SCENAR 2030 PATHWAYS FOR THE EUROPEAN AGRICULTURE AND FOOD SECTOR BEYOND 2020 - Europa EU

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SCENAR 2030

PATHWAYS FOR THE EUROPEAN AGRICULTURE

AND FOOD SECTOR BEYOND 2020

SUMMARY REPORT

FOOD SYSTEMS EFFICIENT, INCLUSIVE AND RESILIENT

SUSTAINABLE USE OF NATURAL RESOURCES

ADDRESS CLIMATE CHANGE

SUSTAINABLE RURAL AREAS

ECO FRIENDLINESS

R. M'barek, J. Barreiro-Hurle,

P. Boulanger, A. Caivano, P. Ciaian,

H. Dudu, M. Espinosa, T. Fellmann,

E. Ferrari, S. Gomez y Paloma,

C. Gorrin Gonzalez, M. Himics,

K. Louhichi, A. Perni, G. Philippidis,

G. Salputra, P. Witzke, G. Genovese

EUR 28883 EN

Joint

Research

Centre

This publication is a Science for Policy report by the Joint Research Centre (JRC), the European Commission’s science and knowledge service. It aims to provide evidence-based scientific support to the European policymaking process. The scientific output expressed does not imply a policy position of the European Commission. Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use that might be made of this publication. Contact information Name: Robert M’barek Address: Email: Robert.M’barek@ec.europa.eu Tel.: +34-954488489 JRC Science Hub https://ec.europa.eu/jrc JRC109053 EUR 28883 EN PDF ISBN 978-92-79-76678-7 ISSN 1831-9424 doi:10.2760/749027 Luxembourg: Publications Office of the European Union, 2017 © European Union, 2017 Reuse is authorised provided the source is acknowledged. The reuse policy of European Commission documents is regulated by Decision 2011/833/EU (OJ L 330, 14.12.2011, p. 39). For any use or reproduction of photos or other material that is not under the EU copyright, permission must be sought directly from the copyright holders. How to cite this report: R. M’barek, J. Barreiro-Hurle, P. Boulanger, A. Caivano, P. Ciaian, H. Dudu, M. Espinosa, T. Fellmann, E. Ferrari, S. Gomez y Paloma, C. Gorrin Gonzalez, M. Himics, K. Louhichi, A. Perni, G. Philippidis, G. Salputra, P. Witzke, G. Genovese; Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 (Summary report), EUR 28883 EN, Publications Office of the European Union, Luxembourg, 2017, ISBN 978-92-79-76678-7, doi:10.2760/749027, JRC109053. All images © European Union 2017. Complex pathways for the European agriculture and food sector by 2030 Analysing stylised scenarios with economic modelling tools reveals complex relations, incentives and trade-offs of the different policy instruments, in particular regarding the environmental dimension. Marginal areas of the EU are most vulnerable to drastic policy changes. Visualisation of results The reader is invited to consult the JRC agro-economic portal DataM at https://datam.jrc.ec.europa.eu for more details of the modelling results in interactive dashboards. The interactive infographics about this study is under the “Agro-economic studies” visualisation section. Direct link: Printed in Spain

SCENAR 2030 Pathways for the European agriculture and food sector beyond 2020 SUMMARY REPORT

TABLE OF CONTENTS

Acknowledgements

Executive summary

1 The Scenar 2030 approach

2 The scenarios

3 The EU agri-food system between markets and

societal challenges (scenarios)

3.1 Economic dimension

3.2 Social dimension

3.3 Environmental dimension

4 Scenar 2030 and the long road ahead: achievements

and remaining challengesTable of contents

Acknowledgements............................................................................................................................................................................................. 9

Executive summary............................................................................................................................................................................................ 10

1 The Scenar 2030 approach.............................................................................................................................................................. 15

2 The scenarios................................................................................................................................................................................................ 17

3 The EU agri-food system between markets and societal challenges (scenarios)......................... 19

3.1 Economic dimension............................................................................................................................................................................. 19

3.2 Social dimension..................................................................................................................................................................................... 23

3.3 Environmental dimension................................................................................................................................................................... 25

4 Scenar 2030 and the long road ahead: achievements and remaining challenges...................... 31

List of figures and tables.............................................................................................................................................................................. 33

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 7ACKNOWLEDGEMENTS / 0 EXECUTIVE SUMMARY

Acknowledgements

The ‘Scenar 2030 – Pathways for the European agriculture The CAPRI model work was carried out by the JRC CAPRI

and food sector beyond 2020’ report was prepared by the team under the leadership of Jesus Barreiro-Hurle (JBH)

European Commission’s Joint Research Centre (JRC) with with support from Peter Witzke (PW) at EuroCARE. The

support from Wageningen Economic Research (WECR) and other team members are: Thomas Fellmann (TF), Mihaly

EuroCARE, as well as contributions from the Directorate- Himics (MH) and Guna Salputra (GS). MH provided the

General for Agriculture and Rural Development. baseline; MH and GS, with the support of PW, implemented

the scenarios; and TF, MH, GS and JBH analysed and cross-

The overall coordination of the study was the responsibility checked the results and drafted the relevant sections of

of Robert M’barek, who also edited the report together the report.

with George Philippidis.

The IFM-CAP model work for Scenar 2030 was carried

The initial design of the study was supported by senior out by the JRC IFM-CAP team under the leadership of

staff of the European Commission (John Bensted-Smith, Pavel Ciaian (PC). The other team members are: Kamel

Tassos Haniotis, David Wilkinson, Jacques Delincé, Pierluigi Louhichi (KL), Maria Espinosa (ME), Angel Perni (AP) and

Londero and Giampiero Genovese) and model experts, in Sergio Gomez y Paloma (SGP). The tasks were performed

particular Hans van Meijl, Martin Banse, Wolfgang Britz, by the team members as follows: data preparation and

Harald Grethe, Thomas Heckelei and John Helming. implementation of CAP direct payments was performed

by ME, KL, PC and AP; baseline preparation was performed

The conceptual development was supported by colleagues by PC, KL and ME; model setting and the implementation

from the Directorate-General for Agriculture and Rural of scenarios was undertaken by KL, PC, ME and AP; result

Development, coordinated by Koen Dillen. visualisation was carried out by AP, KL and ME; and result

cross-checking and analysis, and drafting relevant sections

The MAGNET model work was carried out by the JRC CGE of the report was conducted by PC, KL, ME, AP and SGP.

team under the leadership of Emanuele Ferrari (EF) with

valuable support from George Philippidis (GP) at WECR. The visualisation of results was implemented mainly

The other team members are: Pierre Boulanger (PB), Hasan by Arnaldo Caivano, Celso Gorrin Gonzalez and Saulius

Dudu (HD) and Robert M’barek (RM). GP and EF provided Tamosiunas. Emiliano Bruno and Massimiliano Fucci

the baseline and implemented the scenarios; HD took care designed the cover page. Administrative support was

of result visualisation; and RM, PB, HD and EF analysed provided by Sandra Marcolini, Mathilde Drouin, Els De

the results and drafted the relevant sections of the report. Rademaker and Tanja Acuna.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 9Executive summary

The Common Agricultural Policy (CAP) of the European investigation before any conclusions are made with regard

Union (EU) faces the challenge of evolving towards a to which policy option best meets them. In this context,

multifunctional policy that responds to the constantly expanding the analysis to a food systems approach could

changing needs of society. The CAP must respond to provide further insights into other impacts of the policy

demands related to increased market efficiency and options.

competitiveness; guarantee a territorial balance; fostering

jobs and ‘smart’ growth; contributing to climate change The study considers three scenarios, designed beginning

mitigation while adapting to a changing climate; ensuring of 2016, that take polar paths, against a reference

responsible and sustainable biologically renewable scenario, to characterise different visions for the CAP. The

resource management; and still respecting its initial aim first scenario, Income & Environment (Inc&Env), assumes

of ensuring food security. a more restrictive compliance with agri-environmental

objectives needed for direct payment eligibility while

The present report was carried out by the Joint Research maintaining the EU’s CAP budget at its current nominal

Centre (JRC) and external experts in the context of the level. The second scenario, Liberalisation & Productivity

JRC’s analytical support to the Directorate-General for (Lib&Prod), assumes a strong reduction in subsidies (the

Agriculture and Rural Development. The report analyses removal of Pillar 1 direct payments, which are returned to

the impact on the agricultural sector of stylised scenarios, tax payers), with a shift of Pillar 2 payments to productivity-

reflecting the main drivers of policy debate. While the increasing measures and further trade liberalisation1. As a

scenarios presented do not represent real policy options, variant of the Lib&Prod scenario, the No Policy (NoCAP)

they underline the potential for changes to current agri- scenario also eliminates Pillar 2 payments, thus removing

food policies to address societal challenges and demands. all budgetary support to agriculture.

The analysis of the social, economic and environmental Scenario results emphasize the vulnerability of small

impacts of various options for the next CAP employs the farms, in particular in marginal areas of the EU, where

iMAP platform models MAGNET, CAPRI and IFM-CAP in agricultural subsidies are economically more important

an integrated manner, covering different spatial scales than market income. The trade liberalisation scenarios

(global, EU, Member State, NUTS 2 region and individual reveal opportunities for some but risks for most agri-food

farm levels). sectors. Special attention must be paid to the complex

relations, incentives and trade-offs of the different

The general caveats that apply to all modelling exercises instruments, in particular regarding the environmental

(i.e. a simplified representation of reality, no forecasting dimension. The objective of direct payments has to be

models, high uncertainty, etc.) apply to this study. Moreover, clearly defined and translated into implementation rules

many of the concerns that surround the agricultural policy (i.e. targeting, conditionality) during the policy design

debate, such as generational renewal, value distribution phase, as they still represent the largest share of the

along the food chain and structural change, cannot be budget dedicated to agriculture and steer most of the

captured in the model results and warrant additional sector’s responses. If the objective is redistribution,

1

Cumulative impact of 12 bilateral or regional trade agreements, as described JRC report (2016) “Cumulative economic impact of future trade agreements on EU agricul-

ture”, http://ec.europa.eu/agriculture/trade-analysis/impact-assessment/.

10 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary reportthen the target population needs to be better defined; farm income, greenhouse gas (GHG) emissions from the

if the objective is environmental performance, then agri-food sector, nitrogen surplus, utilised agricultural area

conditionality has to be better designed. and farm jobs. Negative values show a reduction in these

indicators under a given scenario and positive values

The policy scenarios are assessed with regard to their an increase. While an increase in agricultural production

impact on markets (production, demand, trade and prices), and farm income are considered a positive outcome, an

land use, the environment and farmer income from the increase in GHG emissions and nitrogen surplus indicate a

global level to the farm level. The figure below summarises negative impact on the environment and the climate.

the impact of the three scenarios on agricultural production,

Overview of scenario impacts

Agricultural production

5,0%

0,0%

-5,0%

Farm jobs -10,0% Farm income

-15,0%

-20,0%

-25,0%

Utilized agricultural area GHG emissions agrifood

Nitrogen surplus

Inc&Env Lib&Prod NoCap Reference

The Inc&Env scenario shows only marginal changes for through extended greening measures and a limit on

production, land use and emissions. The more pronounced nitrogen use, is associated with a small, economy-wide

focus of this scenario on the environment, implemented cost, but contributes to an improving trend for agricultural

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 11nitrogen balance. However, the reduction of about 1% of Under both the Lib&Prod and NoCAP scenarios, there

the nitrogen surplus in this scenario compared with the would be trade-offs between slightly reduced production,

reference is not sufficient to address the nitrogen balance a mixed impact on the environment and a strongly

problem in areas already in surplus. Under this scenario, negative impact on farm income. Beyond the structural

farm income in the EU increases, but not its distribution, job contraction common in baseline and all scenarios,

as measured by a Gini coefficient. Thus, key challenges most of the additional impacts on jobs will affect

related to the environment and a fair standard of living for small farms in the net beneficiary countries, and would

farmers are only partly addressed, suggesting that even increase farm income inequality even more and put the

more stringent environmental and distributional conditions resilience of many farms at risk. The scenarios show, also

are needed to achieve those objectives. as a consequence of further trade liberalisation, that

there would be an increase in the vulnerability of crop

The Lib&Prod scenario and its even more extreme and cattle/beef farmers. As production decreases and

variant, the NoCAP scenario, have a much stronger consumption remains more or less constant, Europe would

impact on farm income, land use, production and become a net importer of many commodities under these

emissions. The decrease in agricultural production, leading scenarios. This gives rise to concerns about the transfer

to price increases in the NoCAP scenario, is within the of the positive and negative externalities associated with

limit of interannual variation, but is associated with a agricultural production to other world regions.

pronounced reduction in land use. This affects territorial

balance, with marginal areas being further marginalised Finally, the aggregated welfare results are contingent on

or, at worst, abandoned, possibly leading to environmental how effectively the funds released from agricultural policy

degradation, with fewer jobs, and intensive agricultural are used for alternative public expenditure. Our analysis

areas being further concentrated. Less production, in assumes that expenditure in other sectors will increase

principle, reduces the overall use of resources and thus welfare.

reduces environmental impacts like, for example, GHG

emissions. However, if GHG emissions decline in the EU, The Scenar 2030 scenarios show that designing an

this decline is likely to be levelled out through the leakage agricultural policy that tackles all of its societal objectives

effect, by which increased emissions occur in the other is a daunting task. At best, the policy will have to focus on

world regions to which production is shifted. Releasing land key priorities and accept that trade-offs will have to be

from agricultural uses could also provide an opportunity made with regard to others. An internationally competitive

for the creation of carbon dioxide sinks, such as forests agriculture sector in Europe might come at the expense of

and other ecological areas, with important benefits for increased environmental pressures or further job losses in

biodiversity. However, additional measures would be the sector.

needed to ensure that abandoned land is indeed used

to benefit the environment. While a reduction in nitrogen Further research must also be dedicated to identifying

use could be seen as an environmental improvement its the areas in which investing in model linkage does in

reduction will not be homogenously distributed and might fact improve analytical capacity. The JRC should also

even lead to an increase in nitrogen use in some areas, invest some additional resources in improving key

which could increase the corresponding environmental parameters, such as the impact on productivity of

pressure. Pillar 2 payments.

12 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary reportAt the time of finalising this report, the main uncertainties Brexit negotiations. The JRC will continue to support the

about the future of the agricultural sector and its related analysis of these topics using the tools described in this

policies stemmed from the early stages of discussions report.

on the Multiannual Financial Framework 2021-2027 and

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 13THE SCENAR 2030 1 APPROACH

1 The Scenar 2030 approach

The CAP is evolving into a multifunctional policy that can models of the iMAP platform hosted by the JRC. This

respond to the constantly changing needs of society. The suite of economic models ranges from one that models

CAP must meet market-efficiency and competitiveness macroeconomic aspects (a CGE model, i.e. MAGNET4) to

criteria; be a motor of job creation and ‘smart’ growth also in those that model more sectoral economic aspects (a PE

rural areas; continue to aid the fight against climate change model, i.e. CAPRI5) and microeconomic aspects related to

as an environmentally accountable policy measure; act (in the impact on individual farms (IFM-CAP6).

tandem with other policies) as a custodian of responsible and

sustainable biologically renewable resource management; MAGNET, CAPRI and IFM-CAP are run in an integrated

and still respect its initial aim of ensuring sufficient amounts manner on different spatial scales (global, EU, MS, NUTS 2,

of food for all citizens at affordable prices. individual farm), having as a common reference the EU

Agricultural Outlook published at the end of 2015 (DG

Given the above, the design of post-2020 farm policy is AGRI, 2015), generated with the AGLINK-COSIMO7 PE

once again under consultation and a wide range of policy model.

options are being considered, from retaining the status

quo to radical reform. The reference scenario in Scenar 2030 is based on ‘EU

Agricultural Outlook: Prospects for EU agricultural markets

The present report2, in the tradition of the ‘Scenar 2020’ and income 2015-2025’, published in December 2015

studies, contributes to the analysis of selected scenarios (DG AGRI, 2015). It assumes the implementation of the

and provides a framework for further exploration of the 2013 CAP reforms, as well as the ratified FTAs.8

process of designing the future CAP.3 It complements

recent, more qualitative, forward-looking studies with The reader is reminded that the general caveats that apply

a well-elaborated baseline and multiple perspectives to all modelling exercises (i.e. a simplified representation

through the use of different models. of reality, no forecasting models, high uncertainty, etc.)

apply here. Furthermore, using three different models and

This analysis of the social, economic and environmental their (soft) linkages adds complexity and a certain degree

impacts of several options for the next CAP employs of inconsistency (e.g. different commodity categories).

2025 DG AGRI

PRIMES GLOBIOM Market Outlook PRIMES IMAGE

GHG 2030 Trends 2030 Production

Net trade, GHG 2030 Land supply 2030

Productivity

CAPRI 2025 MAGNET Productivity

CAPRI 2030 2030

Models in

Prices Yields Scenar 2030

External

IFM-CAP models

2030 Data flow

FIGURE 1: MODEL CHAIN.

Source: own presentation.

2

This report is a summary of the full Scenar 2030 report, https://datam.jrc.ec.europa.eu/datam/mashup/SCENAR2030.

3

See http://ec.europa.eu/smart-regulation/roadmaps/docs/2017_agri_001_cap_modernisation_en.pdf.

4

Modular Applied GeNeral Equilibrium Tool (MAGNET), http://www3.lei.wur.nl/magnet/.

5

Common Agricultural Policy Regionalised Impact (CAPRI) model; http://www.capri-model.org/docs/capri_documentation.pdf.

6

Individual Farm Model for Common Agricultural Policy Analysis (IFM-CAP); https://doi.org/10.1093/erae/jbx029.

7

AGLINK-COSIMO; http://publications.jrc.ec.europa.eu/repository/bitstream/JRC92618/jrc92618%20online.pdf.

8

Asian FTA means Japan, Vietnam, Thailand, Philippines and Indonesia.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 15THE SCENARIOS 2

2 The scenarios

Scenar 2030 looks at three scenarios that take polar paths, eligibility, while keeping the EU CAP budget at its current

against a reference scenario (the baseline), to characterise nominal level.

different visions for the CAP.

The second scenario (Lib&Prod) was defined to include a

The baseline, or reference scenario (or the business-as- strong reduction in subsidies (the removal of Pillar 1 direct

usual scenario), was generated on the basis of the latest payments, which are returned to tax payers), with a shift

available reference at the time of the study, i.e. the 2015 to productivity-increasing measures and further trade

EU Agricultural Outlook9, with a perspective up to 2025. liberalisation.

The baseline was extended up to 2030 in order to cover

the timeline of the Scenar 2030 study. The third scenario (NoCAP) is a variant of the Lib&Prod

scenario, but it also eliminates Pillar 2 payments, and is

The first scenario (Inc&Env) was defined on the basis of basically intended to represent a removal of agricultural

a more restrictive level of farmer compliance with agri- policy.

environmental objectives needed for direct payment

Income & Environment Liberalisation & Productivity NoCAP

(Inc&Env) (Lib&Prod) (Incl. liberalisation)

Extended greening, Pillar 1&2 Trade Pillar 1 Pillar 2 Trade Pillar 1 Pillar 2

Nitrogen limits Budget changes liberalisation Budget removed Investments liberalisation Budget removed removed

Productivity

CAPRI MAGNET CAPRI MAGNET CAPRI MAGNET

2030 2030 2030 2030 2030 2030

Prices Yields Prices Yields Prices Yields

Extended greening, IFM-CAP IFM-CAP IFM-CAP

Nitrogen limits

2030 2030 2030

Various indicators on different spatial scales Various indicators on different spatial scales Various indicators on different spatial scales

FIGURE 2: OVERVIEW OF THE SCENARIOS.

Source: own presentation.

The policy scenarios are assessed with regard to their to the farm level. In the following section, the key results

impact on markets (production, demand, trade and prices), are presented in relation to their economic, social and

land use, environment and farmer income from the global environmental dimensions.

9

EU Agricultural Outlook: Prospects for EU agricultural markets and income 2015-2025. Directorate-General for Agriculture and Rural Development, European Com-

mission.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 17THE EU AGRI-FOOD SYSTEM

3 BETWEEN MARKETS AND

SOCIETAL CHALLENGES

(SCENARIO RESULTS)3 The EU agri-food system between markets

and societal challenges (scenario results)

In the following section, the key results of the three in terms of changes with respect to the results given by

scenarios are described according to the economic, social the baseline (reference or business as usual scenario).10

and environmental dimensions. The results are presented

3.1 | Economic dimension

Agricultural production is declining, but not disappearing, in most extreme

scenarios

The results show a small negative impact on agricultural 4% and 6%, respectively. The differences between EU-15

production under the Inc&Env scenario, whereas under the and EU-13 are negligible, and the variability between EU

Lib&Prod and NoCAP scenarios production decreases by MSs is greatest under the NoCAP scenario.

Inc&Env Lib&Prod NoCap

0%

-1%

-2%

-3%

-4%

-5%

-6%

-7%

EU28 EU15 EU13

FIGURE 3: AGRICULTURAL PRODUCTION, EU-28, TOTAL QUANTITY CHANGES COMPARED WITH REFERENCE (%).

Source: Scenar 2030, CAPRI model.

Producer prices increase if the CAP is eliminated

Following the small decreases in agricultural production elimination of all CAP payments, the stronger EU production

under the Inc&Env scenario, aggregated EU producer declines cannot be fully compensated by imports, leading

prices increase by about 1%. In the Lib&Prod scenario, to increased aggregated EU producer prices of about 5% in

EU producer prices drop by almost 1%, as EU production the NoCAP scenario.

decreases are compensated by cheaper imports. With the

6%

5%

4%

3%

2%

1%

0%

-1%

Inc&Env Lib&Prod NoCap

-2%

EU28 EU15 EU13

FIGURE 4: PRODUCER PRICE, EU-28, CHANGES COMPARED WITH REFERENCE (%).

Source: Scenar 2030, CAPRI model.

10

More details can be found under this link: https://datam.jrc.ec.europa.eu/datam/mashup/SCENAR2030.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 19More imports than exports 30.000

20.000

Imports increase in all scenarios, leading to a decrease in 10.000

Imports

the EU trade balance. Although exports in the Lib&Prod 0 Exports

scenario grow substantially, also thanks to the ambitious Trade Balance

-10.000

trade agenda pursued by the EU, they cannot compensate

for the higher level of imports. In the NoCAP scenario, -20.000

the trade balance is reduced by about EUR 25 billion, -30.000

Inc&Env Lib&Prod NoCap

billion trade surplus in 2030 under the reference scenario,

bringing back the EU to net importer status. FIGURE 5: EU IMPORTS, EXPORTS AND TRADE BALANCE CHANGES (EUR

MILLION) COMPARED WITH REFERENCE, 2030.

Source: Scenar 2030, MAGNET model.

Income of farms decreases strongly when the CAP is abolished

Under the Inc&Env scenario, gross farm income increases following the larger decreases in EU production. Again,

by around 4.5%, mainly through higher prices, with the the EU-13 farming sector experiences a stronger negative

CAP budget remaining stable. The negative effects in the impact on income than the EU-15, reflecting a generally

Lib&Prod scenario (–20%) mean that there is a slightly higher importance of CAP payments in total income..

larger income decrease than under the NoCAP scenario,

10,0%

Inc&Env Lib&Prod NoCap

0,0%

-10,0%

-20,0%

-30,0%

-40,0%

EU28 EU15 EU13

FIGURE 6: GROSS FARM INCOME (% CHANGE RELATIVE TO REFERENCE).

Source: Scenar 2030, CAPRI model.

The simulated effects are less heterogeneous between

Inc&Env Lib&Prod NoCAP

economic sizes classes than they are across farm

Specialist COP 1.2 –23.5 –22.6

specialisations. However, there is a relatively consistent

Specialist other field crops 0.4 –2.1 –0.2

pattern indicating an inverse relationship between the

Specialist horticulture –0.9 1.9 0.8

magnitude of the simulated impacts and economic farm

Specialist wine 0.4 –7.1 –7.6

size in all three simulated scenarios. Among the most

Specialist orchards – fruits –2.7 –4.0 –6.2

affected farm specialisations, mainly in the Lib&Prod and

Specialist olives –11.6 –20.6 –19.9

NoCAP scenarios, are the specialists cattle, COP (cereals,

Permanent crops combined –1.5 –7.7 –9.2

Specialist milk –0.1 –8.7 2.6

oilseeds and protein), and olives.

Specialist sheep and goats –0.5 –12.1 –11.9

Specialist cattle –2.3 –36.7 –31.8

Specialist granivores 1.0 –3.7 3.6

Mixed crops –0.3 –2.8 –3.6

Mixed livestock 1.8 –12.0 –3.0

Mixed crops and livestock 0.2 –14.8 –9.7

TABLE 1: INCOME VARIATION BY FARM SPECIALISATION IN THE EU-27 (%

CHANGE RELATIVE TO REFERENCE).

Source: Scenar2030, IFM-CAP.

20 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary reportOverall, economic growth effects are small, but are substantial for some

Member States

The CAP has an important role to play in territorial cohesion. EU-13. In general, the gains observed in the scenarios with

The effect of the scenarios on GDP is very small (maximum a large or complete reduction in CAP payments for the EU-

–0.3% in the NoCAP scenario for the EU-13); however, 15 countries drive the EU-28 GDP to a small but positive

under all scenarios, changes in GDP are negative for the value.

0,3%

0,2%

0,1%

0,0%

Inc&Env Lib&Prod NoCap

-0,1%

-0,2%

-0,3%

-0,4%

EU28 EU15 EU13

FIGURE 7: GDP, CHANGE FROM REFERENCE (%), 2030.

Source: Scenar 2030, MAGNET model.

When looking at the individual MS results, sizeable One can observe that most of the EU-13 and some EU-15

impacts are observed for Croatia, Cyprus, Greece, Latvia countries not only experience a high absolute per capita

and Lithuania, who lose up to 1.7% of their GDP compared welfare loss, but even more in relative terms (here in %

with the reference scenario. change of household expenditure).

Small increase of prosperity, but only for richer EU-15 countries

Using so-called Equivalent variation (EV) as a welfare The welfare decomposition highlights the reasons behind

measure, i.e. the real income change, we observe a similar these developments. The EV results in, for instance, the

pattern as that observed for GDP, namely that the scenarios Lib&Prod scenario show losses for the ‘new’ EU-13 MSs

have only small impacts on welfare. Compared with the vis-à-vis EV gains for the ‘old’ EU-15 MSs. For the EU-13

reference scenario in 2030, the Inc&Env scenario for the MSs this result is mainly driven by changes to the CAP

EU-28 results in a slightly negative EV of EUR 2.6 billion budget, whereas efficiency gains and improving terms

(–0.08%), the Lib&Prod scenario shows a EUR 18.4 billion of trade occur in the EU-15 MSs and lead to an overall

welfare gain (+0.15%) and, finally, the NoCAP scenario positive welfare effect in the Lib&Prod scenario..

shows a EUR 0.1 billion welfare gain (+0.01%).

30.000

25.000

Allocative

20.000

15.000 CAP Budget

10.000 Distributional

5.000 Endowment

0 Population

-5.000 Technological

-10.000

Terms of Trade

-15.000

Total

-20.000

Inc&Env Lib&Prod NoCap Inc&Env Lib&Prod NoCap Inc&Env Lib&Prod NoCap

EU28 EU15 EU13

FIGURE 8: WELFARE (EV) DECOMPOSITION IN THE EU-28, EU-15 AND EU-13, 2030, EUR MILLIONS, SCENARIOS VS. REFERENCE.

Source: Scenar 2030, MAGNET model.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 21The time dimension of scenario shocks matters for welfare

The dynamics of the scenarios’ impacts on welfare (and In the Lib&Prod scenario, and even more so in the NoCAP

other indicators) have to be closely observed, on the one scenario, EU-13 welfare growth shows a substantial de-

hand to anticipate temporary hardships and the necessary cline in 2025 after the policy change in 2020, but recovers

accompanying measures, on the other hand to monitor the in the period from 2025 to 2030 due to the market evolu-

recovering of an economy after a (structural) adjustment. tion and structural adjustment of the economy.

EU28 EU15 EU13

3

2

1

0

-1

-2

-3

-4

-5

-6

-7

-8

2025 2030

Lib&Prod NoCap Lib&Prod NoCap

Inc&Env Inc&Env

FIGURE 9: WELFARE GROWTH, CHANGES (%) FROM BASELINE FROM ONE PERIOD TO THE NEXT WITHIN A SCENARIO, IN EUR BILLION.

Source: Scenar 2030, MAGNET model.

22 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report3.2 | Social dimension

In this subsection, the income distribution among farms

and the impacts on jobs are analysed.

Small farms lose a higher proportion of their incomes than larger farms

With the exception of the smallest farms in the Inc&Env higher than for larger farms. It should be noted that the

scenario, all farm sizes lose income under all scenarios. income calculation on the farm level is slightly different

The smaller farms are generally more affected because from the gross farm income calculation.

the share of subsidies in their total income is usually

8 000 -< 25 000 25 000 -< 100 000 100 000 -< 500 000

2 000 -< 8 000 EUR EUR EUR EUR >= 500 000 EUR

5

0

-5

-10

-15

-20

Inc&Env Lib&Prod NoCAP

FIGURE 10: INCOME VARIATION BY ECONOMIC FARM SIZE IN THE EU-28 (% CHANGE RELATIVE TO REFERENCE).

Source: Scenar 2030, IFM-CAP model.

CAP subsidies play an income equalisation role among inequality, where a higher Gini coefficient indicates higher

farms in the EU. Decreasing or cutting payments increases inequality.

Gini coefficient

0.77

0.76 0.758

0.752

0.75

0.74

0.73

0.72

0.71 0.707

0.705

0.7

0.69

0.68

0.67

Reference Inc&Env Lib&Prod NoCAP

FIGURE 11: GINI COEFFICIENT FOR INCOME DISTRIBUTION IN THE EU-27.

Source: Scenar 2030, IFM-CAP.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 23Job numbers decrease

Under all three scenarios, in addition to the job decline of and NoCAP scenarios (–5%) than in the Inc&Env scenario

about 25% in the reference scenario, there is a negative (–1.8%). Decreases in employment in the food industry are

effect on jobs in the agricultural sector. The decrease less noticeable.

in agricultural jobs is more pronounced in the Lib&Prod

Inc&Env Lib&Prod NoCap

0%

-1%

-2%

-3%

-4%

-5%

-6%

EU28 EU15 EU13

FIGURE 12: IMPACT OF SCENARIOS ON EMPLOYMENT NUMBERS, 2030.

Source: Scenar 2030, MAGNET model.

%

+2

-14

FIGURE 13: IMPACT OF LIB&PROD SCENARIO ON EMPLOYMENT NUMBERS

(IN % CHANGE), 2030.

Source: Scenar 2030, MAGNET model.

24 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report3.3 | Environmental dimension

With regard to the environmental dimension, the results

are considered in the context of land use, nitrogen surplus

and GHG emissions.

More land is abandoned with diverse impacts

The slight increase in UAA in the Inc&Env scenario of 0.3% directly linked to the removal of direct payments, which

(+0.6 million ha) contrasts with the substantial decreases immediately affect the profitability of all crop production

of 7.3% (–13.1 million ha) in the Lib&Prod scenario and activities, and the decreases in EU production levels, es-

about 6.9% (–12.4 million ha) in the NoCAP scenario. The pecially the decline in cereal production and pasture, i.e.

decreases in UAA in the Lib&Prod and NoCAP scenarios are part of the land is taken out as economic returns decrease.

2%

Inc&Env Lib&Prod NoCap

0%

-2%

-4%

-6%

-8%

-10%

EU28 EU15 EU13

FIGURE 14: UAA, % CHANGE.

Source: Scenar 2030, CAPRI model.

Under the Inc&Env scenario, UAA increases by 0.3% (+0.6 the Lib&Prod scenario and by about 6.9% (–12.4 million

million ha) compared with the reference scenario, whereas ha) in the NoCAP scenario.

UAA substantially declines, by 7.3% (–13.1 million ha), in

Inc&Env Lib&Prod NoCAP

5,0%

0,0%

-5,0%

-10,0%

-15,0%

-20,0%

ry

ly

lta

a

-28

-15

ria

m

en

d

a

ece

ic

in

any

m

d

and

atia

nce

ia

ic

Rom l

ia

via

tria

3

ark

nds

rus

a

lan

ani

oni

lan

-N1

ubl

Ita

ubl

Spa

nga

uan

ven

gdo

tug

giu

d

lga

Ma

Lat

Cyp

nm

Gre

Aus

Fra

EU

EU

rm

e

Pol

rla

Cro

Est

Ire

Fin

Rep

Rep

Sw

Bel

Por

EU

Slo

Hu

Bu

Lith

Kin

Ge

the

De

ch

vak

ited

Ne

Cze

Slo

Un

FIGURE 15: CHANGE IN UAA PER MS (CHANGE RELATIVE TO REF).

Source: Scenar 2030, CAPRI model.

A similar decrease in grassland area (–8.8%) can be maintenance of (permanent) grassland. This is relevant

observed, driven by the removal of direct payments from a public goods point of view (e.g. landscape, tourism).

and by the absence of any CAP measure targeting the

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 25Nitrogen - a particular challenge

High concentrations of nitrates in the soil and water the Inc&Env scenario, by 1%. The increase of 3% in the

constitute a widespread problem caused by nitrogen Lib&Prod scenario illustrates the challenge of sustainable

surplus. Nitrogen surplus per ha decreases under only intensification.

4%

3%

2%

1%

0%

-1%

Inc&Env Lib&Prod NoCap

-2,%

EU28 EU15 EU13

FIGURE 16: NITROGEN SURPLUS PER HA.

Source: Scenar 2030, CAPRI model.

The limitation in animal stocking density and the restriction UAA, respectively. The increase in N-surplus is, on the one

on nitrogen use lead to a decrease in the N-surplus of hand, driven by the decrease in UAA and, on the other

0.8 kg N/ha UAA. A considerable reduction is reported hand, the intensification of livestock and crop production

in particular in Member States and regions with a high on the remaining UAA. In both scenarios, more substantial

N-surplus in the reference scenario, such as Belgium and increases in N-surplus are indicated for regions that already

the Netherlands, mostly related to reductions in stocking have the highest N-surplus in the reference scenario, as

densities. In contrast, under the Lib&Prod and NoCAP these are among the most competitive regions.

scenarios, the N-surplus increases by 2 and 0.5 kg N/ha

Inc&Env Lib&Prod NoCAP

7

6

5

4

3

2

1

0

-1

-2

-3

-4

-5

-6

-7

-28

-15

3

tria

m

ia

atia

ly

via

rus

ic

ark

a

d

nce

any

ece

ry

and

ia

nds

and

al

a

ic

ia

in

en

m

lan

oni

ani

-N1

ubl

ubl

Ita

Spa

gar

uan

ven

tug

nga

giu

gdo

d

Lat

Cyp

nm

Aus

Gre

Fra

rla

EU

EU

rm

e

Irel

Pol

Cro

Est

Rom

Fin

Rep

Rep

Sw

Bel

Bul

Por

EU

Slo

Lith

Hu

Kin

the

De

Ge

ch

vak

Ne

ited

Cze

Slo

Un

FIGURE 17: CHANGE IN N-SURPLUS PER MS (ABSOLUTE CHANGE IN KG N/HA UAA RELATIVE TO REF).

Note: Malta has been removed from the graph to improve the readability. The values for Malta are: Inc&Env -14%, Lib&Prod +17%, NoCAP +12%”.

Source: Scenar2030, CAPRI.

Looking at the regional distribution of the N-surplus the

increase is concentrated in productive areas that already

have high N-surplus in the reference scenario.

26 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary reportGHG emissions – a question of leakage?

The GHG emissions of EU agriculture follow directly the

production developments. Therefore, changes are rather

limited in the Inc&Env scenario, with a decrease of 0.5% in

EU-28 emissions; however, considerably larger decreases

are indicated under the Lib&Prod scenario (–4.2%) and

NoCAP scenario (–5.8%). The impact of technological

GHG mitigation options is very limited in the scenarios

(i.e. the technologies are not widely applied), which is why

the predicted GHG changes mirror production changes so

closely. Moreover, the GHG emission analysis does not

take into account that the land taken out of EU production

could be used for afforestation and therefore as a carbon

sink. At the MS level, the changes in agricultural non CO2

GHG emissions also reflect the corresponding production

changes in the scenarios.

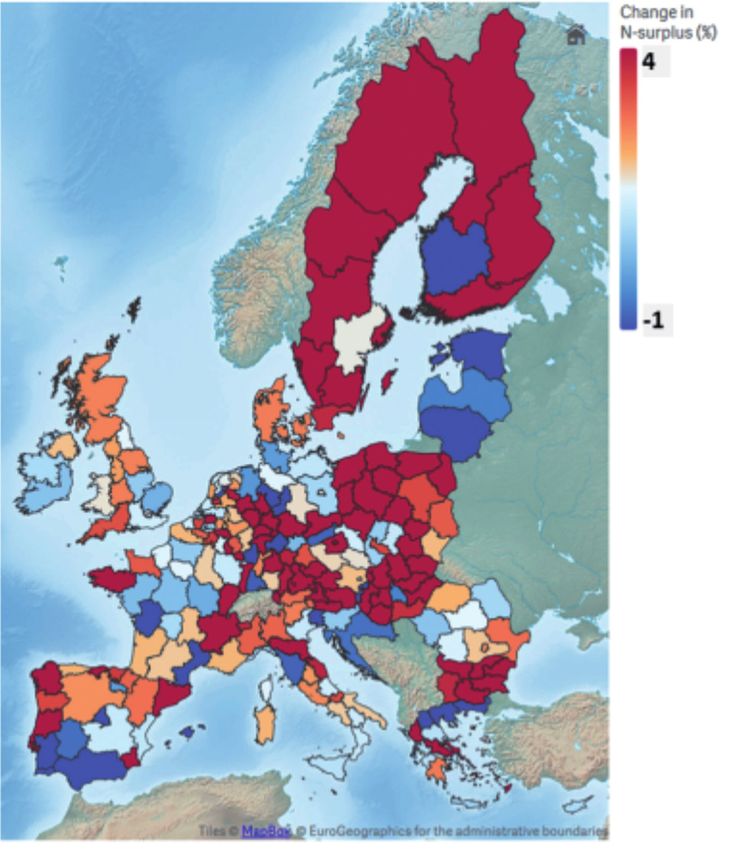

FIGURE 18: NITROGEN SURPLUS PER HA, % CHANGES IN THE LIB&PROD

SCENARIO.

Source: Scenar 2030, CAPRI model.

Inc&Env Lib&Prod NoCap

0,0%

-1,0%

-2,0%

-3,0%

-4,0%

-5,0%

-6,0%

-7,0%

EU28 EU15 EU13

FIGURE 19: CHANGE IN AGRICULTURAL NON-CO2 GHG EMISSIONS (%).

Source: Scenar 2030, CAPRI model.

REF Inc&Env Lib&Prod NoCAP

80

Mio tonnes CO2 eq

70

60

50

40

30

20

10

0

S in

De lic

Fin a

Ire y

ly

Gr y

Bu m

Po d

nd

tia

Ge ce

Sl lic

m

ia

Sl Rom al

ia

Lit ia

ria

er a

Re ia

Ki en

ia

nd

Hu ce

Es k

s

Re s

ar

an

ni

n

nd

u

ar

t

Ita

a

an

en

tv

g

n

ar

iu

do

b

l

b

an

ee

la

la

ec ypr

d

oa

la

st

Ne Ma

Sp

to

a

ng

rtu

nm

pu

pu

rm

la

lg

La

ite we

lg

Po

ov

hu

ng

Au

Fr

Cr

Be

C

th

h

ak

d

ov

Cz

Un

FIGURE 20: AGRICULTURAL NON-CO2 GHG EMISSIONS IN THE EU MSs (IN MIO TONNES CO2 EQ).

Source: Scenar 2030, CAPRI model.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 27From a worldwide perspective, the emission reductions the increase of agricultural GHG emissions in Mercosur

in the EU are widely compensated by emission increases or Australia & New Zealand. As a result of emission

in non-EU countries, mainly due to increased production leakage, the net benefit of EU emission reductions on

and exports of agricultural commodities to the EU. This global agricultural GHG emissions is minimal.

emission leakage effect is for example illustrated by

3,5

3,0

2,5

2,0

1,5

1,0

0,5

0,0

NAFTA Mercosur Australia & New Zealand Asian FTA

-0,5

Inc&Env Lib&Prod NoCap

FIGURE 21: GHG EMISSIONS IN AGRICULTURE, DIFFERENT REGIONS, 2030, DIFFERENCE (%) FROM REFERENCE.

Note: Asian FTA means bilateral trade agreements between the EU and Japan, Vietnam, Thailand, Philippines and Indonesia respectively.

Source: Scenar 2030, MAGNET model.

The main caveat in relation to the scenarios’ consideration importance of GHG emission leakage through increased

of GHG emissions is that only a rough estimation of GHG EU imports.

emissions is possible. However, the main message is the

28 Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary reportSCENAR 2030 AND THE

4 LONG ROAD AHEAD:

ACHIEVEMENTS AND

REMAINING CHALLENGES4 Scenar 2030 and the long road ahead:

achievements and remaining challenges

The present study offers a well-established, model- During the course of this study, experiences have revealed

based agro-economic analysis enriched with new repeatedly that the linkage of models is a challenge.

features, providing a framework for future policy analysis. Furthermore, the assumptions on the impact of policies on

In particular, an attempt has been made to deliver a productivity are of particular importance, pointing to the

fully transparent study report, linked to an interactive need for more research.

visualisation of the results.

At the time of finalising this report, many uncertainties

The scenarios chosen are instructive and show the about the future of the agricultural sector remain. They

existence of trade-offs. include the early stage of discussions on the Multiannual

Financial Framework (MFF) 2021-2027, the Brexit, the

In particular, the combination of different types of models ongoing free trade negotiations, the implementation of

allows the analysis of the scenarios from all three COP21 and SDGs, the Renewable Energy Directive, and the

sustainability perspectives and on different spatial scales, evolving bioeconomy among others.

i.e. from the global market to the individual farm level.

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 31LIST OF FIGURES AND TABLES

List of figures

Figure 1: Model chain.............................................................................................................................................................................................................. 15

Figure 2: Overview of the scenarios............................................................................................................................................................................. 17

Figure 3: Agricultural production, EU-28, changes compared with reference (%)...................................................................... 19

Figure 4: Producer price, EU-28, changes compared with reference (%).......................................................................................... 19

Figure 5: EU imports, exports and trade balance changes (EUR million) compared with reference, 2030.............. 20

Figure 6: Gross farm Income (% change relative to reference)................................................................................................................ 20

Figure 7: GDP, change from base line (%), 2030................................................................................................................................................ 21

Figure 8: Welfare (EV) decomposition in the EU-28, EU-15 and EU-13, 2030, EUR millions, scenarios vs.

reference.................................................................................................................................................................................................................... 21

Figure 9: Welfare growth, changes (%) from baseline from one period to the next within a scenario, in EUR

billion, for all scenarios in years 2025 and 2030......................................................................................................................... 22

Figure 10: Income variation by economic farm size in the EU-28 (% change relative to reference).............................. 23

Figure 11: Gini coefficient for income distribution in the EU-27................................................................................................................. 23

Figure 12: Impact of scenarios on employment numbers, 2030............................................................................................................... 24

Figure 13: Impact of Lib&Prod scenario on employment numbers (in % change), 2030........................................................ 24

Figure 14: Utilised agricultural area (UAA), % change....................................................................................................................................... 25

Figure 15: Change in UAA per MS (change relative to REF)........................................................................................................................... 25

Figure 16: Nitrogen surplus per ha................................................................................................................................................................................... 26

Figure 17: Change in N-surplus per MS (absolute change in kg N/ha UAA relative to REF)................................................... 26

Figure 18: Nitrates per ha, % changes in the Lib&Prod scenario............................................................................................................... 27

Figure 19: Global warming potential of agriculture, change in %............................................................................................................. 27

Figure 20: Agricultural non-CO2 GHG emissions in the EU MSs (in Mio tonnes CO2 eq)............................................................ 27

Figure 21: GHG emissions in agriculture, different regions, 2030, difference (%) from reference..................................... 28

List of tables

Table 1: Income variation by farm specialisation in the EU-27 (% change relative to reference)....................................... 20

Scenar 2030 - Pathways for the European agriculture and food sector beyond 2020 - Summary report 33Europe Direct is a service to help you find answers

to your questions about the European Union.

Freephone number (*):

00 800 6 7 8 9 10 11

(*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you).

More information on the European Union is available on the internet (http://europa.eu).

HOW TO OBTAIN EU PUBLICATIONS

Free publications:

• one copy:

via EU Bookshop (http://bookshop.europa.eu);

• more than one copy or posters/maps:

from the European Union’s representations (http://ec.europa.eu/represent_en.htm);

from the delegations in non-EU countries (http://eeas.europa.eu/delegations/index_en.htm);

by contacting the Europe Direct service (http://europa.eu/europedirect/index_en.htm) or

calling 00 800 6 7 8 9 10 11 (freephone number from anywhere in the EU) (*).

(*) The information given is free, as are most calls (though some operators, phone boxes or hotels may charge you).

Priced publications:

• via EU Bookshop (http://bookshop.europa.eu).KJ-NA-28883-EN-N

JRC Mission

As the science and knowledge

service of the European Commission,

the Joint Research Centre’s mission

is to support EU policies with

independent evidence throughout

the whole policy cycle.

EU Science Hub

ec.europa.eu/jrc

@EU_ScienceHub

EU Science Hub - Joint Research Centre

Joint Research Centre

EU Science Hub

doi:10.2760/749027

ISBN 978-92-79-76678-7You can also read