Reducing volatility for a linear and stable growth in a cryptocurrency

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

EXAMENSARBETE INOM DATATEKNIK, GRUNDNIVÅ, 15 HP STOCKHOLM, SVERIGE 2021 Reducing volatility for a linear and stable growth in a cryptocurrency Encourage spending, while providing a stable store of value over time in a decentralized network GUSTAF SJÖLINDER CARL-BERNHARD HALLBERG KTH SKOLAN FÖR KEMI, BIOTEKNOLOGI OCH HÄLSA

Reducing volatility for a linear and stable growth in a cryptocurrency Encourage spending, while providing a stable store of value over time in a decentralized network Reducering av volatilitet för en linjär och stabil tillväxt i en kryptovaluta Uppmana användning, samt tillhandahålla ett värdebevarande över tid i ett decentraliserat nätverk Gustaf Sjölinder Carl-Bernhard Hallberg Degree Project in Computer Engineering First cycle,15 ECTS Stockholm, Sverige 2021 Supervisor at KTH: Luca Marzano Examiner: Ibrahim Orhan TRITA-CBH-GRU-2021:047 KTH The School of Technology and Health 141 52 Huddinge, Sverige

Sammanfattning Internet gav människor möjlighet att utbyta information digitalt och har förändrat hur vi kommunicerar. Blockkedjeteknik och kryptovalutor har gett människan ett nytt sätt att utbyta värde på internet. Med ny teknologi kommer möjligheter, men kan även medföra problem. Ett problem som uppstått med kryptovalutor är deras volatilitet, vilket betyder att valutan upplever stora prissvängningar. Detta har gjort dessa valutor till objekt för spekulation och investering, och därmed gått ifrån sin funktion som valuta. För att en valuta ska anses som ett bra betalmedel, bör den inte ha hög volatilitet. Detta är inte bara begränsat till kryptovalutor, då till exempel Venezuelas nationella valuta Bolivar är en fiatvaluta med historiskt hög volatilitet som förlorat sin köpkraft på grund av hyperinflation under de senaste åren. Med detta i åtanke föreslår vi en ny kryptovaluta; Dynamic Network Token, vars uppgift är att reducera volatiliteten i en kryptovaluta genom att reglera utbudet dynamiskt med hjälp av burning och minting. Denna implementeringsuppgift är att minska hög volatilitet till fördel för en mer stabil och linjär tillväxt och samtidigt uppmana användare att använda Dynamic Network Token mellan varandra i nätverket. Nyckelord Kryptovalutor, Volatilitet, Burning, Minting, Dynamiskt, Värde, Investering, Stabil, Tillväxt

Abstract The Internet provided humans a new way to exchange information digitally and has changed how we communicate. Blockchain and cryptocurrencies have given humans a new way to exchange value over the internet. With new technology, new possibilities arise, but not always without issues. One problem that has risen with cryptocurrencies is their high volatility, meaning that the currency has big price swings. It has made these currencies objects for speculation and investment almost exclusively, and therefore they have lost their functionality as a currency. For a currency to be viewed as a good means of payment, it cannot be associated with high volatility. This is not only restricted to cryptocurrencies, as for example the Venezuelan Bolivar is a fiat currency with historically high volatility and has been losing its purchasing power due to hyperinflation in the recent years. In regard to this we propose a new cryptocurrency; the Dynamic Network Token, which aims to reduce the volatility in a cryptocurrency by regulating the supply dynamically with burning and minting. The implementation of this functionality will strive to remove the high volatility in the token for the benefits of a more stable and linear growth, and at the same time encourage users to transact with the Dynamic Network Token between each other. Keywords Cryptocurrencies, Volatility, Burning, Minting, Dynamic, Value, Investing, Stable, Growth

Acknowledgment To whom it may concern, the authors are grateful for the aid received during the work done in this thesis project. - Vires in numeris.

Glossary Bitcoin - The first cryptocurrency. It uses proof of work for validating transactions on its blockchain and has a hard cap. Blockchain - A distributed digital ledger, storing blocks of transactions made with the native currency related to the specific blockchain. It is maintained and validated by nodes in a decentralized peer-to-peer network. Burning - A method that removes tokens from the total supply. Cryptocurrency - A digital currency recording transaction in a decentralized network using cryptography. Ether - The native token of the Ethereum protocol. Ethereum - A cryptocurrency ecosystem powered by the EVM (Ethereum Virtual Machine) allowing for the deployment of smart contracts and decentralized apps. Ethereum test-net - Ethereum development network used for developing and testing cryptocurrencies and other decentralized applications. Two examples are the Goerli and Ropsten test networks. ERC20 - A token deployed on the Ethereum blockchain as a smart contract. EVM - Ethereum Virtual Machine. Fiat Currency - A physical currency such as the U.S dollar and Swedish krona controlled by the government. Hard Cap - A cryptocurrency with a finite supply. Market Cap - The total value of a fiat currency invested in an asset, often nominated in dollars. In cryptocurrencies the market cap is calculated by multiplying price with circulating supply. Miner - A computer that solves a computational problem to verify Bitcoin transactions. Minting - A method that adds tokens to the total supply. OpenZeppelin - A library provider for developing cryptocurrencies.

Residual - A measurement of how far a data point is from a regression line. Smart Contract - A self-executing transaction protocol with terms of agreement between a buyer and a seller being written in code that is deployed on a blockchain. Stable Coin - A cryptocurrency, which is pegged to a fiat currency, i.e., has a 1:1 ratio. Tether - A stable coin with a 1:1 ratio to the U.S dollar. Token - A type of cryptocurrency representing an asset residing on a blockchain. It is fungible and tradable, meaning that one token is always equal to another making it suitable for transactions.

Table of contents 1 INTRODUCTION ................................................................................................... 1 1.1 PROBLEM .................................................................................................................................... 1 1.1.2 SUPPLY AND DEMAND ............................................................................................................... 2 1.1.3 VOLATILITY IN CRYPTOCURRENCIES ........................................................................................... 3 1.1.4 HYPERINFLATION ...................................................................................................................... 4 1.2 GOALS ........................................................................................................................................ 5 1.2.1 THE DYNAMIC NETWORK TOKEN ............................................................................................... 5 1.2.2 CAUSES FOR VOLATILITY IN CRYPTOCURRENCIES ....................................................................... 6 1.2.3 CONTROL OF VOLATILITY IN CRYPTOCURRENCIES ....................................................................... 6 1.2.4 REGULATE GROWTH IN CRYPTOCURRENCIES .............................................................................. 7 1.2.5 SELECTION OF PARAMETERS ..................................................................................................... 7 1.3 DELIMITATIONS ............................................................................................................................ 8 1.4 CONTRIBUTION OF AUTHORS ........................................................................................................ 9 2 THEORY AND BACKGROUND ......................................................................... 11 2.1 INFLATIONARY CURRENCIES ....................................................................................................... 12 2.2 DEFLATIONARY CURRENCIES ...................................................................................................... 12 2.3 BITCOIN .................................................................................................................................... 13 2.4 ETHEREUM ................................................................................................................................ 14 2.4.1 SMART CONTRACTS ................................................................................................................ 14 2.4.2 ERC-20 TOKEN ...................................................................................................................... 15 2.4.3 BURNING AND MINTING IN AN ERC20 ....................................................................................... 16 2.4.4 DEPENDENCY OF ETHEREUM................................................................................................... 17 2.5 TETHER .................................................................................................................................... 17 2.6 BLACK-SCHOLES PRICING MODEL ............................................................................................... 18 2.7 REAL WORLD USE CASES............................................................................................................ 18 2.7.1 IMPLICATIONS OF DYNAMIC NETWORK TOKEN .......................................................................... 19 2.8 RELATED WORK ......................................................................................................................... 20 2.8.1 BURN AND MINT IN CRYPTOCURRENCIES .................................................................................. 20 2.8.2 BURN MINT EQUILIBRIUM ......................................................................................................... 21 2.8.3 RELATED PRICE MODELS ......................................................................................................... 22 2.8.4 EVALUATION MODELS .............................................................................................................. 22 2.8.5 RELEVANCE OF RELATED WORK ............................................................................................... 22 3 METHODOLOGY ................................................................................................ 25 3.1 ROAD MAP ................................................................................................................................ 25 3.2 LITERATURE STUDY ................................................................................................................... 26 3.2.1 WHITEPAPERS AND REPORTS .................................................................................................. 27 3.2.2 DOCUMENTATION ................................................................................................................... 27 3.3 TOOLS ...................................................................................................................................... 28 3.3.1 OPEN-ZEPPELIN ..................................................................................................................... 28 3.3.2 INTEGRATED DEVELOPMENT ENVIRONMENTS ............................................................................ 28 3.4 BURNING AND MINTING ............................................................................................................... 29 3.4.1 BURNING................................................................................................................................ 30 3.4.2 MINTING................................................................................................................................. 33 3.5 ALTERNATIVE METHODS FOR CONTROLLING THE VOLATILITY ......................................................... 35 3.6 SIMULATION OF PRICE ................................................................................................................ 36

3.6.1 JAVA PROGRAM ......................................................................................................................36 3.6.2 VOLATILITY AS STANDARD DEVIATION .......................................................................................37 3.6.3 GEOMETRIC BROWNIAN MOTION ..............................................................................................37 3.6.4 BLACK-SCHOLES MODEL .........................................................................................................38 3.6.5 GEOMETRIC BROWNIAN MOTION PROGRAM...............................................................................39 3.7 ALTERNATIVE SIMULATION METHODS ...........................................................................................40 3.7.1 CONSTANT ELASTICITY OF VARIANCE ........................................................................................40 3.7.2 SABR VOLATILITY MODEL ........................................................................................................41 3.8 LINEAR REGRESSION MODEL .......................................................................................................41 3.8.1 R-SQUARED AND RMSE..........................................................................................................42 3.9 TESTING OF THE TOKEN ..............................................................................................................43 3.9.1 METAMASK AND ETHERSCAN ...................................................................................................43 3.9.2 TRUFFLE AND GANACHE ..........................................................................................................44 4 RESULTS ............................................................................................................ 45 4.1 PRICE SIMULATION .....................................................................................................................45 4.1.1 UNREGULATED PRICE ..............................................................................................................45 4.1.2 REGULATED PRICE ..................................................................................................................45 4.2 COMPARISON OF PRICE SIMULATIONS ..........................................................................................46 4.3 EVALUATION OF LINEAR REGRESSION ..........................................................................................49 4.3.1 LINEAR REGRESSION WITH REGULATION ...................................................................................50 4.3.2 LINEAR REGRESSION WITHOUT REGULATION .............................................................................51 4.3.3 COMPARISON OF REGRESSION MODELS ....................................................................................53 5 ANALYSIS AND DISCUSSION .......................................................................... 55 5.1 INTERPRETATION OF PRICE SIMULATIONS .....................................................................................55 5.1.1 RELIABILITY OF SIMULATED RESULT ..........................................................................................55 5.2 ACCURACY OF REGRESSION MODELS ..........................................................................................56 5.3 IMPACTS OF THE DYNAMIC NETWORK TOKEN...............................................................................56 5.3.1 ECONOMICAL IMPACT ..............................................................................................................56 5.3.2 SOCIAL AND ETHICAL IMPACT ...................................................................................................57 5.3.3 ENVIRONMENTAL IMPACT .........................................................................................................58 5.4 ASSUMPTIONS ...........................................................................................................................58 5.5 BLACK-SCHOLES FOR CRYPTOCURRENCIES.................................................................................59 5.6 CHOICE OF BURN AND MINT METHOD ...........................................................................................59 5.7 CHOICE OF SIMULATION METHOD ................................................................................................60 5.8 REALISTIC PRICE SIMULATION .....................................................................................................61 5.9 RESTRICTIONS AND LIMITATIONS .................................................................................................61 6 CONCLUSIONS .................................................................................................. 63 6.1 FUTURE WORK ...........................................................................................................................63 7 REFERENCES .................................................................................................... 65 APPENDIX A - LINEAR REGRESSION MODELS ................................................ 77 APPENDIX B - BLACK SCHOLES AND GBM CODE .......................................... 79 APPENDIX C - REMIX TRANSFER FUNCTION ................................................... 81

1 Introduction | 1 1 Introduction This chapter intends to lay out the introduction of this paper as well as presenting the problem set to solve for this thesis project. In section 1.1, the problem regarding volatility will be presented along with crucial concepts related to the problem. Section 1.2 will formulate the goals of the work and section 1.3 will set the delimitations to reduce the workload to something comprehensible. To finish this chapter, section 1.4 will discuss the contribution of the authors. A digital currency seems less unintuitive today than ever before. Humans have gone from using physical means of payments such as metals commodities or cash, to almost paying everything with credit cards [1]. With Bitcoin becoming a household name and the rapid growth of adoption for cryptocurrencies [2], the birth of a new form of transacting value emerges. This new way of transacting contrasts with the traditional credit or debit card, fully decentralized and uses the distributed ledger of a blockchain with no middle hand intervening, delaying, or taking a percentage on the transaction [3]. The functionality and capabilities of the blockchain and cryptocurrency technology seems promising, but it still is in its infancy and needs improvement. As with most new technologies, for example as with the electric car manufacturer Tesla, their cars were more inclined to catch on fire in the early days than they are now. According to their vehicle safety report, the rate of a fire related accident has dropped from one each 170 million miles to one each 205 million miles between 2018 and 2020 [4]. This is a good example of how new technologies may experience problems in the beginning, but still have great use cases which will improve and bring benefits for the world in the long run. This is the case with cryptocurrencies as a means of payment. Bitcoin, which was intended as a means of payment or “electronic cash” [5], is almost solely viewed as a store of value because of its deflationary properties [6]. 1.1 Problem In recent years, the popularity and interest in cryptocurrencies has grown rapidly and it is not slowing down. As this asset class is in its infancy, its place in society is not clear nor well defined. Today we view cryptocurrencies as currencies and not as

2 | 1 Introduction securities or commodities [7], which put them in the same category as any other fiat- currency such as the Swedish krona or the U.S dollar. But even though cryptocurrencies are viewed as a form of currency, they share many attributes of commodities and securities, as they are subject to volatility and price speculation. In most cases the volatility is greater than that of commodities like gold or oil [8]. This creates a problem for the asset class, as it is not a property suited for a currency. According to Gresham's Law [9], bad money will drive out good money in a society. This means that currencies with the same face value in a society will experience a higher circulating supply (i.e., higher spending) of the currency that is viewed as less good, as the good money will be more desirable to keep [10]. This principle can in a way be applied to cryptocurrencies against fiat currencies when it comes to spending because of the volatility associated with cryptocurrencies. This is because it creates an opportunity to capitalize on volatility to the upside, as well as lose purchasing power if the cryptocurrency experiences volatility to the downside. To create more of an equilibrium and to get users of cryptocurrencies to spend the currencies, the volatility must be removed or reduced significantly to encourage spending. For example, if you look at Bitcoin which as of 8th of April 2021, is the number one cryptocurrency by market cap [11], it has gone from being created with an intention to be used as a means of payment between two parties without a middle hand [5], to now be viewed as a store of value similarly to gold or an investment opportunity. This is a direct consequence of its high volatility to the upside and has led to less spending and more holding and trading of the asset. Another consequence is when the volatility is high to the downside, as Bitcoin loses its purchasing power. Meaning that the holders of Bitcoin cannot buy as much as before due to high drops in value compared to its fiat pairing. The result of volatility to the upside and the downside is the discouragement of spending, as the stability of Bitcoins value becomes speculative and unpredictable. 1.1.2 Supply and demand Volatility arises consequently from an uneven balance between buyers and sellers in any given asset. When there are more buyers than sellers, the price goes up and vice versa. This phenomenon is what is known in economic theory as supply and demand, and it is the standard model used to evaluate the price of any commodity or asset of today. The supply and demand theory states that; if the demand is high, but the supply is scarce or getting scarcer with the same demand, it will increase the price of the asset in the upwards direction. The same goes for the opposite; if the supply is

1 Introduction | 3 high and the demand is low or the demand is low and the supply is increasing, this will create an uneven balance of the price in the downwards direction [12]. When it comes to commodities like gold for example, the supply can be viewed as limited. This is because the process of extracting gold is not only time consuming but also hard due to the rarity of the metal [13]. This restriction of supply is one of the main factors making gold historically looked upon by most people and societies as a store of value or an investment [14]. As the supply is low and the demand is high, this creates a rise in price. 1.1.3 Volatility in cryptocurrencies Bitcoin is known to be an asset associated with high volatility. In 2017 it experienced a 1318% increase in price, making an unforgettable impact in the financial world when reaching its high of 19114 U.S dollars in late 2017. Figure 1.1: Chart of Bitcoin in U.S Dollars between Sep-16 to Jan-18, Source: Thompson, 2021. In mid-2018 the price of Bitcoin dropped 72.6% from its peak, creating a yearly range from 16477 down to 3314 dollars. As can be seen, both the positive and negative years when it comes to price for Bitcoin can be considered extremes. Even the average annual return from Bitcoin is 408.8%, which also can be considered extreme [15]. Bitcoin is not the only cryptocurrency experiencing this extreme price volatility. Both the number two and three cryptocurrencies Ethereum and Binance Coin, behave in the same way in regard to volatility [16] which can also be seen in figure 1.2. For instance, Binance Coin, which is a relatively young currency in comparison to Bitcoin, has experienced an increase in price like Bitcoin in its infancy. In the span

4 | 1 Introduction of three years, Binance Coin has had a 4635% increase in price which furthermore proves the volatility in the cryptocurrency market [11]. Figure 1.2: Chart of Ethereum and Binance Coin’s volatility between Feb-17 to Mar-20. Source: Cryptoz.ai, 2018. 1.1.4 Hyperinflation Cryptocurrencies are custom to volatility as described in section 1.1.2. This can be seen on the price over time graphs for most of the cryptocurrencies [17]. But cryptocurrencies are not the only currencies experiencing high volatility, as traditional types of fiat currencies can experience what is known as hyperinflation. All fiat currencies of today experience inflation to some degree, due to the government's ability to print more money. This means that the purchasing power of the currency weakens over time, resulting in a price increase of goods and services [18]. Hyperinflation can be viewed as inflation, with the main difference being the rate of the weakening of the currency. If the rate of inflation grows with more than 50 percent per month, the currency is experiencing hyperinflation [19]. A good example of hyperinflation in a fiat currency would be the Bolivar, which is the national currency of Venezuela. In comparison to the U.S dollar, the Bolivar has gone from being worth 0.232558 per one dollar in 2012, to zero per one dollar as of April 20th, 2021 [20].

1 Introduction | 5 Figure 1.3: 10-year chart of the Bolivar in comparison to the U.S Dollar. Source: Xe.com. This is not exclusive to the Venezuelan bolivar, as there have been many cases of hyperinflation in history. For example, the Zimbabwe dollar experienced it a decade ago, peaking out in 2008, resulting in the discontinuation of the local currency the Zimbabwe dollar [19]. When a nation experiences hyperinflation, the usual response is that the people seek to store their wealth in some other currency, commodity, or asset. But as no fiat currency is immune to inflation and commodities or assets do not provide a good way to transact in day-to-day life, the cryptocurrency developed in this thesis can provide a solution to the problem. 1.2 Goals This section intends to present the goals for this thesis project, giving a clear insight into what needs to be done when developing the cryptocurrency in regard to the problem of volatility postulated in section 1.1. In 1.2.1 the presentation of the token developed called the Dynamic Network Token will be laid out, and by narrowing down the theoretical work needed to four specific topics presented under 1.2.2, 1.2.3, 1.2.4 and 1.2.5, the goals of the thesis become more tangible for the development of the cryptocurrency. 1.2.1 The Dynamic Network Token The practical goal for this thesis is the development of a cryptocurrency that will be called Dynamic Network Token or in short, DNT. This development will be done with the aim of trying to solve the problem of volatility in cryptocurrencies described in 1.1. For the development to succeed, the topics brought up in the other subsections needs to be addressed and studied. If these topics can be answered and implemented

6 | 1 Introduction in the Dynamic Network Token, the practical goal of creating a less volatile cryptocurrency will be achieved. To summarize the goals that needs to be achieved in the implementation of the Dynamic Network Token, which are separately described in the subsections 1.2.2, 1.2.3, 1.2.4 and 1.2.5, the following questions and its relevant concepts must be understood and studied: ● What causes the volatility in cryptocurrencies? ○ Hard caps ○ Supply and demand ● Can the volatility be controlled in a cryptocurrency? ○ Burning ○ Minting ● Is it possible to regulate the growth so it becomes more linear and stable? ○ Linear growth ○ Wiener process and geometric Brownian motion ○ Burn-to-mint ratio 1.2.2 Causes for volatility in cryptocurrencies For the project to succeed, the question of what factors causing the volatility in cryptocurrencies must be derived. Concepts such as supply and demand discussed in section 1.1.2, in combination with concepts such as hard caps and deflationary currencies described in 2.1, will bring more clarity to the causes behind the volatility. The goal of identifying the reasons behind the volatility will make it possible to focus on controlling these aspects when implementing the functionality for the Dynamic Network Token. This results in us understanding regarding what creates or does not create the volatility in other cryptocurrencies. 1.2.3 Control of volatility in cryptocurrencies As cryptocurrencies can be viewed as programmable money [21], the reduction of the volatility will be achieved through taking the methodological approaches using functionalities such as minting and burning in the smart contract protocol governing the Dynamic Network Token. Minting and burning itself is adding and subtracting tokens from the total supply of the token, which will create a possibility to regulate the price of the token.

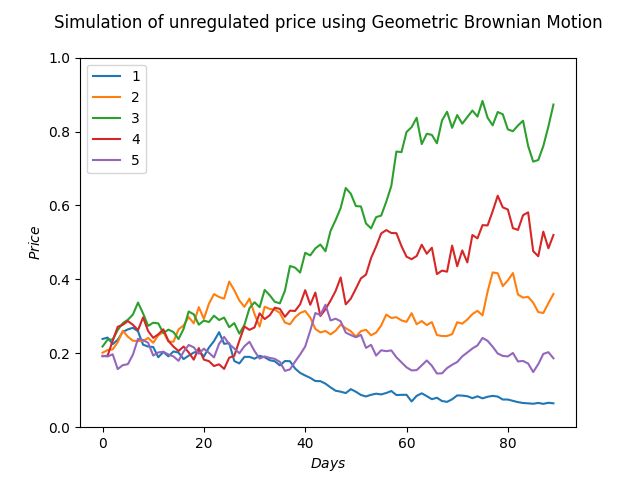

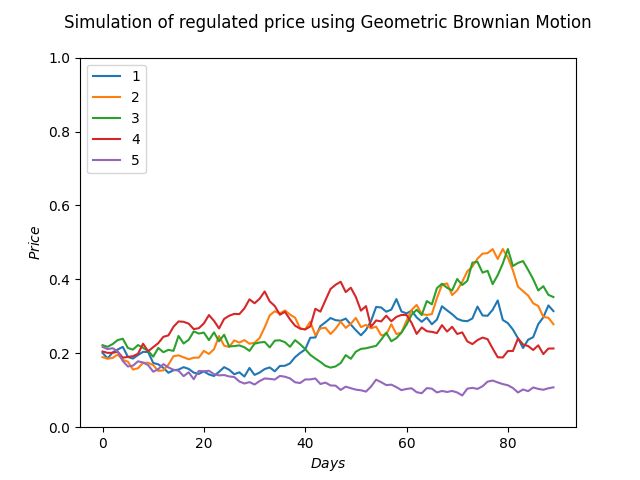

1 Introduction | 7 Minting implies as with traditional central banks, following the monetary banking system [22], the printing of money. In the case for a cryptocurrency, the minting implies adding coins or tokens to the total supply. Burning is the concept of reducing the total supply by sending coins or tokens to a “black hole” address [23], making these coins or tokens non-retrievable. This will create a regulation in the supply of the currency, making it scarcer. By the knowledge gained from studying causes for volatility in other cryptocurrencies as mentioned in section 1.2.1, the practical focus can be targeted at developing functionality preventing volatility in the Dynamic Network Token. 1.2.4 Regulate growth in cryptocurrencies To regulate the price growth and to reduce the volatility, a model for achieving this must be created for the Dynamic Network Token. The goal of creating linear growth for the price of the token will be achieved by controlling the volatility as mentioned in 1.2.2. To see if the functionality of the algorithm for minting and burning tokens works, development of a Python script implementing the geometric Brownian motion formula using the Black-Scholes model [24], simulating price growth over time and studying the results obtained is a good approach. Implementing the script with the use of geometric Brownian motion came to be because of its use in the traditional financial markets for pricing options [25], giving an idea of where price is going based on the three factors of starting price (s0), interest rate ( ) and volatility ( ). By studying the results with different values for these three parameters; starting price, interest rate and volatility, a better understanding of how the price will behave in different scenarios can be derived. This will give insights regarding how the price growth will hypothetically look like over time and if the burn-to-mint ratio is sustainable. 1.2.5 Selection of parameters The different parameters needed for the geometric Brownian motion program utilizing the Black-Scholes model for price simulation, will govern how the price and volatility will behave in the simulation. This section therefore intends to present the selection process of these parameters. The first parameter is the starting price or s0. Selecting the starting price can be done

8 | 1 Introduction somewhat arbitrarily, because it is not known in the simulation stage what the price will be when deploying the Dynamic Network Token. It is also the parameter which sets the starting point for the random walk of the Brownian motion, thus only dictating the start of the walk and will not interfere in the studying of volatility. As the Dynamic Network Token does not yield interest simply by holding the token in a standard cryptocurrency wallet, the interest rate parameter or will be chosen based on the average yield from Bitcoin, Ethereum and Tether as of the 26th of April 2021, from holding the cryptocurrency in an interest account with the company BlockFi [26]. Standard deviation is seen as the statistical measure of volatility in a market or asset [27]. Therefore, the volatility parameter should be calculated from the standard deviation of price over iterations. To obtain this parameter, an iterative Java- program will be developed and then the standard deviation can be derived from the total number of transactions from the iteration. 1.3 Delimitations The delimitations set in the thesis intend to restrict the theoretical work to the studies of a few cryptocurrencies and concepts such as Ethereum's ecosystem, smart contracts and the ERC20 token standard [28]. The ERC20 standard offers a secure and interoperable way to implement a cryptocurrency with well documented and audited libraries provided by OpenZeppelin [29]. This will reduce the practical work surrounding the development, so it can be more directed at implementing functionality handling the volatility in the Dynamic Network Token. The following bullet points provide a summary of the delimitations set: ● Deeper studies of other cryptocurrencies will be restricted to: ○ Bitcoin ○ Ethereum ○ Tether ● Cryptocurrencies with burning and minting will be restricted to: ○ Binance Coin ○ Helium ○ Factom

|9 ● Development of the currency will follow the ERC20 standard for minimizing the risks associated with un-audited code. ● Development using the ERC20 standard will also reduce the amount of code to be written, so the focus can be targeted at implementing the functionality solving the postulated problem. ● Dependencies and libraries used during development will solely come from OpenZeppelin, as they provide the most secure and audited libraries in the cryptocurrency space. 1.4 Contribution of authors The distribution of the workload between the authors has been divided equally, from writing the code, to the testing and writing the report. During programming of the Dynamic Network Token, the method of couple programming was used. This method makes it easier to detect errors in the code, as one person programs and the other supervises the code live. It also makes it easier to find better solutions, as a discussion on implementation can be had simultaneously as programming. For testing of the token, both the authors have been active as users of the token in the network. Gustaf has been deploying the smart contract on a Ethereum test-net, mainly Ropsten and Goerli which are the names of two of the most common test- nets for developing, then sending tokens to Carl-Bernhards wallet on the same test- net. This made testing of the practical functionality of the token possible, as we could evaluate if the token behaved as we wanted. Work that was done separately was the detailed study of different coins. As Gustaf had a lot of prior experience using the Ethereum network and transacting ERC20 tokens, he focused on the details of Ethereum, Ethereum’s whitepaper, its ecosystem and the ERC20 standard. Carl-Bernhard focused on the study of the stable coin Tether, its whitepaper, and its stabilization mechanisms, as it was needed for a better understanding of how a low to non-volatile cryptocurrency can be created.

10 |

2 Theory and background | 11 2 Theory and background This chapter intends to lay out the theory and background regarding the problem with volatility in cryptocurrencies and how it came to be, as well as presenting the theoretical framework proposed for the solution. The choice of the coins mentioned in this chapter has been carefully selected because of their respective functionality, contributing to the implementation in this thesis project. The first two sections 2.1 and 2.2, intend to explain the two main types of currencies in use today. These are inflationary currencies, which are the most common type of currencies used by any government today in the form of fiat-currencies [30]. The other type of currencies are deflationary currencies, which are often not only currencies, but rather a means of payment. In section 2.3, a summary regarding the first cryptocurrency Bitcoin, inflationary currencies and deflationary currencies will be presented. Bitcoin was chosen because it has the most history and has some properties of a deflationary currency i.e., it has a hard cap and a regulated supply due to the halvening mechanism [31]. It has also experienced high volatility historically, making it the most suitable deflationary and volatile coin to study. In section 2.4, the Ethereum cryptocurrency and ecosystem will be presented, along with the concept of smart contracts and ERC-20 tokens. Ethereum was chosen for its ability to host another token, making it suitable as a platform for our project, as it reduces the development time and provides greater interoperability between our token and other ERC-20 tokens. Section 2.5 presents the concept of a stable coin and Tether, the stable coin issued by Tether Limited, which is of current time the most used stable coin. The choice of studying a stable coin seemed to be the most natural contrast to a highly volatile coin such as Bitcoin, as it is a coin with low volatility in comparison. Under section 2.6 the Black-Scholes model is presented, which is a model used for pricing of stocks and options. This model was chosen because of its wide usage in traditional finance and wide recognition. Section 2.7 will address the potential use cases for the Dynamic Network Token and what impacts it could have in the real world. These use cases being that it is inflationary resistant, provides a vehicle for investment and is fair in regard to its users.

12 | 2 Theory and background In the last section, 2.8, the related work surrounding the choices made for the methods implemented will be acknowledged. This includes the studies of other cryptocurrencies, price simulation models and evaluation models. 2.1 Inflationary currencies Today every country is using some form of physical cash or currency backed by a government [32]. These currencies are known as fiat-currencies and share two important aspects; centralized governance and are by nature inflationary. In economics, the concept of inflation is simple. It can be viewed as a growth of the general price level, resulting in less purchasing power for any given currency. A currency experiences inflation when more of it is added to the circulating supply, resulting in a devaluation of the currency itself [18]. As the process of creating new fiat currency is relatively easy and does not have the same uncertainties as for example gold mining [33], the possibility to add fiat currency is quite simple in comparison. Figure 2.1: Graph of the total money supply of the U.S dollar from 1959 to 2021. Source: fred.stlouisfed.org 2.2 Deflationary currencies The most known asset that can be used as means of payment and can be considered deflationary is gold. Throughout history, gold has been one of the main metals used in coins because of its rarity, practicality, and sustainability against the elements [34]. This was what made it valuable and accepted among different societies. What makes gold deflationary is the long and hard process related to the extraction of the precious metal [33], making the minting of new gold to the total supply an

2 Theory and background | 13 uncertain and difficult process. As the chance of finding gold makes the metal scarce, it is considered an asset that has a finite supply or a hard cap. Bitcoin is another example of a currency with deflationary properties [31]. As opposed to traditional currencies (fiat-currencies), Bitcoin has a built-in mechanism in its protocol known as the halvening, that cuts the reward that miners receive for each block that has been mined in half. Miners are the nodes validating transactions through solving cryptographic puzzles, keeping the Bitcoin blockchain and its distributed ledger secure [35]. This mechanism impacts the supply in a predictable way and reduces the adding of the circulating supply, i.e., slowing down the growth rate for Bitcoins in circulation [36]. The effect of the halvening results in a deflationary behaviour, making the supply of bitcoins less available over time. Bitcoin also has what is known as a hard cap, meaning that there will never be more than a certain number of coins in circulation. This function in tandem with the halvening, contributes to deflation as the supply gets scarcer and there is only a finite number of coins, resulting in demand only being the factor that can drive the purchasing power [37]. 2.3 Bitcoin In the ashes of the financial crash of 2008, Bitcoin emerged seemingly from nowhere as a means of payment with the vision to be resistant against inflation and centralized governance. In Bitcoins whitepaper, it is stated in the abstract that the idea of Bitcoin is to act as a pure peer-to-peer electronic means of payment to rule out the middle hand, i.e., financial institutions [5]. Bitcoin provides an optional way to exchange value, but as its protocol is programmed to be deflationary in regard to supply, there is no encouragement to spend as there would be in an inflationary currency losing its purchasing power over time. Therefore, Bitcoin has become a store of value rather than being a means of payment which was the intention of Satoshi Nakamoto when presenting Bitcoin’s Whitepaper in 2008. The evolution for Bitcoin has thus gone from being intended as an electronic cash system, to a currency used as an asset similarly to gold. And by every means, the two assets share many attributes such as: it has a finite supply, i.e., scarcity, it is fungible and divisible, thus it can be used as a means of payment and its supply behaves deflationary. This has led to the minting of the terms “Gold 2.0” and “digital gold” [38] as reference to Bitcoin because of its similarities to gold.

14 | 2 Theory and background 2.4 Ethereum Ethereum in comparison to Bitcoin, is vastly different. The intention the Ethereum initiative had with proposing the idea for Ethereum in 2013 was to create an alternative protocol for building decentralized applications where anybody could execute scripts, deploy a smart contract containing immutable code and run decentralized applications on the Ethereum Virtual Machine. In Ethereum’s whitepaper, it is stated that the design behind Ethereum is intended to follow five core principles. The first principle, simplicity, is Ethereum’s way of saying that the protocol should be as simple as possible and that optimization that adds complexity should only be implemented if it provides substantial benefit for the network. The second principle that is stated in Ethereum’s whitepaper, universality, is the idea of providing a programming language which a programmer can use to construct any smart contract or transaction type that can be mathematically defined. The third principle, modularity, where Ethereum’s protocol is designed to be as modular and separable as possible. This leads to better security and less need for modification for the application stack when one has modified a small protocol. The fourth principle, agility, is there for constant changes in the Ethereum protocol if it is beneficial for the network. In short, the details of the Ethereum protocol are not set in stone. The final principle, the non-discrimination principle simply means that anyone can use the protocol without restriction or prevent specific categories of usage. For example, a programmer could run a program that infinitely increments a variable by one in an infinite loop if the programmer pays the per-computational-step transaction fee in Ether [39]. 2.4.1 Smart contracts Smart contracts can be viewed as a protocol or program, governing transactions by executing them according to the terms defined in the contract. The objective of a smart contract is to rule out any third-party governing transactions, i.e., a trusted intermediate who has the role to create trust between the two parties transacting. As every transaction is stored publicly and all users oblige to the same rules in the protocol, smart contracts create a way of transacting between arbitrary participants without the need of trust from a third party.

2 Theory and background | 15 To execute a smart contract, it must be compiled and stored on a blockchain. Often associated with the compiling and storing of the smart contract on a blockchain, is a transaction fee. In the case with Ethereum, the smart contract will be executed on the EVM after the payment of this transaction fee made in Ether. This transaction fee is also known as “gas” [40]. 2.4.2 ERC-20 token The ERC20 (Ethereum Request for Comments 20) token is a fungible Ethereum based token, meaning that one token is always equal to another token from the same smart contract, creating a means of payment when utilizing the token between two parties. To be viewed as an ERC20 token, it must have some standard functionality related to it. This incorporates the following functions and events: Functions needed for an ERC20 token: ● function name() public view returns (string) ● function symbol() public view returns (string) ● function decimals() public view returns (uint8) ● function totalSupply() public view returns (uint256) ● function balanceOf(address _owner) public view returns (uint256 balance) ● function transfer(address _to, uint256 _value) public returns (bool success) ● function transferFrom(address _from, address _to, uint256 _value) public returns (bool success) ● function approve(address _spender, uint256 _value) public returns (bool success) ● function allowance(address _owner, address _spender) public view returns (uint256 remaining) Events needed for an ERC20 token: ● event Transfer(address indexed _from, address indexed _to, uint256 _value) ● event Approval(address indexed _owner, address indexed _spender, uint256 _value) The ERC20 standard also provides interoperability between different ERC20 tokens, as they all are built upon the Ethereum blockchain, making it easier to interact with different types of ERC20 tokens [28].

16 | 2 Theory and background 2.4.3 Burning and minting in an ERC20 The ERC-20 token is the standard for smart contract tokens deployed on the Ethereum blockchain. By implementing the functions and events mentioned in section 2.4.2, a token can be defined as an ERC-20 token. The ERC-20 standard thus creates a possible base for every token in the Ethereum ecosystem, making it possible to transact [41]. The ERC-20 standard alone will not make it possible for a token to become volatility resistant, therefore the concepts of burning and minting must be added to the implementation. Burning and minting are two concepts related to smart contract development, making it possible to control the number of tokens in existence. Burning is the functionality that will reduce [42] the number of tokens and minting is the functionality creating new tokens, adding them to the supply in the same way as traditional mints add to the supply of a fiat currency [43]. The implementation of burning and minting is something that is unique to every token, as the developer(s) must come up with algorithms or protocols for the functionality suiting the goals for their specific token. It is common to implement burning so it will interact with the transfer function of the ERC-20 standard. In this way, burning can be achieved when transferring a token or some conditions regarding the transfer(s) of ERC-20 tokens. When a burn is called in the protocol of the smart contract, the number of tokens set to be burned will be sent to the 0x0 address, also known as the “black hole address” [23]. This address can be viewed as an address that is consuming ether and tokens, never to be retrievable again, making it a “black hole”. Figure 2.2: Overview of the 0x0 Address as of 28th of April 2021. Source: Etherscan.io.

2 Theory and background | 17 Minting is the opposite of burning, as it adds new tokens to the supply. Every smart contract, and therefore every ERC-20 token, must do at least one minting when the contract is deployed [44]. This will create the initial supply, setting the balance of the wallet address deploying the smart contract equal to the amount minted. As minting new tokens to the supply of a cryptocurrency is in practice the same thing as governments printing fiat currency, most cryptocurrencies will not use minting functionality embedded in the protocol as it will increase inflation of the token. 2.4.4 Dependency of Ethereum As all ERC20 tokens are deployed as smart contracts on the Ethereum blockchain, the dependency of Ethereum is inevitable. This implies that the functionality for any ERC20 relies on the Ethereum project and its ability to function properly. If the Ethereum network would stop working, become insecure or the value of the Ether in dollars would go to zero, the miners on the Ethereum network would no longer have an incentive to keep the network running because there would not be any value in the reward earned from fees. This would result in exposure to problems such as double spending which would devalue the network or even destroy it [45]. If things like an insecure Ethereum blockchain or a low to zero value of ether in dollars would occur, all ERC-20 tokens would be affected as they reside on the Ethereum blockchain. It could even result in making the transacting of any ERC20 token impossible, thus removing the value in the tokens. Alas Ethereum makes it easier for the deployment of a cryptocurrency with great interoperability potential, but at the same time it also creates a dependency where faith in the value of Ether is necessary. 2.5 Tether Tether Limited is a company behind the Tether cryptocurrency whose purpose is to have a one-to-one ratio with the U.S Dollar in contrast to Bitcoin whose vision is to be resistant against inflation and centralized governance. In their proposal of the Tether cryptocurrency, the main benefit is the ratio to the dollar and the possibility for world assets to migrate to the Bitcoin blockchain since Tether is running on top of Bitcoin’s blockchain via the Omni Layer protocol [46]. Since it is hard to match the dollar with a one-to-one ratio, Tether states in their whitepaper that proof of reserve is the way to ensure a one-to-one ratio. This means that for every US Dollar transferred to Tether Limited’s bank account, they will issue

18 | 2 Theory and background the same amount of dollars transferred into Tether. This ensures a one-to-one ratio to the dollar and makes Tether a so-called “stable coin” [47]. However, the proof of reserve method does not come without any problems that need to be solved. In Tether’s whitepaper it is stated that four weaknesses have been identified and handled by Tether Limited to ensure the security of their assets. Tether Limited, the company that issues Tether’s could go bankrupt but the assets that are in circulation would still be safe and redeemable. Their bank could go insolvent, but Tether’s assets are insured by the banks that they use, as the banks accept Tether’s business model. The most dangerous weakness with Tether is the fact that their bank could freeze or confiscate the funds which would lead to Tether’s being worth absolutely nothing [48]. 2.6 Black-Scholes pricing model The Black Scholes model is a model for pricing options and stocks in the traditional financial markets [24]. Since its inception, it has become a standardized way to predict and simulate the price of different assets. The model itself makes use of what is known as a geometric Brownian motion [25] to create a continuous stochastic process. Using a Brownian motion or wiener process in combination with the parameters (interest rate) and (volatility), the Black-Scholes model makes it possible to simulate the behavior of a financial asset such as an option or a stock. The model provides a way to simulate and predict prices of assets in the financial markets, it is used heavily by economists and large companies around the world. For example, PricewaterhouseCoopers (PwC) stated in their Stock Compensation report from 2017 that over 82% of large companies solely relied on the Black-Scholes model for predicting prices of stock compensations [58]. 2.7 Real world use cases Postulated in section 1.1, the problem of volatility is not only restricted to cryptocurrencies. A fiat currency experiencing hyperinflation, is also experiencing high volatility. In 2.1 and 2.2 the concept of inflationary and deflationary currencies was postulated. These concepts are somewhat opposites of each other. The inflationary approach taken in fiat currencies diminishes the purchasing power of a currency by adding more of it, i.e., adding to the supply. In contrast, a deflationary currency like Bitcoin regulates the supply by making it scarcer with mechanisms such as the halvening and by having a hard cap. This brings up a dilemma. That in theory, deflationary money should be preferred over

2 Theory and background | 19 inflationary types of money, as it increases the purchasing power over time. But the problem that arises with deflationary money is that it demotivates spending in accordance with Gresham’s law [10] and by the definition of deflation, as it will presumably be more valuable over time. As the goal of the Dynamic Network Token is to remove high volatility coming either from deflation or inflation, this creates a real-world use case where users get the best of the two; a growing value over time with incentive to spend the token as a means of payment. 2.7.1 Implications of Dynamic Network Token The Dynamic Network Token which is proposed as the solution to volatility within cryptocurrencies can be used in several ways. Not only as a means of transacting to other entities in the network or store for financial gain. But more importantly it could be used as an exchange of value without being affected by inflation and deflation. Stated in 1.1.3, the problem with the national currency of Venezuela experiencing hyperinflation, could seek a solution in the use of the Dynamic Network Token or a currency with the same functionality, as it is inflation resistant. The usage of such a currency would result in slowing, reducing, or removing the possibilities of hyperinflation, bringing back the purchasing power to the Venezuelan people. By exchanging their national fiat currency for the Dynamic Network Token or begin the development of their own national digital currency with the same properties as the Dynamic Network Token, they can avoid losing purchasing power. Besides looking at the possibilities of helping troubled countries with their inflation, the project also provides investors seeking to gain capital an opportunity by holding the Dynamic Network Token. Even though the token’s utility is highly based on using the token as a currency, investors can still use it as a means of capital gains by holding the token until they are satisfied with the results. Since the Dynamic Network Token will be built upon its community, implementations within real world scenarios are endless depending on what the community needs and what it wants to be developed. In case the community wants to use the token for online purchases, it can be developed for the satisfaction of the community.

20 | 2 Theory and background 2.8 Related work This section intends to bring up the related work. Section 2.8.1 will address related work regarding the implementation of burning and minting in other cryptocurrencies, section 2.8.2 will address other hybrid solutions using burning and minting. Section 2.8.3 will bring up related work regarding other pricing models that could have been used for simulating price, and 2.8.4 will acknowledge relevant work done regarding evaluation models for cryptocurrencies. Lastly, the relevance of this related work will be stated in section 2.8.5. 2.8.1 Burn and mint in cryptocurrencies Prior to this work, research in the cryptocurrency field regarding burning and minting was done. The focus of the research targeted projects using this type of functionality, and how these projects had implemented it. With different goals and ambitions, projects use different approaches to this area. The projects chosen for studying these functionalities are Binance coin and the Helium token. Both projects are considered well established and have drawn a lot of capital to them and reside in the top 100 rankings by market capitalization as of April 2021 [11]. Helium was chosen mainly for its minting functionality, while Binance coin was chosen for its unique approach to burning. Other projects under consideration for the studying of the functionality were Dogecoin and Safemoon Protocol. Dogecoin was considered as it mints 10,000 new coins for each block mined, which leads to approximately 14 million new coins being minted every day [49]. Safemoon Protocol was considered due to its burning fee functionality that both locks liquidity and distributes a percentage of the transaction to all its token holders. However, these were disregarded due to the projects being considered unserious. For example, Dogecoin developers have recently started working on the project again due to its media attention and its creator admittingly says it was created as a joke [50]. Dogecoin also as of May 2021 has the highest volatility of all cryptocurrencies [51], making it very unstable and therefore also making the study of the mintings impact on volatility hard. In the case with Safemoon, it has functionality implemented preventing some users in the network from paying the burning fee when transacting, making it an unfair network and is therefore unserious [52]. Binance coin is the native coin of the Binance blockchain, whose approach to burning their coins is interesting. From the initial coin offering of Binance coin, the company announced that they would burn 50% of its total supply by buying back Binance coins

You can also read