the global

business confidence and high levels of expect global trade in volume to grow container rate, USD per FEU) but re-

capacity utilization. Capital expendi- by +5.4% in 2022 and +4.0% in 2023. main six times above pre-pandemic

ture in several sectors (e.g. computers While short-run disruption is expected levels. However, China is expected to

and machinery and equipment) has to remain high, given the renewed keep its zero-Covid policy at least until

increased above long-term averages. Covid-19 outbreaks, we anticipate a the fall this year, which will continue to

In Europe, investment growth remains decreasing tensions for trade as trans- bring volatility into global supply

muted, suggesting a significant poten- portation bottlenecks reach a turning chains.

7Allianz Research

Figure 5: Current account balances, bn USD

United States United Kingdom

Emerging Asia (excl. China) Japan

China (mainland) Euro Area

Middle East and North Africa Latin America and Caribbean

Sub-Saharan Africa

800

300

-200

-700

-1200

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Sources: Eurostat, Euler Hermes, Allianz Research

However, external imbalances are in- As the recovery takes hold, the gradual to prevent a de-anchoring of inflation

creasing, too. In the US, the current withdrawal of monetary and fiscal pol- expectations. The Fed is already dial-

account deficit widened to -3.4% of icy support needs to ensure an effec- ing back its accommodative stance by

GDP, the highest level since 2008, and tive rotation towards private demand speeding up the pace of tapering, with

will remain high over our forecast hori- and sustainable growth. Differences in stronger inflation and growth outturns

zon (-3.0% to -3.5% of GDP). Current the normalization of policy support suggesting economic slack diminishing

account deficits are also widening in across countries has increased imbal- more quickly than anticipated. After

emerging markets, especially Latin ances across countries. On fiscal policy, accelerating the tapering of its asset

America. On the other side, China’s the fiscal consolidation in the US will be purchases until March, we expect that

current account surplus is estimated to stronger than in Europe. Most EMs are the Fed will start a two-year tightening

remain high in 2022-23 (+1.7% and reducing budget deficits, but commodi- cycle in the second quarter. The recent

+1.4% respectively) because of contin- ty exporters remain vulnerable to a surge in the long-term yields in the US

ued strong global demand for elec- downcycle in the future. On monetary indicate that markets are anticipating

tronics and China’s lower services policy, current inflationary pressures in a more aggressive monetary stance,

trade deficit as overseas travels advanced economies imply a slightly which has also increased the price vol-

slumped. The Eurozone’s current ac- more hawkish monetary stance with- atility in bond markets. The ECB is ex-

count surplus is also expected to in- out a fundamental change in the ex- pected to remain patient and tolerate

crease to above pre-pandemic levels pected hiking cycle while key EMs are some overshoot in inflation as inflation

(+3.5% in 2023) and should be boosted already hiking rates. expectations remain largely anchored

by the surplus in services. Large Euro- and wage growth spotty, with no rate

zone countries will continue to register Monetary policy is becoming less ac- hikes likely before 2023. Tapering is

opposite developments: expect the commodative. Central banks in ad- likely to be announced in December

trade surplus in Germany to widen in vanced economies have been cautious 2022 and concluded by mid-2023 with

2022, in the same way as the trade about withdrawing monetary stimulus a first rate hike expected in September

deficit in France. too early but are now moving forward 2023.

813 January 2022

Other large central banks have similar- tor, as well as (ii) cyclical weaknesses, will remain an exception, with a very

ly began shifting their forward guid- based on currency volatility & depreci- progressive normalization in ASEAN.

ance towards a less accommodative ation, inflation rates, stock and bond Conversely, China will strengthen the

monetary stance. For emerging mar- market performance as well as bond policy easing that started in July 2021

kets, rate hikes will remain the norm to spreads, we identify 10 emerging coun- through further rate cuts (at least -

contain FX depreciation as the US and tries most at risk from a faster-than- 10bp in loan prime rate in H1 2022)

other advanced economies start their expected monetary policy by the Fed: and liquidity injections (-50bp in re-

tightening cycle. Looking at two main Argentina, Brazil, Chile, Egypt, Hunga- serve requirement ratio in H1 2022,

indicators for emerging markets: (i) ry, Nigeria, Romania, South Africa, along with open market operations) to

liquidity risk, an indicator that includes, Turkey and Ukraine. We expect the stabilize economic growth and avoid

current account balance, external debt most aggressive rate hikes to come contagion risks from the real estate

repayment in 2022, imports cover rati- from Latin America, Eastern Europe sector.

os and credit growth to the private sec- and, to a lesser extent, from Africa. Asia

Figure 6: Eurozone and US-Inflation (z-score)

5

5 Eurozone

4 US

4

3

3

2

2

1 1

0 0

-1 -1

-2 -2

-3 -3

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

EZ Inflation Tracker* EZ Official Inflation Measures** US Inflation Tracker* US Official Inflation Measures**

Sources: Refinitiv, Euler Hermes, Allianz Research.

Note: */ Equally-weighted and normalized composite measure comprising 15 subsegments (underlying trends (modified/trimmed measures), forecasts, market-

based inflation measures, expected inflation implied by term structure models, monetary aggregates, consumer and producer price components, labor market

indicators, commodity prices, corporate margin & profitability and proxies for price effect from supply chain disruptions); **/ Equally-weighted and normalized

composite measure comprising headline and core inflation reported by national authorities.

Figure 7: Eurozone and US - Expected policy rates

0.4 4.0

Eurozone US

0.2

3.0

0.0

2.0

-0.2

-0.4 1.0

-0.6

2020 2021 2023 2024 2025 0.0

2020 2021 2023 2024 2025

Symmetry adj. Inertia Rule Low output gap weight rule ECB Deposit Rate

Forecast - Allianz Market Pricing (OIS) AIT augmented Inertia Rule Low output gap weight rule Fed Funds (High)

Forecast - Allianz Market Pricing (EuroDollar) Market Pricing (FFF)

Sources: Refinitiv, Euler Hermes, Allianz Research.

9Allianz Research

Figure 8: Selected advanced and emerging market economies: monetary and fiscal

stance (2021-23)

-6

Looser

US

-4

2021

2022 UK

-2 EZ

2023

Real Effective Policy Rate

BRA JPN

0

(In percent)

CHN

2

4

6

Tighter 8

-8 -6 -4 -2 0 2 4

Tighter Fiscal Impulse Looser

(In percentage points)

Sources: FAO, Euler Hermes, Allianz Research

Fiscal consolidation is underway. While East and Sri Lanka, Pakistan, the Philip- Adverse virus dynamics would slow the

the fiscal impulse in most countries is pines and India in Emerging Asia will recovery and exacerbate global imbal-

diminishing, the US has slowed fiscal be debt sustainability hot spots in ances. The emergence of yet another

consolidation while Europe will begin 2022. Covid-19 mutation has created re-

structural tightening only next year. newed uncertainty about the growth

Chinese authorities’ policy stance has Financing conditions remain favorable, outlook, though the economic impact

shifted towards easing to support do- but financial stability risks are building. of the virus is generally weakening.

mestic demand and mitigate the im- Banks remain broadly well-capitalized, Rising infection rates underscore that

pact from the real estate market. Most with capital buffers likely large enough as long as vaccination rates remain

EMs have improved their fiscal position to absorb loan losses. They have been below the coverage required to reach

due to higher government revenues, able to slowly absorb rising impair- herd immunity and continue to differ

resuming remittances, export revenues ments without a significant change in significantly between most advanced

and capital inflows. In 2021, budget their capital ratios, thanks to continued and emerging markets, virus mutations

deficits narrowed in almost all EMs borrower support and effective capital- raise the prospects of renewed lock-

compared to 2020, except for Czechia, conservation measures. However, dete- downs and keep the recovery uneven

Latvia, Nigeria, Slovakia and Tunisia riorating asset quality as support and incomplete. A new Covid-19 wave

and several emerging Asian econo- measures expire could test the ade- could significantly prolong the current

mies, though most of the latter group quacy of current loan-loss provisioning, imbalance between goods-intensive

and the three EU economies have suffi- especially in countries where private catch-up demand and squeezed sup-

cient fiscal space. However, current sector leverage is high, and banks are ply. Tighter restrictions as well as par-

budget deficits, the materialization of heavily exposed to hard-hit sectors. In tial (and more targeted) shutdowns

contingent liabilities (from state-owned some countries, there has been exces- could slow the recovery momentum

enterprises and state guaranteed sive risk-taking in a context of low inter- and decrease aggregate demand but

loans), but also increasing debt-service est rates, heightened competition and less so compared to previous waves

costs in an environment of higher inter- rising house prices. Looser lending (with real activity adjusting better to

est rates, will drive public-debt accu- standards combined with high growth stricter containment measures). The

mulation. Argentina and Brazil in Latin in residential real estate prices suggest economic implications of current virus

America; Tunisia and Ghana in Africa; that vulnerabilities might be building dynamics, especially the potential in-

Bahrain, Jordan, Oman in the Middle up. crease in the severity, transmissibility

1013 January 2022

and containment measures have yet to demand and global trade to health- put loss has been sizeable, especially in

be fully understood. We estimate that related restrictions. A slower recovery economies with higher shares of con-

omicron-related uncertainty and soft would mean additional economic scar- tact-intensive sectors, which could also

stops could shave off (only) up to - ring, with further adverse distributional be more affected by repeated virus

0.3pp of quarterly GDP growth in ad- effects and rising inequality. While waves and associated economic im-

vanced economies in Q1 2022, thanks most countries are reaching their pre- pacts (Figure 10)

to a diminishing sensitivity of domestic crisis output levels, the cumulative out-

Figure 9: Europe: expected crisis output loss vs. share of

highly-affected sectors* (2022) (in percent)

15 20 25 30 35 40 45 50

0.0

Romania

0.5 Estonia

Hungary Finland

1.0 Ireland Sweden Denmark

Latvia

Slovakia

1.5 Lithuania

Poland Bulgaria

Czech Republic

2.0 Slovenia

Luxembourg

France

2.5

Germany

Belgium Netherlands

3.0 y = 0.1648x - 3.4901

Austria

R² = 0.2783

3.5 Malta

Italy

Spain

4.0 Portugal

Sources: Refinitiv, Euler Hermes, Allianz Research

Note: */ Expected output loss based on current forecast of GDP level in 2022

relative to projected GDP level in 2022 as of end-2019 (pre-crisis); x-axis shows

the share of highly-affected sector in gross value added (GVA); chart excludes

Greece (with output loss of 9.0%) due to scaling.

Downside risk to inflation could force Core inflation in both the Eurozone where price pressures tend to be more

central banks to hasten withdrawing and the US continues to be driven in short-lived. Household spending pref-

their support and risk over-tightening large part by catch-up effects under- erences on (durable) goods rather

their monetary stance. As pandemic- pinning robust aggregate demand than services is likely to continue but

related technical/one-off factors are (Figures 10 and 11), not just supply- goods-intensive catch-up demand will

fading, one of the key questions relates side constraints (with are difficult to slow. At the same time, virus concerns

to what will happen to underlying infla- overcome with monetary policy tools). could delay the rotation of demand

tionary pressures if the emergence of Record levels of net disposable house- back to services, barring renewed mo-

the potentially more damaging omi- hold income mean that there is still bility restrictions due to further out-

cron variant slows the recovery mo- plenty of spare cash to disproportion- breaks. However, the replacement cy-

mentum and delays the pace of re- ately flow into the consumption of cle for durable goods seems to be

opening. For instance, the US Fed has goods, especially if the pandemic dis- coming to an end, which would facili-

signaled that it would act faster if ruption drags on for longer than ex- tate the adjustment of demand to

needed to keep long-term inflation pected. This might also delay the rota- tighter supply and soften price pres-

expectations and yields under control. tion of consumption back to services, sures5.

5

UN Moreover, there are upside risks for inflation: permanent costs of resilient rather than efficient supply chains, downward price rigidities in concentrated sectors, lower productivity due to

inefficient resource reallocation.

11Allianz Research Figure 10: US core inflation (y/y %) Figure 11: EZ core inflation (y/y %) Sources: Refinitiv, Euler Hermes, Allianz Research Sources: Refinitiv, Euler Hermes, Allianz Research The risk of policy mistakes is looming including the further deterioration of “known unknowns” are concerned, the large. Tighter financial conditions or a Sino-American relations and the brew- (mis-) handling of the Covid-19 crisis is premature withdrawal of policy sup- ing conflict in Ukraine, could trigger likely to take center stage in national port could undermine the recovery and another round of political risk with ad- polls. Aside from a heavy election increase private and public sector vul- verse effects on markets. schedule in Europe with key votes tak- nerabilities, with the potential for cliff- ing place in Portugal, Sweden, France edge effects in some countries. Con- Several key developments will shape and Hungary (a vote on its EU future), versely, if inflationary pressures persist, the balance of risks this year. We could the two largest economies in the world central banks could fall behind the see rising volatility around the Fed’s will also head to the polls. In China Xi curve, with overshooting inflation caus- expected tapering conclusion in March Jinping will likely embark on his third ing potential adverse wage-price feed- 2022 as markets prepare for the onset five-year mandate further cementing back effects that could stymie growth of a fresh rate hiking cycle. With the his political grip when the communist dynamics. The divergence of policy ECB a late-bloomer in rolling back its Party choses its new leadership at the normalization across countries could crisis support, the high-flying USD could 20th Party Congress in late 2022. There be disruptive to international trade weigh on the global economy and EMs will also be key elections in other large and cause adverse spillover effects to until mid-2022. For the ECB, a commu- economies (Australia, Brazil and India; emerging markets. Given the increas- nication shift in the second half of the Figure 12). Meanwhile, the Biden ad- ing divergence of the monetary and year with fresh macroeconomic fore- ministration in the US could see its poli- fiscal stance in Europe and the US, casts eventually extending as far as cy wings clipped in mid-term elections there is a rising risk of decoupling, 2025, is likely to bring interest rate in November if current polls are any- which could feed into capital market hikes back on the agenda and in turn a thing to go by. In emerging markets, dislocations. The spillover effects of further widening in Italian spreads. voters in economic heavyweights in- higher capital outflows and FX volatili- Assuming a pro-EU Italian presidential cluding the Philippines, Columbia and ty as the US begins to tighten financing candidate wins the elections scheduled Brazil will cast their votes. On the geo- conditions, the (largely) self-inflicted for late January, dynamics should re- political front, the US-China relation- currency crisis in Turkey and rising un- main manageable. On fiscal policy, a ship is likely to remain strained, with certainty about the implications of highlight includes the EU fiscal frame- the Olympic Winter Games in Beijing slowing external demand from China work reform discussions. A further likely to pose a first test as to whether for commodity-exporters could weigh standstill could seriously undermine the tensions might flare up again. on the outlook for EMs. In addition, success of the Green Deal. Political risk adverse geo-political developments, also looms large this year. As far as the 12

13 January 2022

Figure 12: Overview of General and Presidential Elections in 2022

Sources: Euler Hermes, Allianz Research

Besides accelerating the vaccination elevated debt levels of member over the near term. Rising inflation

rollout, the key policy priority is to cali- countries, reforming the fiscal rules expectations triggered by broad-

brate support to the pace of the recov- could entail shifting to an expendi- ening price pressures in recent

ery, while gradually shifting to more ture growth rule with a debt an- above-consensus inflation prints

targeted measures focusing on grow- chor, along with a permanent cen- could considerably erode the

ing firms and sectors. Another im- tralized fiscal capacity for stabili- effectiveness of forward guidance

portant challenge is to identify the po- zation and investment6. A particu- and alter the scale and duration of

tential size of the reallocative needs lar focus on climate investment monetary policy normalization (i.e.

and the role that policy should play in could also be a more efficient way the “hiking cycle”). Over the longer

facilitating reallocation in response to to progress toward the EU’s com- term, the development in labor

the scale of structural transformation. mon climate goals, given that in- markets and its impact on inflation

On fiscal policy, the US Administra- vestment returns may be higher in developments (outturn and expec-

tion will likely need to amend the countries with less fiscal space and tations) as well as the crisis impact

Build-Back-Better (BBB) Frame- that the benefits of reducing car- on trend growth, will be key as-

work to ensure Senate approval so bon emissions are felt across na- pects of the evolving stance. De-

that additional capital-spending tional borders. spite the higher stakes for credible

plans on infrastructure and climate On monetary policy, the ECB and forward guidance, with the possi-

policy can be funded and imple- the Fed should be ready to act if bility of a slightly more hawkish

mented in the near term. Without price pressures broaden and tone, we still expect the overall

the BBB, our growth forecast for threaten to become self- tightening cycle to be less aggres-

this year would materially decline reinforcing, raising the prospect of sive than suggested by current

by about 0.5pp. On the other side an adverse feedback loop be- market pricing: shallow and pro-

of the Atlantic, the EU will face a tween inflation expectations and tracted relative to historical stand-

pivotal discussion on the future of wages. In the fresh round of mac- ards in the US and little real tight-

the suspended fiscal rules and the roeconomic projections, both the ening in the Eurozone.

scope of potential changes once Fed and ECB project higher infla-

they are restored. Recognizing the tion but lower growth, especially

6

Such a reform would drastically simplify the rules and improve compliance with and enforcement of the rules. It would also implicitly take account of the differing conditions of EU countries,

by allowing high-debt countries a longer period to achieve the common debt objective than those starting with more modest levels of indebtedness and by linking expenditure growth to a

country‘s nominal growth rates. Setting up a central fiscal capacity for macroeconomic stabilization and investment could help in various ways: (i) providing incentives for compliance with the

fiscal rules by making access contingent on compliance; (ii) boosting public investment in the EU and (iii) enhancing the resilience of the Eurozone.

13Allianz Research

REGIONAL

OUTLOOKS

US: still going strong but less monetary The peak of inflation surprised on the squeeze, especially given the cash

and fiscal support upside in 2021, suggesting economic buffers of households and corporates,

slack diminishing more quickly than thanks to crisis-related support and (ii)

After +5.6% in 2021, we expect US GDP anticipated. We have revised on the pressures on prices and salaries are

growth of +3.9% in 2022 and +2.8% in upside our inflation forecast to 4.4% in much stronger today, with unemploy-

2023. The fiscal impulse of crisis- 2022 and 2.0% in 2023. We continue to ment at 4.2% (November 2021). With

related support is waning but contin- see the major drivers of this overshoot rapidly rising wages, the major upside

ues to support growth, with the focus as temporary. The Fed has already risk to the inflation forecast is that high-

shifting towards long-term spending accelerated the tapering of its asset er inflation becomes embedded in the

measures, such as infrastructure pro- purchases, and we expect the first rate economy, creating an adverse price

jects and social security. We expect the hike no later than the end of Q1 2022, feedback effects amid a tightening job

US deficit to be close to 6% of GDP followed by up to two additional rate market. While inflation expectations

against 12.5% in 2021. If the Build Back hikes this year and four rate hikes in still remain elevated, the labor partici-

Better program is further delayed (or 2023. While the projected hiking cycle pation rate remains below the long-

not approved at all by the US senate), will be protracted and shallow by his- term average (61.8% in November

we would revise down our forecast by torical standards, the time period be- 2021 compared with 64.5% since 2000)

0.5pp in 2022, 0.25pp in 2023 and tween the end of tapering and the first and artificially dampens the unemploy-

0.2pp in 2024 to account for the miss- rate hike will be shorter compared with ment rate, especially for low-skilled

ing capital spending of EUR514bn for previous episodes of monetary policy workers, which have seen a stronger

new public infrastructure until 2031. normalization (e.g. in 2014, the first acceleration of wages than their high-

Renewed restrictions due to the omi- rate hike occurred two years after the er-skilled peers. However, the partici-

cron variant are likely to reduce annu- start of tapering). There are two main pation rate is likely to normalize over

alized q/q growth by about 3pp be- reasons for this: (i) unlike after the GFC, the coming months as most support

tween Q4 2021 and Q2 2022 financial institutions and banks are in a programs are about to expire.

(assuming half the economic impact much better shape, and rising interest

compared to previous waves). rates would not create a credit

1413 January 2022

Eurozone: recovery on track but losing edly from recent highs. Moreover, Euro- remain non-structural in nature and

steam zone services should benefit from an should dissipate during the course of

improving pandemic situation, making this year as the effects of supply-

The Eurozone economic cycle will re- up for most of the output lost during demand imbalances and higher ener-

main volatile in 2022, reflecting devel- the fourth wave. In that context, still- gy prices fade. Inflation expectations

opments on the pandemic front. Fol- elevated household savings and a remain largely anchored and wage

lowing a strong consumption-led strengthening labor market - with un- growth spotty. We expect inflation at

growth spurt last summer, growth dy- employment swiftly returning to pre- 2.8% this year and 1.8% in 2023. Lower

namics turned decidedly weaker to- crisis levels - should provide fertile inflation this year will give the ECB

wards the end of 2021. In addition to ground for a pick-up in consumption breathing room to manage a gradual

prolonged supply-chain stresses keep- during the second half of the year. Fis- transition from the expiring crisis-

ing a lid on industrial prospects until cal flagship measures – including pub- related asset purchase program

mid-2022, the recovery in private con- lic business support measures and fur- (PEPP) and delay “real tapering”, i.e.

sumption – notably services - is now lough schemes – will be extended in winding down the APP program, until

also on pause as another Covid-19 the most affected countries and help January 2023. We expect a first rate

wave sweeps the region and the pick- prop up domestic demand. Eurozone hike after the conclusion of the APP in

up in inflation is hurting household pur- fiscal policy will continue to remain September 2023 – a first since summer

chasing power. As a result, Eurozone modestly supportive as some modest 2011 and the beginning of the first

GDP growth should slow to on average reforms of the suspended EU fiscal meaningful hiking cycle since late 2005

+0.5% q/q in both Q4 2021 and Q1 rules are likely to provide some breath- – more than a year after the Fed. How-

2022, down from +2% q/q in Q3 2021. ing space to national governments ever, inflation risks remain skewed to

Nevertheless, the Eurozone still kicks from 2023 onwards. Tailwinds from the the upside over the medium term. If

off the year 2022 with GDP back at pre NGEU recovery package will peak in inflation remains above target next

-crisis levels. 2022-23, contributing up to 1.5pp to year, the ECB will have to shift its cur-

GDP growth. Overall, GDP growth is rent monetary policy stance much

Following a weak start to the year, the forecast to slow to +4.1% in 2022 and more abruptly than currently envi-

Eurozone’s growth stars will once +2.3% in 2023 after +5.2% last year. sioned, which could weigh on the

again realign come spring, with quar- growth dynamic and raise financial

terly GDP growth rising above +1% q/q Similar to the US, the inflation over- stability concerns.

between April and September. For one, shoot in the Eurozone is proving more

supply-side challenges should start to pronounced and stickier than initially

fade and energy prices recede mark- expected but current price pressures

15Allianz Research

Germany: no longer leading the Euro- 19-related restrictions hinder the nor- 2.0% in 2023, but remain convinced

zone recovery malization of services demand. Ser- that elevated inflation remains non-

vices that require direct customer inter- structural.

While Germany originally fared better action, such as the leisure industry and

than most Eurozone economies during hospitality as well as physical retail Creative fiscal maneuvering will allow

the crisis, its growth momentum sub- services, are likely to be particularly for a more, albeit limited, expansion of

stantially weakened in late 2021. With affected, but some of the economic fiscal policy in the coming years. Addi-

2021 GDP growth at +2.7%, according impact would be cushioned by public tional below-the-line investment

to our current estimates, the region’s support measures, which we expect to spending aimed at circumventing the

largest economy has fallen not only be extended until at least end-March. constitutionally-enshrined debt brake

behind France but also Italy in its re- Most of the output lost during the win- will still see total deficit spending

turn to pre-crisis GDP levels. Growth is ter wave should be made up over the capped at about 1% of GDP between

likely to pick up to +3.7% this year be- course of 2022. On the whole, the 2023 and 2025. Moreover, the fiscally

fore slowing to +2.3% in 2023. No ma- growth impact should prove less se- conservative Liberal Party, the junior

jor leaps can be expected from Ger- vere than in previous waves as con- coalition partner in the new German

man industry until Q2 this year, when sumers have already adjusted their government in charge of the finance

we expect supply-side bottlenecks to behavior. Inflationary pressures due to ministry is expected to keep fiscal plans

ease and energy prices to moderate. base and reopening effects have been in check. Still, a precedent of circum-

Consumption, the most important driv- stronger and more long-lasting than venting the debt brake will be set. Ex-

er of the recovery, is likely to decelerate initially thought but are still non- pect off-balance-sheet debt to remain

during the next few months as catch- structural. We have revised up our in- a feature of German fiscal policy in the

up demand fades and renewed Covid- flation forecast to 3.1% this year and coming years.

France: strong momentum from con- Like in other Eurozone countries, infla- In a context of a positive labor market

sumer confidence as the labor market tion (CPI) rose significantly to an aver- outlook, maintaining purchasing power

begins to tighten age of 2% last year (after 0.5% in 2019) will emerge as the dominant economic

and will remain elevated in H1 2022 topic of the presidential elections that

While the renewed Covid-19 wave has before decreasing slightly to 2.0% by will take place in April 2022 (at a time

muted rising business and consumer the end of the year (2.6% on average in when France will also hold the EU pres-

confidence during the last quarter, the 2022). On the back of the dynamic la- idency). President Macron is expected

economic implications seem limited so bor market recovery, the unemploy- to run again but has not yet officially

far and concentrated on lower-than- ment rate is expected to decline further declared his candidacy. Recent opinion

expected tourism activity. In Q1 2022, from 8.1% in Q4 to 7.8% in H1 2022. polls indicate that he would be the

we expect real activity to slow slightly However, long-lasting structural issues lead candidate in the first round (27%

as infections peak, followed by a pro- (e.g. the lack of qualified workers, skill voting intentions). Valérie Pécresse, the

gressive normalization during the re- mismatches and little incentives to take candidate of the conservative party

mainder of the quarter; we expect up work) will prevent a significant drop (LR) appears to take a similar stance to

growth at +0.2% q/q, with an estimated of unemployment below the pre-crisis Macron on tax policy but has advocat-

-0.3pp drag on activity from the re- level of 7.5%. Amid higher consumer ed for greater fiscal discipline – with

newed Covid-19 outbreak. Private con- prices, wages pressures are set to in- the aim of cutting public debt to GDP

sumption will continue to drive growth tensify, in particular in tradable ser- to 100% (by -14pp) in ten years. So far,

this year as real purchasing power will vices. We expect average wage growth the campaigns have been mostly silent

remain slightly positive. We expect to increase to +2.5% in 2022 (up from on economic policies to tackle the chal-

overall GDP growth to reach +3.6%, 1.8% in Q4 2021). lenges from the “green transition”.

followed by +1.9% next year.

1613 January 2022

Italy: strong short-run momentum but major source of growth support as recovery plan and major structural

long-term challenges households draw down their excess reforms (e.g. legal procedures, retire-

savings, with the savings rate projected ment age). However, the initiated re-

Italy continues to experience a very to decline from 14% to 10% of disposa- forms and the effects of the NGEU in-

dynamic recovery, with private con- ble income. We expect GDP growth to vestments will only have a noticeable

sumption and foreign trade being the reach +4.5% this year, followed by impact on potential growth in the me-

main drivers of a strong growth im- +2.1% in 2023. dium term. We estimate a cumulative

pulse during the second half of last growth impact of around 2.0% until

year. In the short run, high-frequency Inflationary pressures have remain 2026. But by frontloading fiscal expan-

indicators are signaling a continued contained. We expect inflation to rise sion and delaying consolidation efforts

expansion of economic activity, espe- only moderately to 2.4% this year (up after 2024, public finances will become

cially in the manufacturing sector from 2.0% last year). The current infla- more sensitive to interest rate risk. In an

where the PMI reached an all-time tion differential to Germany is close to environment where signs point to a

high of 62.8pts in November. GDP an all-time high of 1.4pp, which should tightening of monetary policy, this may

growth is now clearly above the Euro- support the relative price competitive- cause tensions in the future, especially

zone average, which resulted in a re- ness of Italian manufacturing, which on sovereign bond markets. The up-

cent rating upgrade by Fitch from tends to be more price elastic com- coming presidential elections could

“BBB-“ to BBB. GDP is now only 1.4% pared to that of Germany. In 2022, the become a significant downside risk

below the pre-crisis level, similar to difference should remain at 0.7pp, when the seven-year mandate of Ital-

Germany despite Italy’s much stronger which can be explained, among other ian president Sergio Mattarella comes

recession in 2020 (-9.0% vs -4.9%). things, by subdued wage pressure to an end in February 2022. Prime Min-

While Italy is expected to reach its pre- (+0.6% in 2022), with a still high unem- ister Mario Draghi signaled his willing-

crisis GDP level in mid-2022, it will ployment rate of 9.1% next year. It will ness to be a candidate and if he were

probably not be able to close the out- be partly compensated by government to run and be elected, a government

put gap until 2023. The renewed sani- spending as the effects of the recovery reshuffle or snap elections could be on

tary restrictions in response to the fifth plan unfold and fiscal policy remains the cards. If Mario Draghi were to

Covid-19 wave may shave off 0.2pp of expansive (-5.6% deficit in 2022 and no leave office, the specter of Italy’s fiscal

quarterly growth in Q4 and Q1. But a return to -3% level before 2025). policy could return at a time when the

significant part of these costs may only ECB exits from its crisis-related asset

occur if tightened travel restrictions Mario Draghi’s national unity govern- purchase program (PEPP) and Europe-

affect tourism. In the coming quarters, ment continues to deliver, especially on an leaders start discussing the future of

private consumption will remain the the adoption of the roadmap for the the EU fiscal rules.

17Allianz Research

Spain: steady recovery with the best the Spanish economy, of which around weak due to high structural unemploy-

yet to come 40% will be allocated to climate policy ment. Job creation was particularly

and renewable energy generation. strong in hospitality, arts and entertain-

Spain has experienced the largest eco- Improving labor market conditions, ment, IT and communications. Labor

nomic scarring amongst the Euro- favorable financing conditions and the markets have been more resilient than

zone’s big economies but has coped NGEU funds will be key drivers of in previous crises as efforts to put in

well with the renewed wave of virus growth in 2022 by boosting private place job-retention schemes seem to

infections. While the economic impact consumption and investment. Howev- have paid off. We expect a return to

of moderate sanitary restrictions has er, expected inflation close to 4% this the pre-pandemic unemployment rate

been limited, the delayed rebound in year, especially high energy prices, will of 13.9% this year, thanks to the exten-

tourism limits positive spillovers from weigh on households’ real purchasing sion of the partial unemployment

strong growth of +2% q/q during the power. We expect GDP growth to be scheme until February 2022. Risks to

final quarter of 2021. The continued +5.7% this year, followed by +3.4% in employment stem from the predomi-

fiscal impulse until 2023 will support 2023. nance of SMEs, which are more vulner-

greater public investment, while the able to liquidity shocks, and from the

funds from the NGEU recovery pack- Despite a significant rebound in job high share of temporary contracts.

age will inject a total of EUR70bn into growth, the labor market remains

UK: starting the normalization to the new wave of infections will delay the pace of tapering, which will not

catch-up effects but not derail them, start until the policy rate reaches 0.5%

Strong domestic demand has support- shaving -0.3pp off real UK GDP growth at least, so not before H2 2022. With a

ed the recovery on the back of improv- at the turn of the year. markedly lower share of household

ing business sentiment. We expect GDP mortgages at variable rates, the

growth to reach +4.4% this year, fol- The Bank of England has commenced squeeze in cash flow from the rise in

lowed by +2.6% in 2023. We expect a cautious tightening cycle to keep interest rates should remain limited.

business investment to continue to re- inflation expectations anchored and

cover (+5.8%) as disruptions to global prevent an adverse wage-price loop in Fiscal consolidation is underway. The

supply chains delayed some decisions light of rising wage pressures. House- UK has already started the post-crisis

last year. Non-financial corporates still hold inflation expectations have risen fiscal consolidation, with a focus on

accumulate cash at a higher speed to their highest level since 2013, with revenue measures. The threshold for

compared to their pre-crisis pace, with two-thirds of current inflationary pres- personal tax allowances for house-

cash buffers having risen to GBP138bn sures driven by higher energy prices, holds is frozen as of this year for four

(i.e. 6% of GDP), which should boost tax increases, Covid-19 related base years and, as of April 2023, the corpo-

capital expenditure. Tight labor mar- effects and supply-chain bottlenecks rate tax rate for companies with profits

kets will keep wage growth at 3.5% in (which were amplified by Brexit). We of GBP250,000 or greater (around 10%

2022 and 3% in 2023. Hence, the fall in expect price pressures from supply-side of firms) will be raised from 19% to

real disposable income is expected to constraints to remain high during the 25%, slightly above the advanced

remain moderate (-0.3% in 2022) and first half of this year, which should add economy average. Overall, the an-

above-pre-crisis household savings more than +1pp to headline inflation nounced tax hikes will increase the tax

(+5pp of gross disposable income) will (3.8%). Energy prices are also likely to burden from 34% to 35% of GDP in

continue to boost consumer spending stay elevated due to the revision of the 2025-26, its highest level since the late

this year (+6.3%), before slowing down energy price cap in April 2022. We do 1960s. Renewed Brexit-related

next year (+2.7%). We estimate that not see the BoE going beyond a maxi- challenges could amplify supply-chain

only half of the pent-up demand was mum of three rate hikes in 2022 (with disruptions this year. The UK was the

absorbed by consumer spending last two being our baseline for the time only G7 country to experience a fall in

year. Restrictive measures in response being). The hiking cycle will determine exports in volume in 2021 (-2.8%).

18You can also read