IFAST Research Update: Indonesia 2022 Outlook: Continued macro recovery to support extended rally

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

iFAST Research Update: Indonesia 2022 Outlook: Continued macro recovery to support extended rally Following the strong rally in 2021, we think that there is still upside potential for Indonesian equities going forward. In this article, we will present the outlook for the economy and the market and explain why we still think Indonesia is worthy of the 3.0 Stars "Attractive" rating. Indonesia has been one of our favourite markets since the start of 2021. Our benchmark for Indonesian equities, the Jakarta Composite Index (JCI Index), is up 9.4% by the end of 2021. The strong performance has been in line with the earnings upgrades that we have seen so far, as the Indonesian economy performed better than expected while exporters benefitted from stronger commodity prices and robust external demand. Figure 1: JCI Index historical performance since 2021 iFAST Research Team 10 February 2022

Reopening of the economy in sight, despite low vaccination rates In Q3 2021, Indonesia did not kick start well as the pandemic risk loomed large, with cases increasing substantially. With the detection of more transmissible virus strains - Delta, the new confirmed cases per day spiked and hit the record high of more than 55K daily in July. With that, Indonesia has again re-imposed restrictions to curb the dramatic rise in covid-19 cases, which largely blamed the highly transmissible Delta strain. In Indonesia, the government employs a multi-tier system for applying public activity restrictions (PPKM) in individual cities and regencies based on local disease activity. The system consists of PPKM levels 1 through 4 in order of increasingly strict controls. With the enforcement of stricter and wider lockdown, Indonesia has successfully mitigated the spread of COVID-19. The wave of infections had passed its peak, with daily confirmed cases on the decline (see Figure 2). With that, Indonesia's government has decided to reopen their economy, where almost all of the sectors are allowed to operate now. Besides, to resurrect the local tourism industry, Indonesia has agreed on a travel corridor with countries such as Malaysia through the bilateral Vaccinated Travel Lane (VTL). Nevertheless, the vaccination rates in Indonesia are still slower than most of the countries in Southeast Asia at this juncture (See Figure3). The slow vaccination rates were mainly attributed to the depleting supplies of vaccines, where Indonesia has fallen short of the shots it needs like many other countries. Additionally, the complicated geography of the world's largest archipelago nation and hesitancy among some Indonesians are also the major roadblocks of the vaccination program. Figure 2: Indonesia's new confirmed cases per day iFAST Research Team 10 February 2022

Figure 3: Vaccination rate among the countries in Southeast Asia. iFAST Research Team 10 February 2022

Indonesia to post solid GDP growth in 2022 In 2021, the surge in virus cases and stricter control measures derailed the nation's economy from the recovery path. Nevertheless, with the pickup in vaccination rates and fall in confirmed Covid cases, we are still holding an optimistic view toward the Indonesia economic prospect and expecting it to post solid GDP growth in the following quarters as the reopening of the economy would fuel the nation's economic activities in overall. Regarding the yearly growth projection, Indonesia is expected to wrap up the year 2021 with a growth of 3.50% and at a stronger pace of 5.20% in 2022, see Figure 4. Figure 4: Yearly GDP Growth forecast As a matter of fact, the Indonesian government has been ramping up its vaccination program since H2 2021. The health ministry has roped in the military, police force, and civil society groups to speed up the vaccination. On top of that, the arrival of more vaccine doses starting from August has eased the worries on the supply bottleneck, bringing the Indonesia vaccination rates back on track. Despite the low vaccination rates in Indonesia, the nation still managed to curb the spread of the virus. With the significant drop in cases, the economy is expected to extend its recovery in 2022 once the vaccination rates ramped up. iFAST Research Team 10 February 2022

Strong economic recovery ahead, underpinned by exports Following the relaxation of lockdown measures, Indonesia managed to extend its trade balance surplus for the 18 consecutive months in October (See Figure 5). The exports continue to outpace the imports, mainly backed by the factor of high commodities price and improved global demand buoyed exports. The YoY figures continue to show sustainable recovery for both oil and gas and non-oil and gas exports while marking October's total export value above the level of $20 billion for the third consecutive month, see figure 6. Figure 5: Indonesia records 16 consecutive months of trade balance surplus iFAST Research Team 10 February 2022

Figure 6: Indonesia's exports show continued recovery With an expectation of improving external demand across the globe, Indonesia would potentially be one of the beneficiaries as it is a crucial exporter in the world. At this juncture, the countries including China, the United States, and Japan are the major trading partners of Indonesia, where they are highly relying on imported products such as coal, palm oil, and manufactured goods. Besides, we also opine that the commodity price would continue to stay high, fuelling the export growth over a more extended period. Therefore, in the future, we expect the sustainable global economic recovery and high commodity price will likely continue to be the tailwinds that allow resource-rich Indonesia to book big export earnings in 2022. As a result, higher exports would magnify the top and bottom line for these related companies in Indonesia. iFAST Research Team 10 February 2022

Consumption to strengthen further as labour market recovery continues. The sudden spike of virus cases in Indonesia in H2 2021 has once again put the recovery at risk as Indonesia reimplemented containment measures to curb the virus, putting people off for job looking. However, the hindrance was short-lived as the domestic consumer demand has recovered lately, proven by the strong rebound in Retail Sales and Consumer Confidence data after the virus started to ease in July, see Figure 7. Figure 7: Retail Sales and Consumer Confidence Index continued to rebound in October As mentioned earlier, the Indonesian government is now on the right track of reopening its economy. Against such a backdrop, the labor market is expected to strengthen further as companies are likely to increase their hiring activity to prepare themselves well for the return of economic activity to the pre-pandemic level (See Figure 8). As a result, the job market's recovery is expected to bolster private consumption, consumer confidence, and retail sales. iFAST Research Team 10 February 2022

Figure 8: Indonesia's Unemployment Rate Forecast Bank Indonesia remains in its accommodative tone, sticking to the objective of reviving the nation's economy In line with our expectation, Bank Indonesia continued to maintain its accommodative monetary policy unchanged, supporting its economy throughout the fallout of the pandemic. At its December rates meeting, Bank Indonesia's board of governors agreed to leave its benchmark interest rate at 3.50% record low while maintaining the Deposit Facility (DF) rates at 2.75% and Lending Facility (LF) rates at 4.25%. Without a doubt, the projected low economic growth outlook and high uncertainty about the course of the pandemic were the main factors causing such a decision has been made. Other measures such as storing a great level of Fx reserves up to USD145.9 billion as of November 2021 are acting as a buffer to defend Indonesia from any further external shock (see Figure 9). Under the roof of loosening monetary policy, Bank Indonesia is enabled to protect the stability of the exchange rate and financial system and tide the economy through the pandemic gloom. iFAST Research Team 10 February 2022

Figure 9: Bank Indonesia's Foreign Exchange Reserves Going forward, the objective of reviving the nation's economy would still be the priority of Bank Indonesia. With that, we opine Bank Indonesia to extend its loose monetary policy for a longer time, whereby the first rate hike is foreseen in Q3 2022, which is expected to continue to be the tailwind for Indonesia's equities market (See Figure 10). iFAST Research Team 10 February 2022

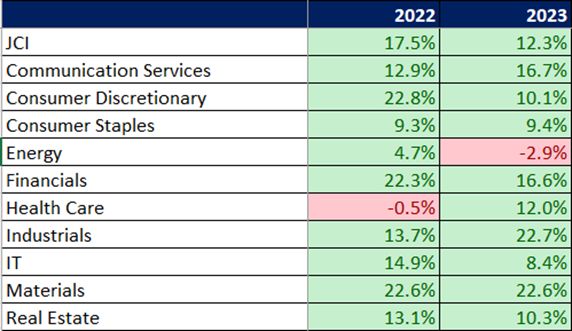

Figure 10: BI 7-days Reverse Repo Rate (%) Fundamentals for Indonesian equities still look solid going forward Fundamentals for Indonesian equities still look solid going forward, with earnings for the JCI Index expected to see double digit growth for the next two years, 17.5% in 2022 and 12.3% in 2023. The 2022 and 2023 EPS forecasts have also been upgraded since the start of the year, reflecting increased optimism in Indonesia. Figure 11: JCI Index and Sector Earnings Estimates iFAST Research Team 10 February 2022

We are seeing healthy broad based positive growth across all sectors. The main contributors to the earnings growth

are cyclical sectors, including Financial and Materials sectors which constitutes 39% and 12% of JCI Index

respectively.

Index heavyweight Financials sector is expected to grow earnings by 22.3% in 2022 and 16.6% in 2023 as NIM

improve amid rising rates and NPLs stabilize, led by the top 3 banks in Indonesia - Bank Central Asia, Bank Rakyat

Indonesia, Bank Mandiri. The Materials sector is expected to see strong EPS growth of 22.6% in both 2022 and 2023,

benefiting from the higher commodity prices and robust demand for commodities.

Additionally, there are a few sectors namely Consumer Discretionary, Consumer Staples and Communication

services, are expected to continue to benefit from the strong consumption growth from the young rising middle class

population.

But all in all, what we like about Indonesia is its broad-based growth across all sectors and not just a few beneficiaries.

In terms of valuations, the JCI index is now trading at 14X P/E based on 2023 estimated earnings, which is several

multiples below our in-house fair P/E of 16.0X. Our end 2023 target price for JCI Index is 7,525 which is a decent 14%

upside potential compared to the current level of around 6,600.

As a conclusion, yes, we think there is still upside for the market that we continue to like Indonesia. However, the

strong rally in 2021 has reduced the upside potential for the market compared to before. Hence, we have downgraded

our Star Ratings for Indonesian equities to 3.0 stars “Attractive” from 3.5 stars "Attractive".

JCI Index FY2021 FY2022 FY2023

PE Ratio (X) 18.5 15.8 14.0

Expected Earnings

- 17.5% 12.3%

Growth (YoY %)

Earnings Per Share

356.6 419.0 470.4

(EPS)

Projected Fair Price

- 6,700 7,525

(Based on 16X Fair PE)

Potential

- - +14.0%

Upside/Downside (%)

Dividend Yield (%) - 2.1% 2.4%

Source: Bloomberg Finance L.P., iFAST compilations. Data as of 4 January 2022.

iFAST Research Team 10 February 2022Disclaimer This article is not to be construed as an offer or solicitation for the subscription, purchase or sale of any fund. No investment decision should be taken without first viewing a fund's prospectus, product highlight sheet (PHS), and if necessary, consulting with financial or other professional advisers. Any advice herein is made on a general basis and does not take into account the specific investment objectives of the specific person or group of persons. Amongst others, investors should consider the fees and charges involved. The relevant prospectuses have been registered and lodged with the Securities Commission. Past performance and any forecast are not necessarily indicative of the future or likely performance of the fund. The value of units and the income from them may fall as well as rise. Where a unit split/distribution is declared, investors are advised that following the issue of additional units/distribution, the NAV per unit will be reduced from pre-unit split NAV/cum-distribution NAV to post- unit split NAV/ex-distribution NAV. Where a unit split is declared, investors should be highlighted of the fact that the value of their investment will remain unchanged after the distribution of the additional units. All applications for unit trusts must be made on the application form accompanying the prospectus. The prospectuses and PHS can be obtained from ifastcapital.com.my. Opinions expressed herein are subject to change without notice. Please read our disclaimer on the website. Investment involves risks. It is as likely that losses will be incurred rather than profit made as a result of buying and selling securities, commodities, foreign exchanges, derivatives or other investments. The price of a security may move up or down, and may become valueless. Past performance is not necessarily indicative of future performance. Foreign investments carry additional risks not generally associated with investments in the domestic market, including but not limited to adverse changes in currency rate, foreign laws and regulations. This document does not and is not intended to identify any or all of the risks that may be involved in the securities or investments referred to herein. Investors should read and fully under-stand all the offering documents relating to such securities or investments and all the risk disclosure statements and risk warnings therein before making any investment decisions. The securities, commodities, foreign exchanges, derivatives or investments referred to in this document may not be suita-ble for all investors. No consideration has been given to any particular investment objectives or experience, financial situa-tion or other needs of any recipient. Accordingly, no representation or recommendation is made and no liability is accept-ed with regard to the suitability or appropriateness of any of the securities and/or investments referred to herein for any particular person's circumstances. Investors should understand the nature and risks of the relevant product and make in-vestment decision(s) based on his/her own financial situation, investment objectives and experiences, willingness and abil-ity to bear risks and specific needs; and if necessary, should seek independent professional advice before making any in-vestment decision(s). This document is not intended to provide any professional advice and should not be relied upon in that regard. iFAST Research Team 10 February 2022

You can also read