CIO Strategy Bulletin - The US Election and the Economy: Double, double, toil and trouble October 11, 2020 - Citi Private Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CIO Strategy

Bulletin

October 11, 2020

The US Election and the Economy: Double, double, toil and trouble

David Bailin, Chief Investment Officer

Steven Wieting, Chief Investment Strategist and Chief Economist

Joe Fiorica, Malcolm Spittler and Joseph Kaplan contributed to this Bulletin

Summary

• Markets have swung from hope to fear and back due to an increasing prevalence of COVID and the absence of

congressional action. In an unprecedented way, partisan political divisions has delayed emergency fiscal action for

more than three months. The encroaching US election may delay stimulus further and COVID-impacted individuals,

industries and municipalities may suffer for another three months.

• Financial markets have mostly taken the stimulus dithering in stride. This is consistent with our expectation for

medical solutions to COVID in the coming year. Yet, without an immediate medical solution and aid for those most

harmed by COVID, the probability of a near-term economic set back (of reduced scope) has risen.

• We urge investors to look at the coming quarter’s volatile prospects differently than the coming year when we expect

“pent-up demand” and COVID’s end to broaden economic recovery.

A “Made for TV” Election Update

With President Trump coming back to the campaign trail after a weeks absence due to his hospitalization for COVID-19, the landscape

of the election has shifted markedly. Beginning with the first Presidential debate, polled voters began a shift away from the President.

Then, with the President’s diagnosis, hospitalization, trip to wave at well-wishers, and subsequent revelations about a White House

event at which more than two dozen attendees contracted the disease, older voters began to favor Biden. In 2016, Trump won “seniors”

by seven percent versus Clinton. In a NBC/Wall Street Journal poll out last week, Joe Biden led Trump by 27 points among seniors

(62% to 35%) and in a CNN/SSRS poll out on Friday the advantage to Biden was 21 points (60% to 39%).

Finally, the cancellation of the second debate and the waning number of days until the election provide the President with diminished

opportunity to change the course of the election. Here is the most recent aggregated polling data from 538.com which weights all polls

based on prior accuracy (see Figure 1).

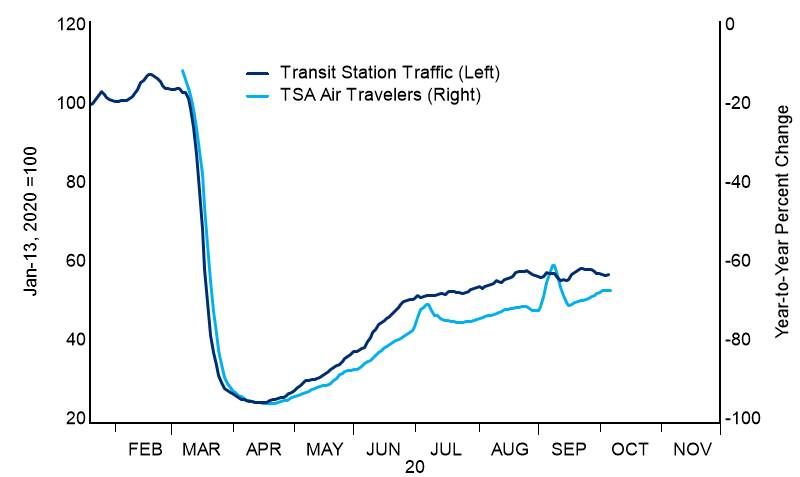

Figure 1: Who’s ahead in the national polls? An updating average of 2020 presidential election polls Source: FiveThirtyEight though October 10, 2020 The shift in the polls makes the odds of Democratic control of the Senate somewhat higher. While less conclusive than the one-on-one Presidential race, based on polls and a variety of factors, FiveThirtyEight’s latest forecast put the probability of a switch to Democratic control at 68%. The issue of which party controls the Senate may not be decided until January 5th, when a run-off special election in Georgia will be decided. Fiscal Stimulus on Hold? In an unprecedented way, partisan political divisions in the US have delayed emergency fiscal action for more than three months. Seven Senate races are currently “too close to call” according to pollsters (six Republican and one Democratic incumbents). Thus, it is likely that the attention and energy of many in Washington will remain severely divided, making it hard to craft and pass significant bipartisan legislation. We did not predict this degree of congressional inactivity given the clear benefits of a further boost to the US economy and the need for specific aid to certain industries, like airlines. The aid is needed to support workers and parts of the economy that are still highly impacted by COVID before a medical solution brings the pandemic to an end. In the event that a worker cannot afford to miss work, they will work even if infected. Such workers will infect others and the virus will continue to accelerate. As the delays ground on, it has seemed more likely that the Presidential election would get in the way of any agreement at all, perhaps until January. There have been glimmers of hope. Days before the President’s hospitalization, it seem that his negotiators and the Democrats had agreed bridge gaps between a $1.5 and $2.2 trillion aid package. But then, to the shock of markets on Tuesday, President Trump announced that he was “stopping stimulus talks until after the election.” Later that evening, he said he would gladly sign any stand-alone bills to repeat the $1200-per-family stimulus checks of April, subsidize small business employment, and support beleaguered airlines. Interestingly, the latest Republican offer is just $400 billion less than a plan passed by House Democrats. A middle ground would be close to the $2 trillion we said would be needed to secure the expansion deep into 2021, assuming the COVID spread remained disruptive (please see “Wave 1 Virus Acceleration Requires Wave 2 Stimulus,” July 19, 2020). With US airline passenger traffic still down 60%, the solvency of the industry depends on waiting out the virus. The story is the same for municipalities, where public transportations use has fallen 50%. A collapse in government revenues has, as usual impacted education budgets, where worker’s bear the brunt of the impact of partial- or full school closures as a result of COVID (see Figure 2).

Figure 2: US Education Employment: State and Local Governments

Source: Haver Analytics as of October 8, 2020.

A Clock Winding Down

With 23 days until the election, the congressional calendar itself is a major hurdle for significant legislative progress on COVID stimulus.

The decision to hold hearings for the new Supreme Court Justice and the strong preference of all 35 Senators and every member of the

House to be “at home” to campaign for re-election creates little appetite for congressional processes that can be delayed easily through

procedural actions in both the House and Senate.

Furthermore, the prospect that the election will unify the US Congress and Presidency under one party makes negotiations even less

likely. With Vice President Biden ahead in the polls, Democrats are not negotiating further. And Republicans may have little incentive

to cooperate on legislation during the so-called “lame duck” session following the election in mid-November.

At the end of all this is the very real and very likely possibility that the US economy will enter Winter with many vulnerable individuals

and weak sectors of the economy in sustained distress for at least three months.

Resilience and Vulnerabilities

We have been very clear about the need for further fiscal stimulus in these pages since April. We had forecasted that Q4 would be a

tough period for the economy and had built a stall in GDP for Q4 into our models.

While the overall US economy has performed close to our expectations, the labor market recovery has been even faster and stronger.

This is true even though peak fiscal support is now five months in the rear-view mirror (see Figure 3). The economy’s adaptations to

COVID, with consumer goods purchases surging and millions of jobs saved with telecommuting (see Figure 4), has erased more than

half of the 22.2 million net job losses since April. A rise in unfilled job openings since April suggests further employment and economic

gains (see Figure 5).

Figure 3: Peak in US Transfer Payments Was April 2020 Figure 4: Video Conferencing Enables Work Amid Social-

Distancing: Zoom Meetings Per-Month

214 Personal Current Transfer Payments

212

210

208

$ Billions

206

204

202

200

198

Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20

Source: Haver Analytics, Factset and Zoom as of October 8, 2020. This is shown for illustrative purposes only, it is not a recommendations to buy nor a solicitation to sell

the aforementioned equity.

Figure 5: US Total Employment and Job Openings (non-farm):

Job Opening Rebound to 2018 level, Employment 2016

Source: Haver Analytics as of October 8, 2020.

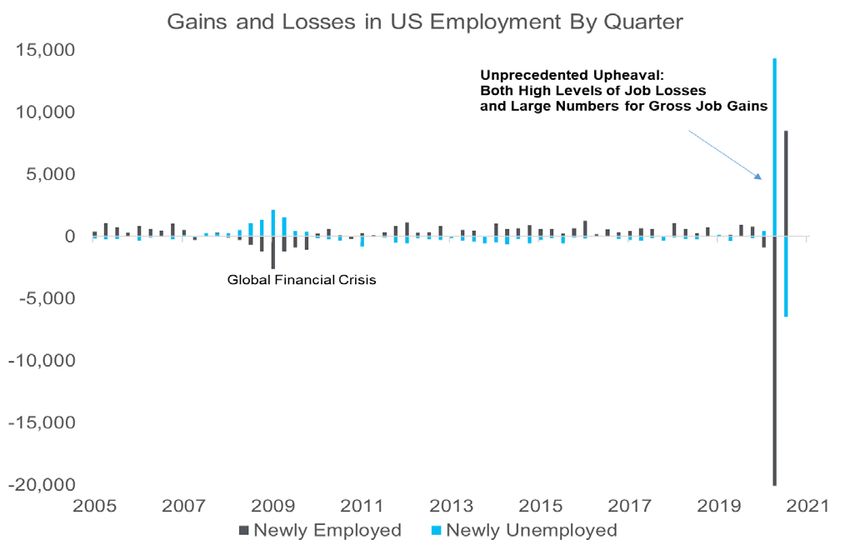

Below the surface, the net job gains mask severe and unusual turmoil. As Figure 6 shows, the pace of both firing and hiring has been

unprecedented. This is why the typically reliable, high quality indicator for gross layoffs – unemployment insurance claims – has remained

high and troubling in the face of a significant jobs recovery.

Workers who were temporarily furloughed accounted for the majority of the job losses and the majority of the employment rebound. Of

the 18.0 million temporarily jobless in April, only 4.6 million remain. Permanent job losses have risen by 2.5 million since February, but

that is far less than the 4.8 million people who were impacted in 2008/2009 (see Figure 7).

Figure 6: Upheaval: US Hiring and Firing Both Surge Figure 7: Moderate Rise in Permanent Job Losses Masked

by Sharp Rebound From Temporary Job Losses

Source: Haver Analytics as of October 8, 2020. All forecasts are expressions of opinion and are subject to change without notice and are not intended to be guarantees

of future events.

The Winter Challenge Before Us

With COVID-19 cases and hospitalizations rebounding as schools and other gathering places have reopened, it seems highly likely that

labor market progress will slow much further. The broader macroeconomic rebound since May does not eliminate the emergency need

for “safety net” measures for those most impacted. For COVID-impacted industries that have never recovered, progress has been

modest and relief is not in sight (see Figure 8). The unencumbered parts of the US economy, meanwhile, seem poised to make less

progress through the winter.

Figure 8: US Airline Passenger Travel and Mobility At

Public Transportation Sites (Feb 1 = 100)

Source: Haver Analytics, Google, Conference Board as of October 8, 2020

COVID Weakening?

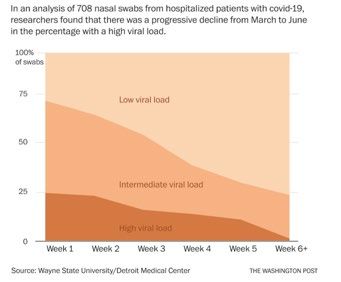

There is some good news about the virus, though it will not help the economy immediately. COVID appears to be less deadly now than

at its introduction. This may be due to precautions and lower levels of exposure at introduction as noted by the viral load data below

(Figure 9). As we noted in August 9 Bulletin: "Resilience and Adaptation: Why the Global Economy is Poised for Accelerating Growth",

most viruses become less deadly over time due to mutations that make them less deadly, new treatments or vaccines.

On August 13th, the Journal of the American Medical Association published a report from eight Houston hospitals that identified a major

difference between what they called surge 1 and surge 2 patients. In Surge 2 (from May 16 to July 7), a smaller percentage of patients

required intensive care (20 versus 38 percent in Surge 1). They spent less time in the hospital (4.8 days versus 7.1 days). And most

importantly, they were much less likely to die (5.1 percent versus 12.1 percent). Note that a broad meta-analysis of 53 countries and

regions with the highest coronavirus death rates identified similar trends.

Figure 9: Falling viral load data

Source: Wayne State University/Detroit Medical Center as of October 8, 2020

What This Means for Markets Between Now and January

Winter 2020 has not yet begun. The interactions between open or partially open schools and restaurants and plunging winter

temperatures are unknown in terms of spreading the virus.

While polls are heading in a more decisive direction for the Presidential campaign, there are no guarantees that a clear outcome will

emerge by November 4. Republicans can challenge the validity of absentee ballots in swing states. Absentee ballots are rejected for

many reasons including missed deadlines, forgotten signatures, non-matching signatures or lack of a witness signature in states where

there are such requirements. (These include Missouri, North Carolina, Oklahoma and Wisconsin, and would have included Virginia,

Minnesota and Rhode Island, which waived them due to the virus.) This exercise may only be effective if the Presidential race is close,

however, under some scenarios, determining Senate control may take longer than the outcome of the Presidential election.

In essence, much of the very near-term (3 months) is unlikely to be a period of strong clarity on the direction of US policy or the end

point for COVID. This will likely mean bouts of financial market volatility will return in that timeframe before the stronger prospects for

we see for 2021 are clear.

Earnings Season: Scrooge Returns

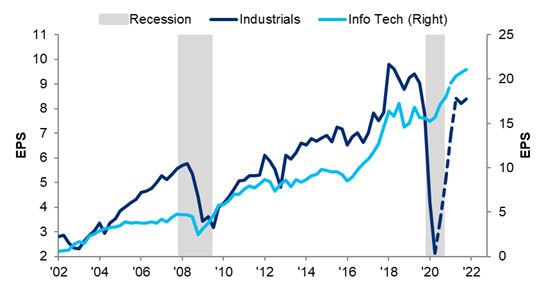

We believe that the coming earnings reporting season this month will differ little from 2Q 2020, with a continued dichotomy between

“COVID-defensive” (Information Tech) earnings outperformance, and “COVID cyclical” weakness (see Figure 10 and recent Earnings

preview). The same will be true for the calendar fourth quarter. Therefore, we also believe investors in depressed industries will have

to wait out the volatility the US election and COVID-winter will bring (see Figure 11).

Figure 10: S&P IT and Industrials Sectors: EPS and Figure 11: Select “COVID Cyclical” Industry Groups,

Estimates through 2021 Remaining S&P 500 Sectors

Source: Haver Analytics, Factset. COVID cyclical industry groups in figure 10 are airlines, hotels, restaurants and leisure, retailing REITS and, hotel and resort REITS

Reference in paragraph above on “COVID-defensive” includes information technology, health care, communications services, consumer staples, utilities and e-commerce

sectors. The COVID-cyclicals entire sub-group include industrials, financials, consumer discretionary excluding e-commerce, real estate, energy, and materials sectors

Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only and do not represent the performance of any specific

investment. Index returns do not include any expenses, fees or sales charges, which would lower performance. For illustrative purposes only. Past performance is no

guarantee of future results. Real results may vary. All forecasts are expressions of opinion and are subject to change without notice and are not intended to be

guarantees of future events.

Looking Forward to 2021

While infections from COVID are going up and will likely spike over the next few months, the US public’s heightened awareness and

actions, ironically improved by the President’s diagnosis, should yield a profound and beneficial difference from the initial shock the

world experienced in 1Q 2020.

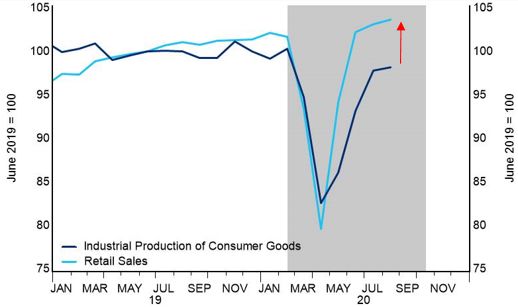

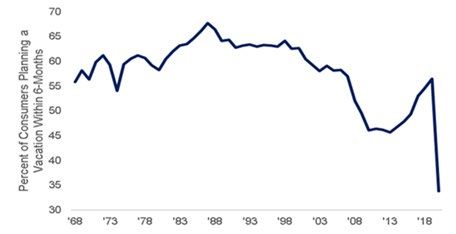

Looking ahead to 2021, pent up demand is building in the economy as life was put on hold this year (see Figure 12). Retail sales have

been outpacing production, suggesting a further ramp up in trade and industrial activity in 2021 (see Figure 13). Travel, tourism and

hospitality industries are like a “coiled spring wound tight” for a period when COVID is no longer a threat.

Assuming eventual passage of US fiscal stimulus, the combination of latent demand, greater global trade and a COVID vaccine provides

a great deal of fuel for an above-average recovery from a short, sharp recession.

Figure 12: Vacation Intentions of US Consumers

Source: Haver Analytics as of October 8, 2020.

Figure 13: US Retail Sales and Consumer Goods Production

Source: Haver Analytics as of October 8, 2020.

What to Watch For in Markets

We have watched keenly as US long-term interest rates have perked up slightly over the past month even as political uncertainty has

grown unabated. This suggests that rates will go higher when a medical solution is found and a broader economic expansion becomes

certain.

We have also seen US small cap stocks and other cyclicals start to eclipse technology shares in the second-half 2020-to-date. This also

suggests that the economy may be at a turning point where industrials and other impacted industries will return to a normal revenue and

earnings trajectory. The “COVID winter” may delay further progress. But the Russell 2000 is still trailing the Nasdaq 100 by 34

percentage points this year after the 1H plunge in SMID. This is suggestive of a major “catch up” opportunity during the year ahead (see

Figures 14-15).

Note that we expect many “digitization” innovators to have stronger long-term growth rates than the broader US economy. They

represent a Citi Private Bank “unstoppable trend.” However, 2020 and 2021 should be considered distorted years given COVID’s arrival

and likely departure. As figure 4 suggests, video conferencing will grow in time, just as it has in the past five years. Yet if there is a

COVID vaccine, it may be very hard to exceed 2020’s level given a 250% growth rate this year. That is why beaten down industry

sectors, in contrast to those that have surged, represent a stronger tactical opportunity for 2021 looking at the peculiar conditions of this

year.

Finally, in the event of a Democratic sweep, markets may swoon. Fears of higher taxes, higher spending and increased regulatory

action may be the cause. We would view this as a buying opportunity for equities.

Figure 14: Nasdaq 100, Russell 2000 and S&P 500 Equal Figure 15: Nasdaq 100, Russell 2000 and S&P 500 Equal

Weight Index July 6, 2020 =100 Weight Index Dec 31, 2019 = 100

120 150

Russell 2000 Small Cap Russell 2000 Small Cap

140

Nasdaq-100 Large Cap (Tech) Nasdaq-100 Large Cap (Tech)

115 Equal Weight S&P 500 130 Equal Weight S&P 500

120

110 110

July 1 =100

Jan 1 =100

100

105 90

80

100 70

60

95 50

Jul-06 Jul-18 Jul-30 Aug-11 Aug-23 Sep-04 Sep-16 Sep-28 Oct-10 Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Source: Haver Analytics as of October 9, 2020. Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only and

do not represent the performance of any specific investment. Index returns do not include any expenses, fees or sales charges, which would lower performance. For

illustrative purposes only. Past performance is no guarantee of future results. Real results may vary.

INVESTMENT PRODUCTS: NOT FDIC INSURED · NOT CDIC INSURED · NOT GOVERNMENT INSURED

· NO BANK GUARANTEE · MAY LOSE VALUE

This email contains promotional materials. If you do not wish to receive any further promotional emails from Citi Private Bank,

please email donotspam@citi.com with “UNSUBSCRIBE” in the subject line. Email is not a secure environment; therefore, do not use

email to communicate any information that is confidential such as your account number or social security number.

Citi Private Bank is a business of Citigroup Inc. (“Citigroup”), which provides its clients access to a broad array of products and services available

through bank and non-bank affiliates of Citigroup. Not all products and services are provided by all affiliates or are available at all locations. In the U.S.,

investment products and services are provided by Citigroup Global Markets Inc. (“CGMI”), member FINRA and SIPC, and Citi Private Advisory, LLC

(“Citi Advisory”), member FINRA and SIPC. CGMI accounts are carried by Pershing LLC, member FINRA, NYSE, SIPC. Citi Advisory acts as

distributor of certain alternative investment products to clients of Citi Private Bank. CGMI, Citi Advisory and Citibank, N.A. are affiliated companies

under the common control of Citigroup.

Outside the U.S., investment products and services are provided by other Citigroup affiliates. Investment Management services (including portfolio

management) are available through CGMI, Citi Advisory, Citibank, N.A. and other affiliated advisory businesses. These Citigroup affiliates, including

Citi Advisory, will be compensated for the respective investment management, advisory, administrative, distribution and placement services they may

provide.

Read additional important information.

Past performance is not indicative of future results. Real results may vary

MBS are also sensitive to interest rate changes which can negatively impact the market value of the security. During times of heightened volatility, MBS

can experience greater levels of illiquidity and larger price movements

Important information, including information relating to risk considerations can be found in the link above..

Views, opinions and estimates expressed herein may differ from the opinions expressed by other Citi businesses or affiliates, and are not intended to

be a forecast of future events, a guarantee of future results, or investment advice, and are subject to change without notice based on market and other

conditions. Citi is under no duty to update this presentation and accepts no liability for any loss (whether direct, indirect or consequential) that may arise

from any use of the information contained in or derived from this presentation.

© 2020 Citigroup Inc. All Rights Reserved. Citi, Citi and Arc Design and other marks used herein are service marks of Citigroup Inc. or its affiliates,

used and registered throughout the world.

www.citiprivatebank.com

You can also read