Refrigeration and Air Conditioning Green-house Gas Inventory for the Philippines

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Refrigeration and Air Conditioning Green- house Gas Inventory for the Philippines

As a federally owned enterprise, GIZ supports the German Government in achieving its objectives in the field of international cooperation for sustainable development. Published by: Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH Registered offices Bonn and Eschborn Friedrich-Ebert-Allee 36 + 40 53113 Bonn, Germany T +49 228 44 60 - 0 F +49 228 44 60 - 17 66 Dag-Hammarskjöld-Weg 1–5 65760 Eschborn, Germany T +49 (0) 6196 79 - 4218 F +49 (0) 6196 79 - 804218 proklima@giz.de www.giz.de/proklima Programme/project description: Cool Contributions fighting Climate Change (C4)/ Proklima In cooperation with Department of Energy Department of Environment and Natural Resources Responsible: Philipp Munzinger, C4 Project Manager (GIZ Proklima) Authors and Data Collectors: Regina Karakina, Dr. Simon Mischel (HEAT GmbH) Rolando Abad, Jr., Onofre Escota (DENR-EMB), Ella Deocadiz, Manuel Azucena, Orland Tubola, Jhunearl Getalaga, Fausto Abadines Acknowledgement for Review and Input Maraida Licerio, Philipp Munzinger (GIZ) Photo credits/sources Cover photo: © GIZ Proklima Design: Jeanette Geppert pixelundpunkt kommunikation, Frankfurt URL links: This publication contains links to external websites. Responsibility for the content of the listed external sites a lways lie with their respective publishers. When the links to these sites were first posted, GIZ checked the third-party con- tent to establish whether it could give rise to civil or criminal liability. However, the constant review of the links to external sites cannot reasonably be expected with concrete indication of a violation of rights. If GIZ itself becomes aware or is notified by a third party that an external site it has provided a link to gives rise to civil or criminal liability, it will remove the link to this site immediately. GIZ expressly dissociates itself from such content. Maps: The maps printed here are intended only for information purposes and in no way constitute recognition under international law of boundaries and territories. GIZ accepts no responsibility for these maps being entirely up to date, correct or complete. All liability for any damage, direct or indirect, resulting from their use is excluded. On behalf of The German Federal Ministry for the Environment, Nature Conservation and Nuclear Safety Division KI II 7 International Climate Finance, International Climate Initiative 11055 Berlin, Germany T +49 30 18 305-0 F +49 30 18 305-43 75 GIZ is responsible for the content of this publication. Printed and Distributed by GIZ 2019 Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH Publication Date and Place July 2019, Manila

© trainman32 / fotolia

This publication is a product of the Cool Contributions fighting Climate Change (C4)

Project implemented by GIZ Proklima. It is part of the International Climate Initiative (IKI).

The Federal Ministry for the Environment, Nature Conservation, and Nuclear Safety (BMU)

supports this initiative on the basis of a decision adopted by the German Bundestag. The

project supports an international control for F-gases in combination with increased

energy efficiency in the refrigeration and air conditioning sector. It strengthens cooperation

between various initiatives such as the UNFCCC and the Montreal Protocol by promoting

a coordinated agreement and reducing overlaps. Furthermore, the project advises s elected

partner countries in formulating national GHG mitigation strategies in the refrigeration

and air conditioning sector and thereby advancing their NDCs. The project runs from 2016

until 2021.

3

TABLE OF CONTENTS

LIST OF FIGURES AND TABLES 6/7

ACKNOWLEDGEMENTS 10

SUMMARY 11

1. INTRODUCTION 14

1.1 Project framework 14

1.2 Importance and benefits of RAC sector inventories 14

1.3 Geography and basic information of the Philippines 16

1.4 Energy production, energy consumption and other factors influencing the growth of

RAC appliances 16

1.5 RAC stakeholders 18

1.6 Climate and F-gas policies 19

2. SCOPE OF THE INVENTORY 20

2.1 Methodology 21

2.2 Data collection process 23

2.3 Modelling parameters 24

3. RESULTS 26

3.1 Subsector sales and stock data analysis 26

3.1.1 UAC sales and stock data 26

3.1.2 AC chillers sales and stock data 27

3.1.3 Mobile air conditioning 28

3.1.4 Domestic refrigeration 30

3.1.5 Commercial refrigeration 30

3.2 BAU emissions and projections in the RAC sector 32

4 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES

3.3 Total emissions 33

3.3.1 Mitigation scenario emissions for the Philippine RAC sector 33

3.3.2 Energy saving potential 35

3.3.3 Use of low-GWP refrigerants 35

3.3.4 Reporting to UNFCCC 37

3.3.5 Unitary air conditioning emissions 37

3.3.6 AC chiller emissions 38

3.3.7 Mobile air conditioning emission mitigation potential 39

3.3.8 Domestic refrigeration emission mitigation potential 40

3.3.9 Commercial refrigeration emission mitigation potential 40

4 REFERENCES 42

5 ANNEX 44

5.1 Contacted companies via questionnaires of unitary air conditioning and

domestic refrigeration subsectors 44

5.2 Subsector definitions 44

5.3 Applied modelling parameters and results of model calculations 47

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 5

LIST OF FIGURES AND TABLES

Figure 1: Projected Business-as-Usual (BAU) scenario for GHG emissions in the RAC sector until 2050

and the predicted MIT emissions 11

Figure 2: Projected Business-as-Usual (BAU) scenario for GHG emissions with the Kigali amendment

in the RAC sector until 2050 and the predicted MIT emissions 12

Figure 3: Mitigation potential of the Philippine RAC sector in the year 2050. The grey color of the first

column shows the unabated emissions. The next columns to the right of the first column

show the emission mitigation potential of each subsectors both for direct (dark blue) and

indirect (light blue) emissions 12

Figure 4: BAU, the BAU under Kigali and MIT scenarios of HFC consumption and Kigali schedule 13

Figure 5: Climate chart of Manila. Source: compiled by www.klimadiagramme.de, source:

National Climatic Data Centre (NCDC) 16

Figure 6: Total primary energy supply (TPES) for the Philippines for the year 2016, Mtoe =

Million-tons oil equivalent 17

Figure 7: Energy consumption by sector, Mtoe = Million tons oil equivalent 17

Figure 8: Approaches for GHG emission estimates relevant to the RAC&F sector (Munzinger et al., 2016) 21

Figure 9: Overview RAC refrigerant demand versus RAC total emissions 22

Figure 10: Unitary AC units sold (2010 to 2016) 26

Figure 11: Unitary AC unit stock historic and forecasted (2010 to 2017; 2018 to 2050) 27

Figure 12: Sold units (2010 to 2016, top) and stock units of AC chiller (2010 to 2050, bottom) 28

Figure 13: Sales 2010 to 2016 in the mobile AC subsector 29

Figure 14: Stock unit development (2010 to 2050) in the mobile AC subsector 29

Figure 15: Domestic refrigeration unit stock taken from the GCI database (2010-2050) and

adjusted by expert knowledge 30

Figure 16: Stock data (2010-2050 CGI database projections) from the commercial refrigeration sector 30

Figure 17: Total BAU GHG emission for the Philippine RAC sector by subsectors in 2017 31

Figure 18: Direct GHG emissions of the RAC subsectors in 2017 31

Figure 19: Indirect GHG emissions of the RAC subsectors in 2017 31

Figure 20: Projected BAU GHG emissions in the RAC sector for the years 2010-2050 32

Figure 21: Total annual emissions from the RAC sector, BAU and mitigation scenario 33

Figure 22: Direct and indirect mitigation potential for the year 2030. The grey color of the first

column shows the unabated emissions. The columns to the right of the first column

show the emission mitigation potential of each subsectors both for direct (dark blue)

and indirect (light blue) emissions 34

Figure 23: Chart showing the direct and indirect mitigation potential for the year 2050. The grey color

of the first column shows the unabated emissions. The columns to the right of the first

column show the emission mitigation potential of each subsectors both for direct (dark blue)

and indirect (light blue) emissions 34

6 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES

Figure 24: Total cumulative energy saving potential (17.9 TWh) of the Philippine RAC sector (2018 to 2030) 35

Figure 25: Total cumulative energy saving potential (214.5 TWh) of the Philippine RAC sector (2018-2050) 35

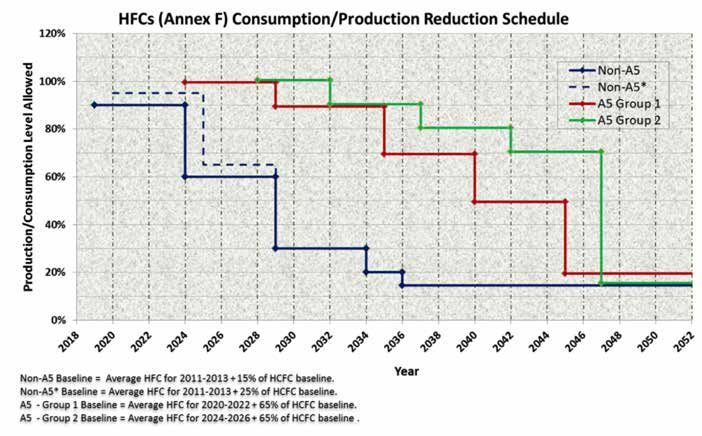

Figure 26: HFC reduction steps according to UNEP 36

Figure 27: HFC consumption under BAU, BAU-Kigali and mitigation (MIT) scenario and Kigali schedule 37

Figure 28: Projected GHG emissions of the unitary air conditioning subsector for the years 2010 to 2050 38

Figure 29: Projected GHG emissions of the chiller subsector for the years 2010 to 2050 39

Figure 30: Projected GHG emissions of the mobile air conditioning subsector for the years 2010 to 2050 39

Figure 31: Total emission of the Domestic refrigeration sector for the years 2010 to 2050 40

Figure 32: Total emission of the commercial refrigeration subsector for the years 2010 to 2050 41

Table 1: Statistical data of the Philippines 17

Table 2: Overview of institutions relevant for the RAC sector and their contribution to the survey 18

Table 3: RAC subsectors and related systems 20

Table 4: Modelling parameters for BAU scenario 24

Table 5: Assumed future growth rates of appliance sales 25

Table 6: Sold units for the AC chiller subsector for the years 2010 to 2015 27

Table 7: Mobile AC sales data for the years 2010-2015 (calculated from GCI stock estimates) 29

Table 8: List of contacted companies 44

Table 9: Overview of air conditioning subsectors 44

Table 10: Description of Iran’s special case equipment 45

Table 11: Overview of refrigeration subsectors 46

Table 12: Assumed average energy efficiency ratios in equipment sales for the Business as

Usual scenario 47

Table 13: Refrigerant distribution in sales for Business as Usual and Mitigation scenario 48

Table 14: Calculated sales 51

Table 15: Calculated stock 52

Table 16: Common reporting format (CRF) 2016 54

Table 17: Common reporting format (CRF) 2017 56

Table 18: Common reporting format (CRF) 2018 58

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 7

ABBREVIATIONS

AC Air conditioner

BAU Business-as-Usual

BMU German Federal Ministry for the Environment, Nature Conservation and Nuclear Safety

C4 Cool Contributions fighting Climate Change

CCD Cooling Degree Days

CCU Climate Change Unit

CFC Chlorofluorocarbons

DOE Department of Environment

EEI Energy Efficiency Index

EER Energy Efficiency Ratio

ERTLS Energy Research and Testing Laboratory Services

F-GAS Fluorinated gas

GCI Green Cooling Initiative

GDP Gross Domestic Product

GEF Grid Emission Factor

GHG Greenhouse gas

GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH

GWP Global warming potential

HVAC Heating, Ventilation and Air Conditioning

HEAT Habitat, Energy Application and Technology GmbH

HPMP HCFC phase-out management plan

HC Hydrocarbon

HCFC Hydrochlorofluorocarbon

HFC Hydrofluorocarbon

HFO Unsaturated HFC or Hydrofluoroolefin

IEA International Energy Agency

IKI International Climate Initiative

INDC Intended Nationally Determined Contribution

IPCC Intergovernmental Panel on Climate Change

LATL Lighting and Appliance Testing Laboratory

MAC Mobile Air Conditioning

MEPS Minimum Energy Performance Standard

MIT Mitigation scenario

MLF Multilateral Fund of the Montreal Protocol

8 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES

© tmal / pixabay

MRV Measuring, Reporting and Verification

Mtoe Million tons oil equivalent

MW Megawatt

NAMA Nationally Appropriate Mitigation Action

NDC Nationally Determined Contributions

NOU National Ozone Unit

ODP Ozone depleting potential

ODS Ozone depleting substances

RAC Refrigeration and air conditioning

SATBA Renewable Energy and Energy Efficiency Organisation

SEER Seasonal Energy Efficiency Ratio

UAC Unitary Air Conditioning

UNDP United Nations Development Program

UNEP UN Environment Progamme

UNIDO United Nations Industrial Development Organization

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 9

ACKNOWLEDGEMENTS

This report is the result of a comprehensive data collection and assessment process that has been carried out

since September 2017 within the project “Cool Contributions fighting Climate Change” (C4)* implemented by

Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH and funded by the German Federal Ministry

for the Environment, Nature Conservation and Nuclear Safety (BMU) under the International Climate Initiative (IKI).

The project aims to develop a greenhouse gas (GHG) mitigation strategy in the refrigeration and air conditioning

(RAC) sector as part of the Philippines’ Nationally Determined Contributions (NDCs), including establishing

parameters for increased energy efficiency in RAC technology, finding solutions for greener RAC technologies and

fostering their marketability and local manufacturing.

The GHG inventory provides a detailed profile of GHG emissions resulting from refrigeration and air conditioning

(RAC) in the Philippines and may serve as a basis for further development of emission reduction measures in the

RAC sector in contribution to the Philippine climate targets. It shall serve as a basis for further planning of the

Philippines’ NDCs and HFC phase-down schedules in contribution to the Montreal Protocol’s Kigali Amendment.

We would like to express our gratitude for the support of all the institutions, companies and other stakeholders

in the Philippines. The conduct of this inventory was led by the Environmental Management Bureau (EMB) of the

Department of Environment and Natural Resources (DENR). The DENR is the focal agency in the GHG inventory

and mitigation action in the Industrial Processes and Product Use (IPPU) sector of the Philippine inventory system

in line with Executive Order No. 174 in partnership with the Climate Change Commission (CCC) as National

Inventory compiler. We acknowledge the EMB leadership of Director Metodio U. Turbella and former Assistant

Director Jacqueline A. Caancan for their support.

The process was a learning experience for the DENR-EMB working on an integrated approach of ozone and

climate protection. Moreover, it was a new experience to work with other national government agencies given the

cross-cutting nature of the RAC sector compliance and enforcement.

We especially thank the Lighting and Appliance Testing Laboratory (LATL) of the Department of Energy (DOE)

Energy Research and Testing Laboratory Services (ERTLS) whose expertise and collaboration were indispensable

for the realization of this report. The development of a Minimum Energy Performance for RAC appliances is a

starting point in establishing a database for all RAC appliances in the Philippines, which hopefully would be a

valuable tool in succeeding RAC inventories in the near future.

* http://climate.emb.gov.ph/wp-content/uploads/2017/01/EO-174-National-GHG-Inventory.pdf

10 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINESSUMMARY

Summary of key findings »»Following the current climate trends, the predicted

temperature rise for the Philippines would be be-

Over the last few years, there has been a tremendous tween 0.8-2.0 °C by 2050 2 , coupled with more frequent

growth in the Philippine RAC industry. The growing pop- occurrence of heat waves and dry spells. Thus, the

ulation and climate warming have led to a continuously need for air conditioning and refrigeration will rise and

rising demand for air conditioning and refrigeration. the annual emissions in the Philippine RAC sector are

expected to increase up to 44.6 Mt CO2eq by the year

»»In 2017, the RAC sector was responsible for 24.7 Mt 2050 (see Figure 1). This amount of GHG emissions

CO 2eq of GHG emissions, constituting 18.0% of the equals approximately what 11.5 coal-fired power plants

Philippines’ overall energy-related emissions of would release in one year of operation 3 . With an ambi-

137 Mt CO2eq1. tious mitigation strategy, the emissions can be reduced

to 29.1 Mt CO2eq by the year 2050 (dotted “mitigation”

MIT curve).

50

45

40

35

30

Mt CO2eq

25

20

15

10

5

0

2010 2015 2020 2025 2030 2035 2040 2045 2050

■ UNITARY AIR CONDITIONING ■ CHILLER ■ MOBILE AIR CONDITIONING ■ DOMESTIC REFRIGERATION ■ COMMERCIAL REFRIGERATION

■ INDUSTRIAL REFRIGERATION ■ TRANSPORT REFRIGERATION ● ● ● TOTAL MIT EMISSIONS

FIGURE 1: PROJECTED BUSINESS-AS-USUAL (BAU) SCENARIO FOR GHG EMISSIONS IN THE RAC SECTOR UNTIL 2050 AND THE PREDICTED

MIT EMISSIONS

1 See https://publications.europa.eu/en/publication-detail/-/publication/41811494-f131-11e8-9982-01aa75ed71a1/language-en

2 Climate Impact Lab, 2018.

2 Assuming a coal power plant emitting ca 3.8 Mt CO2eq per year. https://www.epa.gov/energy/greenhouse-gas-equivalencies-calculator, last accessed 08.02.2019

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 1150

45

40

35

30

Mt CO2eq

25

20

15

10

5

0

2010 2015 2020 2025 2030 2035 2040 2045 2050

■ UNITARY AIR CONDITIONING ■ CHILLER ■ MOBILE AIR CONDITIONING ■ DOMESTIC REFRIGERATION ■ COMMERCIAL REFRIGERATION

■ INDUSTRIAL REFRIGERATION ■ TRANSPORT REFRIGERATION ● ● ● TOTAL MIT EMISSIONS

FIGURE 2: PROJECTED BUSINESS-AS-USUAL (BAU) SCENARIO FOR GHG EMISSIONS WITH THE KIGALI AMENDMENT IN THE RAC SECTOR UNTIL

2050 AND THE PREDICTED MIT EMISSIONS

The RAC sector has a large GHG mitigation potential »»Compared with the BAU scenario, 15.5 Mt CO 2eq can

with technologically and economically feasible mitigation be prevented by 2050 as shown in Figure 3, where mit-

actions. igation action regarding direct GHG emissions accounts

for 8.3 Mt CO2eq and indirect GHG emissions mitigation

contributes to a reduction of up to 7.2 Mt CO2eq.

50

■ DIRECT EMISSIONS

■ INDIRECT EMISSIONS

45

Total emmissions (Mt CO 2eq)

40

35

30

25

BAU scenario Unitary Air Air Mobile Air Domestic Commercial Industrial Transport

Conditioning Conditioning Conditioning Refrigeration Refrigeration Refrigeration Refrigeration

Chillers

FIGURE 3: MITIGATION POTENTIAL OF THE PHILIPPINE RAC SECTOR IN THE YEAR 2050. THE GREY COLOR OF THE FIRST COLUMN SHOWS THE

UNABATED EMISSIONS. THE NEXT COLUMNS TO THE RIGHT OF THE FIRST COLUMN SHOW THE EMISSION MITIGATION POTENTIAL OF EACH

SUBSECTORS BOTH FOR DIRECT (DARK BLUE) AND INDIRECT (LIGHT BLUE) EMISSIONS

12 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINESA large GHG mitigation potential lies in transitioning Figure 4 shows the RAC-related HFC consumption

refrigerants from highly climate-damaging hydro under the BAU scenario, the “freeze” in consumption

chlorofluorocarbons (HCFC) and hydrofluorocarbons and reduction steps under the Kigali Amendment adopted

(HFC) to alternatives with low global warming potential as “BAU-Kigali scenario” as well as the consumption

(GWP) in a timely manner, ahead of the current HFC according to a more ambitious mitigation scenario

phase-down schedule stipulated in the Kigali amendment (MIT), which assumes the application of best available

to the Montreal Protocol (Clark and Wagner, 2016). technologies and use of low-GWP refrigerants. The term

low-GWP refrigerants is applied for refrigerants with

GWP below 10.

10

9

8

7

6

Mt CO2eq

5

4

3

2

1

0

2015 2020 2025 2030 2035 2040 2045 2050

■ BAU ■ BAU-KIGALI ■ KIGALI SCHEDULE ■ MIT

FIGURE 4: BAU, THE BAU UNDER KIGALI AND MIT SCENARIOS OF HFC CONSUMPTION AND KIGALI SCHEDULE

Furthermore, the transition to low-GWP refrigerants This RAC inventory, which demonstrates direct, indirect

can bring other benefits besides the abatement of GHG and total GHG emissions in the RAC sector, is the first of

emissions. Such co-benefits are energy and cost savings its kind in the Philippines. As no data on RAC emissions

through improved energy efficiency as well as the crea- in the country were established prior to the compila-

tion of local employment through local manufacturing of tion of this RAC emission inventory, they are so far not

refrigerants and appliances. A reduced energy use also included in the Philippines’ Intended National Determined

contributes to the Philippines’ national energy security. Contributions (INDCs) to the Paris Agreement submitted

in 2015 4 . With the information provided with this inven-

tory, the Philippines will have a more robust RAC sector

emissions estimate as a basis for mitigation planning

and action as part of the Philippines’ NDCs.

4 https://www4.unfccc.int/sites/submissions/INDC/Published%20Documents/Philippines/1/Philippines%20-%20Final%20INDC%20submission.pdf

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 131 INTRODUCTION

In this chapter, we will discuss the general context »»BAU scenario considering the Kigali amendment,

of the project and the inventory, specifically address- referred to as “Kigali BAU”;

ing the relevance of the inventory of the RAC sector

to the national strategies on the Paris Agreement and »»potential market penetration of energy-efficient

the M

ontreal Protocol. We will then review the specific appliances using refrigerants with low global warming

climatic and market conditions in the Philippines and potential (GWP);

provide general information on its RAC sector, including

main stakeholders as well as RAC- and energy-related »»potential to mitigate GHG emissions from refrigerant

policies. This will serve as a background for further use and energy consumption in the RAC sector and its

detailed analysis of this sector’s current emissions and subsectors.

mitigation potential.

This report describes the RAC appliances currently avail-

able on the Philippine market, their energy consumption,

1.1 PROJECT FRAMEWORK the refrigerants used and the respective GHG emissions.

Currently used RAC technologies are compared with in-

The C4 project works among others closely with ternational best practice technologies in order to deter-

the following local authorities: the Climate Change mine the related emissions mitigation potential. Future

C ommission (CCC), the Department of Environment trends in each of the RAC subsectors are analysed with

and Natural Resources (DENR) with its Environmental respect to both BAU and mitigation (MIT) scenarios.

Management Bureau (EMB) of the Philippine Govern-

ment, the P hilippine Ozone Desk (POD), the Department

of E

nergy (DOE), the Department of Trade and Industry 1.2 IMPORTANCE AND BENEFITS OF

(DTI) and the Land Transportation Office (LTO). Close RAC SECTOR INVENTORIES

coordination among different entities and authorities

is essential to promote a coherent and sustainable Inventories that are based on an estimation of the stock,

development of the Philippine RAC sector. The full list i.e. the number of installed equipment in different RAC

of entities relevant to the project can be found in the subsectors, as well as average technical parameters

section 1.5. Additionally, Philippine industry associations per subsector provide a sound database and as such a

on heating, ventilation, air conditioning (HVAC), vocation- starting point for all GHG emission reduction activities

al training institutions such as the Technical Education and their monitoring.

and Skills Development A uthority (TESDA), as well as

refrigerant distributors and the petrochemical industry This equipment-based RAC GHG inventory provides the

(for information on possible local production of natural following information:

refrigerants) were involved in the project.

»»Sales and stock per subsector as well as growth rates

The purpose of this inventory is to provide an overview per subsector;

of the current state of GHG emissions of the RAC sector

in the Philippines. The report includes information on the »»technical data on systems, which determines their

following topics: GHG emissions such as average energy efficiency,

refrigerant distribution and leakage rates;

»»BAU GHG emissions resulting from refrigerant and

energy consumption of the RAC sector; »»GHG emissions on RAC unit basis;

14 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES© hpgruesen / pixabay

»»GHG emissions for the whole RAC sector including the Based on these advantages and different purposes, we

distribution between direct and indirect emissions; believe that the following Philippine stakeholders can

benefit from RAC inventories:

»»future projections of RAC-related GHG emissions;

»»The Climate Change Commission of the Philippines can

»»mitigation scenarios based on the introduction of integrate RAC sectoral mitigation targets into their

different technical options. climate mitigation strategies and in the regular climate

communication (National Communications and Biennial

The collected information can be used for the following Update Reports);

purposes:

»»The Department of Environment and Natural Resources

»»To identify key subsectors with the highest GHG (DENR) will be able to control GHG emissions and

emissions as well as the highest emission reduction start mitigation planning as well as UNFCCC reporting

potential based on available technologies; on HFCs. The methodology and information provided

through this inventory can be used to support the

»»to support country-wide GHG emission inventories that F-gas reporting included in the National Communica-

can be used for reporting under the UNFCCC. Based on tions and Biennial Update Report;

the projections, they indicate how GHG emissions will

develop in the future. Sectoral RAC mitigation plans »»The Department of Energy (DOE) will be able to

based on GHG inventories and GHG emission projections develop and track a national product database for

can support the development of NDC targets; continuous monitoring, reviewing and updating RAC

equipment related MEPS and labels.

»»to provide planning tools for mitigation action, such

as the formulation of Minimum Energy Performance »»the RAC industry can gain understanding of the

Standards (MEPS) and labelling or bans on refrigerants national development of the RAC sector regarding its

with high-GWP; carbon footprint in order to develop product and sales

strategies consistent with the required low carbon

»»to give an indication of the impact of legislation on development;

stakeholders in different subsectors;

»»the Department of Trade and Industry (DTI) will benefit

»»to form the basis for a Measuring, Reporting and using this report during development of RAC related

Verification (MRV) system or a product database; testing standards on product safety;

»»to support the development of climate finance project »»the Department of Finance (DOF) including Government

proposals with the aim of reducing GHG emissions in Financial Institutions (GFIs) and private banks can

the RAC sector, such as Nationally Appropriate Mitigation develop financial mechanisms and incentives for the

Actions (NAMAs). transition to low carbon strategies;

»»vocational training institutions (e.g. TESDA) can

integrate low carbon technology practices into their

training plans and training curricula.

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 151.3 CURRENT CLIMATE AND ECONOMIC Due to the hot temperatures throughout the year, the

STATUS Philippines has a high demand for cooling technologies.

The need for cooling increases during the months of

The Republic of the Philippines is an island country May to November with hot and humid months.

in Southeast Asia, which consists of more than 7,600

islands. It is in the Pacific Ring of Fire and has an area With higher global temperatures, the number of Cooling

of 300,000 km² and a population of 103.3 5 million (as Degree Days (CDDs) in the Asian region will increase be-

of 2016). Most of the mountainous land area is covered tween 30% and nearly 100% by 2100 under the climate

with tropical rainforest, the climate is dominated by a reference scenarios RCP2.5 and RCP8.5, respectively

rainy season and a dry season. The summer monsoon (Hasegawa et al., 2016). With rising temperatures, not

brings heavy rains from May to October. Contrasting only the air conditioning sector will face challenges, but

the winter monsoon, where colder and drier air dom- also the demand for food cooling is expected to rise.

inates from December to February. The mean annual

temperature in Manila is 27.3°C with about 1.800 mm

precipitation (Figure 5). 1.4 ENERGY PRODUCTION, ENERGY

CONSUMPTION AND OTHER FACTORS

INFLUENCING THE GROWTH OF RAC

APPLIANCES

The demand for RAC appliances in the Philippines is

growing continuously with multiple factors driving this

growth (Oppelt, 2013), as listed in Table 1 below. The

growing population and number of households leads

to an increased demand for more appliances on the

market. The high GDP growth rate indicates general

economic growth, which coupled with increasing de-

mand and growing urbanisation increase the sales in the

sector. The current number of households can also give

a realistic general guidance on how many appliances

such as ACs and domestic refrigerators are in use by

the end users. The current total electricity consump-

tion in the country can be compared to the equivalent

consumption in different mitigation scenarios and thus

the potential contribution of the RAC sector to the total

country emissions abatement in case of the introduction

on nationwide programs.

FIGURE 5: CLIMATE CHART OF MANILA.

SOURCE: COMPILED BY WWW.KLIMADIAGRAMME.DE

SOURCE: NATIONAL CLIMATIC DATA CENTRE (NCDC)

5 https://www.iea.org/countries/Philippines/

16 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINESTABLE 1: STATISTICAL DATA OF THE PHILIPPINES 6 15.1%

26.1%

STATISTICS OR THE PHILIPPINES VALUE

POPULATION (MILLION) 103.3 17.7%

TOTAL :

POPULATION GROWTH RATE (2010–2015)7 1.72 54.8 Mtoe

HOUSEHOLDS (MILLION)8 22.42 1.3% 18.9%

6.0%

URBANISATION (2015-2020) [%]9 1.99

14.9%

GDP GROWTH RATE10 6.7%

ENERGY PRODUCTION (MTOE) 28.5 ■ COAL ■ CRUDE OIL ■ OIL PRODUCTS ■ NATURAL GAS

■ HYDRO ■ GEOTHERMAL ■ BIOFUELS/WASTE

TOTAL PRIMARY ENERGY SUPPLY

(TPES, MTOE) 54.8

FIGURE 6: TOTAL PRIMARY ENERGY SUPPLY (TPES) FOR THE

PHILIPPINES FOR THE YEAR 2016, MTOE = MILLION-TONS OIL

ELECTRIC CONSUMPTION (TWH) 82.5 EQUIVALENT12

CO2 EMISSIONS (MT CO2)11 137

1.4% 3.6%

Most of the Philippines energy is generated from oil and 24.1%

12.2%

oil products (33.8%), coal (26.1%), geothermal, solar and

other renewables (19%) as well as biofuel and waste

(17.7%). The other energy sources (natural gas and

TOTAL :

hydro) supply 7.3%, being minor contributors to the total 31.6 Mtoe

primary energy supply (TPES, see Figure 6).

36.2%

22.5%

Approximately two third of Philippines’ total energy is

consumed by the industry (25%) and the transport (38%)

sector (Figure 7).

■ INDUSTRY ■ TRANSPORT ■ RESIDENTIAL ■ COMMERCIAL

■ AGRICULTURE/FISHING ■ NON-ENERGY USE

FIGURE 7: ENERGY CONSUMPTION BY SECTOR, MTOE = MILLION

TONS OIL EQUIVALENT12

6 https://webstore.iea.org/download/direct/2291?fileName=Key_World_2018.pdf

7 http://psa.gov.ph/population-and-housing

8 http://www.psa.gov.ph/content/housing-characteristics-philippines-results-2015-census-population

9 https://population.un.org/wup/DataQuery/

10 World Bank

11 See https://publications.europa.eu/en/publication-detail/-/publication/41811494-f131-11e8-9982-01aa75ed71a1/language-en

12 https://www.iea.org/statistics/?country=PHILIPPINE&year=2016&category=Energy%20supply&indicator=TPESbySource&mode=table&dataTable=BALANCES

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 171.5 RAC STAKEHOLDERS

Table 2 provides an overview of the Philippines’ key

institutions from private and public domains relevant for

the climate and energy conservation policy in the RAC

sector as well as key non-state institutions and stake-

holders in the sector.

TABLE 2: OVERVIEW OF INSTITUTIONS RELEVANT FOR THE RAC SECTOR AND THEIR CONTRIBUTION TO THE SURVEY

INSTITUTION/DEPARTMENT DUTIES/FUNCTIONS/RESPONSIBILITIES

THE CLIMATE CHANGE COMMISSION The Climate Change Commission (CCC) is an independent and autonomous

government body. The CCC is under the Office of the President and is the “sole

policy-making body of the government which shall be tasked to coordinate, monitor

and evaluate the programs and action plans of the government relating to climate

change”. The CCC is the political partner for the implementation of the C4 projects

in the Philippines.

ENVIRONMENTAL MANAGEMENT The DENR with its EMB, which has administrative jurisdiction over the POD

BUREAU/DEPARTMENT OF ENVIRON- (below) and its Climate Change Division (CCD), is responsible for the calculation of

MENT AND NATURAL RESOURCES (EMB/ refrigerant related emissions and their management in the Philippines; As mandated

DENR) under Executive Order 174, the Department of Environment and Natural Resources

(DENR) shall take the lead in the GHG Inventory in the Industrial Processes and

Product Use (IPPU). GHG emissions from RAC&F is a one of the IPPU categories as

defined by the IPCC.

DENR is an implementation partner for the C4 project.

THE PHILIPPINE OZONE DESK (POD) AT The POD is the national coordinating body of the Montreal Protocol for the

DENR Philippines with the mandate to manage chemical refrigerants. It has managed the

chlorofluorocarbon (CFC) phase out plan and is currently managing the hydrochloro-

fluorocarbon (HCFC) phase-out plan. The POD is also in charge in managing issues

related to the management of hydrofluorocarbon (HFC) under the Kigali Amendments,

where the ratification of the Philippines is pending. The POD coordinates policies and

climate strategies coordination related to the GHG management of refrigerants,

including national GHG emissions reporting and related inputs to the NDC.

DEPARTMENT OF FINANCE (DOF)/ • Reporting on imports of regulated substances (so far CFCs and HCFCs)

BUREAU OF CUSTOMS (BOC) • Provided the information on codes for appliances

DEPARTMENT OF AGRICULTURE (DA)/ • Provided information on cold store warehouses

NATIONAL MEAT INSPECTION AUTHORITY

DEPARTMENT OF ENERGY (DOE) • Responsible for ensuring energy security of the Philippines. Implements the

renewable energy act and energy efficiency programs. It is an implementing

partner for the project;

• The Lighting and Appliances Testing Laboratory at the Energy Research and Testing

Laboratory Services (ERTLS) and Energy Utilization Management Bureau (EUMB)

provided information on the unitary air conditioning and refrigeration sector

DEPARTMENT OF TRADE AND • Responsible for developing and promoting standards and certification;

INDUSTRY (DTI)/ BUREAU OF PHILIPPINE • Responsible for import licenses;

STANDARDS (BPS)

• Provided the records related to the issuance of certificates for imported units and

certification marks for locally manufactured RAC-equipment

• Provided the information on codes for appliances

DEPARTMENT OF TRANSPORTATION • Responsible for all land transportation in the Philippines, the implementation of

(DOT)/LAND TRANSPORTATION OFFICE transportation laws, rules and regulations;

(LTO)

• Provided data on registered motor vehicles

• Also acted as partner for data on mobile air conditioning and transport

r efrigeration, with assistance of the Philippine Ozone Desk Multilateral Fund (POD

MLF).

18 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINESTABLE 2: OVERVIEW OF INSTITUTIONS RELEVANT FOR THE RAC SECTOR AND THEIR CONTRIBUTION TO THE SURVEY

INSTITUTION/DEPARTMENT DUTIES/FUNCTIONS/RESPONSIBILITIES

PHILIPPINE STATISTICS AUTHORITY Census of Philippine Business and Industry

COLD CHAIN ASSOCIATION OF THE • Establishing formal linkages with the government and delineating the role of the

PHILIPPINES private business sector in the food security and development program;

• Spearheading the formulation, promulgation and enforcement of industry standards

necessary to ensure efficient performance of all activities within the cold chain;

and

• Fostering cooperation and coordination among members in addressing industry

concerns, particularly those that pertain to industry development.

PHILIPPINE ASSOCIATION OF BUILDING Internationally affiliated, accredited and the only recognized Association in the

ADMINISTRATORS Philippine Building Management Industry

PHILIPPINE GREEN BUILDING INITIATIVE Non-profit, voluntary group of professional associations involved with the built-

environment who share a common concern on the impacts of global warming and

climate change.

ASHRAE PHILIPPINE CHAPTER An international organization with mission of advancing heating, ventilation, air

conditioning and refrigeration to serve humanity and promote a sustainable world

through research, standards writing, publishing and continuing education.

PHILIPPINE SOCIETY OF VENTILATION; Non-stock, non-profit organization of engineers, consultants, contractors, suppliers

AIR CONDITIONING AND REFRIGERATION and manufacturers directly involved in air-conditioning, ventilating and refrigerating

ENGINEERS (PSVARE) practices.

REFRIGERATION AND AIR CONDITIONING RACTAP is an organization of refrigeration and air conditioning technicians providing

TECHNICIANS ASSOCIATION OF THE training and support to professional RAC technicians.

PHILIPPINES (RACTAP)

1.6 CLIMATE AND F-GAS POLICIES the annual import quotas for HCFCs consistent with the

phase-out schedule of the Montreal Protocol, approves

Regulatory frameworks are required for the implementation importers, and issues import quotas to registered im-

of most changes towards environment-friendlier technology porters in coordination with the Bureau of Customs.

alternatives in the RAC sector. The Philippines signed the

Montreal Protocol on Substances that Deplete the Ozone Policies targeting the RAC sector so far are mainly

Layer on Sept. 14, 1988 and ratified it on March 21, 1991. driven by ODP management under the HPMP.

So far, the Philippines has been compliant with the

Montreal Protocol. The current NDC, which is still under development with

key stakeholders, includes an economy wide target of a

Stage I of the HCFC phase-out management plan (HPMP) 70% reduction of GHG emissions by 2030 compared to

for the Philippines was approved at the 68th meeting to BAU213 . Whilst the NDC states this as an economy-wide

accomplish the 10 per cent reduction from the baseline target, so far, no specific quantitative targets for the

by 2015 resulting in the phase-out of 45.0 ODP tonnes of RAC sector or its subsectors have been included in the

HCFCs. At the 79th meeting, on behalf of the Government of NDC. Discussions for the NDC update 2020 covered en-

the Philippines, the World Bank, as the designated imple- ergy efficiency measures for home appliances, including

menting agency, submitted a request for funding for stage refrigerators and air conditioners, the transition to low

II of the HPMP. The Environmental Management Bureau GWP refrigerants and the enforcement of the building

(EMB) through the Philippine Ozone Desk (POD) establishes code 14 .

13 https://www4.unfccc.int/sites/submissions/INDC/Published%20Documents/Philippines/1/Philippines%20-%20Final%20INDC%20submission.pdf

14 See http://www.climate.gov.ph/images/NDC/Sofitel/02_PH-NDC_Liza-Andres.pdf last accessed 12.02.2019

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 192 SCOPE OF THE INVENTORY

The inventory covers GHG emissions from the RAC sector TABLE 3: RAC SUBSECTORS AND RELATED SYSTEMS

based on a stock model covering the major RAC sub

sectors and their appliances. The current and future SUBSECTOR SYSTEMS

stock is derived from historic sales figures, while

historic growth trends and dynamics help to determine

UNITARY AIR Window-type air conditioners

the future stock. The emissions are calculated for each CONDITIONING Split residential air condi-

subsector and appliance type based on critical technical tioners

parameters determining direct and indirect emissions. Split commercial air condi-

tioners

The inventory covers the following elements: Duct split residential air

conditioners

»»The calculated mitigation potential of the RAC sector Commercial ducted splits

of the Philippines using the guidelines of the Inter Rooftop ducted

governmental Panel on Climate Change (IPCC); Multi-splits

CHILLERS Air conditioning chillers

»»for each of the subsectors and their respective

appliance types (Table 3), an inventory of historic and MOBILE AIR Car air conditioning

future unit sales and stock data is established; CONDITIONING Large vehicle air conditioning

»»for each appliance type, the historic, current and DOMESTIC Domestic refrigerators

future energy and refrigerant use and their respective REFRIGERATION

emissions are estimated; COMMERCIAL Stand-alone equipment

REFRIGERATION Condensing units

»»currently deployed RAC technologies are compared Centralized systems for

with international best practice technologies for their supermarkets

potential to mitigate GHG emissions on a unit basis;

»»Future trends of RAC subsectors are analysed both

with respect to BAU and mitigation scenarios. This document presents preliminary results based on

statistical data, questionnaires, interviews, workshop

The RAC subsectors and all appliances covered by the feedback, methodology and assumptions.

inventory are categorized according to key subsectors as

outlined in the RAC NAMA Handbook, Module 1: Inventory Future projections have been included, mostly using

(Heubes and Papst, 2014) and further illustrated in Table growth rates based on expert judgements or economic

25 and Table 26 of the Annex. growth projections.

As outlined in the methodology below, the inventory

is based on actual emissions gathered at the unit or

appliance level. This methodology is also applied for the

calculation of appliance related refrigerant emissions

as opposed to inventory methodologies based on the

bulk refrigerant consumption across different sectors.

The latter approach is usually applied for estimating

emissions as part of ozone depleting substances (ODS)

alternative surveys.

20 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES© FreePhotos / pixabay

2.1 METHODOLOGY

The methodology adopted for the report draws on the

concepts outlined by Heubes et al. (Heubes and Papst,

2014), Penman et al. (2006) and on the IPCC Tier 2 TIER 1 TIER 2

methodology from 2006. It should be noted that the

word ‘system’ is used interchangeably in this report

with the words ‘appliance’, ‘equipment’ or ‘unit’.

Potential emission

i A t emission

Actual

While alternative refrigerant inventories, such as ODS

alternative surveys, are typically based on the Tier 1

methodology, this inventory is based on the IPCC

Tier 2 methodology to cover not only refrigerant-related

emissions and their mitigation options, but also GHG consumption often Activities leading to

emissions from energy use and their mitigation o ption. aggregated on entire emissions disaggregated

country on subsector basis

In addition, the Tier 2 methodology allows for the prepa-

ration of GHG mitigation actions (such as NAMAs) in

relevant RAC subsectors and further NDC development

and review. As Tier 2 inventories are based on unit

appliances, an MRV system of mitigation efforts can be Number of appliances &

established at the unit level. technical parameters

Tier 1 and Tier 2 methodologies have the following basic

differences15:

ODS alternatives UNFCCC Common Reporting

survey under the MP Format - Category 2:

»»Tier 1: emissions are calculated based on an

aggregated sector-based level (Heubes and Papst, Industrial Processes

Reporting under and Product Use:

2014; Penman, 2006).

Article 7 of MP

Refrigeration/AC and Foam

»»Tier 2: emissions are calculated based on a

disaggregated unit-based level (Heubes and Papst,

2014; Penman, 2006). Approaches for Refrigerant

Direct Emissions distribution

The difference between the Tier 1 and Tier 2

methodology are further illustrated in Figure 8. Graphic Key

Mitigation action planning

Approaches in contribution to NDCs

Data used for

for estimates (e.g. NAMA)

Figure 8: Approaches for

GHG emission

estimates relevant indirect direct

to the RAC&F emissions emissions

sector

15 Please note that sector and application here are used in the context of this report, FIGURE 8: APPROACHES FOR GHG EMISSION ESTIMATES RELEVANT

where IPCC 2006 methodology refers to sector as application and application as

sub-application TO THE RAC&F SECTOR (MUNZINGER ET AL., 2016)

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 21© Sunti / Shutterstock.com

The Tier 2 methodology used in this report accounts for include refrigerant emissions from leakage of refrigerant

direct and indirect emissions at the unit level as illus- gases during manufacture, servicing, operation and at

trated in Figure 9 for the stock of appliances in use, end-of-life of cooling appliances. The Tier 2 methodology

their manufacturing and disposal emissions. Indirect goes beyond the Tier 1 approach, which only focuses on

emissions result from electricity generation for cooling, the demand and use of refrigerants. The Tier 1 approach

considering the annual electricity consumption and the does not include indirect emissions from the energy use

Philippines’ grid emission factor (GEF). Direct emissions of appliances.

Production of

Appliances Stock (= Appliances in Use) -> Bank

(First Fill)

Manufacture In-Use Disposal Energy

Emissions Emissions (Refill) Emissions Consumption

Fill Refill Direct Emissions Indirect Emissions

Demand Total Emissions

FIGURE 9: OVERVIEW RAC REFRIGERANT DEMAND VERSUS RAC TOTAL EMISSIONS

22 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINESRefrigerant consumption is accounted for at all stages »»Secondary data was used from Department of Energy -

during the product life of the equipment: Lighting and Appliance Testing Laboratory (DOE-LATL17,

ASEAN-Shine18 , BRG Building Solutions19 and from the

»»Refrigerants that are filled into newly manufactured Department of Environment and Natural Resources -

products Environmental Management Bureau (DENR-EMB) 20

HPMP Baseline Survey. Some data was aggregated from

»»Refrigerants in operating systems (average annual World Air Conditioner Demand by Region Report from

stocks) The Japan Refrigeration and Air Conditioning Industry

Association (JRAIA, 2018)21. Data for the mobile AC

»»Refrigerants remaining in products at decommissioning subsector was taken from the Land Transportation Of-

fice (LTO) 22 . The data was compared and updated with

data from the Philippines Room Air Conditioner Market

2.2 DATA COLLECTION PROCESS Assessment and Policy Options report (CLASP, 2019)23 .

The following steps were taken to complete the inventory: »»Tertiary data was used to fill gaps, where other data

was not available. The stock number of the domestic

Step 1. National kick-off workshop with relevant stake- and the commercial subsector (e.g. stand-alone units,

holders on 27th of September 2016. condensing units and centralized systems for super-

markets were inserted based on estimates carried out

Step 2. Preparation of questionnaires and list of stake- in the GCI Database 24 (‘Green Cooling Initiative’, 2013).

holders for selected subsectors. Detailed questionnaires

were prepared for manufacturers in the sub-sectors AC The following challenges were encountered during data

and domestic refrigeration. collection for this inventory from primary data resources:

Step 3. Sending questionnaires to stakeholders. »»Reluctance to provide information or willingness

to provide only partial information due to the

Step 4. Face-to-face interviews with stakeholders to confidentiality policy of the companies.

explain the required data.

»»Difficulties with filling out questionnaires on the part

Step 5. Validation checks of primary data and gathering of the companies; questionnaires had to be explained

of complementary information from secondary and ter- during personal visits to get information.

tiary data, call-backs and compilation of data received

through questionnaires into the master sheets from data »»No customs data on imported equipment or car

entry forms. registration records could be collected.

Step 6. Verification of data during a national inventory »»Despite multiple feedback loops, the attribution of

workshop in Manila on the 29th of May 2018. collected equipment data to the appliance groups

defined in the inventory was difficult. Some appliance

»»For primary data, a survey was conducted among groups such as self-contained AC were left empty. It

manufacturers of unitary AC and domestic refrigeration is assumed that those categories are included in other

equipment such as Kolin, LG, Concepcion Carrier and groups, but this could not be verified.

Daikin. Manufacturers were contacted individually or

through associations, four of them provided data16 . The Due to those difficulties, the primary data collected

domestic refrigeration subsector was supplemented by was found incomplete and estimates from s takeholders

data from the GCI Database (‘Green Cooling Initiative’, were often used instead of the collected data. The assump-

2013). tions are presented in detail in the following chapters.

16 A complete list of approached and responding companies is provided in the Annex

17 https://www.doe.gov.ph/ertls

18 https://storage.googleapis.com/clasp-siteattachments/ASEAN_SHINE_AC_Regional_Roadmap__Report_Final-new-2.pdf

19 http://www.brgbuildingsolutions.com/industry-sectors/air-conditioning-heating-ventilation-market-research-reports-data

20 https://emb.gov.ph/

21 https://www.jraia.or.jp/english/World_AC_Demand.pdf

22 http://www.lto.gov.ph/

23 https://clasp.ngo/publications/philippines-rac-market-assessment-and-policy-options-analysis-2019

24 http://www.green-cooling-initiative.org/

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 232.3 MODELLING PARAMETERS and information from interviews where possible. Gaps

were filled with default values obtained from the Green

For the analysis of this inventory the modelling Cooling database. The major stakeholders consented to

parameters derived from primary and secondary data the preliminary data, but it is important to note that

collection as shown in Table 4 were applied. The this is mainly due to the lack of comparison data in the

modelling parameters are derived from questionnaires Philippines.

TABLE 4: MODELLING PARAMETERS FOR BAU SCENARIO

EQUIPMENT TYPE LIFETIME MAIN INITIAL EER SERVICE DISPOSAL

[YEARS] REFRIGERANTS CHARGE (IC) (2017) EMISSION EMISSION

[KG] FACTOR25 FACTOR

[% OF IC] [% OF IC]

WINDOW TYPE AC 8 R410A, R22, 0.8 3.29 10% 95%

R32

SPLIT RESIDENTIAL AC 8 R410A, R22, 0.65 3.5 10% 95%

R32

SPLIT COMMERCIAL AC 10 R410A, R22 2.9 3.15 10% 80%

ROOFTOP DUCTED 10 R22, R407C, 2 3.38 5% 75%

R410A

MULTI-SPLITS 15 R22, R407C, 3.325 3.27 10% 80%

R410A

AIR CONDITIONING CHILLERS 20 R134a, R123 35 2.79 22% 95%

CAR AIR CONDITIONING 15 R134a 0.6 2.71 20% 100%

LARGE VEHICLE AIR CONDITIONING 15 R134a 8 2.71 30% 80%

DOMESTIC REFRIGERATION 20 R134a, R600a 0.175 1.42 2% 80%

STAND-ALONE EQUIPMENT 15 R134a 0.8 1.42 3% 80%

CONDENSING UNITS 20 R134a 4 2.21 30% 85%

CENTRALIZED SYSTEMS FOR 20 R22, R134a 230 1.73 38% 90%

SUPERMARKETS

The grid emission factor (GEF) is a measure of CO 2 No substantial indications from industry representatives

emission intensity per unit of electricity generation in were provided for the future growth rates of appliances.

the total grid system. In the presented study the GEF of Therefore, growth rates are derived from the historic

0.63 26 has been used. As there are no future predictions growth rates and trends were conservatively applied for

of a potential GEF, which can be implemented in the modelling future unit sales in the respective subsectors

model, the data presented in this report uses the same as listed in Table 5.

GEF for the BAU and the MIT scenario.

25 Values taken from http://www.green-cooling-initiative.org and modified according stakeholder/industry consultation

26 https://pub.iges.or.jp/pub/list-grid-emission-factor

24 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES© GIZ / Proklima

TABLE 5: ASSUMED FUTURE GROWTH RATES OF APPLIANCE SALES

SUBSECTORS APPLIANCE TYPES 2016-2020 2021-2030 2031-2050

UNITARY AIR CONDITIONING Window-type air conditioners 4.5% 2.3% 0.6%

UNITARY AIR CONDITIONING Split residential air 7.5% 5.0% 3.3%

conditioners

UNITARY AIR CONDITIONING Split commercial air 7.5% 2.5% 0.6%

conditioners

UNITARY AIR CONDITIONING Rooftop ducted 7.5% 2.5% 0.6%

UNITARY AIR CONDITIONING Multi-splits 4.5% 1.5% 0.3%

CHILLERS Air conditioning chillers 1.7% 0.6% 0.1%

MOBILE AIR CONDITIONING Car air conditioning 2.5% 0.8% 0.2%

MOBILE AIR CONDITIONING Large vehicle air conditioning 1.2% 0.4% 0.1%

DOMESTIC REFRIGERATION Domestic refrigeration27 2% 2% 2%

COMMERCIAL REFRIGERATION Stand-alone equipment 1.7% 0.6% 0.1%

COMMERCIAL REFRIGERATION Condensing units 1.7% 0.6% 0.1%

COMMERCIAL REFRIGERATION Centralized systems for 1% 0.3% 0.1%

supermarkets

COMMERCIAL REFRIGERATION Centralised supermarket units 3.2% 0.4% 0.1%

Growth is estimated using CAGR between 2018 and 2050

27

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 253 RESULTS

3.1 SUBSECTOR SALES AND 3.1.1 UAC sales and stock data

STOCK DATA ANALYSIS

The total sales of unitary air conditioning appliances

The data was acquired and analysed by subsectors have been steady, with a rising trend in the last years

according to the classification presented in section 2.2; and current amounts of over 800,000 units a year. The

the results are presented and described below. biggest sales share are window type air conditioners,

followed by split residential air conditioners. In the near

The process of secondary data collection and review future it is assumed that the split air conditioners will

targeted both locally manufactured and imported be the technology of choice in the Philippines.

equipment. The sales and stock development in the

key subsectors were examined. The stock analysis

considers the phase-in of new equipment driven by the

sales d

evelopment and the phase-out of old equipment

considering standardised assumptions for the lifetime

of the equipment.

900.000

800.000

700.000

600.000

Sold units

500.000

400.000

300.000

200.000

100.000

0

2010 2012 2014 2016

■ WINDOW-TYPE AIR CONDITIONERS ■ SPLIT RESIDENTIAL AIR CONDITIONERS ■ SPLIT COMMERCIAL AIR CONDITIONERS

■ ROOFTOP DUCTED ■ MULTI-SPLITS

FIGURE 10: UNITARY AC UNITS SOLD (2010 TO 2016)

26 REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES© terimakasih0 / pixabay

16

14

12

Stock units (millions)

10

8

6

4

2

0

2010 2015 2020 2055 2030 2035 2040 2045 2050

■ WINDOW-TYPE AIR CONDITIONERS ■ SPLIT RESIDENTIAL AIR CONDITIONERS ■ SPLIT COMMERCIAL AIR CONDITIONERS

■ COMMERCIAL DUCTED SPLITS ■ ROOFTOP DUCTED ■ MULTI-SPLITS

FIGURE 11: UNITARY AC UNIT STOCK HISTORIC AND FORECASTED (2010 TO 2017; 2018 TO 2050)

The stock model shows that there are currently around 3.1.2 AC chillers sales and stock data

7 million appliances on the Philippine market and rapid

growth of the stock is expected starting from year 2025, According to the acquired data, a significant increase in

assumedly due to the phase-in of new appliances and the numbers of chillers has been observed in the last 3

increase in local production/manufacturing. The current years.

breakdown by appliances

■ WINDOW-TYPE is shown ■inSPLIT

AIR CONDITIONERS Figure 11. AIR CONDITIONERS ■ SPLIT COMMERCIAL AIR CONDITIONERS

RESIDENTIAL

■ COMMERCIAL DUCTED SPLITS ■ ROOFTOP DUCTED ■ MULTI-SPLITS

TABLE 6: SOLD UNITS FOR THE AC CHILLER SUBSECTOR FOR THE YEARS 2010 TO 2015

SUBSECTOR 2010 2011 2012 2013 2014 2015 2016

AC CHILLERS 290 330 310 340 370 400 450

REFRIGERATION AND AIR CONDITIONING GREENHOUSE GAS INVENTORY FOR THE PHILIPPINES 27You can also read